Warren Street is expanding our team of experts! We are incredibly proud to officially introduce our new Lead Advisor, Victor Campos, CPA, CFP®. Based right here in Southern California, Victor brings a rare and powerful combination of tax expertise and comprehensive financial planning to our clients.

As both a Certified Public Accountant and a Certified Financial Planner™, Victor is uniquely equipped to look at the big picture of your wealth—ensuring your investment strategies, retirement goals, and tax mitigation plans work hand-in-hand. We sat down with Victor to learn more about his background, his client-first philosophy, and what he’s most excited about as he steps into this new role at Warren Street. Please join us in giving him a warm welcome!

In your role as Lead Advisor, how do you assist Warren Street’s clients?

I assist Warren Street clients by being a trusted first point of contact and providing them guidance based on their financial goals and aspirations.

What impact do you hope to make at Warren Street?

How does Warren Street align with your personal values?

Warren Streets Core Values of “Clients Best Interest First” and “Integrity & Honesty” align with my approach to providing guidance. I think these values differentiate us in the financial world as we truly strive to help our clients reach their financial goals in a way that is free of conflicts of interest.

Who or what motivates you?

My family motivates me more than anything. Being able to help them in any way I can and striving to be the best version of myself for them brings me a lot of happiness and fulfillment.

What do you enjoy doing outside of work?

I like to stay active by working out and playing anything that has a tactical approach to it like video games or tabletop games.

What are three fun facts about you?

I have gone night swimming with Manta Rays.

I can make a pretty good pizza from scratch.

I have only broken one bone but I still have screws and a plate from the surgery. (It was my left leg and it was 13 years ago.)

—

Whether you are looking to optimize your tax strategy or fine-tune your long-term wealth plan, Victor is ready to help you navigate the path ahead. Next time you connect with our team, please join us in welcoming Victor to the family!

Jennifer La

Director of Sales & Marketing, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/06/Victor-Campos-Headshot.png1030824Jennifer Lahttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJennifer La2026-07-21 09:05:032026-07-21 09:13:39Meet the Team: Victor Campos, CPA, CFP®

The Warren Street team is growing again! We are absolutely thrilled to introduce the newest addition to our team, Jennifer Horner. Jennifer joins us as our Operations & Compliance Associate, bringing a wealth of experience, a fresh perspective, and a deep commitment to protecting and supporting our clients.

At Warren Street, we believe that seamless daily operations and robust compliance are the backbone of a great client experience. We sat down with Jennifer to learn more about her background, her role, and what makes her a perfect fit for our firm. Please enjoy this virtual introduction to Jennifer!

In your role as Operations & Compliance Associate, how do you assist Warren Street’s clients?

At Warren Street I look forward to assisting clients and team members with the transactions and daily operations for brokerage accounts managed by our firm. This could include new account paperwork, updating account information, transaction processing, money movement requirements.

I will also be helping with compliance for the staff and the whole firm. This includes keeping up with required filings to make sure everything’s protected and in order.

What impact do you hope to make at Warren Street?

I’m excited to use my experience and insight to help Warren Street clients and staff achieve their financial and business goals. By actively supporting the Operations and Compliance teams I aim to enhance client experience while offering a fresh perspective on Warren Street’s core values. I look forward to helping everyone I work with day to day here at Warren Street.

How does Warren Street align with your personal values?

Integrity and honesty are big deals here, and those are values I try to live by every day, personally and professionally. I hope that I have instilled the same values in my children.

Who or what motivates you?

My strong family motivates me. When I was younger I found strength in my mom and grandmother. As very strong women they helped me realize that strength is internal & will always hold me up. More recently my youngest son has been a motivation for me. He has demonstrated strength that he may have never known he possesses. I can get through any adversity because of the strength within me and those I love.

What do you enjoy doing outside of work?

I enjoy spending time with my family. Both of my sons are athletes so my husband and I have enjoyed many days at a soccer game, football game, baseball game, or track meet watching them do what they love.

I also enjoy being creative with crafts, reading books & taking in the Southern California sunshine.

What are three fun facts about you?

I was an aspiring Olympic Synchronized Swimmer (now Artistic Swimming) at age 10 and remain a devoted fan, watching the sport during every Summer Olympics.

I have hands-on experience in construction, having helped my dad build an addition onto his home. I learned to put up walls, work on a roof, and pull electrical wires—a skill set that makes me believe I can tackle nearly any DIY project.

My passion for musical theater extends backstage: as a young teen, I helped my mom stage manage several community theater productions. I also love watching musicals and was thrilled to see Hamilton both on Broadway (2019) and at the Pantages (2022).

—

Jennifer’s dedication to integrity, her strong work ethic, and her passion for helping others make her an incredible asset to both our internal staff and the clients we serve every day. Whether she is processing your account paperwork behind the scenes or ensuring our firm meets the highest regulatory standards, we know our clients are in excellent hands with Jennifer on the team.

Next time you speak with the office, please join us in giving Jennifer a warm Warren Street welcome!

Jennifer La

Director of Sales & Marketing, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Warren Street is growing again! We are delighted to introduce you to Isaiah Knox, our Onboarding Coordinator! Isaiah plays a vital role in ensuring a seamless and positive experience for new clients joining Warren Street Wealth Advisors.

In this Q&A, Isaiah shares insights into his role, what drives him, and how he helps set the foundation for successful client relationships.

In your role as Onboarding Coordinator, how do you assist Warren Street’s clients?

As an Onboarding Coordinator, I play a critical role in maintaining the sales pipeline, tracking client cases, and ensuring seamless communication throughout the onboarding process. I coordinate client onboarding communications and proactively manage follow-ups on inquiries, creating a responsive, high-quality experience that makes each client feel supported and valued from day one.

What impact do you hope to make at Warren Street?

I’m here to enhance the onboarding experience for every client by leveraging my client relationship management skills. My goal is to uphold and contribute to the high standard of service Warren Street is known for by nurturing and supporting clients during their very first interactions with the firm. I believe that making a strong, positive first impression sets the foundation for long-term trust and success.

How does Warren Street align with your personal values?

I strongly believe in doing what’s best for the client. Warren Street Wealth’s independence as an investment advisor allows for recommendations that are truly aligned with each client’s unique financial situation. That commitment to personalized, client-first guidance closely reflects my own values and approach to service.

Who or what motivates you?

I’m motivated by building meaningful relationships and by my family. Both inspire me to bring my best self to everything I do, personally and professionally.

What do you enjoy doing outside of work?

Outside of work, I enjoy spending quality time with my children, playing board games, and going on hikes in nature. These activities help me stay balanced, energized, and connected.

What are three fun facts about you?

I used to compete in amateur boxing.

