A few years ago, ads from financial services companies asked, “What’s your number?” The “number” represented the amount of money you needed to retire comfortably. There are, of course, various approaches to estimating your retirement “number,” all of which are influenced by your goals and factors, such as your expected retirement age and the lifestyle you hope to maintain in retirement. So, while this question may have been an effective way to spark conversations about retirement, we believe that it doesn’t paint the complete picture.

Retirement isn’t just about reaching a specific monetary goal. It also involves creating a comprehensive strategy that looks to optimize your various savings vehicles, each playing a different role in your retirement income approach. It also means factoring in healthcare costs, thinking about the legacy you wish to leave, and being flexible enough to adapt to life’s unexpected twists and turns. Ultimately, your strategy needs to consider how your assets will work together to fund the retirement you envision.

An essential part of orchestrating your retirement income strategy is determining which assets to take and in which order.

There is no one-size-fits-all answer, but some general guidelines can help when you are starting to think about a withdrawal strategy.

For example, one approach to consider is withdrawing money from taxable accounts first, then tax-deferred, then tax-exempt. By using taxable money first, you can avoid paying taxes as long as possible with tax-deferred investments. And your tax-exempt accounts remain tax-exempt for a longer period. Ultimately, your decision will be influenced by a wide range of other considerations, including withdrawal fees, surrender charges, and other costs that may be associated with each specific account. But when possible, consider using the power of tax deferral and tax exemption to your advantage.

Regardless of your age or financial position, having a well-thought-out retirement strategy is one of the most critical actions you can take. If you would like to review your current strategy, please contact our office. We’re here for you!

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/02/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2026-02-06 10:58:592026-02-06 10:59:05How Much Do I Need to Retire in 2026?

If you’re a business owner, you’ll eventually step away from the company you’ve built. You might cash out to the highest bidder or work out a deal to sell the business to the next generation of your family or even to employees. The question is will you be able to make this transition on your own terms? The reality is that most business owners don’t have a clear, documented exit plan. And if you find yourself among them, you could find it leaves you in a tight spot when it’s time for you to step down.

Delaying planning your exit risks settling for a below-market sale price, losing control of choosing your successor or rushing into choices that don’t reflect your vision. Delays also leave you with little time to take steps to boost the business’s valuation and ensure business continuity. A clear exit plan helps maximize options and value. If you haven’t mapped out yours yet, there’s no time like the present. Consider these steps:

Put a Price on Your Business

Proper valuation of your business is the first step in exit planning. Some back-of-the-envelope math can provide a decent starting point. But to really understand what your business is worth, meet with a valuation expert. Besides a healthy dose of objectivity, these professionals bring market expertise and a knowledge of valuation standards. They can identify intangible sources of value you may have overlooked and help ensure your valuation passes muster with potential buyers and the IRS.

There are three main approaches to determining value:

The asset approach adds up the value of your company’s tangible and intangible assets, then subtracts liabilities.

The income approach calculates value according to your business’s expected future cash flows.

The market approach compares your business to recent sales of similar companies.

You may find one approach is more apt than another for the type of business you own, but a comprehensive valuation is likely to incorporate all three in one way or another. Bear in mind that valuation isn’t a one-time event. As your business grows and market conditions change, you’ll likely want to update your valuation.

Clarify Your Vision

Before you can build an effective exit plan, it’s necessary to clarify your goals. Be as specific as possible as you define what a successful transition looks like to you.

Some questions to keep in mind: Do you want to maximize the sale price, selling at the highest price possible? Do you intend to keep the business within your family or pass it to a handpicked successor? What are your obligations to employees? Is it important that your business maintains a consistent set of values when you’re gone? What timeline makes sense for you? How involved—if at all—do you want to be with the business after you exit?

The answers to these questions will guide the decisions that follow. They can be deeply personal, and we’re here to be a resource as you consider what’s truly important to you.

Shape Your Exit

With valuation and goals in hand, there are a range of steps you can take to support your transition. What you do will depend largely on the type of exit you’re planning. For some owners, you might make strategic adjustments to boost the value of your business, such as reducing unnecessary expenses or diversifying revenue streams to make your company more attractive to buyers.

