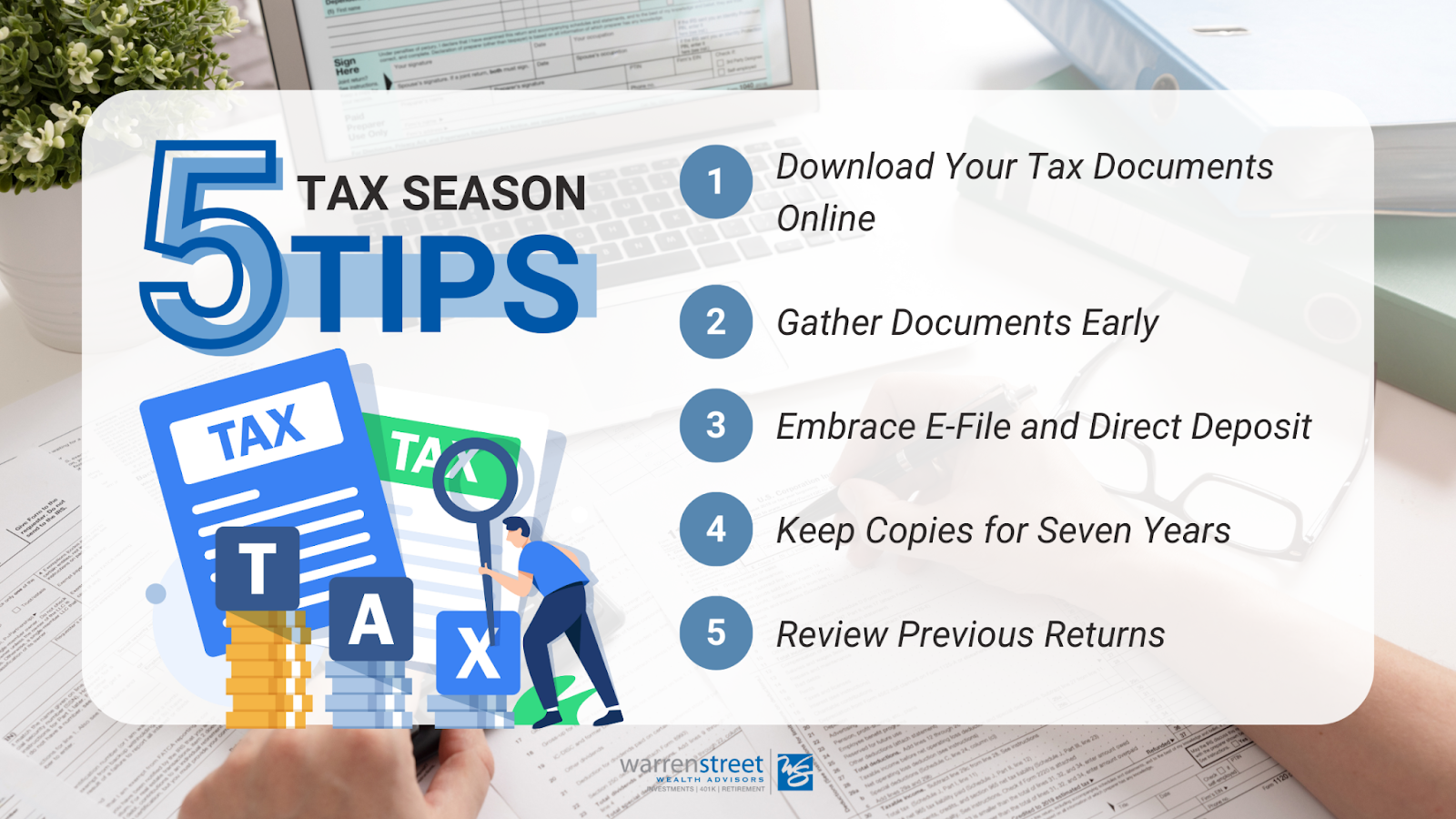

New Year, New Tax Considerations: What You Need to Know Before Filing Your 2025 Taxes

Filing your tax return may feel routine. But the devil is in the details, as they say, and those details have a pesky habit of shifting from year to year. The 2025 tax year is a good example: Rule changes this year include both incremental adjustments and larger shifts stemming from the One Big Beautiful Bill Act (OBBBA), passed in July. Understanding these changes now can help you maximize deductions, spot planning opportunities and avoid surprises when you file.

