A few years ago, ads from financial services companies asked, “What’s your number?” The “number” represented the amount of money you needed to retire comfortably. There are, of course, various approaches to estimating your retirement “number,” all of which are influenced by your goals and factors, such as your expected retirement age and the lifestyle you hope to maintain in retirement. So, while this question may have been an effective way to spark conversations about retirement, we believe that it doesn’t paint the complete picture.

Retirement isn’t just about reaching a specific monetary goal. It also involves creating a comprehensive strategy that looks to optimize your various savings vehicles, each playing a different role in your retirement income approach. It also means factoring in healthcare costs, thinking about the legacy you wish to leave, and being flexible enough to adapt to life’s unexpected twists and turns. Ultimately, your strategy needs to consider how your assets will work together to fund the retirement you envision.

An essential part of orchestrating your retirement income strategy is determining which assets to take and in which order.

There is no one-size-fits-all answer, but some general guidelines can help when you are starting to think about a withdrawal strategy.

For example, one approach to consider is withdrawing money from taxable accounts first, then tax-deferred, then tax-exempt. By using taxable money first, you can avoid paying taxes as long as possible with tax-deferred investments. And your tax-exempt accounts remain tax-exempt for a longer period. Ultimately, your decision will be influenced by a wide range of other considerations, including withdrawal fees, surrender charges, and other costs that may be associated with each specific account. But when possible, consider using the power of tax deferral and tax exemption to your advantage.

Regardless of your age or financial position, having a well-thought-out retirement strategy is one of the most critical actions you can take. If you would like to review your current strategy, please contact our office. We’re here for you!

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/02/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2026-02-06 10:58:592026-02-06 10:59:05How Much Do I Need to Retire in 2026?

When you’re deciding when to start claiming Social Security benefits, you’re facing a trade-off. Claim as early as age 62, and you’ll receive a larger number of smaller payments. Delay as late as age 70, and you’ll receive a smaller number of larger payments. To weigh your options, it’s helpful to find your “break-even” point—the age at which waiting longer to claim Social Security will result in a greater lifetime benefit.

Picking the Right Horse

To begin, here’s a little scenario to help illustrate what a break-even is. Imagine a race between two horses—Early Bird (No. 62) and Late Breaker (No. 70). Late Breaker is a faster horse than Early Bird, no question. So to keep the competition interesting, Early Bird gets a half-lap head start.

We know that, given enough time, Late Breaker will eventually catch up to Early Bird. Let’s call that moment the break-even. If the race ends any time after that break-even point, Late Breaker is a sure thing. If the race ends any time before the break-even, all the smart money is on Early Bird.

We can think of the way Social Security benefits accumulate in a similar way. Claiming early gives you a head start in accumulating benefits, but they come at a slower pace. Claiming later can earn you bigger checks, but it will take time before it catches up to the total accumulated benefits of claiming earlier. If you live past that break-even point, you will ultimately receive more income by claiming later. If you don’t, you will receive more by claiming earlier.

A Concrete Example

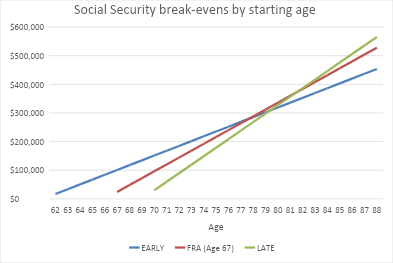

In reality, there are more than two horses in a race, and there are more than two options for when to start claiming Social Security benefits. In fact, you can choose any point after you reach your early retirement age of 62. For every year between the ages of 62 and 70, your monthly benefits will increase. (You can wait longer than age 70, but your benefits won’t continue to grow.) Any two points between ages 62 and 70 will have their own break-even.

Let’s consider three scenarios:

1. You claim your benefits at age 62.

2. You wait until full retirement age (67 for anyone born in 1960 or later) to claim.

If you chart the accumulated benefits of those three scenarios on a line graph, you’ll find the break-evens where the lines intersect:

You’ll notice that the break-even between claiming at 62 and claiming at 67 is around age 78. Meanwhile, the break-even between claiming at 67 and claiming at 70 is around age 82, and the break-even between claiming at 62 and claiming at 70 is around age 80.

There’s a lot of math to consider—including a key variable we haven’t discussed: how long you expect to live. If you expect to live past 78, claiming benefits at full retirement age may be worth more over time than claiming at 62. If you expect to live past 83, then claiming benefits at age 70 may be worth more over time than claiming at 67. If you expect to live past 80, then claiming benefits at age 70 may be worth more over time than claiming at 62.