I enjoy attending live theater and try to see as many plays as I can.

I also love tinkering and building things, especially projects for my children.

We are excited to have Isaiah Knox on board and look forward to the positive impact he will continue to make for our clients.

Jennifer La

Director of Sales & Marketing, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Understanding why we behave the way we do with money is the first step toward transforming our relationship with it. In part one of this series, we explored the concept of money scripts—the unconscious beliefs about money that shape our financial decisions. And we dug into four dominant money scripts: money status, money worship, money avoidance and money vigilance.

These scripts are not inherently good or bad. However, without awareness, they can create challenges in how we manage our finances. The good news? You can take control of your money script and reshape it in ways that better serve you. In this second part of the series, we’ll focus on actionable strategies to manage these scripts, flip unhelpful patterns and build healthier financial behaviors.

Managing Money Status

For individuals with a money status script, the drive to prove their own worth through financial achievements can lead to overspending, debt accumulation or a constant cycle of comparison.

To break free from the hold of money status, create intentional space between the desire to purchase and the action of buying. Pause and ask yourself: Am I making this purchase to fulfill an emotional need? Will buying this truly solve or address that need?

For example, if the urge to splurge on a luxury item hits, reflect on whether the purchase aligns with your long-term financial goals or if it’s merely an emotional reaction. Being mindful around purchases can help you gain control over impulsive spending habits and reduce the emotional weight you place on money as a source of self-esteem.

It may help to consider that we tend not to factor debt into our perceptions of others. When it comes to the proverbial Joneses (whom you might be tempted to keep up with), consider that they may themselves be walking an untenable tightrope, taking on too much debt to truly support their lifestyles. And if this is the case, it may not be something you want to emulate, let alone outdo.

Managing Money Worship

Money worship may show up as the belief that financial success will lead to happiness and fulfillment. And while money may help reduce stress, it doesn’t necessarily lead to lasting contentment. In fact, research shows that while happiness does rise with income, for many, it tends to plateau once they make about $100,000 annually.

To counteract money worship, make a conscious effort to take money out of the happiness equation. Instead, prioritize activities and experiences that truly bring you joy. For instance, you may choose to invest in experiences, taking trips, exploring hobbies or trying something altogether new. Focus on your values. Ask yourself what really matters to you beyond the pursuit of wealth. It might be as simple as spending time with loved ones or giving back to your community.

Rather than chasing external symbols of success, redirect your energy toward building meaningful relationships and activities. This shift can help you redefine happiness in ways that are both fulfilling and sustainable.

Managing Money Avoidance

Money avoidance often stems from the belief that money is inherently bad or shameful. This script can lead to neglecting finances, avoiding budgets or feeling guilty about earning or spending money.

Overcoming money avoidance starts with building a healthy relationship with your finances. Here’s how:

Create financial habits: Start small. Dedicate 15 minutes a week to reviewing your budget, checking account balances or tracking expenses. The more you interact with your money, the less scary it becomes.

Reframe your perspective: Money is not inherently good or bad—it’s a tool. Reflect on the ways financial security can be a positive force in your life and the world around you. For example, having control over your money can empower you to help loved ones, support causes you care about and enjoy more peace of mind.

By consistently engaging with your finances, you can begin to replace feelings of shame or discomfort with a sense of empowerment and control.

Managing Money Vigilance

Money vigilance often leads to responsible financial behavior, like saving diligently and avoiding excessive spending. However, its downside can include anxiety around spending or an inability to enjoy the rewards of hard work.

To ensure your money vigilance doesn’t become overly restrictive, watch for signs of financial anxiety:

Are you monitoring your finances excessively?

Do you feel guilty when spending money, even on things that bring joy or improve your quality of life?

Are you afraid of spending freely, even when you can afford to do so, and your purchases align with your goals?

Striking a balance is key. While saving is vital, allow yourself to enjoy the fruits of your labor. Create space in your budget for small, intentional indulgences.

Discovering Your Script

These four money scripts are not exhaustive, nor are they mutually exclusive. Many people embody a mix of these beliefs, influenced by personal experiences, family teachings and cultural norms. The key is identifying your most dominant scripts and understanding how they impact your financial behaviors.

What are your money scripts? Discovering them requires honest self-reflection. Start by exploring the following questions:

What did family and community members teach me about money? Was money seen as good, bad or taboo? Did financial success signify status? Was it a source of stress or pride?

What did my circumstances teach me? If money was scarce during your childhood, you may now see it as something to hoard or fear. Alternatively, if money provided security, it might feel like a source of safety.

What has my culture taught me? In the U.S., for instance, discussing money is often considered taboo, even though consumer culture places enormous pressure to spend and accumulate wealth.

As you reflect, take note of which beliefs have served you well and which ones may be holding you back. Ask yourself: How have these beliefs impacted my financial decisions? Are they helping me build the life I want, or do they create stress and frustration?

Flipping the Script

Identifying and understanding your money scripts is just the beginning. Transforming them requires ongoing effort, self-awareness and a willingness to experiment with new behaviors.

One way to start the transformation? Be on the lookout for habit loops. What happens when you think about money? Do you go online and shop? Do you go organize your sock drawer? What are the results of these behaviors? Perhaps you find you go on bouts of overspending, deny yourself affordable enjoyments or avoid necessary financial tasks, such as paying your bills.

Reshaping your money scripts is a lifelong journey. As you gather new insights and experiences, you’ll continue to refine your approach to money in ways that align with your goals and values. Taking the time to reflect—and reshape—your mindset can create lasting change. If you’ve applied these tactics and still find yourself struggling, you might consider turning to a financial therapist who can further help uncover the emotions guiding financial decisions and help you work toward healthy financial behaviors. And as always, we’re here to support however we can.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/03/Money-Script-1.png10801080Warren Street Teamhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgWarren Street Team2026-03-20 09:26:322026-03-20 09:26:37Money Scripts—Part 2: How to Manage the Script

When it comes to our finances, we’re only human. We make good decisions and sometimes, not-so-good decisions. Behavioral biases play a big role in our savings, spending and investing decisions. But there’s another reason behind some of the financial decisions we make: It’s how we were brought up.

Psychologist Dr. Brad Klontz calls these our “money scripts”—unconscious rules and beliefs we develop about money that are often passed from generation to generation. Some guide us in positive directions, like learning the importance of saving for a rainy day. And some can lead to challenging behaviors later in life. One study in Britain, for example, found that children who were raised in households where spending was secretive were more likely to develop hoarding and other compulsive money habits as adults.

“The problem is that we take these beliefs for granted as adults, and we rarely go back and examine them, let alone decide to change them,” Klontz says. “Instead, they’re kind of like an actor’s script in a movie; we just continue to read the lines in our heads…and believe that they’re true, when in fact, they are often quite distorted and limit our success.”

