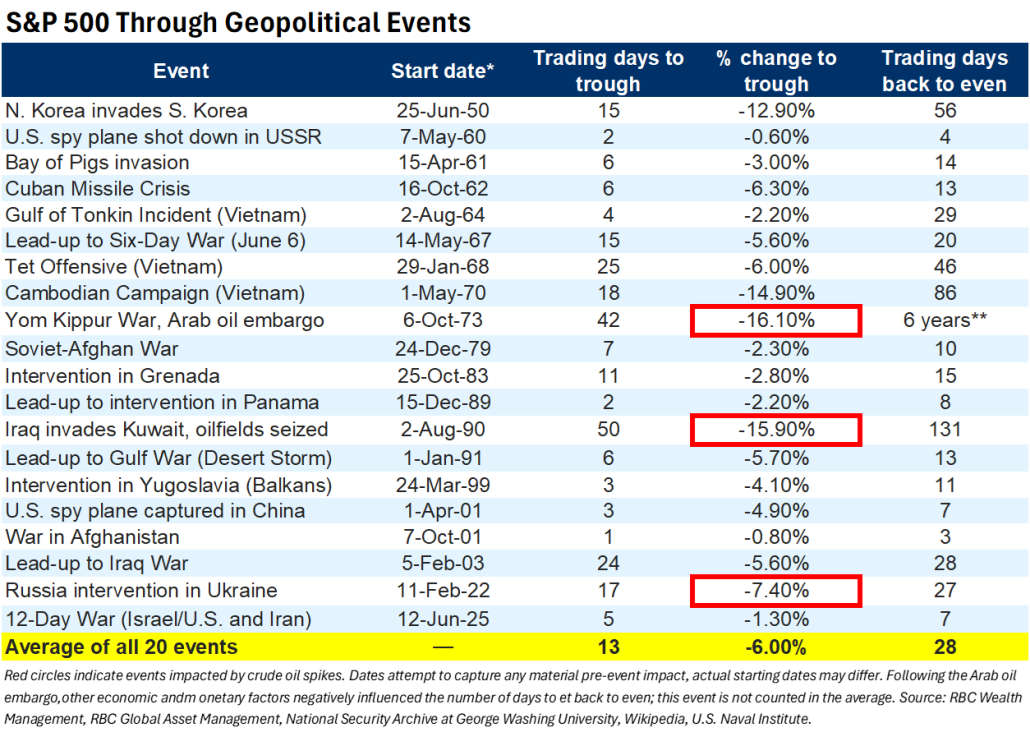

On the War in Iran: Do Markets Not Care, and What’s Next?

