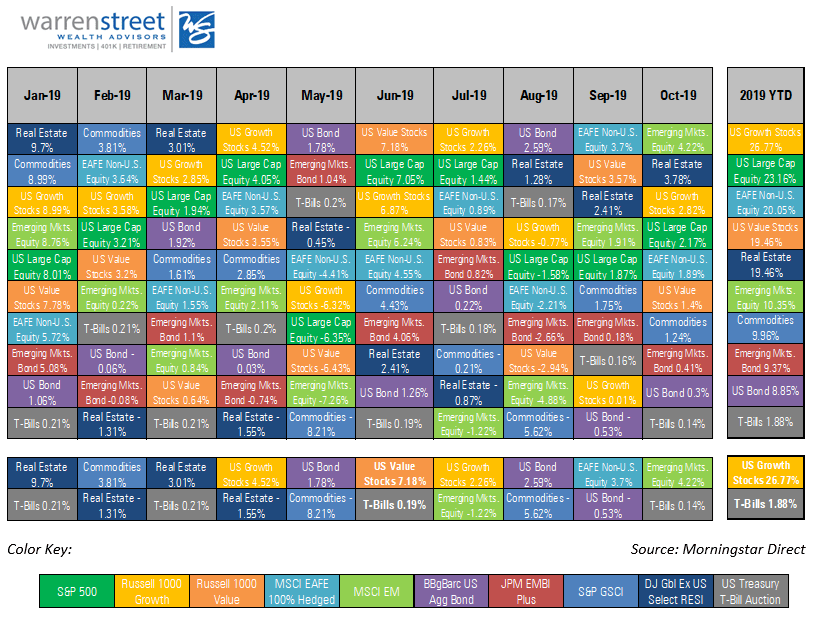

Coronavirus: Here’s a Portfolio Treatment Plan

Wow! Our last published piece on the blog was “2019: A Year for the Record Books”. Two months later and the peace and quiet of yesteryear seem a distant memory. Scary days have arrived, thanks to the concern over how coronavirus might impact our global economy. As we draft this update, headlines are reporting the biggest weekly stock market losses since 2008.

We do not know whether the current correction will deepen or soon dissipate. It is important to remember that what was good advice in mild markets remains good advice today. Given the current climate, let’s take a look at a sound unemotional treatment plan for your nest-egg.

We continue to advise against panicked reactions to market conditions, or trying to predict an unknowable future. That being said, we are aggressively looking for ways to help our clients make lemonade out of this week’s lemons – such as through disciplined portfolio rebalancing and strategic tax loss harvesting. On Friday February 28th, we executed both on behalf of our private wealth clients.

Other lemonade ideas include refinancing your mortgage as interest rates have hit historic lows or executing a ROTH conversion while your portfolio is down, turning the recovery into tax free growth. More than anything, as you’ll see below, a long term perspective during an epidemic pays.