Of course, none of us can predict our life expectancy with any certainty. But we can make some educated guesses based on factors like our current health and our family medical history. For instance, if both of your parents lived well into their 90s, you might have more confidence in your own life expectancy.

Other Important Considerations

Break-evens are a useful tool in deciding when to start claiming Social Security benefits, but they aren’t the only factor. For example, you may prefer to have more money in the early part of your retirement so you can spend more on the experiences money can buy. Coming out ahead in the final tally may be less important to you.

Depending on your specific circumstances, there may be strategic reasons to claim early or claim late—say, to reduce your tax burden or to fill in a necessary income gap. These reasons make this decision about more than simply pitting your expected longevity against different break-even points.

We don’t expect you to calculate break-evens for every possible scenario. Understanding the concept of break-even will help you take a more informed approach to this important decision on your retirement journey. We’re happy to work with you to do the math for different claiming strategies and how they might fit in with your larger financial picture and retirement goals. As always, the best choice is the one that makes the most sense for you.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/11/image-2.png11522048Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-12-09 13:04:382025-12-09 13:04:47Claiming Social Security: What’s a Break-Even?

If you’re a business owner, you’ll eventually step away from the company you’ve built. You might cash out to the highest bidder or work out a deal to sell the business to the next generation of your family or even to employees. The question is will you be able to make this transition on your own terms? The reality is that most business owners don’t have a clear, documented exit plan. And if you find yourself among them, you could find it leaves you in a tight spot when it’s time for you to step down.

Delaying planning your exit risks settling for a below-market sale price, losing control of choosing your successor or rushing into choices that don’t reflect your vision. Delays also leave you with little time to take steps to boost the business’s valuation and ensure business continuity. A clear exit plan helps maximize options and value. If you haven’t mapped out yours yet, there’s no time like the present. Consider these steps:

Put a Price on Your Business

Proper valuation of your business is the first step in exit planning. Some back-of-the-envelope math can provide a decent starting point. But to really understand what your business is worth, meet with a valuation expert. Besides a healthy dose of objectivity, these professionals bring market expertise and a knowledge of valuation standards. They can identify intangible sources of value you may have overlooked and help ensure your valuation passes muster with potential buyers and the IRS.

There are three main approaches to determining value:

The asset approach adds up the value of your company’s tangible and intangible assets, then subtracts liabilities.

The income approach calculates value according to your business’s expected future cash flows.

The market approach compares your business to recent sales of similar companies.

You may find one approach is more apt than another for the type of business you own, but a comprehensive valuation is likely to incorporate all three in one way or another. Bear in mind that valuation isn’t a one-time event. As your business grows and market conditions change, you’ll likely want to update your valuation.

Clarify Your Vision

Before you can build an effective exit plan, it’s necessary to clarify your goals. Be as specific as possible as you define what a successful transition looks like to you.

Some questions to keep in mind: Do you want to maximize the sale price, selling at the highest price possible? Do you intend to keep the business within your family or pass it to a handpicked successor? What are your obligations to employees? Is it important that your business maintains a consistent set of values when you’re gone? What timeline makes sense for you? How involved—if at all—do you want to be with the business after you exit?

The answers to these questions will guide the decisions that follow. They can be deeply personal, and we’re here to be a resource as you consider what’s truly important to you.

Shape Your Exit

With valuation and goals in hand, there are a range of steps you can take to support your transition. What you do will depend largely on the type of exit you’re planning. For some owners, you might make strategic adjustments to boost the value of your business, such as reducing unnecessary expenses or diversifying revenue streams to make your company more attractive to buyers.

If your plan involves transferring the business to a family member or a long-time employee, the sooner you identify them, the better. That way you’ll have plenty of lead time to train them in the leadership skills necessary to provide a smooth handoff. Depending on your situation, you might consider a sale, a gift or a combination of the two. Be aware that gifts to family members above the lifetime gift and estate tax exemption ($15 million for individuals in 2026) might trigger gift taxes. Meanwhile, sales to employees could trigger capital gains taxes. If your business is structured as an S corp or C corp, you might consider an employee stock ownership plan (ESOP), which could defer or even eliminate capital gain taxes if structured properly.

Seeking an external buyer? Preparation is equally as important. In addition to boosting your valuation, you’ll need to organize your financial records, legal documents, contracts, employee agreements and operational procedures. One thing to consider is the type of deal structure that works best for you: Would you like to be paid over time or in one lump sum? And would you like to exit the company immediately or would you be open to staying on in an advisory capacity to help the new owner learn the ropes?

Begin the process of finding and vetting buyers early. These could be industry competitors, investment groups or individual entrepreneurs who may be a good fit. A business broker can help you identify potential buyers and spread the word through their network.