Not all money scripts are bad. But getting caught up in your own negative money scripts can knock you off course as you pursue your financial goals. Learning to recognize your scripts—and discovering ways to counter those negative ones—puts the power in your court, helping you make positive changes to your financial behavior.

In the first of this two-part of this series, let’s explore some of the most common money scripts.

Understanding Money Scripts

While there are many money scripts, Klontz and his fellow researchers have identified four main patterns.

Money status: This category of scripts leads people to tie their self-esteem to how much money they have. It can lead to impulse buying and overspending to flaunt wealth.

It might fuel the urge to keep up with the Joneses—or even show them up. Those who largely view their money as a status symbol believe that buying things like high-end clothes or luxury cars will show the world how successful they are. They might round up when they tell people how much they earn, and keep secrets about money from their partners, especially if their spending leads to living beyond their means. They might also have distorted view of others based on how much money they have, believing rich people should be happy and poor people are lazy or don’t deserve money at all, for instance.

They might also have distorted view of others based on how much money they have, believing rich people should be happy and poor people are lazy or don’t deserve money at all, for instance.

Money worship: Those who identify with money worship often feel like money is the key to happiness, freedom and power—and if they only had more, their problems would be solved.

Closely tied to these feelings is the belief that you can never have too much money, and that you can’t trust other people around money issues.This belief can set money worshippers on a spend, spend, spend treadmill as they chase happiness goal posts that keep shifting further into the distance.

Money avoidance: People who avoid money (or at least managing the money they’ve got) carry a deep-seated belief that money is bad or shameful, that accumulating wealth is greedy and that those who do so are corrupt. It may come as no surprise, then, that money avoidance can hamper the ability to accumulate wealth.

Those who identify with this pattern may have a deep distrust of wealth and rich people and may even think that having less money is virtuous. After all, money corrupts and the rich must be taking advantage of people, right? There may even be some feeling of not deserving to have money.

Money vigilance: Vigilant spenders accept that money is a practical tool best used to save for the future. The money vigilant are often frugal, and they may downplay how much they make and even be secretive about money.

For these people, talking about money can feel shameful or taboo, making it tough to have practical conversations about it. They may have a hard time spending money on themselves, whether it’s buying a new appliance when the old one breaks or shelling out on an interest or activity that brings them joy.

Now, we should note that these categories represent extremes. And as such, they may not read as particularly attractive. Who wants to identify with any of them, really? But in reality, we likely contain a bit of each of these patterns to varying degrees. Some may pull stronger than others, and some that sound overtly negative may offer strengths. For example, it’s okay to buy something flashy every once and a while (and even to get a thrill from showing off a bit), especially if your stronger tendencies lean toward money vigilance.

With an understanding of the most common money scripts under your belt, you’re equipped to start keeping an eye out for where echoes of each appear in your own life in positive and negative ways. This identification process is important, because it allows you to move away from tendencies that don’t serve you well and toward those that do. In the second part of this series, we’ll offer strategies for flipping the script on these common behaviors and exploring your own personal money scripts. Stay tuned!

And in the meantime, we’re here to answer questions or offer strategies that can help you better reach your long-term financial goals.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/03/Money-Script.png10801080Warren Street Teamhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgWarren Street Team2026-03-13 10:02:562026-03-13 10:14:26Money Scripts—Part 1: The Stories We Tell Ourselves in Order to Live, Save and Spend

Over the next few decades, an enormous amount of wealth is expected to pass from older to younger generations. This has been dubbed the “Great Wealth Transfer,” and one estimate suggests that $124 trillion will change hands by 2048. It’s an eye-popping figure, to be sure, but it also highlights the reality that many families are, or soon will be, navigating how to pass on their wealth. A top-of-mind question: Is the next generation ready to take on the responsibility?

Wealth is not just cash in the bank; it can include investments, real estate, businesses and more that require stewardship and foresight. Successful management means preserving and growing assets and using them wisely. Striking the right balance here is key: For the next generation to succeed, it takes intentional preparation and education.

Plant the Seeds of Financial Literacy

Where to begin? In an ideal world, financial education starts in early childhood and is treated as an open and ongoing conversation as kids age. The goal is to build financial literacy gradually, so wealth management feels natural rather than overwhelming.

When kids are young, this might mean introducing simple topics like the difference between saving and spending. Managing an allowance can help put those ideas into practice. As kids get older you can begin introducing more complex topics, such as investing, compound interest, debt and taxes.

It’s equally important to engage adult children, many of whom may have received no other formal financial education. While 29 states now have K–12 financial education requirements in public schools, this focus has largely come to the forefront only in the last few years. If your kids are adults now, they may have missed out. So it’s worth finding out what they know, what they don’t know and what they’d like to know more about.

Put Structure Around Learning

In addition to ongoing conversations about money, your family might benefit from more intentional ways of building financial literacy. Some families hold regular financial meetings where they share goals, key issues and address questions or concerns. Others put together more formal workshops with wealth advisors or other experts.

There also is a wealth of credible educational content online that is built to both educate and engage audiences around financial literacy topics.

Turn Conversations into Action

Eventually, theory should give way to practice. As younger family members learn the basics, you might consider providing a “practice portfolio,” giving them the chance to make investment decisions with small amounts of money and learn from their successes and mistakes.

When family members have honed their knowledge, consider assigning them real responsibilities that match their skills and interest. This might mean relatively simple tasks like helping guide gifts made through a donor-advised fund. Or these responsibilities could be more involved, such as taking a role in the family business or helping to make investment decisions with the family’s wealth. With your guidance and oversight, these experiences can help develop confidence and capability.

Ground Wealth in Purpose and Values

One of the most important things that helps guide families on how to grow and spend wealth is imparting a strong value system. Values can help you frame wealth as a tool rather than a goal.

Your values will be unique to you, but some worth considering may be:

Stewardship: Recognizing the responsibility that comes with wealth. Stewardship encourages careful management and intentional choices so resources can benefit both current and future generations.

Giving back: Using wealth to help create positive change in your community and the greater world.

Self-worth beyond wealth: Remembering that wealth is a tool to achieve goals—whether gaining an education, pursuing passion or giving back, for instance—not a measure of personal value.

By grounding financial decisions in values, families can help prevent counterproductive or reckless financial decisions, foster responsibility and ensure wealth is not seen as something to be simply consumed.

Keep the Conversation Going

Discussing money isn’t always easy, and for many families, it’s downright taboo. While 66% of Americans say conversations about wealth are important, 62% say they never have them.