If your plan involves transferring the business to a family member or a long-time employee, the sooner you identify them, the better. That way you’ll have plenty of lead time to train them in the leadership skills necessary to provide a smooth handoff. Depending on your situation, you might consider a sale, a gift or a combination of the two. Be aware that gifts to family members above the lifetime gift and estate tax exemption ($15 million for individuals in 2026) might trigger gift taxes. Meanwhile, sales to employees could trigger capital gains taxes. If your business is structured as an S corp or C corp, you might consider an employee stock ownership plan (ESOP), which could defer or even eliminate capital gain taxes if structured properly.

Seeking an external buyer? Preparation is equally as important. In addition to boosting your valuation, you’ll need to organize your financial records, legal documents, contracts, employee agreements and operational procedures. One thing to consider is the type of deal structure that works best for you: Would you like to be paid over time or in one lump sum? And would you like to exit the company immediately or would you be open to staying on in an advisory capacity to help the new owner learn the ropes?

Begin the process of finding and vetting buyers early. These could be industry competitors, investment groups or individual entrepreneurs who may be a good fit. A business broker can help you identify potential buyers and spread the word through their network.

Charting the Future

For many business owners, exit planning rarely tops the to-do list. After all, there are plenty of day-to-day demands competing for attention, let alone the fact that it can be difficult for owners to think about the day they’ll no longer lead the company they built. Yet the most successful exits are those planned in advance, allowing owners to optimize value, identify an ideal buyer or successor, and prepare their employees for a smooth transition.

If you’d like to start a conversation about exit planning, we’d be happy to help you explore your options, develop a strategy that meets your financial goals and protects your legacy. here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/11/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-11-07 08:52:472025-11-07 08:52:58Business Exit Strategies on Your Terms

Retirement is a major life shift, one that impacts more than just your schedule. It can reshape your sense of identity, daily habits and even your health. In fact, research has shown that retirement can raise the risk of heart disease and other medical issues by up to 40%. The reason? Experts point to a loss of purpose and reduced social connection, both of which can take a toll on mental and physical well-being.

Without a plan for how to spend your time meaningfully, the transition can bring unexpected emotional challenges.

The Risks of Unstructured Retirement

Many retirees begin this new chapter with a “honeymoon phase”—a period marked by the novelty of free time, relaxation or long-awaited travel plans. But this initial high can eventually fade.

When the excitement of sleeping in and checking items off the bucket list wears off, retirees can find themselves facing unexpected emotional challenges. Common struggles include boredom, loss of routine, identity shifts and social isolation. In fact, 24% of older adults are considered to be socially isolated. Isolation can also have a ripple effect on health: It’s associated with a 50% increase in risk of developing dementia and increased risk of premature mortality.

Designing a Retirement with Purpose

To avoid some of the potential pitfalls of an unstructured retirement, it’s important to think carefully—and proactively—about purpose. What do you want this next phase of life to look and feel like? Beyond financial planning, consider how you’ll meet the deeper needs your pre-retirement life—including work and raising kids—may have fulfilled: structure, identity, accomplishment, social connection and a sense of meaning.

What brings you pleasure and meaning? What have you always wanted to try or learn? Pursuing these activities can provide purpose and help ensure retirement’s not just a long vacation, but a rewarding chapter of your life.

Feeling stuck here? Try asking close friends or family what they see light you up. Often, others can reflect back passions or strengths that are hard to see on your own.

Staying Connected and Active

Relationships and physical routines matter more than ever when you retire. Staying active, both physically and socially, offers measurable health benefits. Regular physical activity lowers risks, including the likelihood of dementia, heart disease, stroke and eight types of cancer.

People-centered activity is important, too. Look for ways to stay engaged, whether through volunteering, mentoring, part-time work, creative pursuits or community involvement. Older volunteers, aged 55 and up, who gave 100 hours or more each year were two-thirds less likely to report poor health than non-volunteers.

Spending more time with family is a high priority for many retirees and can be a great way to fulfill social needs. But make sure that vision is shared. Open conversations with loved ones about time together, expectations and boundaries can help align plans and avoid disappointment down the road.