Charting the Future

For many business owners, exit planning rarely tops the to-do list. After all, there are plenty of day-to-day demands competing for attention, let alone the fact that it can be difficult for owners to think about the day they’ll no longer lead the company they built. Yet the most successful exits are those planned in advance, allowing owners to optimize value, identify an ideal buyer or successor, and prepare their employees for a smooth transition.

If you’d like to start a conversation about exit planning, we’d be happy to help you explore your options, develop a strategy that meets your financial goals and protects your legacy. here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/11/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-11-07 08:52:472025-11-07 08:52:58Business Exit Strategies on Your Terms

Choosing a health care plan at work can be a bit of a headache—charts comparing premiums, copays and deductibles isn’t exactly light reading. One option you might have encountered in this process is the high-deductible health plan (HDHP). The name might sound intimidating. After all, who really wants to pay high deductibles? But when paired with a health savings account (HSA), an HDHP can be a powerful tool to help you save for your health care now and your future.

What is an HDHP?

An HDHP is a type of health insurance plan that comes with lower monthly premiums but higher out-of-pocket costs. In other words, you’ll pay less each month, but you’ll be on the hook for more when you actually visit a doctor. These plans shift more financial risk to you in exchange for upfront savings—and they often come with access to an HSA.

An HSA allows you to set aside pre-tax money to pay for qualified medical expenses like doctor visits, prescriptions, dental care and vision services. Unlike a flexible spending account (FSA), which is “use it or lose it,” the money in an HSA is yours to keep. It rolls over from year to year, stays with you if you change jobs and often has investment options.

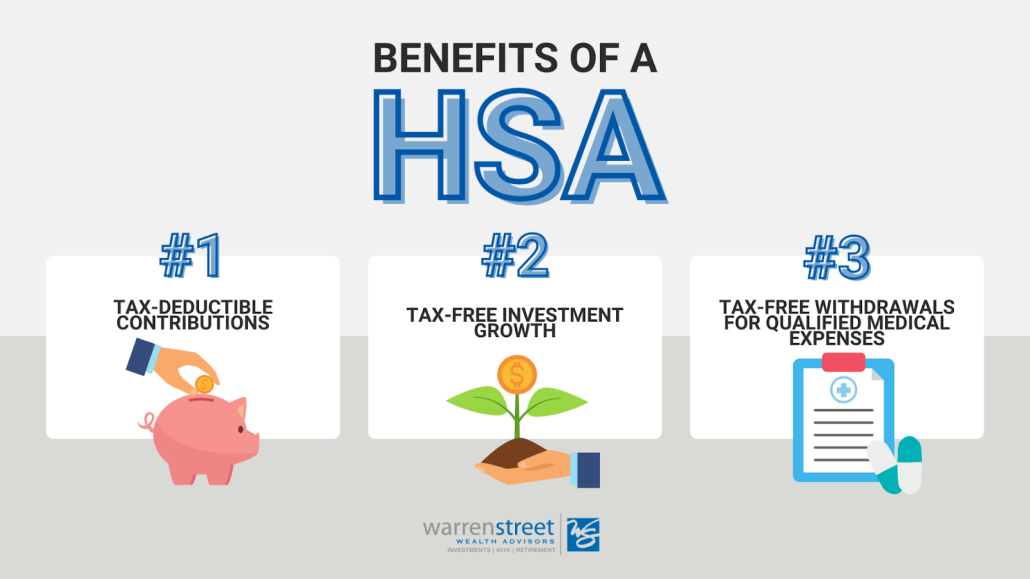

What makes HSAs especially appealing are their triple tax benefits:

Tax-deductible contributions.

Tax-free growth on investments inside the HSA.

Tax-free withdrawals at any time if the money is used for qualified medical expenses.

These features make HSAs one of the most tax-efficient savings vehicles available. But there’s another way to get more from your HSA: It can serve as a powerful retirement savings vehicle.

Should You Use a High-Deductible Health Plan?

Before we get to the benefits of an HSA as an investment vehicle, how do you decide whether to use an HDHP in the first place? Choosing between a traditional plan and an HDHP depends on a few key factors.

First, compare the total potential cost under each plan. That means looking at monthly premiums, deductibles, coinsurance and out-of-pocket maximums. HDHPs typically offer significantly lower monthly premiums but come with higher deductibles. If you’re generally healthy and don’t expect to need much medical care, this tradeoff could work in your favor.

But be honest with yourself about your cash flow. If you had a sudden medical emergency, would you be able to cover the high out-of-pocket costs until your insurance kicks in? For people with chronic health conditions or frequent doctor visits, a traditional plan might offer more predictable costs.