But getting over this hurdle is incredibly valuable. The most successful families treat wealth education not as a one-time event, but as an ongoing process that evolves as your family grows and your financial picture changes. We can work with you to create an environment where family members can openly discuss the unique challenges and opportunities that come with wealth.

Veronica Cabral, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/03/image-1.png9001600Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2026-03-02 09:49:032026-03-02 09:49:08How Do You Prepare the Next Generation to Manage Family Wealth?

Filing your tax return may feel routine. But the devil is in the details, as they say, and those details have a pesky habit of shifting from year to year. The 2025 tax year is a good example: Rule changes this year include both incremental adjustments and larger shifts stemming from the One Big Beautiful Bill Act (OBBBA), passed in July. Understanding these changes now can help you maximize deductions, spot planning opportunities and avoid surprises when you file.

A Boost for Traditional Deductions

The OBBBA made several taxpayer-friendly provisions permanent, starting with a higher standard deduction. For 2025, the standard deduction rises to $15,750 for single filers, up from $15,000 in 2024. For married couples filing jointly, the deduction increases to $31,500, up from $30,000.

The legislation also expanded the Child Tax Credit, raising it to $2,200 per qualifying child, compared with $2,000 under prior law.

Personal deduction for seniors: If you were born before Jan. 2, 1961, you can take a $6,000 deduction ($12,000 if married filing jointly) in addition to your standard or itemized deduction. This deduction is phased out if your modified adjusted gross income (MAGI) is between $75,000 ($150,000 for joint filers) and $175,000 ($250,000 for joint filers).

Tax deduction for tips and overtime pay: The Trump administration has described these provisions as “no tax” on tips and overtime, but that framing oversimplifies how the new code works. In practice, there is now a deduction for voluntary cash or charged tips earned in industries where tipping is customary. From 2025 through 2028, eligible single filers can deduct up to $25,000 in tipped income, though the deduction begins to phase out for individuals with MAGI above $150,000.

A similar deduction applies to a portion of qualified overtime pay from 2025 through 2028. In most cases, this refers only to the premium portion of overtime—for example, the extra “half” in “time-and-a-half” pay—rather than the worker’s full hourly wage. For single filers, the deduction is capped at $12,500 of eligible compensation for those with MAGI below $150,000. The deduction is phased out above that amount and is zeroed out once above $275,000.

Car loan interest deduction:If you financed the purchase of a new vehicle in 2025, you may be eligible to deduct up to $10,000 in interest paid on that loan. But here’s the fine print: The vehicle must be for personal use, and it must have been built in the United States. To determine if your car fits the bill, look at your vehicle identification number (VIN). Cars built in the United States will have a VIN that starts with a 1, 4 or 5. The cap also phases out for single filers with MAGI above $100,000.

In future years, lenders will be required to report auto loan interest payments directly to both taxpayers and the IRS. For this year, you may need to do a little digging through your loan statements, or you can request a summary of interest paid from your lender.

Gift and Estate Tax Exemptions

The OBBBA gave some much-needed clarity to a crucial estate planning rule. The lifetime estate and gift tax exemption was previously scheduled to sunset at the end of the year, which would have reduced the exemption from nearly $14 million to about $6 million. Instead, the higher exemption has been made permanent. Here’s where things stand now:

The annual gift tax exclusion is $19,000 per recipient in 2025 and will remain at that level in 2026.

While it’s too late to make a tax-free gift for 2025, now is a good time to begin planning gifting strategies for 2026.

Tax Reporting on Cryptocurrency

Beginning in 2025, the IRS now requires that crypto transactions are reported. If you sold or exchanged digital assets on a platform such as Coinbase, you should receive a Form 1099-DA. a new tax form created specifically for digital assets. Capital gains taxes may apply to crypto sales and trades. It’s also worth noting that digital currencies may be taxed as ordinary income if you receive them as payment.

It’s Not Too Late to Fund Your IRA

Your window for 2025 401(k) contributions closed at the end of the year. But if you want to pad your traditional or Roth IRA with 2025 contributions, you can do so up until the April 15 filing deadline. The contribution limit for IRAs is $7,000, but you can save an additional $1,000 if you’re 50 or older.

Planning Ahead Matters

The impact of these changes depends on your income, filing status and long-term goals. Take time now to review your situation, gather the right documentation and coordinate tax decisions with your broader financial plan to make most of the current rules. And if you have any questions, we’re here to help bring clarity and confidence as you head into the filing season.

Ernest Jones, CPA

Director of Tax, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

This is for informational purposes only and is not meant to be construed as tax advice. Please consult your accountant for advice or to review any recommendation herein.The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/02/New-Year-New-Tax-Considerations.png10801080Ernest Jones, CPAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgErnest Jones, CPA2026-02-13 08:57:352026-02-13 08:57:43New Year, New Tax Considerations: What You Need to Know Before Filing Your 2025 Taxes

A few years ago, ads from financial services companies asked, “What’s your number?” The “number” represented the amount of money you needed to retire comfortably. There are, of course, various approaches to estimating your retirement “number,” all of which are influenced by your goals and factors, such as your expected retirement age and the lifestyle you hope to maintain in retirement. So, while this question may have been an effective way to spark conversations about retirement, we believe that it doesn’t paint the complete picture.

Retirement isn’t just about reaching a specific monetary goal. It also involves creating a comprehensive strategy that looks to optimize your various savings vehicles, each playing a different role in your retirement income approach. It also means factoring in healthcare costs, thinking about the legacy you wish to leave, and being flexible enough to adapt to life’s unexpected twists and turns. Ultimately, your strategy needs to consider how your assets will work together to fund the retirement you envision.

An essential part of orchestrating your retirement income strategy is determining which assets to take and in which order.

There is no one-size-fits-all answer, but some general guidelines can help when you are starting to think about a withdrawal strategy.

For example, one approach to consider is withdrawing money from taxable accounts first, then tax-deferred, then tax-exempt. By using taxable money first, you can avoid paying taxes as long as possible with tax-deferred investments. And your tax-exempt accounts remain tax-exempt for a longer period. Ultimately, your decision will be influenced by a wide range of other considerations, including withdrawal fees, surrender charges, and other costs that may be associated with each specific account. But when possible, consider using the power of tax deferral and tax exemption to your advantage.

Regardless of your age or financial position, having a well-thought-out retirement strategy is one of the most critical actions you can take. If you would like to review your current strategy, please contact our office. We’re here for you!

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/02/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2026-02-06 10:58:592026-02-06 10:59:05How Much Do I Need to Retire in 2026?

“Is AI a bubble?” my uncle asked as I put my fork down mid-bite on New Year’s Eve. I’d wager that this question dominated dinner tables and family gatherings across the country this holiday season. Even my sister, whose focus lies entirely within the arts and creative pursuits, managed to put the two words “AI” and “Bubble” together.