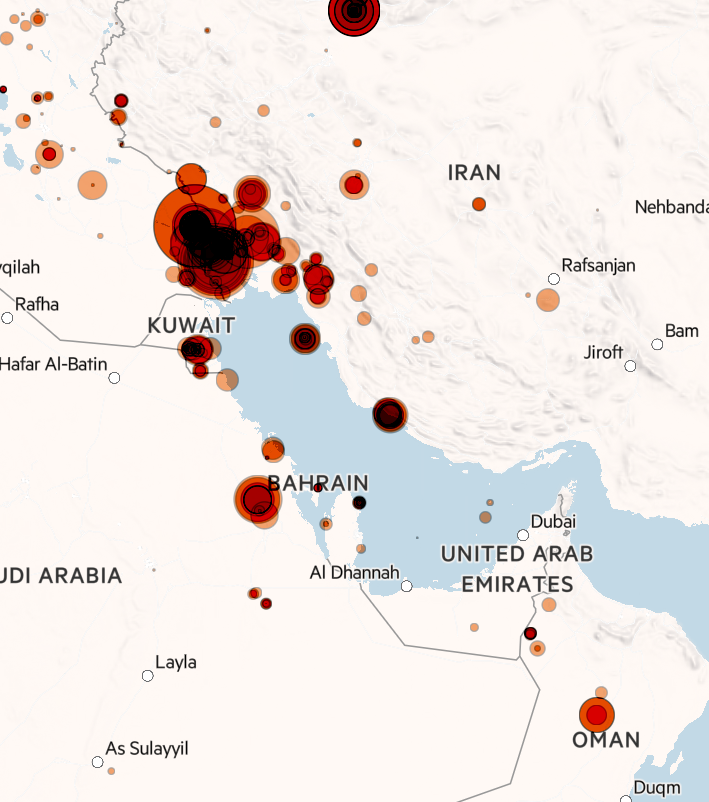

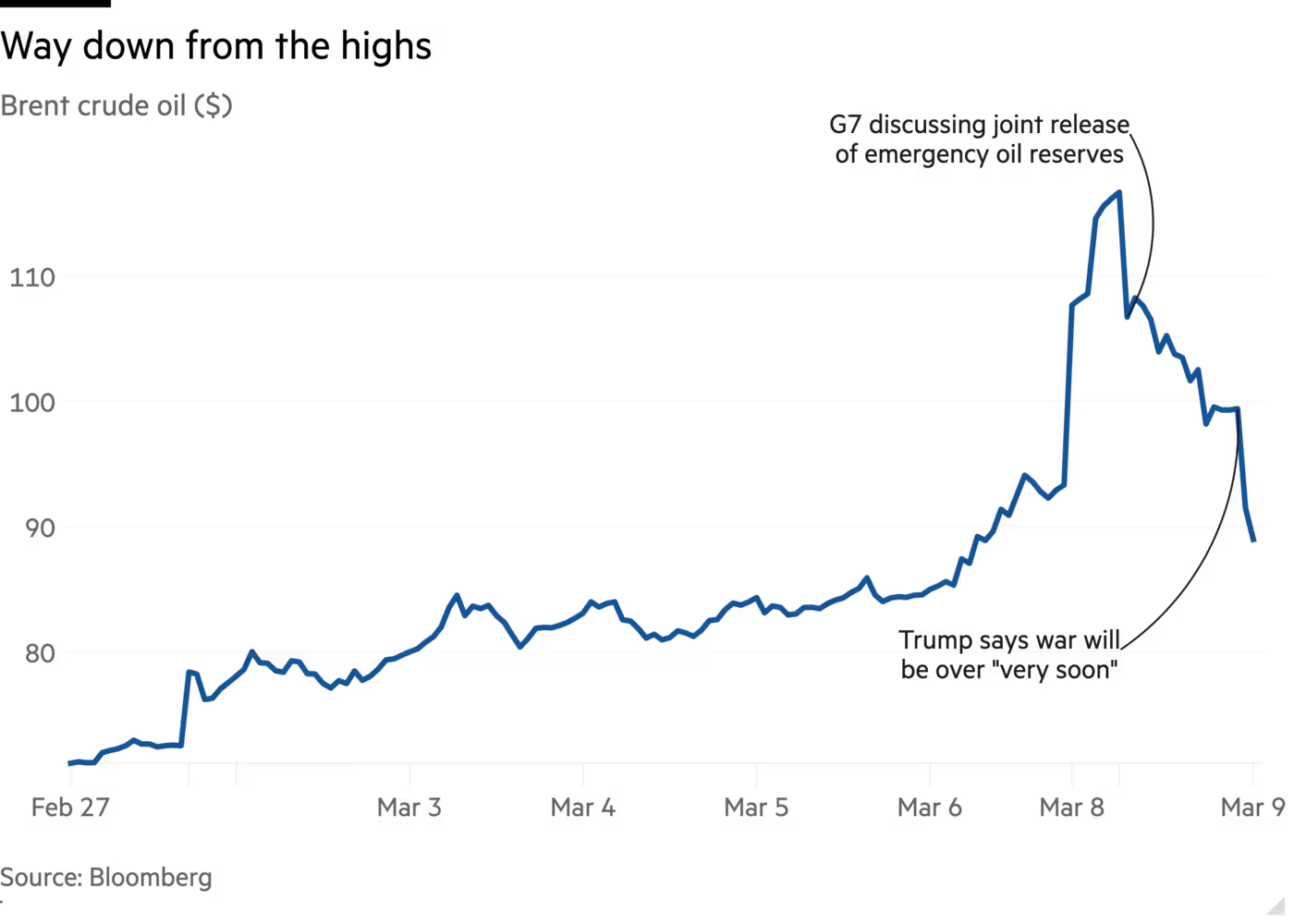

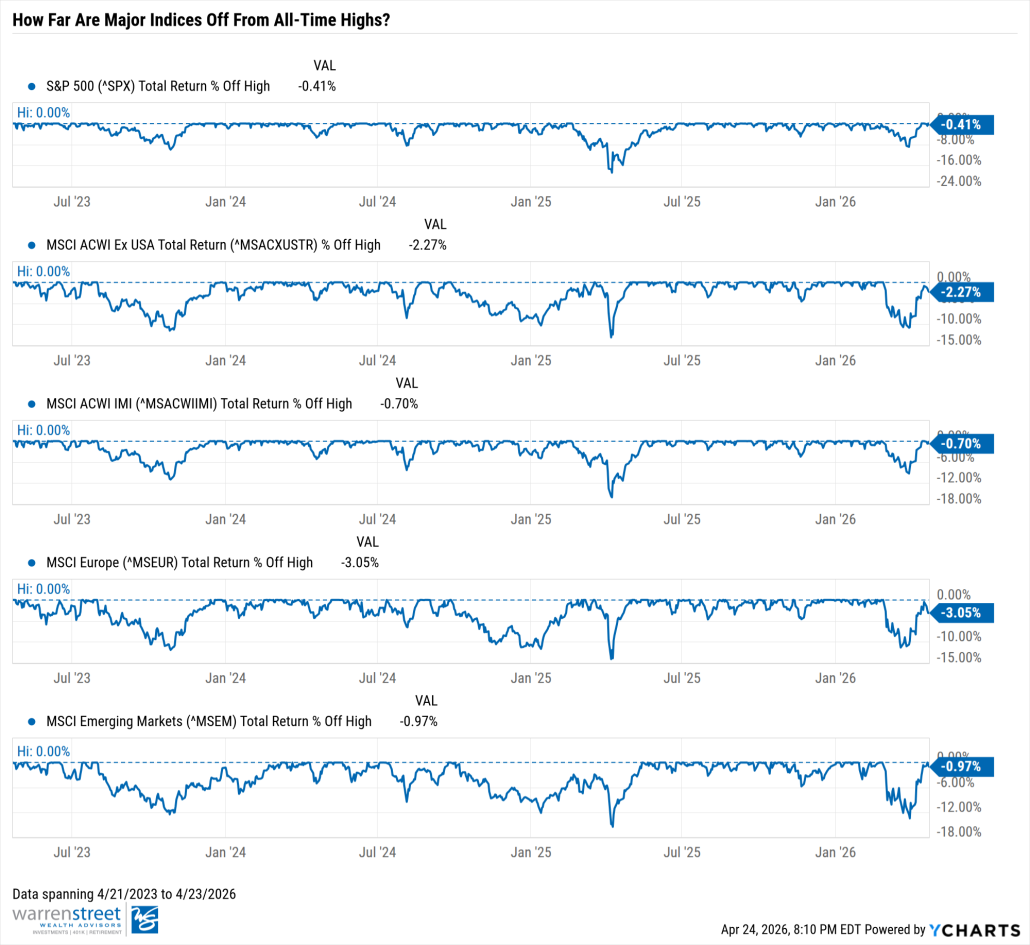

Last month, we emphasized the unpredictability of geopolitical risk and acknowledged its limited ability to depress longer-term returns. Today, we observe roughly 80 oil tankers stranded at sea, a supply shortfall of 9 million barrels per day, and a ceasefire so fragile that ships are still being bombarded. Yet, markets are hovering near all-time highs.

It seems as if markets have already asked, “Will this war matter in a year?” and answered “Probably not.” Are they correct to think that the worst is behind us, or are we seeing an irrational optimism? More importantly, how are we thinking and what are we doing about it?