The Retirement Identity Shift

In many ways, it’s hard to define what retirement is. After all, it’s not a single moment but a series of transitions. For instance, rather than an abrupt shift to not working at all, you may consider bridge employment—usually part-time work in a temporary position or as a consultant in your field or in a different industry. This can offer a gradual shift into retirement, providing continued income and engagement as you adjust.

As your vision for retirement evolves, keep us in the loop. We’d love to hear what you’re planning—and we’re here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-5.png11522048Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-09-26 07:38:002025-10-07 16:02:46The Power of Purpose in Retirement

As a business owner, you’ve spent your life’s work growing your business, taking care of employees, managing your product or service, and looking after your people. Now, you may be getting to a point where your spouse tells you you work too much. Or perhaps you’re watching the clock more than you used to, counting down the minutes until you can head home and unplug from your “boss” responsibilities.

Whatever your reasoning, if you’re starting to ask questions like, “Do I have enough to sell?” and “Will that be enough?” then it’s time to focus on you for a change.

Why Business Owners Need Specialized Financial Planning

Business owners face a unique set of financial challenges and opportunities. Whether you are a small business owner or running a large corporation, the following considerations are critical:

Maximizing tax efficiency

Choosing the most appropriate retirement account type

Evaluating your retirement account options

Managing 401(k) and pension investments

Considering a defined benefit plan, i.e., “pension”

Aligning company benefits offerings with company goals

Our team specializes in helping business owners handle these and other issues while they’re still working. During those years, we help you work through proper planning techniques to diversify your assets, reduce risk, optimize your taxes, and offer competitive benefits. All of these steps help streamline and strengthen your business at the time — but they also set you up for a successful transition into retirement or your next business opportunity.

When you do get to the point of exiting, we help you bring all of this planning together into one critical decision: whether or not you have what you need to move on from your business and into your ideal retirement, whatever that looks like for you.

Creating a Dream Retirement

At Warren Street, we’ve helped many business owner clients over the years answer the “Do I have enough to sell?” question and develop their exit strategies accordingly.

If you choose to work with us during your own exit process, we’ll play a key role on your professional team alongside your attorney. While your attorney looks after the legal structure of the deal, we’ll handle related asset management and tax mitigation. For example, if you’re involved in an all-cash sale with multiple payments coming in the next few years, we will discuss tax deferral opportunities to add into your transition plan. Or, if you’re struggling with a go/no-go decision, we’ll conduct scenario planning to help you make an informed choice based on your current financial situation, projected future state, and personal goals.

No matter where you are in the exit planning process, we can help evaluate your current assets, investments, estate planning, and legacy goals, so you can make a clear and confident decision on what next steps are right for you.

If this sounds like you and you’re a current Warren Street client, please mention your interest to your Lead Advisor! Or, if you’re not a client but are interested in learning how we can help, schedule a complimentary introductory call with us. We hope to hear from you and look forward to exploring how we can make your post-exit dreams a reality.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/12/Do-I-Have-Enough-To-Sell.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-12-28 08:24:002024-06-03 10:46:08Do I Have Enough to Sell My Business?

As a retired Chevron employee and financial advisor, I’m constantly keeping my finger on the pulse of what’s happening at the company. Last month, Chevron sent a letter to employees announcing that, as of June 1, the funds in their retirement plans will be changing.

Given these updates, I wanted to take the time to make sure my Chevron connections understand what’s happening — and what it could mean for your portfolio.

What’s changing?

The gist is this: on June 1, 2023, your Fidelity NetBenefits account will reflect new investment choices. In many cases, your money will be automatically allocated to new funds. For example, If you’re currently in a Vanguard Target Retirement Date Fund, this will map to a BlackRock LifePath® Index Fund. All in all, the 16 existing investment choices will be funneled down into just 11 choices. This applies to both the Employee Savings Investment Plan (ESIP) and Deferred Compensation Plan (DCP).

In my opinion, the most impactful change is the consolidation of three equity funds — Vanguard 500 Index, Vanguard Large Cap Value Index, and Vanguard PRIMECAP — into just one equity fund, the “Equity Index.” This is tricky, because for many people, it made sense to hold a pure S&P 500 fund such as the Vanguard 500 Index. Pure S&P 500 funds allow you to “own” the largest 500 companies in the US, compared to the “Equity Index,” which is more of a mix.