This tells me two things: 1) Concern around AI and “bubble-ness” is virtually inescapable and 2) this question is dominating the audience’s perception of markets, perhaps even more so than the meteoric rise of silver and gold as we enter 2026.

Why Does AI Deserve So Much Attention?

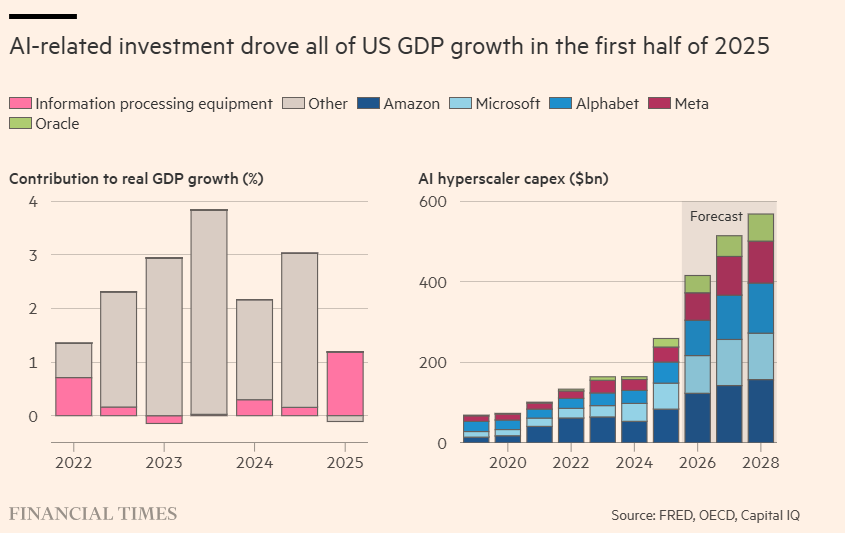

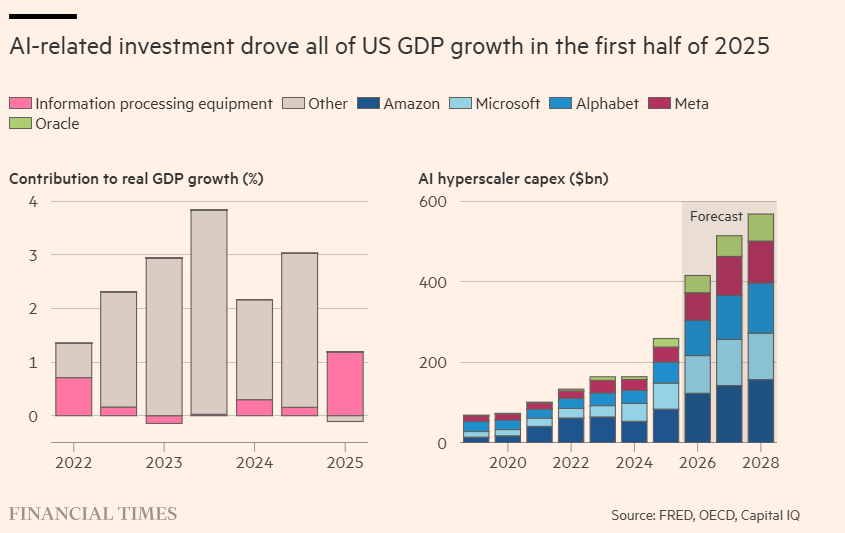

In 2025, AI-related names drove ~60% of the increase in the S&P 500’s value. Furthermore, AI spending from the “Hyperscalers” (Google, Microsoft, etc.) accounted for the lion’s share of our economy’s growth. Without the spending on data center infrastructure—servers, GPUs, and the centers themselves—some estimates suggest US GDP would have grown at a measly 0.1% in the first half of 2025. It’s safe to say that AI alone kept the economy afloat for most of last year.

The robust figures above underscore why AI rightfully commands significant attention. However, fixating on the bubble label can be a trap, much like timing the market. Instead, we should look at bubble psychology and how those excesses may be extending into the AI ecosystem.

Settling the AI Bubble Talk

It’s been over 20 years since we’ve seen such a transformative, general-purpose technology with the potential to deliver productivity gains eclipsing the internet era. This fervor has already minted a class of early winners, leaving everyone else watching with a potent mix of envy and regret. It’s the classic setup for FOMO, where the “AI train” starts looking less like a sound, technological investment and more like a high-speed shortcut to a cushy nest egg.

The danger is that the faster this train moves, the easier it is to speed right past the following flags:

Starting Valuations: We pay prices regardless of whether reasonable returns can be generated.

Risk/Reward Profiles: We stop asking if we’re actually being compensated for the layers of risk we’re adding to our broader portfolio.

Lofty Narratives: AI’s newness unrestrains the imagination to justify price tags that reality can’t yet support.

Behind the Excitement: What’s Different This Time?

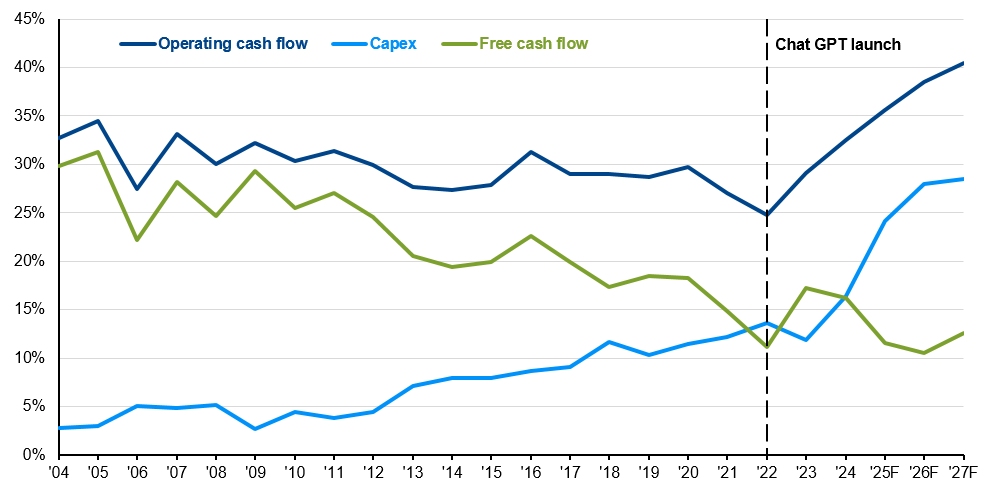

A Stronger Starting Line-Up Unlike the fragile startups of the dotcom era, today’s main AI spenders are profitable, cash-printing businesses. They are self-funding a massive AI arms race with capital expenditures set to leap by 60%, from $250bn in 2025 to over $400bn in 2026. Operating cash flows continue to outspace AI spend as a percentage of sales, allowing this historic investment to feel like a strategic augmentation of their core businesses rather than a reckless gamble.