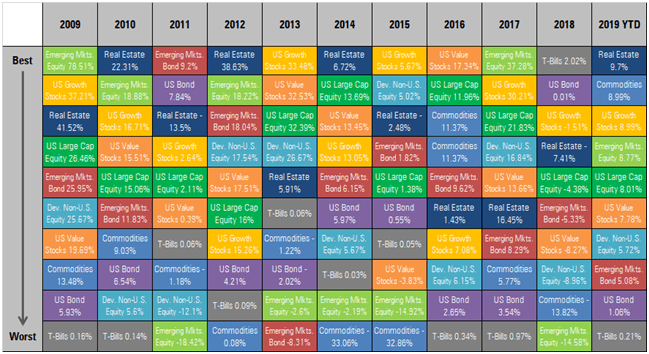

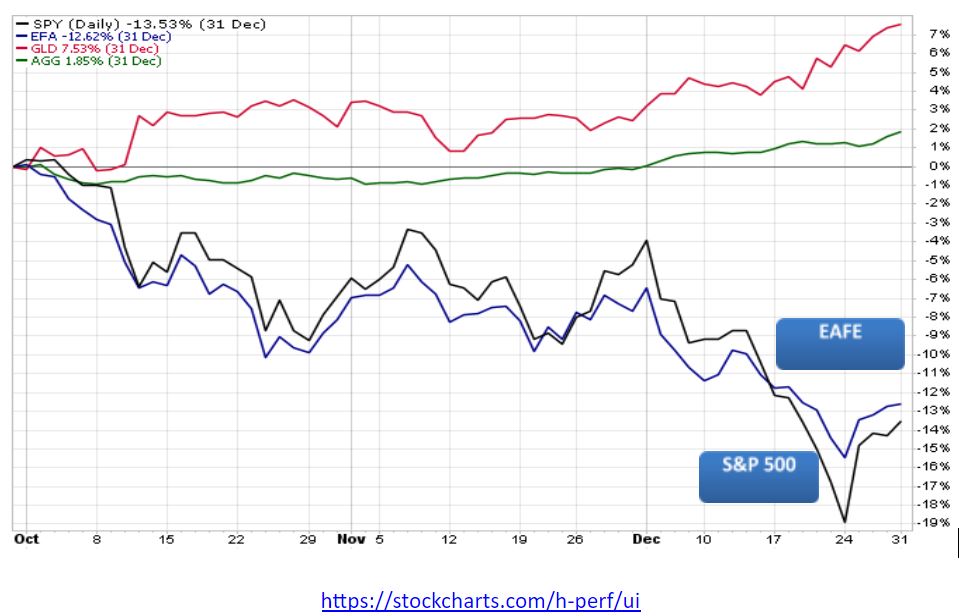

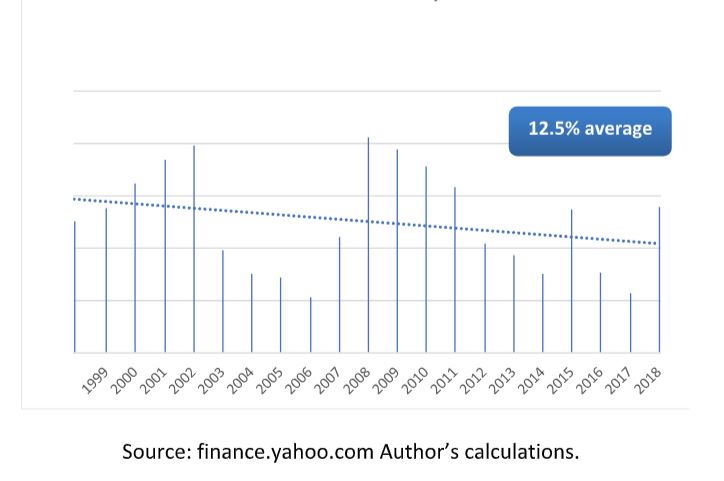

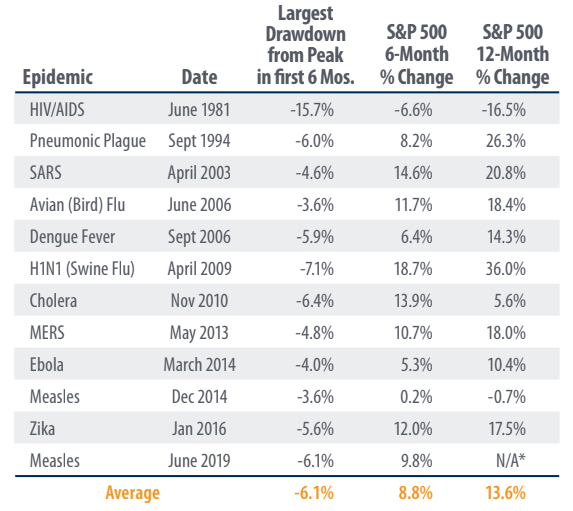

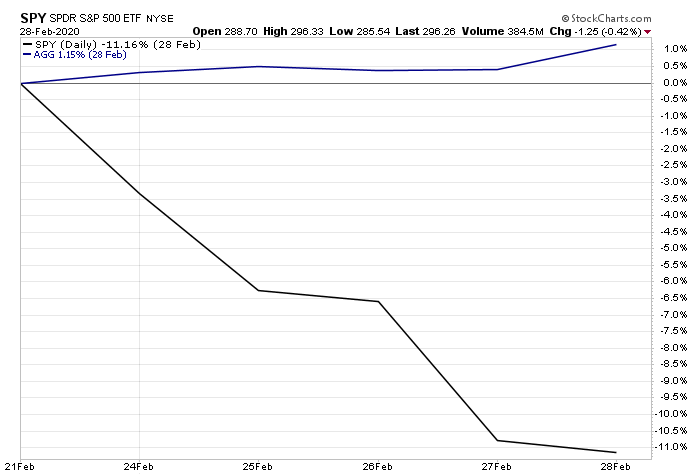

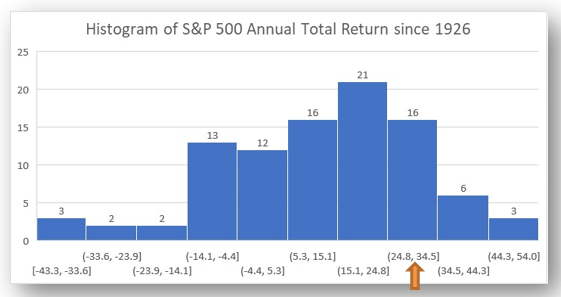

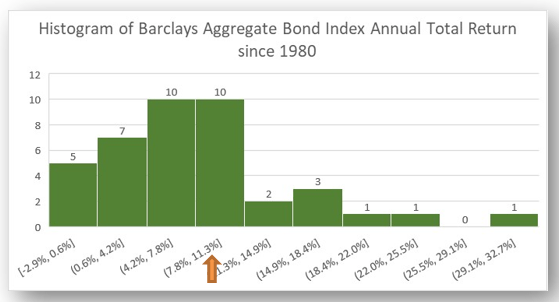

In 11 of the 12 cases above, the U.S. Stock Market was positive 6 months after an epidemic broke out, with an average return of 8.8%. In 9 of the 11 cases the U.S. Stock Market was positive 12 months after with an average return of 13.6%. It’s also important to note diversification worked last week with U.S. Bonds actually netting a positive return while U.S. stocks were down 11.5%.

If we can be of assistance or you want to talk through any of this, please do not hesitate to reach out to our team. In the meantime, here are 10 things you can do right now while markets are at least temporarily tanking.

1. Don’t panic (or pretend not to). It’s easy to believe you’re immune from panic when the financial sun is shining, but it’s hard to avoid indulging in it during a crisis. If you’re entertaining seemingly logical excuses to bail out during a steep or sustained market downturn, remember: It’s highly likely your behavioral biases are doing the talking. Even if you only pretend to be calm, that’s fine, as long as it prevents you from acting on your fears.

“Every time someone says, ‘There is a lot of cash on the sidelines,’ a tiny part of my soul dies. There are no sidelines.” – Cliff Asness, AQR Capital Management

2. Redirect your energy. No matter how logical it may be to sit on your hands during market downturns, your “fight or flight” instincts can trick you into acting anyway. Fortunately, there are productive moves you can make instead – such as all 10 actions here – to satisfy the itch to act without overhauling your investments at potentially the worst possible time.

“My advice to a prospective active do-it-yourself investor is to learn to golf. You’ll get a little exercise, some fresh air and time with your friends. Sure, green fees can be steep, but not as steep as the hit your portfolio will take if you become an active do-it-yourself investor.” – Terrance Odean, behavioral finance professor

3. Remember the evidence. One way to ignore your self-doubts during market crises is to heed what decades of practical and academic evidence have taught us about investing: Capital markets’ long-term trajectories have been upward. Thus, if you sell when markets are down, you’re far more likely to lock in permanent losses than come out ahead.