Using an HSA as a Retirement Account

Once you’ve maxed out your traditional retirement accounts, an HSA becomes an excellent next stop. HSA contribution limits are $4,300 for self-only coverage and $8,550 for family coverage in 2025. You can leave that money in cash or invest it. You can, of course, use it to pay for qualified out-of-pocket medical expenses at any time. But you can also leave it in the account untouched, letting it grow and enjoy the power of tax-advantaged compounding—just as you would with an IRA or 401(k).

Health care is one of the biggest expenses in retirement. So building a tax-free fund dedicated to future medical needs makes a lot of sense. According to recent estimates, a 65-year-old retiring in 2024 can expect to spend around $165,000 on health care in retirement—and that number is only expected to rise.

Here’s the kicker: When you turn 65, you aren’t limited to using your HSA for medical expenses. You can make withdrawals for non-medical expenses, and these will simply be taxed as income, just like withdrawals from a traditional IRA or 401(k). In short, your HSA can function like a traditional retirement account with the added perk of tax-free withdrawals for medical expenses at any age.

Your HSA as Part of Your Investment Strategy

Your HSA is a financial asset, whether it’s sitting in cash or invested in the market. As such, it can play an important role in your strategies for long-term asset allocation, diversification and rebalancing. Managed well, it can contribute meaningfully to your future financial security.

You can manage your HSA investments on your own. Or, depending on your HSA provider, we may be able to manage the assets within the account on your behalf. Even if direct management isn’t possible, we’re here to help you evaluate your options, choose appropriate investments and determine how best to incorporate your HSA into your long-term plan.

If you’re not sure whether an HDHP and HSA are right for you, let’s talk. Together, we can evaluate your health needs, cash flow and retirement goals to determine the best path forward.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/10/HSA-Benefits.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2025-10-10 10:30:532025-10-10 10:31:01Should I Be Using a Health Savings Account?

Retirement is a major life shift, one that impacts more than just your schedule. It can reshape your sense of identity, daily habits and even your health. In fact, research has shown that retirement can raise the risk of heart disease and other medical issues by up to 40%. The reason? Experts point to a loss of purpose and reduced social connection, both of which can take a toll on mental and physical well-being.

Without a plan for how to spend your time meaningfully, the transition can bring unexpected emotional challenges.

The Risks of Unstructured Retirement

Many retirees begin this new chapter with a “honeymoon phase”—a period marked by the novelty of free time, relaxation or long-awaited travel plans. But this initial high can eventually fade.

When the excitement of sleeping in and checking items off the bucket list wears off, retirees can find themselves facing unexpected emotional challenges. Common struggles include boredom, loss of routine, identity shifts and social isolation. In fact, 24% of older adults are considered to be socially isolated. Isolation can also have a ripple effect on health: It’s associated with a 50% increase in risk of developing dementia and increased risk of premature mortality.

Designing a Retirement with Purpose

To avoid some of the potential pitfalls of an unstructured retirement, it’s important to think carefully—and proactively—about purpose. What do you want this next phase of life to look and feel like? Beyond financial planning, consider how you’ll meet the deeper needs your pre-retirement life—including work and raising kids—may have fulfilled: structure, identity, accomplishment, social connection and a sense of meaning.

What brings you pleasure and meaning? What have you always wanted to try or learn? Pursuing these activities can provide purpose and help ensure retirement’s not just a long vacation, but a rewarding chapter of your life.

Feeling stuck here? Try asking close friends or family what they see light you up. Often, others can reflect back passions or strengths that are hard to see on your own.

Staying Connected and Active

Relationships and physical routines matter more than ever when you retire. Staying active, both physically and socially, offers measurable health benefits. Regular physical activity lowers risks, including the likelihood of dementia, heart disease, stroke and eight types of cancer.

People-centered activity is important, too. Look for ways to stay engaged, whether through volunteering, mentoring, part-time work, creative pursuits or community involvement. Older volunteers, aged 55 and up, who gave 100 hours or more each year were two-thirds less likely to report poor health than non-volunteers.

Spending more time with family is a high priority for many retirees and can be a great way to fulfill social needs. But make sure that vision is shared. Open conversations with loved ones about time together, expectations and boundaries can help align plans and avoid disappointment down the road.

The Retirement Identity Shift

In many ways, it’s hard to define what retirement is. After all, it’s not a single moment but a series of transitions. For instance, rather than an abrupt shift to not working at all, you may consider bridge employment—usually part-time work in a temporary position or as a consultant in your field or in a different industry. This can offer a gradual shift into retirement, providing continued income and engagement as you adjust.