Justified Valuations While Forward P/E ratios look expensive, today’s multiples are anchored by real-world profit. Take Nvidia: its stock price increased 14x over the last five years, but earnings grew 20x. Today’s titans aren’t as frothy as the dotcom class of 2000 because they are delivering healthy bottom-line results. However, this optimism hinges on perfection. While bulls argue we are buying “cheaper” growth today than at any point in the decade, that narrative leaves a near zero margin for error if adoption slows.

Infrastructure Demand In contrast to the fiber-optic mania of the 90s, the demand for AI build-outs can’t seem to catch a break. Data center vacancy rates are at a record low of 1.6%, and ~75% of pre-construction builds are already pre-leased. Additionally, past infrastructure bubbles saw spending peak between 2% and 5% of GDP, whereas today’s AI investment sits at roughly 1%. This suggests the build-out still has room to run.

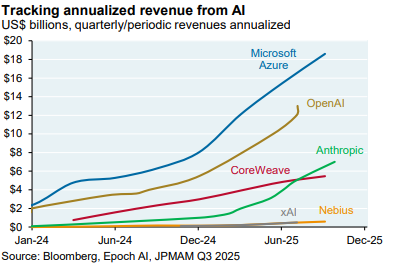

Show Me the Money Revenues are skyrocketing. Alphabet’s Q3 2025 results proved that AI-driven features are accelerating search and ads, with generative AI product revenue surging into the triple-digit percentage range year-over-year. Beyond the titans, some industry participants have grown revenues nearly ninefold since ChatGPT launched. For now, the receipts are keeping the optimism alive.

AI Is Running Fast… But Will it Trip a Wire?

We are in a high-stakes arms race on both a micro level (hyperscalers) and a macro level (US vs. China). Businesses are pouring trillions into this effort to secure US leadership in a technology that will change the fabric of society. But in this race to the top, it’s easy to overlook the blind spots.

Revenues & Profits: Can We Reach the Promised Land? Despite the growth, there is a staggering gap between spending and earning. Analyst Azeem Azhar points out that AI companies are projected to generate $60bn in revenue against $400bn in spending for 2025. That’s a 6-7x gap—far wider than the dotcom bubble (4x) or the railroad boom (2x). Even if revenue catches up, will it translate to profit, or will we see a “race to the bottom” where large language models (LLMs) become commoditized?

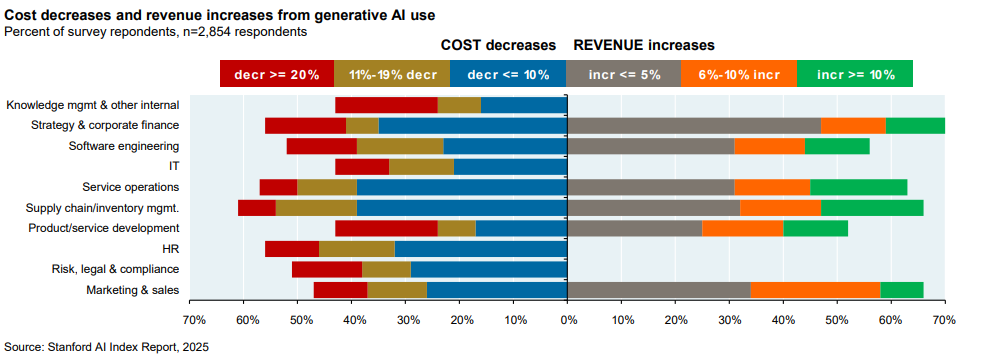

Is Demand Real? Adoption is still in its awkward early stages. Only roughly 10% of firms are using AI to produce goods, though 45% pay for LLM subscriptions. According to the Stanford AI Index and McKinsey, the majority of firms are seeing only modest cost savings (≤10%) and negligible revenue gains (≤5%). Will AI adoption ever truly scale into broad, durable profit expansion?

How Long is Your (Useful) Life? Hyperscalers like Microsoft and Google have boosted profits by extending the “useful life” of their AI assets in their books. If innovation renders chips obsolete in 24 months, these companies will face massive write-downs. More importantly, they are funding this short-lived hardware with 30-year debt, leaving investors holding the bag for “obsolete” infrastructure that won’t be paid off for decades.

The AI Ouroboros There is an increasingly circular dance where Microsoft invests in OpenAI and then books cloud revenue from them. Nvidia buys stakes in the startups they sell chips to. This means a chunk of today’s “booming” revenue is an internal recycling of capital where true economic profit from external customers remains hypothetical.

Cloudy with a Chance of IOUs: While the biggest players usually use cash, we’re seeing a pivot toward the bond market. Oracle and Meta have emerged as outliers, using long-term bonds and project finance to bankroll their data centers. As free cash flow wilts under the weight of AI spend, their stock prices are feeling the gravity. Furthermore, the industry is using Special Purpose Vehicles (SPVs) to hide this leverage off-balance sheet, adding a layer of obscurity to the trillions being spent.

Conclusion: A Massive Collection of What-Ifs

Ultimately, the AI story comes down to “what-ifs.” What if AGI finally shows up and productivity explodes? Or, what if demand never materializes and the hyperscalers finally blink? With cracks showing—like OpenAI’s recent “Code Red”—it’s impossible to say if we’re headed for a minor correction or a systemic burst.

Our 2026 Recommendations:

Keep a seat at the table: Exposure to market-cap weighted indices allows you to benefit if the “promised land” materializes.

Diversify your sources of risk: Anchor beyond US tech. Gold, international markets, and bonds offer a necessary buffer if signs of excess turn into a choppy ride.

Rebalance systematically: Rebalancing is a controllable hedge. When sector weights become excessive, returning to target allocations helps lock in gains and reduce concentration risk.

