WSWA Monthly Market Commentary

WSWA Monthly Market Commentary for January 2019

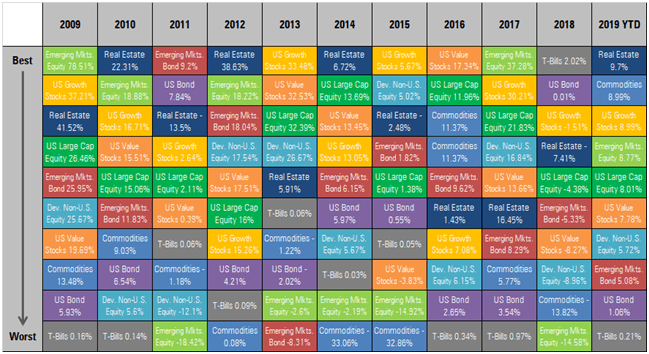

Key Takeaways

- All major asset classes were up strongly in January, one of the best yearly starts in recent memory, despite the month-long partial government shutdown in the U.S. and continuing uncertainty internationally about the economic impact of trade tariffs and the U.K. ‘Brexit’ negotiations

- Global real estate took the lead with a monthly return of 9.7%, followed by commodities and U.S. growth stocks at 9% each. The S&P 500 posted an 8% return for the month

- Recession fears in the U.S. receded as job growth was strong despite the unemployment rate edging up to 4%;Corporate profits continued to grow in the 4th quarter of 2018, though will slow in 2019

- Fears of a recession due to rising interest rates diminished with Federal Reserve officials holding short-term rates steady at their January meeting and commenting on being ‘patient’ with future rate increases

What a way to start the year!

All major asset classes were up strongly in January, one of the best yearly starts in recent memory, despite the month-long partial government shutdown in the U.S., continuing uncertainty about trade tariffs’ impact on international growth, and the failure of U.K. ‘Brexit’ negotiations.

Global real estate took the lead among major asset classes with a monthly return of 9.70%, followed by commodities and U.S. growth stocks at 8.99% each. The S&P 500 gained 8.01% for the month, with emerging markets equities up 8.77% and developed international equities up 5.72%. U.S. bonds also had a strong month, rising 1.06%.

Source: Morningstar Direct

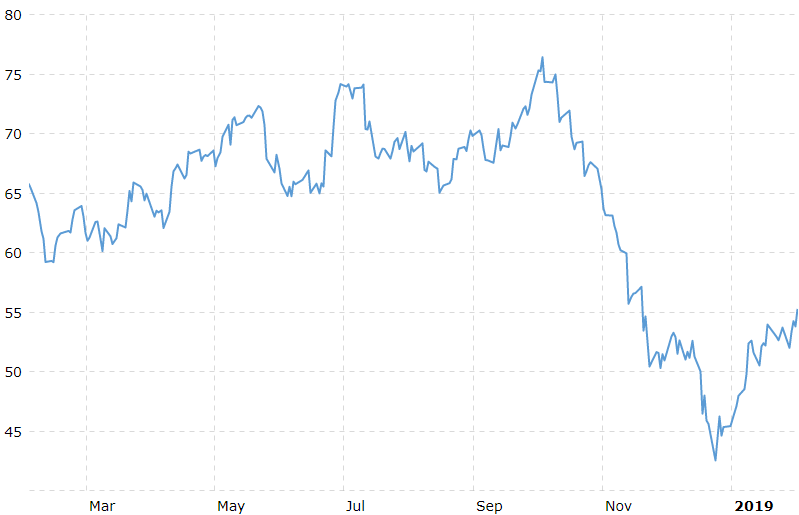

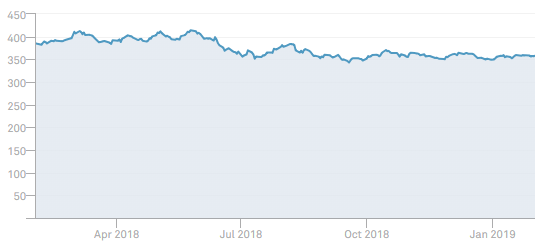

Among commodities, crude oil prices led the way with a strong rebound from the December 24th low of $42.53, ending the month at $53.79. The S&P GSCI Agriculture index, the second largest component of the S&P GSCI index, stabilized after declining steadily in recent years[1].