We are currently investigating this and the other new funds to understand exactly what they entail and how they will interact with the rest of your portfolio.

What should you do?

This fund consolidation is neither good nor bad; however, it does mean that you should talk to an advisor about the impact it will have on your portfolio. The new funds have different risk and return profiles, expense ratios, and diversification characteristics than the old funds, and they’re not necessarily a direct map. It’s critical that you confirm your new funds still support your future retirement goals.

No matter your age or retirement goals, it’s always a good practice to review your 401(k) plan on a regular basis and make sure it still aligns with your needs. The updates to the Chevron 401(k) plans are a good reminder to take a close look at yours and make any necessary changes.

If you don’t already have an advisor or are looking for a new one, I’m also happy to speak with you (no charge) about your portfolio. I’ve been helping Chevron colleagues and clients for more than 40 years and am an expert on the company’s employee benefits package. I’m available to answer any questions you have about the upcoming changes.

Feel free to give me a call at 714-876-6200 or book time with me if you’d like to chat. I hope to hear from you and am here to help!

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/05/Chevron-401k-Changes-Thumbnail.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2023-05-19 07:30:002023-05-18 10:07:43Chevron 401(k) Changes: Unpacking Your New Funds

As a former Chevron employee and current financial advisor, I know firsthand that planning for retirement can be daunting. You might be asking yourself questions like:

How do I anticipate all the different factors that go into retirement?

How much money is enough?

What if I have an unexpected expense in retirement?

If you’re feeling like 2023 is your year but are afraid to take the plunge, read on. These are the top three considerations I discuss with my Chevron friends and clients when they ask me those questions.

1. Wait until at least age 55.

Every case is different, but in general, it’s best to wait until at least age 55 to retire. Every year you wait increases the likelihood you won’t run out of money.

Talk to your advisor about scenario planning (more on that in the next point) to figure out what age makes sense for your specific situation. And remember, there are always exceptions to this advice if it’s a matter of your health or other serious issues.

2. Determine your post-retirement budget.

When you picture your life in retirement, what does it look like? Are you jet-setting the world with your spouse, or enjoying a quiet life at home with your grandkids? Working a part-time job to stay busy, or finally pursuing your hobbies and passions full-time? Upgrading to the big truck you always had your eye on, or getting every last mile out of your current ride?

These are important considerations, as they’ll impact the amount of money you’ll need in retirement. If you think you’ll have similar cash flow needs in retirement as now, that’s important to know. Or, if you anticipate boosting your spending on vacations, supporting other family members, etc., that also needs to be taken into account. Once you have determined your budget needs pre- and post-retirement, your advisor can help you put together a strategy around your paychecks, how much to save in the plan, and what number you need to hit to retire.