Phillip Law, CFA

Senior Portfolio Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

With 2025 in the rear view mirror, we look towards the new year. What lessons did we learn and what trends deserve attention? How do we allocate portfolios based on that knowledge? In this piece, we’d like to share three areas of focus heading into 2026:

Artificial Intelligence and Bubbleness

The State of the US Economy

The Biggest Risks to Asset Markets (Namely Inflation)

2025 Recap: Laughing in the Face of Di-worsification:

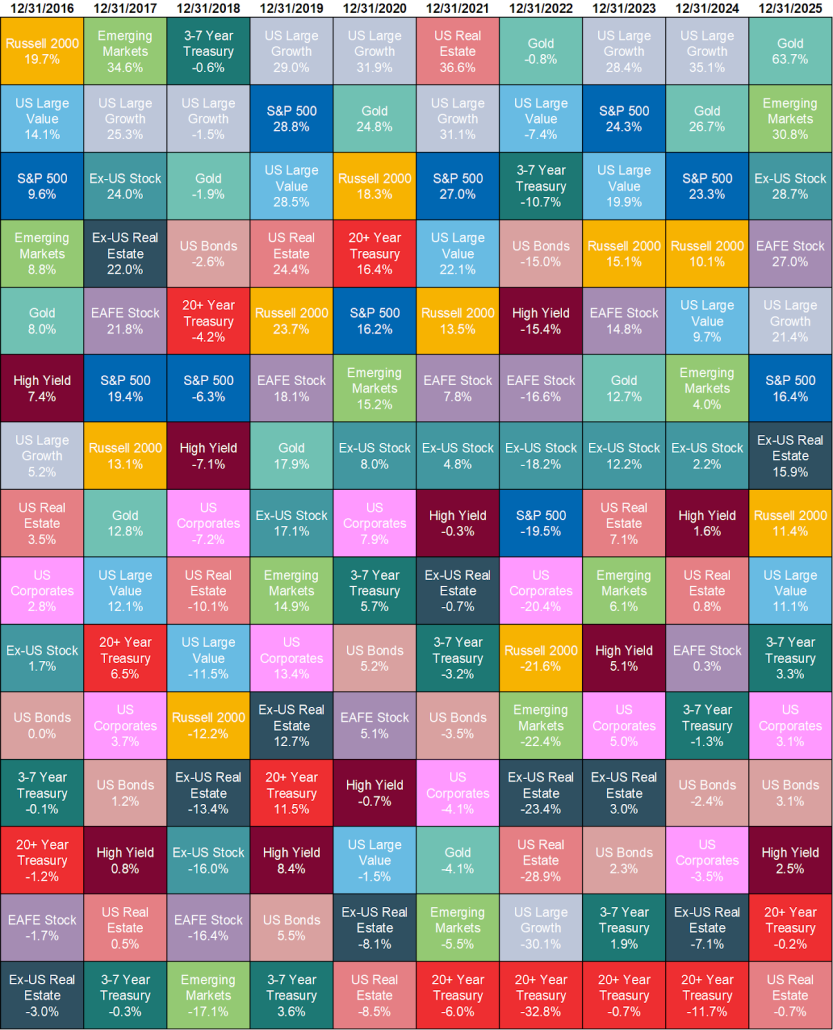

After years of US led-dominance, we saw narratives across asset classes flip on their heads. For the first time in years:

US Stocks underperformed developed international and emerging market geographies.

Gold, held for its diversification benefits, shined more brightly than most major asset categories.

Source: YCharts

The year reminded us that “di-worsification” – a term long used to parody the idea that diversifying into less correlated, non-US assets only made portfolios worse – isn’t a universal truth. In 2025, holding different asset segments helped weather volatile trade policy, weakening dollar, and US deficit concerns.

Ultimately, we left 2025 with a more fragmented globe where nations now emphasize national security and independence over globalized efficiencies. In this new regime where the global economy is de-synchronized, we believe diversification is more essential than ever.

Looking to 2026: What of AI and Its Bubbleness?

The topic of artificial intelligence being a bubble is almost inescapable. AI Hyperscalers, bolstered by massive spending commitments on AI investments, drove over 60% of the S&P 500’s growth and was a key lifeline for the economy in 2025. With AI hyperscalers and key players constituting a significant portion of the S&P 500, the ecosystem will likely continue to define US markets in 2026. So is it a bubble?

We have a separate piece that deep dives into the AI Bubble question which I’ve summarized below:

The Bull Case:

Proponents argue that this time is different compared to other speculative manias. The players here are profitable, cash-printing businesses whose valuations are not only reasonable, but also are pricing in achievable growth. Furthermore, there is ample demand for infrastructure, particularly data centers, unlike the railroad and dotcom bubbles. This all will enable revenue to follow, which has already exhibited enormous growth rates.

The Bear Case:

Despite tremendous growth, AI companies are spending way more than they’re making, (higher than past bubbles). Demand from businesses remains uncertain, with early studies showing only modest cost savings/revenue gains. Also, most revenue booked today is a result of circular investing amongst AI players. Meanwhile, AI companies are using aggressive accounting methods for their chips, which puts future earnings estimates at risk. Lastly, debt is now being used to finance spending, officially adding a shot clock for return on investment to materialize.

What to Do?

Within the deep-dive, we reach two conclusions:

1. Focusing on the “bubble” label is often unproductive. Even if excesses exist, timing the eventual “burst” is a fool’s errand—will it be in one year or five? Selling too early means potentially missing out on healthy gains.

As Peter Lynch noted, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

2. The AI dilemma is ultimately a huge collection of what-ifs, but we believe keeping a seat at the table while diversifying sources of risk and return in other parts of the portfolio such as international stocks, bonds, or gold is prudent.

How’s the US Economy?

Objectively speaking, the economy is in a healthy state heading into 2026. Let’s look at a few primary indicators:

A Productive Economy – GDP grew at an astonishing annualized rate of 4.3% in Q3 2025 and is projected to grow ~2% (long-term average) in 2026. We expect AI spending to continue as hyperscalers add to productivity and other businesses increase adoption.