Both Sides Are Boxed In

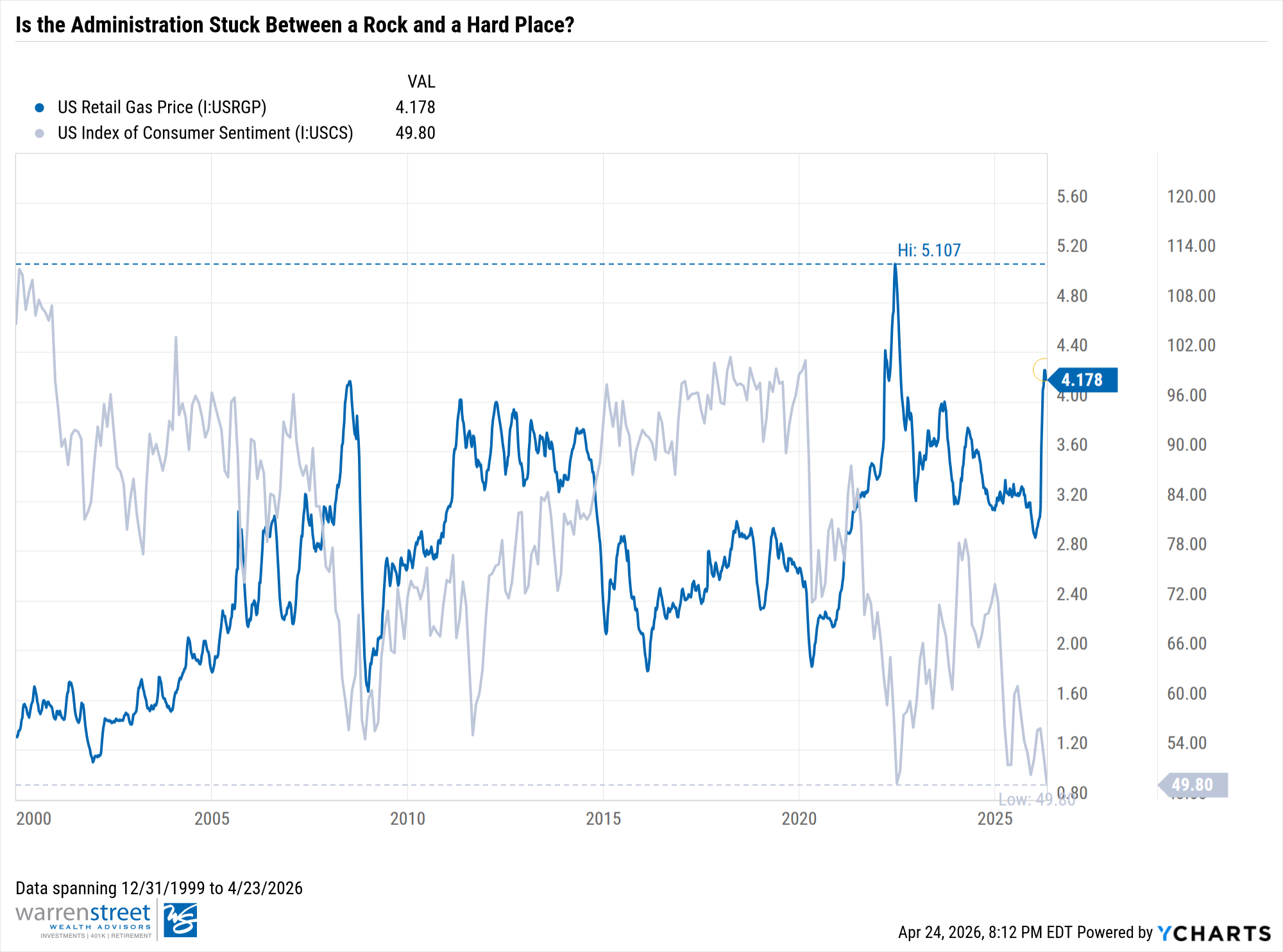

At first glance, it would seem that markets are celebrating the ceasefire. Instead, we believe they’re celebrating the constraints on both sides. Despite the current administration’s bravado on social media, the US is operating within real limits:

- Gas prices are climbing into politically damaging territory.

- We’ve burned through years of munitions stockpiles and missile interceptors — replenishing them adds to an already strained debt picture.

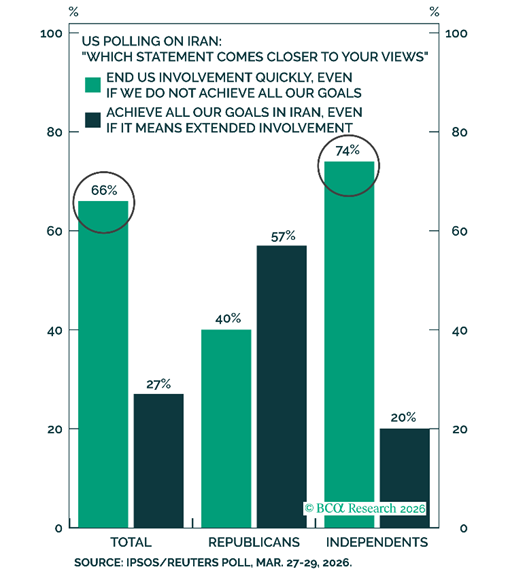

- At the start of the war, only 53% of the public supported it, and support has only eroded from there. With the midterms approaching, this war is becoming a liability.

Iran’s position is also complicated:

- Its arsenal is materially depleted, forcing more selective targeting.

- Headline inflation is near 50%, causing social unrest that has spilled into the streets and warranted radical response.

Yes, the regime is exhibiting an unexpected tolerance for pain despite being under genuine strain. It has come to realize how powerful its leverage over the Strait of Hormuz is, but that leverage has a ceiling. If Iran pushes hard enough to tip the world into recession, the world could coalesce to force the Strait open.

At that point, nobody is negotiating with Tehran and will not care about its capitulation. Iran’s smarter play is subtler — agitate just enough to keep oil prices elevated, respect the ceasefire to the bare minimum, and let the pressure build on Trump’s midterm prospects.