A Boost for Traditional Deductions

The OBBBA made several taxpayer-friendly provisions permanent, starting with a higher standard deduction. For 2025, the standard deduction rises to $15,750 for single filers, up from $15,000 in 2024. For married couples filing jointly, the deduction increases to $31,500, up from $30,000.

The legislation also expanded the Child Tax Credit, raising it to $2,200 per qualifying child, compared with $2,000 under prior law.

Brand New Tax Deductions

The OBBBA introduced several new deductions to be on the lookout for:

- Personal deduction for seniors: If you were born before Jan. 2, 1961, you can take a $6,000 deduction ($12,000 if married filing jointly) in addition to your standard or itemized deduction. This deduction is phased out if your modified adjusted gross income (MAGI) is between $75,000 ($150,000 for joint filers) and $175,000 ($250,000 for joint filers).

- Tax deduction for tips and overtime pay: The Trump administration has described these provisions as “no tax” on tips and overtime, but that framing oversimplifies how the new code works. In practice, there is now a deduction for voluntary cash or charged tips earned in industries where tipping is customary. From 2025 through 2028, eligible single filers can deduct up to $25,000 in tipped income, though the deduction begins to phase out for individuals with MAGI above $150,000.

A similar deduction applies to a portion of qualified overtime pay from 2025 through 2028. In most cases, this refers only to the premium portion of overtime—for example, the extra “half” in “time-and-a-half” pay—rather than the worker’s full hourly wage. For single filers, the deduction is capped at $12,500 of eligible compensation for those with MAGI below $150,000. The deduction is phased out above that amount and is zeroed out once above $275,000. - Car loan interest deduction: If you financed the purchase of a new vehicle in 2025, you may be eligible to deduct up to $10,000 in interest paid on that loan. But here’s the fine print: The vehicle must be for personal use, and it must have been built in the United States. To determine if your car fits the bill, look at your vehicle identification number (VIN). Cars built in the United States will have a VIN that starts with a 1, 4 or 5. The cap also phases out for single filers with MAGI above $100,000.

In future years, lenders will be required to report auto loan interest payments directly to both taxpayers and the IRS. For this year, you may need to do a little digging through your loan statements, or you can request a summary of interest paid from your lender.

Gift and Estate Tax Exemptions

The OBBBA gave some much-needed clarity to a crucial estate planning rule. The lifetime estate and gift tax exemption was previously scheduled to sunset at the end of the year, which would have reduced the exemption from nearly $14 million to about $6 million. Instead, the higher exemption has been made permanent. Here’s where things stand now:

- The estate and gift tax exemption is $13.99 million for 2025 and is scheduled to rise to $15 million in 2026.

- The annual gift tax exclusion is $19,000 per recipient in 2025 and will remain at that level in 2026.

While it’s too late to make a tax-free gift for 2025, now is a good time to begin planning gifting strategies for 2026.

Tax Reporting on Cryptocurrency

Beginning in 2025, the IRS now requires that crypto transactions are reported. If you sold or exchanged digital assets on a platform such as Coinbase, you should receive a Form 1099-DA. a new tax form created specifically for digital assets. Capital gains taxes may apply to crypto sales and trades. It’s also worth noting that digital currencies may be taxed as ordinary income if you receive them as payment.

It’s Not Too Late to Fund Your IRA

Your window for 2025 401(k) contributions closed at the end of the year. But if you want to pad your traditional or Roth IRA with 2025 contributions, you can do so up until the April 15 filing deadline. The contribution limit for IRAs is $7,000, but you can save an additional $1,000 if you’re 50 or older.

Planning Ahead Matters

The impact of these changes depends on your income, filing status and long-term goals. Take time now to review your situation, gather the right documentation and coordinate tax decisions with your broader financial plan to make most of the current rules. And if you have any questions, we’re here to help bring clarity and confidence as you head into the filing season.

Ernest Jones, CPA

Director of Tax, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

This is for informational purposes only and is not meant to be construed as tax advice. Please consult your accountant for advice or to review any recommendation herein. The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.