West Texas Crude Oil Price

Source: www.macrotrends.net

GSCI Agriculture Index

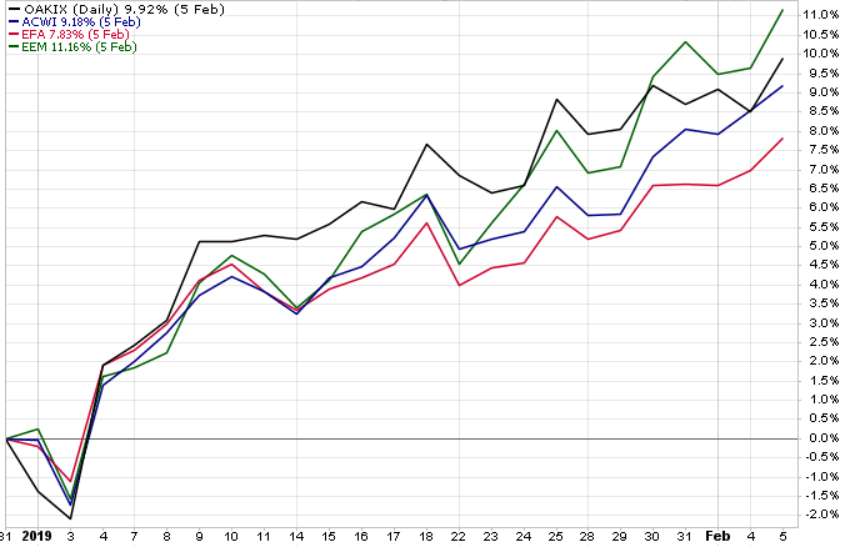

International equity markets are well priced for future growth.

Emerging Markets equities (EEM) led the international equity markets in January, followed by the MSCI All Country World Index (ACWI), with Europe, Australasia, and Far East (EAFE) markets not far behind.

[1]https://us.spindices.com/indices/

European markets posted solid returns despite Prime Minister Theresa May’s Brexit plan being voted down by Parliament. After the Brexit agreement was rejected, Prime Minister May survived a ‘no confidence’ vote and promised renewed efforts to negotiate an acceptable exit plan with European Union leadership.

According to Harris Associates, manager of the Oakmark International fund, international markets have been the victim of “overly emotional equity markets” in recent months[2] and U.K. businesses are generating the highest percent free cash flow in the world (6%[3]). Prominent companies such as Daimler, Lloyds, and Tencent are trading at significant discounts to intrinsic value, and the Oakmark International portfolio has a Price/Cash Flow ratio of 4.8x compared to 7.5x for the world, indicating the shares held in the fund are priced significantly lower than the world markets.

Oakmark International, MSCI ACWI, EAFE, and Emerging Markets Equity Returns

Source: https://stockcharts.com/h-perf/ui

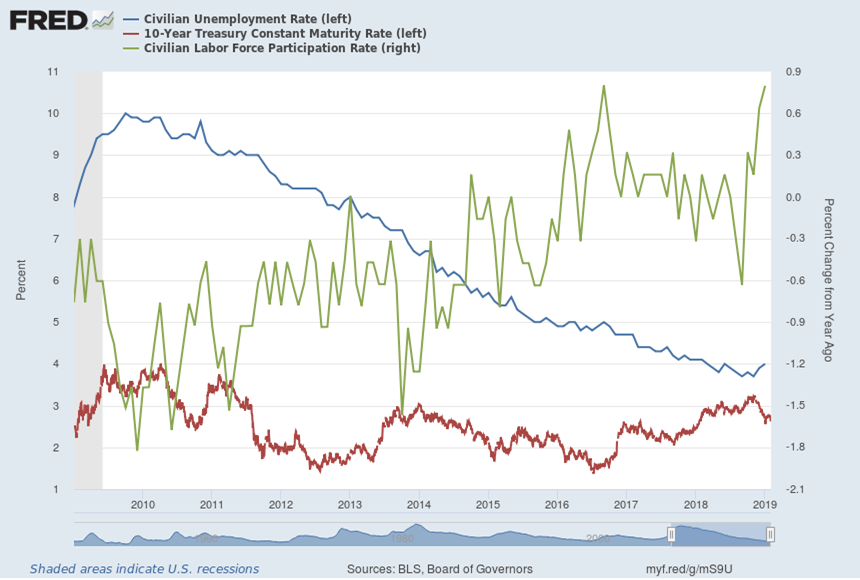

Worries about a near-term recession in the U.S. receded as corporate earnings continued to grow in the 4th quarter of 2018 and employers added more new jobs than expected.

Unemployment in the U.S. remained near historic lows, edging up to 4%[4] due to the temporary addition of government workers furloughed during the partial government shutdown. The labor participation rate continued to increase slowly and job creation exceeded expectations in January with 304,000 jobs added[5].

Fears of rising interest rates derailing the U.S. economy diminished with Federal Reserve officials holding short-term rates steady at their January meeting and commenting on being ‘patient’ with future interest rate increases[6].

[2]https://www.im.natixis.com/us/markets/finding-value-in-overly-emotional-equity-markets

[3] As presented Natixis National Sales Meeting January 10, 2019 Source: Corporate Reports, Empirical Research Partners Analysis as of November 30, 2018. Excluding financials and utilities; data smoothed on a trailing six-month basis.