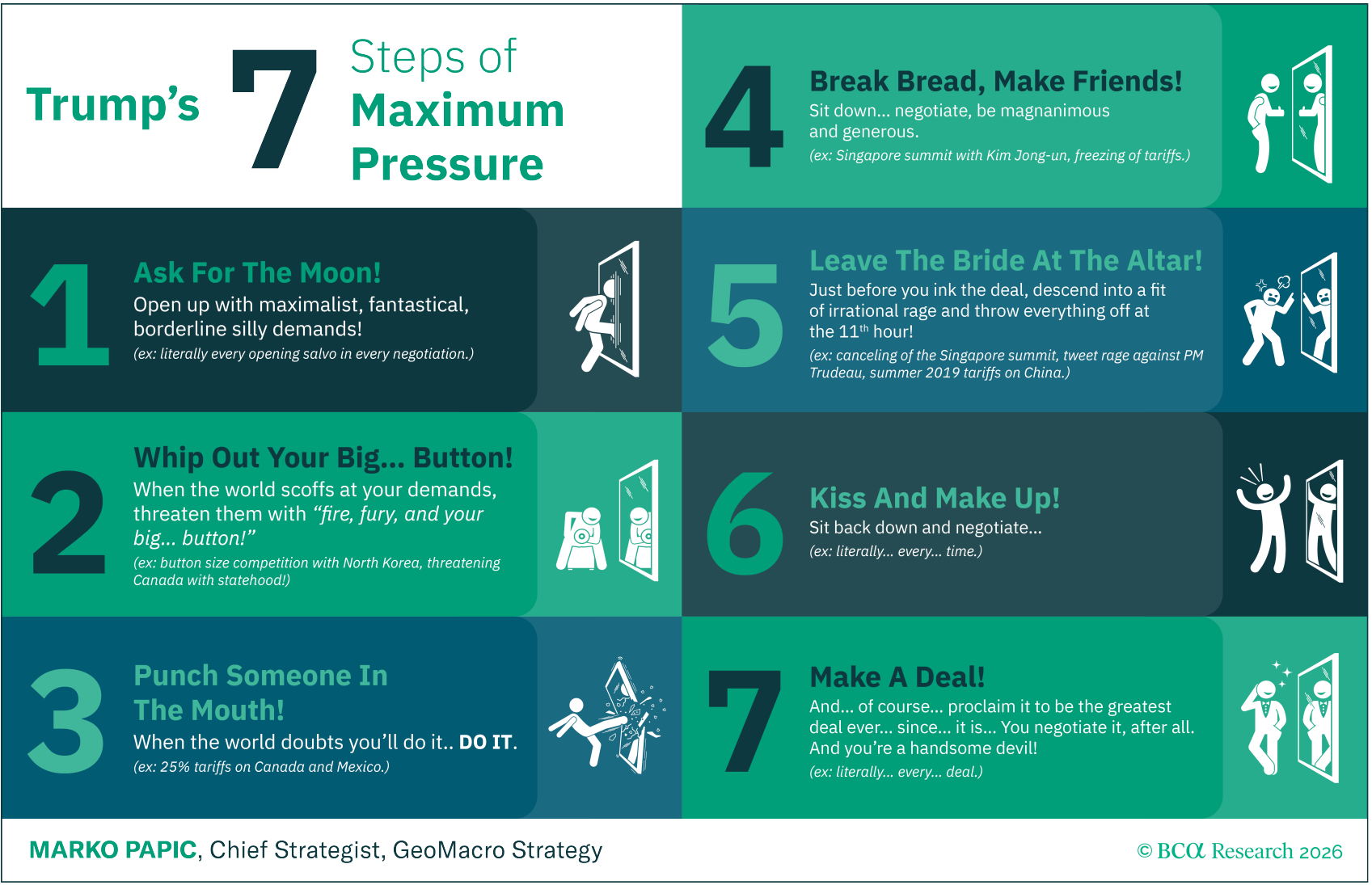

Where Are We in the Playbook?

Some people might describe President Trump’s tactic using the TACO — Trump Always Chickens Out — acronym. Instead, BCA Research’s Marko Papic put together a seven-step framework for Trump’s maximum pressure negotiating style that we find more instructive.

Steps 1 through 3 — maximalist demands, threats, and following through — are in the rearview. We appear to be entering Step 4: fragile ceasefire, back-channel signals, and political jockeying from both sides to frame their position as a win. If the framework holds, we could be in for one more dramatic detour before a deal gets done.

A breakdown in negotiations or a miscalculation on either side could push oil prices meaningfully higher with downstream impacts on earnings and global growth. This is more of a tail-risk scenario, but Trump has left the altar before. The question is – will Iran still be there when he returns?

We imagine the likely base case resembles a uranium moratorium — perhaps similar to the Obama-era Joint Comprehensive Plan of Action, but sold very differently. Trump’s version will lean on the military degradation of Iranian capabilities. For Iran, the goal was always a shift in US policy posture. Both sides will aim to find a version of that story to tell their constituents.