As your vision for retirement evolves, keep us in the loop. We’d love to hear what you’re planning—and we’re here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-5.png11522048Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-09-26 07:38:002025-10-07 16:02:46The Power of Purpose in Retirement

As a business owner, you’ve spent your life’s work growing your business, taking care of employees, managing your product or service, and looking after your people. Now, you may be getting to a point where your spouse tells you you work too much. Or perhaps you’re watching the clock more than you used to, counting down the minutes until you can head home and unplug from your “boss” responsibilities.

Whatever your reasoning, if you’re starting to ask questions like, “Do I have enough to sell?” and “Will that be enough?” then it’s time to focus on you for a change.

Why Business Owners Need Specialized Financial Planning

Business owners face a unique set of financial challenges and opportunities. Whether you are a small business owner or running a large corporation, the following considerations are critical:

Maximizing tax efficiency

Choosing the most appropriate retirement account type

Evaluating your retirement account options

Managing 401(k) and pension investments

Considering a defined benefit plan, i.e., “pension”

Aligning company benefits offerings with company goals

Our team specializes in helping business owners handle these and other issues while they’re still working. During those years, we help you work through proper planning techniques to diversify your assets, reduce risk, optimize your taxes, and offer competitive benefits. All of these steps help streamline and strengthen your business at the time — but they also set you up for a successful transition into retirement or your next business opportunity.

When you do get to the point of exiting, we help you bring all of this planning together into one critical decision: whether or not you have what you need to move on from your business and into your ideal retirement, whatever that looks like for you.

Creating a Dream Retirement

At Warren Street, we’ve helped many business owner clients over the years answer the “Do I have enough to sell?” question and develop their exit strategies accordingly.

If you choose to work with us during your own exit process, we’ll play a key role on your professional team alongside your attorney. While your attorney looks after the legal structure of the deal, we’ll handle related asset management and tax mitigation. For example, if you’re involved in an all-cash sale with multiple payments coming in the next few years, we will discuss tax deferral opportunities to add into your transition plan. Or, if you’re struggling with a go/no-go decision, we’ll conduct scenario planning to help you make an informed choice based on your current financial situation, projected future state, and personal goals.

No matter where you are in the exit planning process, we can help evaluate your current assets, investments, estate planning, and legacy goals, so you can make a clear and confident decision on what next steps are right for you.

If this sounds like you and you’re a current Warren Street client, please mention your interest to your Lead Advisor! Or, if you’re not a client but are interested in learning how we can help, schedule a complimentary introductory call with us. We hope to hear from you and look forward to exploring how we can make your post-exit dreams a reality.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/12/Do-I-Have-Enough-To-Sell.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-12-28 08:24:002024-06-03 10:46:08Do I Have Enough to Sell My Business?

As a retired Chevron employee and financial advisor, I’m constantly keeping my finger on the pulse of what’s happening at the company. Last month, Chevron sent a letter to employees announcing that, as of June 1, the funds in their retirement plans will be changing.

Given these updates, I wanted to take the time to make sure my Chevron connections understand what’s happening — and what it could mean for your portfolio.

What’s changing?

The gist is this: on June 1, 2023, your Fidelity NetBenefits account will reflect new investment choices. In many cases, your money will be automatically allocated to new funds. For example, If you’re currently in a Vanguard Target Retirement Date Fund, this will map to a BlackRock LifePath® Index Fund. All in all, the 16 existing investment choices will be funneled down into just 11 choices. This applies to both the Employee Savings Investment Plan (ESIP) and Deferred Compensation Plan (DCP).

In my opinion, the most impactful change is the consolidation of three equity funds — Vanguard 500 Index, Vanguard Large Cap Value Index, and Vanguard PRIMECAP — into just one equity fund, the “Equity Index.” This is tricky, because for many people, it made sense to hold a pure S&P 500 fund such as the Vanguard 500 Index. Pure S&P 500 funds allow you to “own” the largest 500 companies in the US, compared to the “Equity Index,” which is more of a mix.

We are currently investigating this and the other new funds to understand exactly what they entail and how they will interact with the rest of your portfolio.

What should you do?

This fund consolidation is neither good nor bad; however, it does mean that you should talk to an advisor about the impact it will have on your portfolio. The new funds have different risk and return profiles, expense ratios, and diversification characteristics than the old funds, and they’re not necessarily a direct map. It’s critical that you confirm your new funds still support your future retirement goals.

No matter your age or retirement goals, it’s always a good practice to review your 401(k) plan on a regular basis and make sure it still aligns with your needs. The updates to the Chevron 401(k) plans are a good reminder to take a close look at yours and make any necessary changes.

If you don’t already have an advisor or are looking for a new one, I’m also happy to speak with you (no charge) about your portfolio. I’ve been helping Chevron colleagues and clients for more than 40 years and am an expert on the company’s employee benefits package. I’m available to answer any questions you have about the upcoming changes.