“Do the math. Expect catastrophes. Whatever happens, stay the course.” – William Bernstein, MD, PhD, financial theorist and neurologist

4. Manage your exposure to breaking news. There’s a difference between following current events versus fixating on them. In today’s multitasking, multimedia world, it’s easier than ever to be inundated by late-breaking news. When you become mired in the minutiae, it’s hard to retain your long-term perspective.

“Choosing what to ignore – turning off constant market updates, tuning out pundits purveying the latest Armageddon – is critical to maintaining a long-term focus.” – Jason Zweig, The Wall Street Journal

5. Revisit your carefully crafted investment plans (or make some). Even if you yearn to go by gut feel during a financial crisis, remember: You promised yourself you wouldn’t do that. When did you promise? When you planned your personalized investment portfolio, carefully allocated to various sources of expected returns, globally diversified to dampen the risks involved, and sensibly executed with low-cost funds managed in an evidence-based manner. What if you’ve not yet made these sorts of plans or established this kind of portfolio? Then these are actions we encourage you to take at your earliest convenience.

“Thus, the prudent strategy for investors is to act like a postage stamp. The lowly postage stamp does only one thing, but it does it exceedingly well – it adheres to its letter until it reaches its destination. Similarly, investors should adhere to their investment plan – asset allocation.” – Larry Swedroe, financial author

6. Reconsider your risk tolerance (but don’t act on it just yet). When you craft a personalized investment portfolio, you also commit to accepting a measure of market risk in exchange for those expected market returns. Unfortunately, during quiet times, it’s easy to overestimate how much risk you can stomach. If you discover you’re miserable to the point of breaking during even modest market declines, you may need to re-think your investment plans. Start planning for prudent portfolio adjustments, preferably working with an objective advisor to help you implement them judiciously over time.

“Our aversion to leverage has dampened our returns over the years. But Charlie [Munger] and I sleep well. Both of us believe it is insane to risk what you have and need in order to obtain what you don’t need.” – Warren Buffett, Berkshire Hathaway

7. Double down on your risk exposure – if you’re able. If, on the other hand, you’ve got nerves of steel, market downturns can be opportunities to buy more of the depressed (low-price) holdings that fit into your investment plans. You can do this with new money, or by rebalancing what you’ve got (selling appreciated assets to buy the underdogs). This is not for the timid! You’re buying holdings other investors are fleeing in droves. But if can do this and hold tight, you’re especially well-positioned to make the most of the expected recovery.

“Pick your risk exposure, and then diversify the hell out of it.” – Eugene Fama, Nobel laureate economist

8. Tax-loss harvest. Depending on market conditions and your own circumstances, you may be able to use tax-loss harvesting during market downturns. A successful tax-loss harvest lowers your tax bill without substantially altering or impacting your long-term investment outcomes. This action is not without its tricks and traps, however, so it’s best done in alliance with a financial professional who is well-versed in navigating the challenges involved.

“In investing, you get what you don’t pay for.” – John C. Bogle, Vanguard founder

9, Revisit this article. There is no better time to re-read this article than when the going gets tough, when yesterday’s practice run is no longer an exercise but a real event. Maybe it will take your mind off the barrage of breaking news.

“We’d never buy a shirt for full price then be O.K. returning it in exchange for the sale price. ‘Scary’ markets convince people this unequal exchange makes sense.” – Carl Richards, Behavior Gap

10. Talk to us. We didn’t know when. We still don’t know how severe it will be, or how long it will last. But we do know markets inevitably tank now and then; we also fully expect they’ll eventually recover and continue upward. Since there’s never a bad time to receive good advice, we hope you’ll be in touch if we can help.

“In the old legend the wise men finally boiled down the history of mortal affairs into the single phrase, ‘This too will pass.’”

– Benjamin Graham, economist, “father of value investing”

Blake Street, CFA, CFP ®

Founding Partner

Chief Investment Officer

Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Marcia Clark, CFA, MBA

Marcia Clark, CFA, MBA