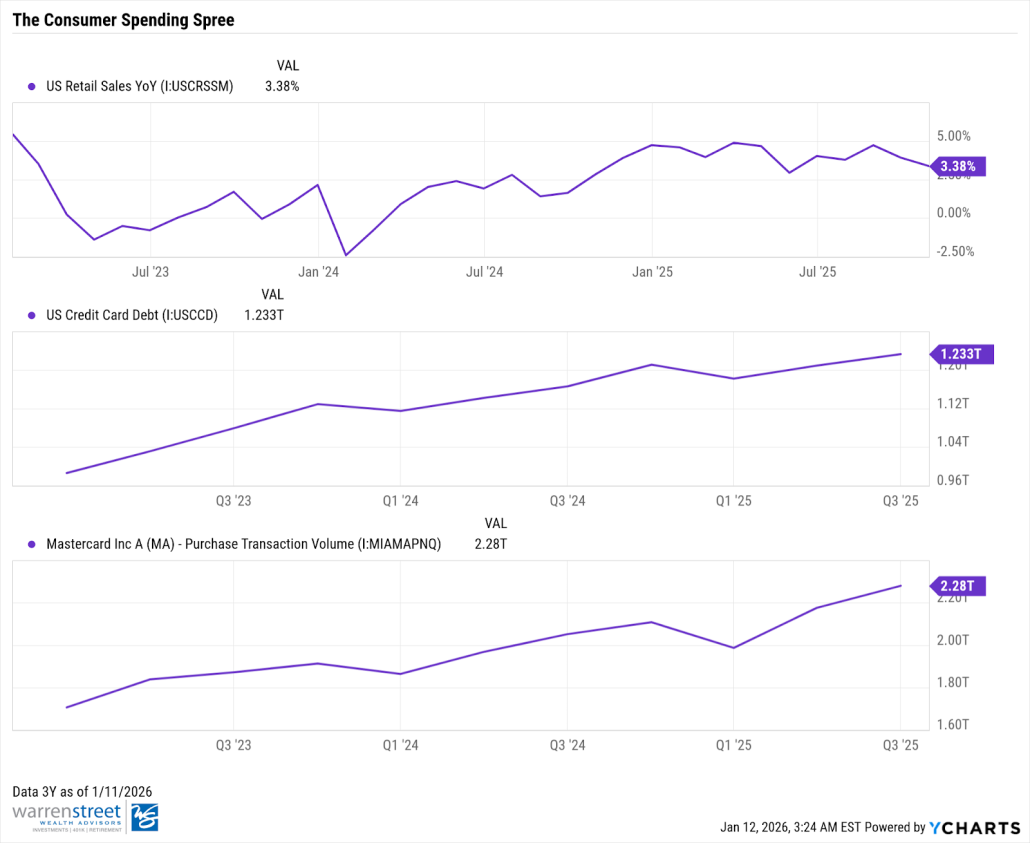

The Spending Surprise – Despite rising concerns around job security and waning sentiment, Americans are still spending. In late 2025, retail sales surged 3.5% year-over-year and we observed a healthy uptick in credit card balances.

Fiscal & Monetary Stimulus:

Heading into 2026, we’ve unlocked tax credits from the One Big Beautiful Bill (OBBB). We take estimates with a grain of salt, but if $100bn in total tax refunds and a $3,750 average tax cut per filer could further stimulate consumer spending.

The market currently anticipates two rate cuts, which will lower the cost of borrowing for both businesses and consumers (maybe more, pending Federal Reserve politics).

With a solid launching pad to start the year followed by additional liquidity in consumers pockets, we believe the US economy is well-equipped heading into 2026.

What About the Risks?

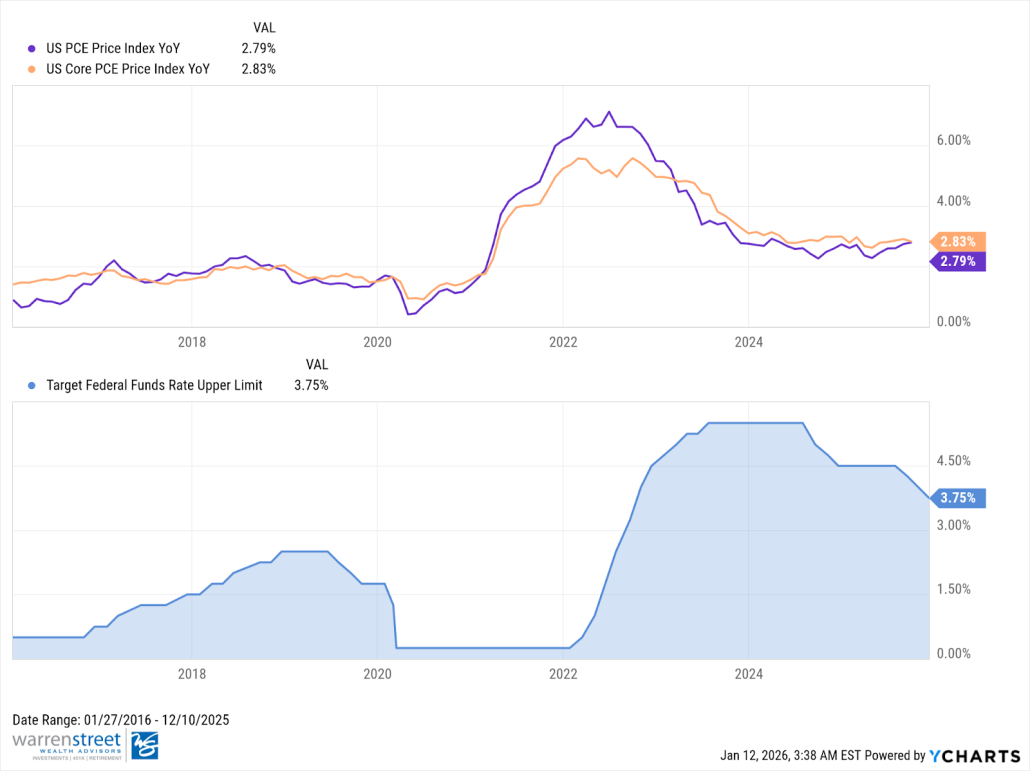

We believe the primary, non-wildcard risk to asset markets is inflation. Although inflation has stabilized from recent years, it remains sticky compared to pre-pandemic levels (around 2%), with the Fed’s preferred measure recently estimated at 2.8%.

The current economic backdrop does allow more sensitivities to a spike in inflation.

Trade fragmentation and tariffs – while most businesses seemingly absorbed the price increases of tariffs in 2025, we’ve begun to see some price hikes passed to consumers in recent inflation prints.

Is Stimulus a Double-Edged Sword? – While increased liquidity for consumers can be helpful, it may also fuel inflation. The prior stimulus checks led to double-digit drops in equities and bonds (2022) as we raised rates to fight policy-driven inflation.

Financial Repression – With US Debt-to-GDP approaching 120%, there is a risk that policymakers resort to “financial repression” – intentionally allowing higher inflation to “inflate away” the real value of government debt.

With US equities trading expensively and bonds vulnerable to inflation, I’d park this risk in the low probability, but high impact camp. To mitigate this risk, owning a portion of your portfolio to hedges (gold, commodities, natural resources) can cushion against a potential 2022 repeat.

Conclusion:

Ultimately, the backdrop seems favorable for US equity markets heading into 2026. Even if markets are frothy, the solution to managing potential excesses and drawdowns is not in timing them, but instead: a) building adequately diversified portfolios b) aligning allocations with your risk tolerance and financial objective and c) rebalancing into weakness to harness the long-term growth of capital markets at more advantageous price levels.

That’s our 2026 outlook. Our advice remains: use these investing principles as your foundation. This will allow 2026 to be less about watching tickers and more about the life you’re building. Hit that PR, read those books, or learn to cook—aim to achieve your best self. While we can recommend investments and share outlooks, there’s no substitute for investing in your own growth and happiness.

Phillip Law, CFA

Senior Portfolio Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.