Feel free to give me a call at 714-876-6200 or book time with me if you’d like to chat. I hope to hear from you and am here to help!

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/05/Chevron-401k-Changes-Thumbnail.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2023-05-19 07:30:002023-05-18 10:07:43Chevron 401(k) Changes: Unpacking Your New Funds

In planning for retirement, one topic is often top of mind: whether or not Social Security will still be around when we retire.

As we covered in a related post, When Should You Take Your Social Security, most of us have been paying into the program our entire working life. We’re counting on receiving some of that money back in retirement.

But then there are those headlines, warning us that the Social Security trust fund is set to run dry around 2034.

Does this mean you should grab what you can, as soon as you’re able? Let’s explain why we agree with Social Security specialist Mary Beth Franklin, who suggests the following:

“While there may be good reasons to file for reduced Social Security benefits early, claiming Social Security prematurely out of fear is a bit like selling stocks in a down market: All you’ve guaranteed is that you’ve locked in a loss. And if future benefit cuts did materialize, the benefits of those who claimed as soon as possible would be reduced even further.”

While we don’t expect Social Security to go bust, we do expect it will need to change in the years ahead. As its trustees have reported:

“Social Security is not sustainable over the long term at current benefit and tax rates … [and] trust fund reserves will be depleted by 2034.”

But let’s unpack this statement. First, “depleted” does not mean the Social Security Administration is going to turn out the lights and go home. It means it could run out of trust fund reserves by then, which are used to top off the total amount spent on Social Security benefits. There are still payroll taxes and other sources to cover more than 77% of the program’s payouts. So, worst case, if we did nothing but wait for the reserves to run out, we’d be forced to make hard choices about an approximate 23% shortfall starting around 2034.

Admittedly, Social Security is between a rock and a hard place. Nobody wants to lose benefits they’ve been counting on or spend significantly more to maintain the status quo. But if we don’t do something to shore up the program’s reserves, our options will likely only worsen.

In this context, the political will to reform Social Security seems strong, and bipartisan. As Buckingham Strategic Partners retirement planning specialist Jeffrey Levine has observed:

“My gut sense is that practically no politician in America would ultimately be happy having to explain to voters why they let Social Security collapse on their watch … That’s not a great message to have to bring to voters, especially older voters who show up at the polls in the greatest numbers.”

As members of Congress wrangle over the “best” (or least abhorrent) solutions for their constituents, they have been submitting proposals behind the scenes, and the Social Security Administration has been weighing in on the estimated effect for each.

Time will tell which proposals become legislated action, but the range of possibilities essentially falls into two broad categories: We can pay more in, or we can take less out.Most likely, we’ll need to do a bit of both.

Possible Ways to Pay More In

To name a few ways to replenish Social Security’s reserves, Congress could:

Raise the cap on wages subject to Social Security tax: As of 2023, earnings beyond $160,200 per year are not subject to Social Security tax. There’s been talk of increasing this cap, eliminating it entirely, or reinstating it for income beyond certain high-water marks.

Increase the Social Security tax rate for some or all workers: Currently, employers and employees each pay in 6.2% of their wages, for a total 12.4% up to the aforementioned wage cap. (This does not include an additional Medicare tax, which is not subject to the wage cap.) As cited in a September 2022 University of Maryland School of Public Policy report, “73% (Republicans 70%, Democrats 78%) favored increasing the payroll tax from 6.2 to 6.5%.”

Increase the tax on Social Security payouts, and direct those funds back into the program: Currently, if your “combined income” exceeds $44,000 on a joint return ($34,000 on an individual return), up to 85% of your Social Security benefit is taxable, as described here. Anything is possible, but taxing retirees more heavily seems less politically palatable than some of the other options.

Identify new funding sources: For example, one recent bipartisan proposal would establish a dedicated “sovereign-wealth fund,” seeded with government loans. Presumably, it would be structured like an endowment fund, with an investment time horizon of forever. In theory, its returns could augment more conservatively invested Social Security trust fund reserves. Other proposals have explored a range of potential new taxes aimed at filling the gap.

Options for Taking Less Out

We could also cut back on Social Security spending. Some of the possibilities here include:

Reducing benefits: Payouts could be cut across the board, or current bipartisan conversations seem focused on curtailing wealthier retirees’ benefits.

Extending the full retirement age: There are proposals to extend the full retirement age for everyone, or at least for younger workers. This would effectively reduce lifetime payouts received, no matter when you start drawing benefits.

Tinkering with COLAs: There are also bipartisan conversations about replacing the benchmark used to calculate the Cost-of-Living Adjustment (COLA), which might lower these annual adjustments in some years.