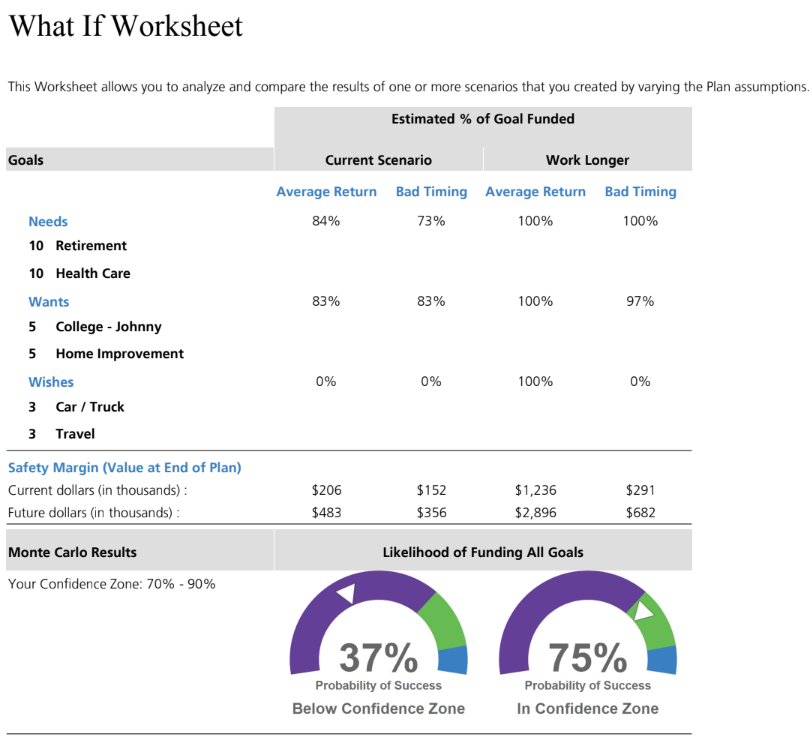

3. Do scenario planning.

We offer free scenario planning, called a Monte Carlo analysis, to help clients measure whether they could retire successfully. This simulation runs thousands of different scenarios based on your personal financial data. Then, it analyzes your “probability of success” in reaching the amount of money you’ll need at your desired retirement age. Best of all, this is a key tool for answering the question, “How much money do I need to retire?”

Whether it’s with Warren Street or another financial advisor, ask your advisor to help you put together a plan that accounts for these different situations, so you can set yourself up for success. As long as you have the relevant information ready to share with us — such as your current assets, expected savings, and time horizon — the analysis process takes no longer than 30 minutes. That’s a short amount of time to invest in your peace of mind!

Many Chevron employees are looking to retire this year, especially given that Chevron stock prices have generally held up. Whether you’re in the “this is my year” camp or still have another five years in you, I’d love to talk with you. Let’s put the numbers together and see what’s possible. I’m here to answer your questions and help you run the numbers, but the final decision is always yours.

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/02/How-to-Retire-in-2023-Chevron-Webinar.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2023-02-24 08:30:002024-11-07 09:24:13Chevron Employees: How to Retire in 2023

Tax planning for your retirement savings is also important. To help with that, you can typically choose between two account types as you save for retirement: Traditional IRA or employer-sponsored plans, or Roth versions of the same.

All Things Roth

Either way, your retirement savings grow tax-free while they’re in your accounts. The main difference is whether you pay income taxes at the beginning or end of the process. For Roth accounts, you typically pay taxes up front, funding the account with after-tax dollars. Traditional retirement accounts are typically funded with pre-tax dollars, and you pay taxes on withdrawals.

That’s the intent, anyway. To fill in a few missing links, the SECURE 2.0 Act:

Eliminates Required Minimum Distributions for employer-sponsored Roth accounts, such as Roth 401(k)s and Roth 403(b)s, to align with individual Roth practices (2024)

Establishes Roth versions of SEP and SIMPLE IRAs (2023)

Lets employers make contributions to traditional and Roth retirement accounts (2023)

Lets families potentially move 529 plan assets into a Roth IRA (2024 – as described above)

There’s one thing that’s not changed, although there’s been talk that it might: There are still no restrictions on “backdoor Roth conversions” and similar strategies some families have been using to boost their tax-efficient retirement resources.

Speaking of RMDs

Not surprisingly, the government would prefer you eventually start spending your tax-sheltered retirement savings, or at least pay taxes on the income. That’s why there are rules regarding when you must start taking Required Minimum Distributions (RMDs) out of your retirement accounts. That said, both SECURE Acts have relaxed and refined some of those RMD rules.

Extended RMD Dates (2023): the original SECURE Act postponed when you must start taking taxable RMDs from your retirement account—from 70 ½ to 72. The SECURE 2.0 Act extends that deadline further. If you were born between 1951–1959, you can now wait until age 73. If you were born after that, it’s age 75.

Reduced Penalties (2023): If you fail to take an RMD, the penalty is reduced from a whopping 50% of the distribution to a slightly more palatable 25%. Also, the penalty may be further reduced to 10% if you fix the error within a prescribed correction window.

Aligned RMD Rules for Personal and Employer-based Roth Accounts (2024): As mentioned above, RMDs have been eliminated from employer-based Roth accounts. If you’ve already been taking them, you should be able to stop doing so in 2024.

Enhanced RMDs for Surviving Spouses (2024): If you are a widow or widower inheriting your spouse’s retirement plan assets, you will be able to elect to determine your RMD date as if you were your spouse. This provision can work well if your spouse was younger than you. As described here: “RMDs for the [older] surviving spouse would be delayed until the deceased spouse would have reached the age at which RMDs begin.”