[4]https://www.wsj.com/articles/global-stocks-edge-up-after-a-january-surge-in-the-u-s

[5]https://www.bls.gov/news.release/empsit.nr0.htm

[6]https://www.federalreserve.gov/monetarypolicy/fomcpresconf20190130.htm

U.S. Unemployment Rate, Participation Rate, and 10-yr. Treasury Yield

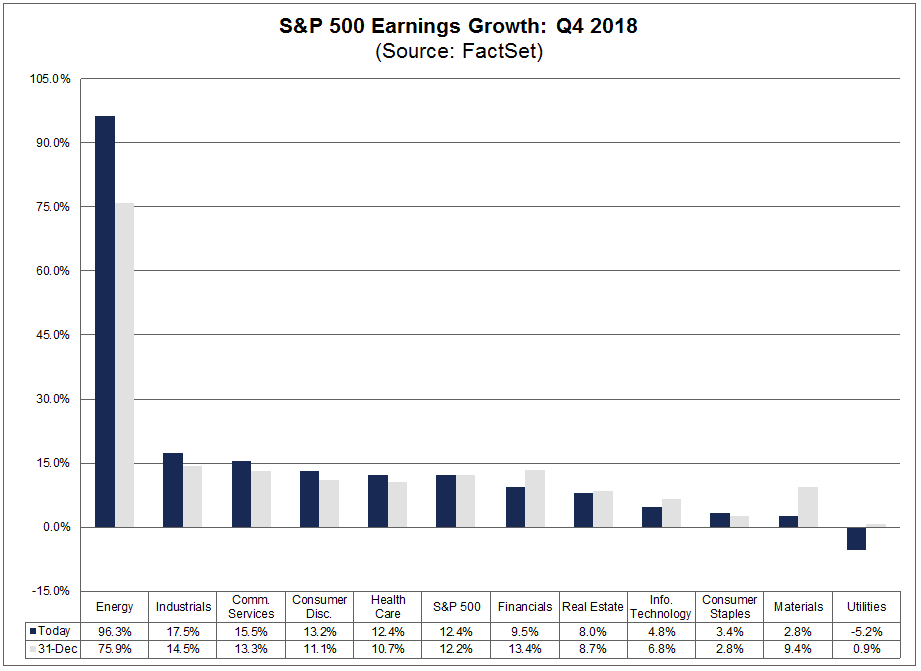

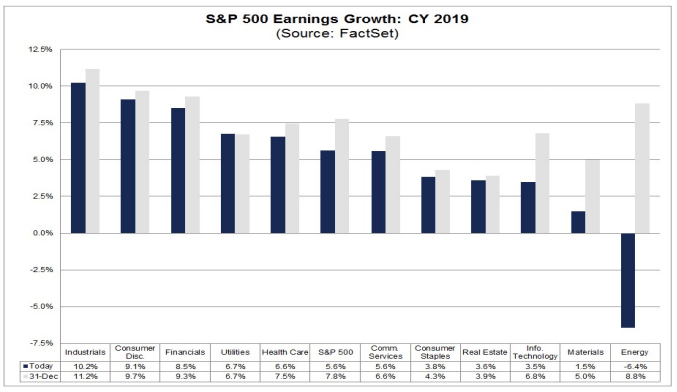

Corporate earnings for the 4th quarter were generally near the 5-year average with 10 of the 11 S&P sectors reporting year-over-year earnings growth.

Energy, Industrials, and Communication Services led the way with double-digit growth rates in the 4th quarter, though earnings estimates for 2019 are trending lower across most sectors[7].

4th Quarter 2018 Actual Earnings Growth vs. 12/31/2018 Projections

2019 Forecast Earnings Growth vs. 12/31/2018 Projections

[7]https://insight.factset.com/earnings-season-update-february-1-2019

The investment team at Warren Street Wealth Advisors held the line through a difficult 4th quarter of 2018, reaping the reward with a strong start to 2019.

The investment team at Warren Street Wealth Advisors held the line through a difficult 4th quarter of 2018, reaping the reward with a strong start to 2019.

Despite some negative headlines in December, the U.S. economy does not seem poised for a recession and we will remain fully invested across market sectors until evidence to the contrary becomes clear. With the Federal Reserve cautious on raising interest rates, job growth and wages increasing, and trade talks moving forward, we expect market volatility in 2019 to settle closer to historic norms, though not without some bumps along the way.

Despite recent weakness in overseas markets relative to the U.S., we are strong in our conviction that international markets are poised to rebound as stock prices stabilize at attractive levels, particularly in Europe and Emerging Markets, and negative headlines diminish. While economic and fundamental data appear mixed globally, we continue to be broadly diversified as international markets work through the next phase of political and economic developments.

As always, if you have any concerns or questions, the investment and financial planning teams at Warren Street Wealth Advisors want to hear from you! Call, write, or drop by our Tustin or El Segundo offices any time. We are here to help.

Marcia Clark, CFA, MBA

Marcia Clark, CFA, MBA

Senior Research Analyst

Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.