Where We Stand

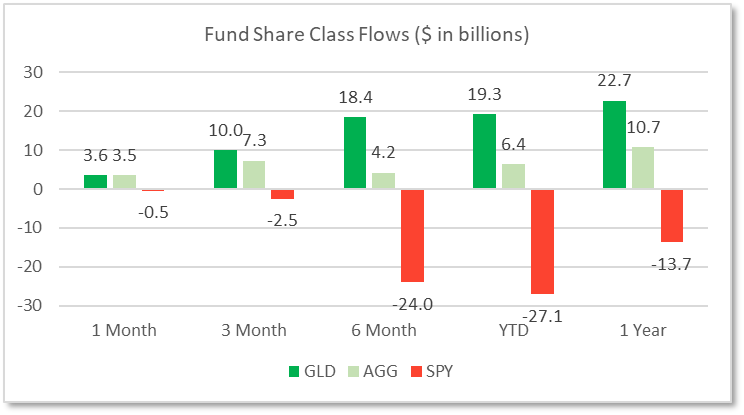

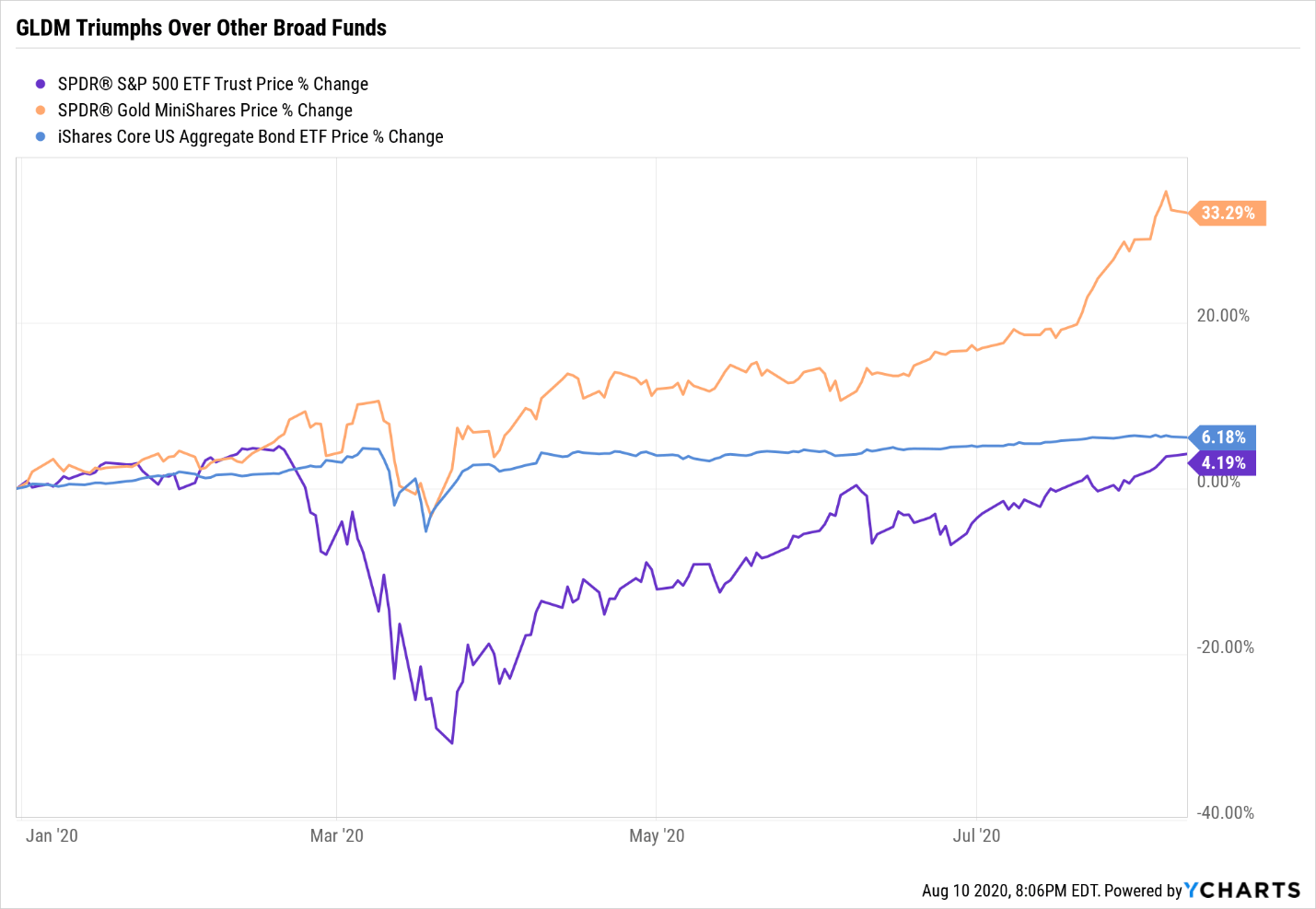

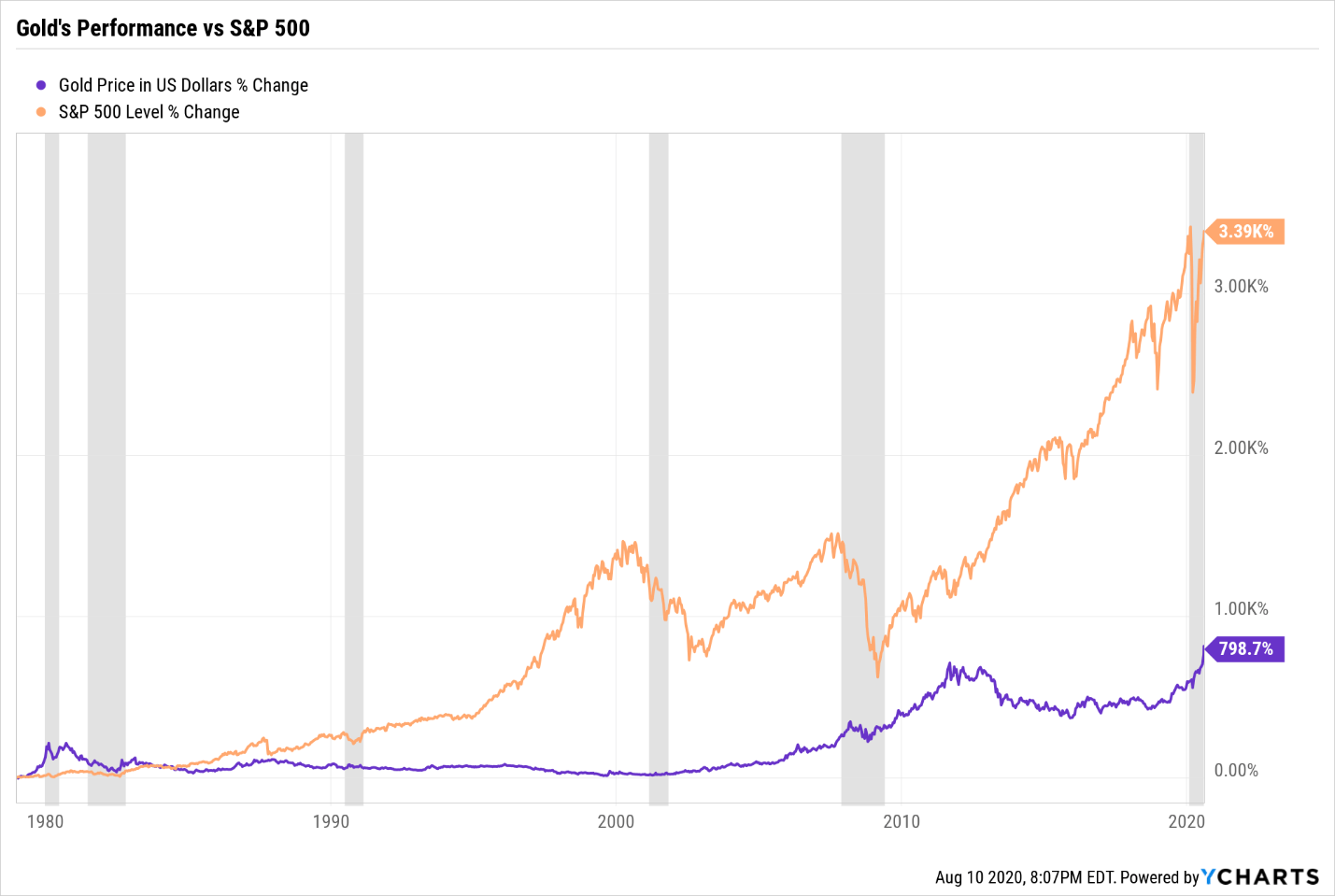

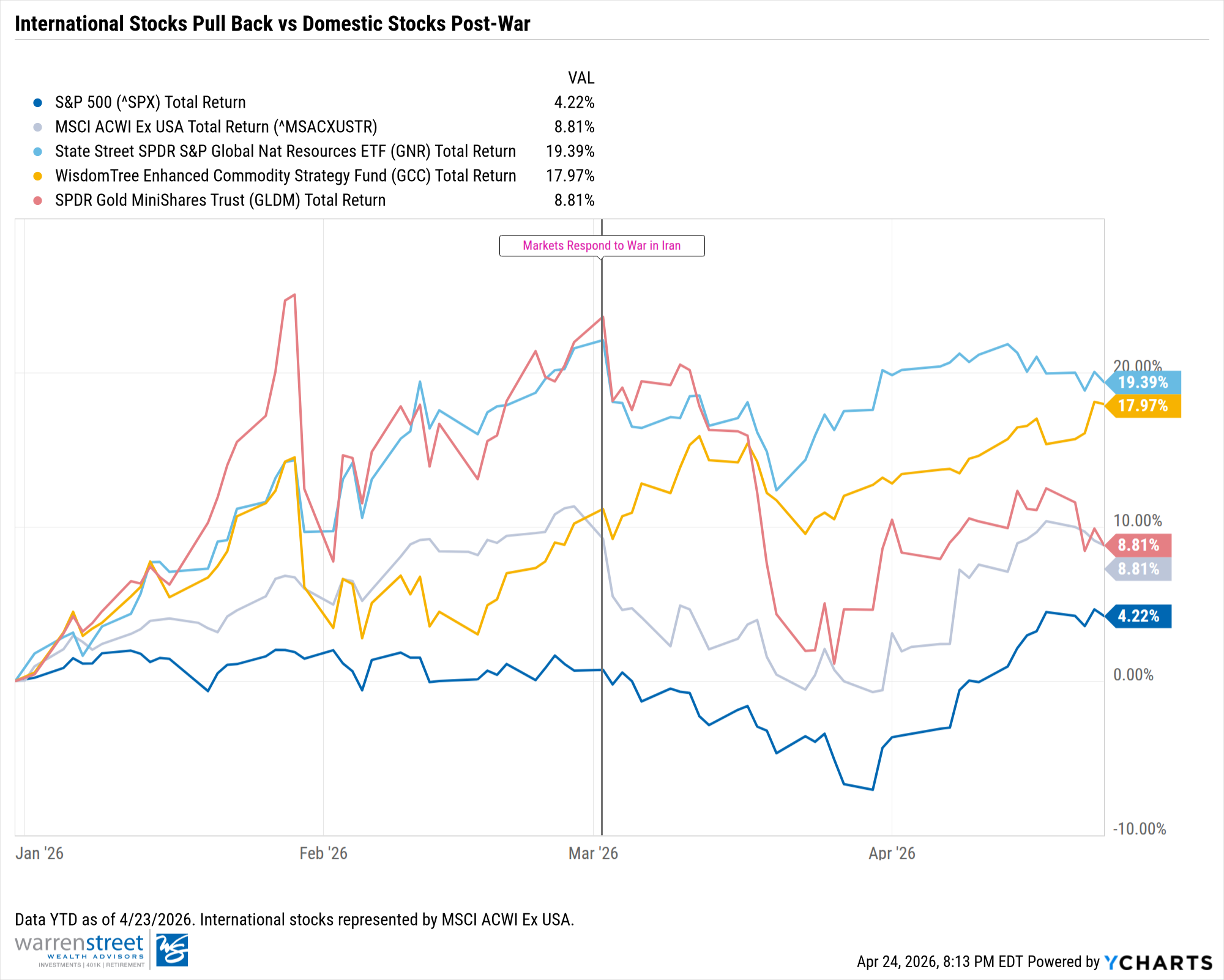

Before the conflict, our strategies had real momentum. Our tilt towards international equities was outperforming the US, and the Diversifiers strategy (i.e., gold, natural resources, commodities) boosted returns. Some of that outperformance has pulled back as international markets are more vulnerable to gulf energy. However, we believe that the bigger picture is unchanged.

Prior to the war, deglobalization was already underway, only to be accelerated by this conflict. Nations that spent decades outsourcing their energy and security needs are now building for self-sufficiency with more urgency. New trade arrangements, energy partnerships, and military alliances are forming in rooms the US is not in. The map is being redrawn, and we want exposure to that.

And What We Did

Our take? Rather than dramatic strategy shifts, we acknowledge the market’s ability to look past geopolitical noise and instead rebalanced firmwide back to target. This trimmed what held up — gold, commodities — and rotated into areas that sold off, including US equities. Should markets sell off further in a tail-risk event, we are actively watching for opportunities to tactically pivot strength into weakness.

To clients, the right posture might seem boring — and boring is probably correct. Sometimes, boring means hedging against the risks you can see, and diversifying against the ones you cannot.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Sources:

- BCA Research