An Addendum For Charitable Donors

One good thing hasn’t changed with SECURE 2.0: Even though RMD dates have been extended as described, you can still make Qualified Charitable Distributions (QCDs) out of your retirement accounts beginning at age 70 ½, and the income is still excluded from your taxable adjusted gross income, as well as from Social Security tax and Medicare surcharge calculations. Plus, beginning in 2024, the maximum QCD you can make (currently $100,000) will increase with inflation. Also, with quite a few caveats, you will have a one-time opportunity to use a QCD to fund certain charitable trusts or annuities.

Next Steps

How else can we help you incorporate SECURE 2.0 Act updates into your personal financial plans? The landscape is filled with rabbit holes down which we did not venture, with caveats and conditions to be explored. And there are a few provisions we didn’t touch on here. As such, before you proceed, we hope you’ll consult with us or others (such as your accountant or estate planning attorney) to discuss the details specific to you.

Come what may in the years ahead, we look forward to serving as your guide through the ever-evolving field of retirement planning. Please don’t hesitate to reach out to us today with your questions and comments.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

It can be hard to save for your future retirement when current expenses loom large. We advise proceeding with caution before using retirement savings for any other purposes, but SECURE 2.0 does include several new provisions to help families strike a balance.

Student Loan Payments Count as Elective Deferrals (2024): If you’re paying off student debt and trying to save for retirement, your student loan payments will qualify as elective deferrals in your company plan. This means, whether you contribute to your company retirement plan or you make student loan payments, your employer can use either to make matching contributions to your retirement account.

Transferring 529 Plan Assets to a Roth IRA (2024): This one is subject to a number of qualifying hurdles, but SECURE 2.0 establishes a path for families to transfer up to $35,000 of untapped 529 college saving plan assets into the beneficiary’s Roth IRA. With proper planning, this may help families “seed” their children’s or grandchildren’s retirement savings with their unspent college savings.

New Emergency Saving Accounts Linked to Employer Plans (2024): SECURE 2.0 has established a new employer-sponsored emergency savings account, which would be linked to your retirement plan account. Unless you are a “highly compensated employee” (as defined by the Act), you can use the account to save up to $2,500, with your contributions counting toward matching funds going into your main retirement plan account.

Relaxed Emergency Plan Withdrawals (2024): SECURE 2.0 relaxes the ability to take a modest emergency withdrawal out of your retirement plan. Essentially, as long as you self-certify that you need the money, you can take up to $1,000 in a calendar year, without incurring the usual 10% penalty for early withdrawal. Once you’ve taken an emergency withdrawal, there are several hurdles before you’re eligible to take another one.

Additional Exceptions to the 10% Retirement Plan Withdrawal Penalty (Varied): SECURE 2.0 has established new exceptions to the 10% penalty otherwise incurred if you tap various retirement accounts too soon. For example, there are several new types of public safety workers who can access their company retirement plans penalty-free after age 50. Various exceptions are also carved out if you’re terminally ill or a domestic abuse victim, or if you use the assets to pay for long-term care insurance. The Act also has modified how retirement plan assets are to be used for Qualified Disaster Recovery Distributions. Many of the new exceptions are fairly specific, so check the fine print before you proceed.

Relaxed Emergency Loans from Retirement Plans (2023): If you end up living in a Federally declared disaster area, SECURE 2.0 also increases your ability to borrow up to 100% of your vested plan balance up to $100,000, with a more generous pay-back window.

Expanded Eligibility for ABLE Accounts (2026): ABLE accounts help disabled individuals save for disability expenses, while still collecting disability benefits. Before, you had to be disabled before age 26 to establish an ABLE account. That age cap increases to 46.

A Tax Break for Disabled First Responders (2027): If you are a first responder collecting on a service-connected disability, at least a portion of your disability payments will remain tax-free, even once you reach full retirement age and begin taking a retirement pension.

Next Steps

If you missed the first part of the blog series, we discussed key provisions in the newly enacted SECURE 2.0 Act of 2022, including updates that impact (1) savers/investors and (2) employers/plan sponsors. Check in next week for the last part of this blog series, where we share tax planning tips under this new Act.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Who doesn’t enjoy tying up year-end loose ends? The original SECURE Act was signed into law on December 20th, 2019. Its “sequel,” the SECURE 2.0 Act, was similarly enacted at year-end on December 29th, 2022.