These are just a few of the possibilities. Some would impact everyone. Others are aimed at higher earners and/or more affluent Americans. It’s anybody’s guess which proposals make it through the political gamut, or what form they will take if they do.

Should You Take Your Social Security Early?

So, given the uncertainties of the day, should you start drawing benefits sooner than you otherwise would? An objective risk/reward analysis helps guide the way.

Many investors feel “safer” taking their Social Security as soon as possible, to avoid losing what seems like a bird in the hand. However, the appeal of this approach is often fueled by deep-seated loss aversion. Academic insights suggest we dislike the thought of losing money about twice as much as we enjoy the prospect of receiving more of it. Thus, we tend to cringe more over a potential loss of promised benefits than we factor in the substantial rewards we stand to gain by waiting. Put another way:

You’re not reducing your financial risks by taking Social Security early. You’re only changing which risks you’re taking. In exchange for an earlier and more assured payout, you’re also accepting a permanent, cumulative cut to your ongoing benefits.

If this still seems like a fair trade-off, consider that Social Security is one of the few sources of retirement income ideally structured to offset three of retirement’s greatest risks:

Life expectancy risk: In an annuity-like fashion, Social Security is structured to continue paying out, no matter how long you and your spouse live.

Inflation risk: The payouts are adjusted annually to keep pace with inflation.

Market risk: Even in bear markets, Social Security keeps paying, with no drop in benefits.

In short, if you are willing and able to wait a few extra years to receive a permanently higher payout, you can expect to better manage all three of these very real retirement risks over time.

This is not to say everyone should wait until their Full Retirement Age or longer to start taking Social Security. When is the best time for you and your spouse to start drawing benefits? Rather than hinging the decision on uncontrollable unknowns, we recommend using your personal circumstances as your greatest guide. Consider the retirement risks that most directly apply to you and yours, and chart your course accordingly.

But you don’t have to go it alone. Please be in touch if we can assist you with your Social Security planning, or with any other questions you may have as you prepare for your ideal retirement.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/04/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2023-05-11 08:28:422024-11-07 09:23:22Why We Believe Social Security Will Endure

Ever since President Franklin D. Roosevelt signed the 1935 Social Security Act, most Americans have pondered this critical question as they approach retirement:

“When should I (or we) start taking my (or our) Social Security?”

And yet, the “right” answer to this common query remains as elusive as ever. It depends on a wide array of personal variables, including how the unknowable future plays out.

No wonder many families find themselves in a quandary when it comes to taking their Social Security benefits. Let’s take a closer look at how to find the right balance for you.

Social Security Planning: A Balancing Act

For Social Security planning purposes, you reach full retirement age (FRA) between ages 66–67, depending on the year you were born. However, you can generally begin drawing Social Security benefits as early as age 62 (with the lowest available monthly starting payments) or as late as age 70 (for the highest available monthly starting payments).

Retirees are often advised to wait at least until their full retirement age, if not until age 70 to begin taking Social Security. In raw dollars, waiting to take your Social Security often works out to be the best deal for many families. Plus, these days, many of us choose to work well into our 60s, 70s, and beyond. Some analyses have even factored in the cost of spending down other assets while you wait, rather than using them for continued investment growth. The conclusion is the same.

However, you’re not “many families.” You’re your family. Your personal and practical circumstances may mean this general rule of thumb won’t point to your best choice. Following are some of the most common factors that may influence whether to start taking Social Security sooner or later.

Alternative Income Sources: First, and perhaps most obviously, if you have few or no alternative income sources once your paychecks stop, you may not have the luxury of waiting. You may need to start taking Social Security as soon as possible.

Life Expectancy: If you’re considering the benefits of waiting until age 70 to take Social Security, remember that this strategy assumes you live to at least the average age someone your age and gender is likely to reach. Even if you can afford to wait, you’ll want to factor in whether your health, lifestyle, and family history justify doing so.

Estate Planning: Have you placed a high or low priority on leaving as much as possible to your heirs and/or favorite charities after you pass? Your preferences here may influence how, and from where you’ll spend down your inheritable estate, which in turn may influence the timing of your Social Security enrollment.

Employment: How likely is it you’ll keep working until your FRA? Once you reach it, you can collect full Social Security benefits, even if you’re still working. But until then, your earnings may reduce your Social Security benefits.

Marital Status: If you’re married, one of you has probably paid in more to Social Security. One is likely to live longer. You may retire at different times, and your ages probably differ. All these factors can complicate the equation. You’ll want to consider the timing, rules, and outcomes under various scenarios—such as when and whether to take Social Security as an earner, the spouse of an earner, the widow or widower of an earner, or an ex-spouse of an earner—while also factoring in whether you and/or your spouse are still working prior to your FRAs, as described above. Ideal start dates for one scenario may not be ideal for another.