Both pieces of legislation seek to reform how Americans prepare for retirement while juggling current spending needs. How, when, or will each of us retire? How can government incentives, regulations, and safety nets help more people safely do so—or at least not get in the way?

These are questions we’ve been asking as a nation for decades, across shifting socioeconomic climates. Throughout, a hard truth remains:

Employers and the government play a role in helping you save for and spend in retirement, but much of the preparation ultimately falls on you.

Neither the original SECURE Act nor SECURE 2.0 has fundamentally changed this reality. SECURE 2.0 has, however, added far more motivational carrots than punishing sticks. Its guiding goal is right there in the name: Setting Every Community Up for Retirement Enhancement (SECURE). Following is an overview of its key components.

Note: Implementation for each SECURE 2.0 provision varies from being effective immediately, to ramping up in future years. A few even apply retroactively. Many of its newest programs won’t effectively roll out until 2024 or later, giving us time to plan. We’ve noted with each provision when it’s slated to take effect.

Saving More, Saving Better: Individual Savers

First, key provisions include several updates to encourage individual savers:

Expanded Auto-Enrollment Requirements (2025): Because you’re more likely to save more if you’re automatically added to your company retirement plan program, auto-enrollment will be required for additional new retirement plans. Even with auto-enrollment, you can still opt out individually. Also, the Act has made a number of exceptions to the rules, including, as described here, “employers less than 3 years old, church plans, governmental plans, SIMPLE plans, and employers with 10 or fewer employees.”

Higher Catch-Up Contributions (2024–2025): To accelerate retirement saving as you approach retirement age, SECURE 2.0 Act has increased annual “catch-up” contribution allowances for many retirement accounts (i.e., extra amounts allowed beyond the standard contribution limits); and, importantly, tied future increases to inflation. However, in many instances, the updates also require high-wage-earners ($145,000/year or higher) to direct their catch-up contributions to after-tax Roth accounts.

Faster Plan Participation for Part-Time Employees (2024): If you’re a long-term, part-time employee, the SECURE Act of 2019 made it possible for you to participate in your employer’s retirement plan. With SECURE 2.0, you’ll be eligible to participate after 2 years instead of 3 years (after meeting other requirements).

Saver’s Match for Low-Income Savers (2027): A Saver’s Credit for low-income families will be replaced by a more accessible Saver’s Match for those whose income levels qualify. While the credit offsets income on a tax form, the match will be a direct contribution into your retirement account, of up to $1,000 in government-paid matching funds.

An Expanded Contribution Window for Sole Proprietors (2024): If you’re a sole proprietor, you’ll be able to establish a Solo 401(k) through the current year’s Federal income tax filing date, and still fund it with prior-year contributions.

Potential Tax Error “Do Overs” (2025): To err is human, and often unintentional. As such, SECURE 2.0 has directed the IRS to apply an existing Employer Plans Compliance Resolutions System (EPCRS) to employer-sponsored plans and to IRAs. The details are to be developed, but as described here, the intent is to set up a system in which “most inadvertent failures to comply with tax-qualification rules would be eligible for self-correction.”

Finding Former Plans (2024): It can be hard for company plan sponsors to keep in touch with former employees—and vice-versa. SECURE 2.0 has tasked the Dept. of Labor with hosting a national “lost and found” database to help you search for plan administrator contact information for former employees’ plans, in case you’ve left any retirement savings behind.

Saving More, Saving Better: Employers

There also are provisions to help employers offer effective retirement plan programs:

Better Retirement Plan Start-Up Incentives (2023): Small businesses can take retirement plan start-up credits to offset up to 100% of their plan start-up costs (versus a prior 50% cap). Also, businesses with no retirement plan can apply for start-up credits if they join a Multiple Employer Plan (MEP)—and this one applies retroactively to 2020.

A New “Starter 401(k)” Plan (2024): The Starter 401(k) provides small businesses that lack a 401(k) plan a simpler path to establishing one. Features will include streamlined regulatory and reporting requirements; auto-enrollment for all employees starting at 3% of their pay; a $6,000 annual contribution limit, rising with inflation; and a deferral-only structure, meaning the plan does NOT permit matching employer contributions.