Other Circumstances: Beyond your marital status, there are other factors that may influence your timing decisions if they apply to you—such as if you’re a business owner, you live abroad, you qualify for Social Security Disability, or your children qualify for Social Security benefits under your account.

Income Taxes: We find many pre-retirees don’t realize that up to 85% of their Social Security income may be taxable. Your annual Social Security income also figures into your modified adjusted gross income (MAGI), which can push you past thresholds for incurring Medicare surcharges (beginning at age 65, based on your MAGI from two years prior). Bottom line, broad tax planning may influence your timing as well.

Degrees of Control

Clearly, there’s a lot to think about when deciding when to start taking Social Security. Whether you’re going it alone or with a financial planner, here’s one piece of advice that should help:

Control what you can. Let go of what you can’t.

What do we mean by that? There are many known factors you can include in your Social Security planning. You know your marital status. You can access your Social Security account and/or use a calculator to estimate your benefits. You can make educated guesses about your life expectancy, how long you’ll work, and so on. Also, if you’ve delayed taking Social Security past your FRA, you may be able to change your mind … to a point. You can file to collect up to six months of retroactive benefits if you end up needing the income sooner than planned.

You can use all of this planning information and more to make reasonable assumptions and timely decisions about when to take your Social Security.

After that, we recommend going easy on yourself if (or more realistically, when) some of your plans don’t go as planned. Come what may, you’ve done your best. Instead of channeling energy into regretting good decisions, use it to make judicious adjustments whenever new assumptions arise. By consistently focusing on what we know rather than what we hope or fear, we remain best positioned to shift course as warranted in the face of adversity.

Whether you’re planning to file for Social Security or you’re already drawing it, we appreciate the opportunity to help you and your family make good choices about when, and how to manage your available options. We hope you’ll contact us today to learn more.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/01/When-Should-You-Take-Your-Social-Security.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-03-30 08:02:002024-11-07 09:23:46When Should You Take Your Social Security?

As a former Chevron employee and current financial advisor, I know firsthand that planning for retirement can be daunting. You might be asking yourself questions like:

How do I anticipate all the different factors that go into retirement?

How much money is enough?

What if I have an unexpected expense in retirement?

If you’re feeling like 2023 is your year but are afraid to take the plunge, read on. These are the top three considerations I discuss with my Chevron friends and clients when they ask me those questions.

1. Wait until at least age 55.

Every case is different, but in general, it’s best to wait until at least age 55 to retire. Every year you wait increases the likelihood you won’t run out of money.

Talk to your advisor about scenario planning (more on that in the next point) to figure out what age makes sense for your specific situation. And remember, there are always exceptions to this advice if it’s a matter of your health or other serious issues.

2. Determine your post-retirement budget.

When you picture your life in retirement, what does it look like? Are you jet-setting the world with your spouse, or enjoying a quiet life at home with your grandkids? Working a part-time job to stay busy, or finally pursuing your hobbies and passions full-time? Upgrading to the big truck you always had your eye on, or getting every last mile out of your current ride?

These are important considerations, as they’ll impact the amount of money you’ll need in retirement. If you think you’ll have similar cash flow needs in retirement as now, that’s important to know. Or, if you anticipate boosting your spending on vacations, supporting other family members, etc., that also needs to be taken into account. Once you have determined your budget needs pre- and post-retirement, your advisor can help you put together a strategy around your paychecks, how much to save in the plan, and what number you need to hit to retire.

3. Do scenario planning.

We offer free scenario planning, called a Monte Carlo analysis, to help clients measure whether they could retire successfully. This simulation runs thousands of different scenarios based on your personal financial data. Then, it analyzes your “probability of success” in reaching the amount of money you’ll need at your desired retirement age. Best of all, this is a key tool for answering the question, “How much money do I need to retire?”

Whether it’s with Warren Street or another financial advisor, ask your advisor to help you put together a plan that accounts for these different situations, so you can set yourself up for success. As long as you have the relevant information ready to share with us — such as your current assets, expected savings, and time horizon — the analysis process takes no longer than 30 minutes. That’s a short amount of time to invest in your peace of mind!

Many Chevron employees are looking to retire this year, especially given that Chevron stock prices have generally held up. Whether you’re in the “this is my year” camp or still have another five years in you, I’d love to talk with you. Let’s put the numbers together and see what’s possible. I’m here to answer your questions and help you run the numbers, but the final decision is always yours.

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/02/How-to-Retire-in-2023-Chevron-Webinar.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2023-02-24 08:30:002024-11-07 09:24:13Chevron Employees: How to Retire in 2023