Expanded SIMPLE Plan Contributions (2024): Under certain conditions, SECURE 2.0 allows for additional employer contributions to, and higher participant contribution limits for SIMPLE IRA plans.

New Household Employee Plans (2023): Families can establish SEP IRA plans for their household employees, such as nannies or housekeepers.

Small Perks (2023): Until now, employers were prohibited from offering even small incentives to encourage employees to step up their retirement savings. Now, de minimis perks are okay, such as a gift card when a participant increases their deferral amount.

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/01/Secure-Act-2.0-Summary-for-Individuals-and-Employers.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2023-01-09 09:25:002023-01-18 09:01:04Secure Act 2.0: Summary for Individuals and Employers

With Chevron’s (CVX) stock price hovering around $185 (as of 11/22/22), I’ve been actively calling my clients to vet their interest in selling stock to diversify their portfolios.

It’s worth noting that we’re not talking about Employee Stock Ownership Plan (ESOP) shares, which are tax advantaged. Those are generally advisable to hold onto long-term.

But when it comes to shares of common stock, this might be the time to sell — or at least take a little off the top. It’s tempting from a psychological standpoint — i.e., recency bias — to want to stick around and see how long the stock price climbs. But you have to be willing to ask yourself the “what ifs:”

What if the war in Ukraine ends?

What if Chevron shares go back to $100 as a result of oil prices dropping?

How would I feel if I held out thinking the price was going to hit $200, and it drops back to $100?

In this blog post, we’ll unpack these questions, as well as share considerations for your decision.

How Will You Feel?

One of the most important questions to ask yourself is how you’ll feel in these what-if scenarios. Sure, Chevron’s stock price could keep going up and make you more money when you sell. But what if it doesn’t? What if the war ends and it drops to $100 overnight? Will you still be able to retire when you want to?

We all tend to have a very short memory span. It wasn’t that long ago that the global economy was going haywire due to Covid. Chevron stock was at $59 a share, because oil wasn’t worth anything. People weren’t traveling, and there was no place to store the oil.

If another wave of Covid hit or the war in the Ukraine ended — where would Chevron be? If the stock price plummeted back below $100, you might be kicking yourself. Or, worse, you may have to work several more years than you planned before retirement.

What Do You Fear?

If you’re confident that you could still retire on time, even if Chevron stock went back to $100, that’s fine. But most people would rather diversify now than risk having to work another five years.

Even if you’re confident that Chevron’s stock price will stay elevated, think about Apple and Amazon. As strong as those tech giants are, their stocks have taken big hits over the years. If employees had all their retirement savings invested in those companies, any one of those stock hits could have drastically slashed those employees’ savings and postponed their retirement dates.

Visualize the What-Ifs

If you don’t have a good sense for whether or not you could retire, it might be time to do some scenario planning. Ask your advisor to conduct a Monte Carlo analysis to help you understand different scenarios. Monte Carlo simulations essentially run hundreds of different scenarios to help you understand the probability of successfully reaching your goals (retirement or otherwise) in the midst of unknown variables.

Another visual that can be helpful is to think of your stock in “chunks” to sell. We can help you put together a plan to sell a certain percentage of your stock over time. That way, you can still capture some of the upside if the stock continues to climb, but also protect yourself if it plummets.

You don’t necessarily need to sell all your Chevron stock, but it’s a good idea to at least start diversifying. We would recommend putting your money to work in both the stock and bond markets and can recommend a model portfolio for you that suits your needs, timeline, and risk tolerance. Diversification is key to making sure you stay on track with your goals and can retire when you want.

As you can tell, your decision about whether or not to sell your Chevron stock doesn’t have to be black or white. If you want to explore options, just want to talk through your situation, or would like to run a Monte Carlo simulation to help with scenario planning, we’re here to help in whatever way we can.

If you’d like to chat, please click here to schedule a complimentary consultation with me.

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/11/Blog-Thumbnail.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2022-11-30 08:51:412022-11-30 09:01:24Update: Should I Sell Some of My Chevron Stock?