There are a lot of things in life where the right move is pretty intuitive. Avoid the top rung of a ladder when you’re changing a lightbulb. Don’t click on that suspicious link in your email inbox.

But when it comes to your money, making smart decisions isn’t always so easy. In fact, there are a lot of times in investing where the intuitive move isn’t the best. A stand-out example is risk: For the most part, our brains and bodies tell us to avoid it. While it may seem smart to dial down risk in your investment portfolio, taking a too-conservative approach might leave you far short of your long-term goals. Making sound financial decisions often involves embracing counterintuitive strategies. Let’s explore a few more.

Less Action Often Leads to Better Results

Scenario: All too frequently, news headlines scream about stocks soaring or plummeting. When alarm bells like these ring, your impulse may be to take action. Zoom out and you’ll realize that a doom-and-gloom news cycle is practically a given. Buying and selling investments based on it is not a good idea.

Counterintuitive advice: The urge to act on market movements can be hard to resist. However, investing is a long-term endeavor, and often the best move is to do nothing at all.

Consider the story of the Voya Corporate Leaders Trust highlighted by Jason Zweig of The Wall Street Journala few years back. Established in 1935, this fund was designed to counteract the speculative excesses that contributed to the 1929 market crash. Its approach was radical: The fund purchased equal shares of 30 stocks and committed to holding them indefinitely. No new stocks could be added, and existing ones could only be sold under extraordinary circumstances, such as bankruptcy or mergers.

Despite being on “permanent autopilot” for nearly a century, the Voya fund has outperformed many actively managed funds—and even the S&P 500 at times. Patience and a hands-off approach can pay off over time.

Your Portfolio Shouldn’t Match the S&P 500

Scenario: When the S&P 500 has had a bang-up year, as it did in 2024—and 2023—you may be tempted to wonder why your portfolio didn’t keep up. In fact, it might lead to what’s known as “tracking error regret,” which occurs when investors second-guess their diversified approach because their returns don’t match a popular benchmark.

Counterintuitive advice: Your portfolio is not built to match the S&P 500, which represents just one slice of the market—the 500 largest U.S. companies.

Instead, it’s designed for reasons that are unique to you, whether it’s funding retirement, paying for kids’ college education or leaving your wealth for the next generation. A well-diversified portfolio is a powerful tool to help you meet those goals. Consider the classic 60/40 portfolio, which allocates 60% to equities and 40% to bonds. While it’s not likely to outperform an all-equity portfolio over the long run, it is structured to provide a buffer during periods of market turmoil.

Remember, it’s not the S&P 500’s performance that matters. What really matters is sticking with the right plan that will help you meet your financial goals.

Embrace the Bear

Scenario: When bear markets happen, it certainly doesn’t feel good. In fact, it may feel like you’re watching your wealth evaporate before your eyes. The impulse might be to cut your losses and sell. But bear markets have a tendency to change course. (In fact, they historically always have.)

Counterintuitive advice: Market downturns provide an opportunity to rebalance your portfolio. Bear markets can be prime buying opportunities. When prices are low, you are essentially given the chance to buy shares of a company or a fund when they’re on sale. You may consider trimming positions in asset classes that have grown and buying more shares in those whose valuations have dropped.

Rebalancing in this way helps you stick closer to the asset allocation strategy that’s at the center of your financial plan.

Putting It All Together

Whether it’s sticking to a diversified portfolio, viewing market downturns as opportunities or making smart spending decisions, counterintuitive strategies can help you stay on track toward your financial goals.

As you reflect on your investments this year, remember that your portfolio is unique to you. It’s designed to meet your specific needs and long-term objectives. And sometimes, the best move is simply to trust your plan and let time do the heavy lifting. We’re here to field any questions you may have along the way.

Phillip Law, CFA

Senior Portfolio Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/07/Counterintuitive-Money-Advice.png10801080Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2025-07-24 09:03:022025-07-24 09:03:07Counterintuitive Money Advice: Investing Against the Grain

The “One Big Beautiful Bill Act” (OBBBA), signed July 4, 2025, is poised to significantly impact nearly every aspect of your financial life. From your tax bill to your healthcare and your children’s future savings, understanding the nuances of this bill is crucial for effective financial planning.

Here’s a breakdown of what the OBBB means for you:

Tax Planning: More in Your Pocket, But Mind the Details

The OBBB makes permanent many of the individual income tax rates and brackets from the 2017 Tax Cuts and Jobs Act (TCJA), providing long-term clarity. But there’s more:

Expanded Standard Deduction: The standard deduction sees a permanent expansion, making tax filing simpler for many and potentially reducing the need to itemize.

Temporary Deductions (2025-2028): Get ready for some new, but temporary, tax breaks.

No Tax on Tips/Overtime: If you earn qualified tip income (up to $25,000) or overtime premium pay (up to $12,500 for individuals, $25,000 for joint filers), you may be able to deduct it. Keep an eye on income phase-outs.

Senior Tax Deduction: Individuals 65 and older meeting income thresholds ($75,000 single, $150,000 joint) can claim an additional $6,000 deduction, aiming to offset federal taxes on Social Security.

Auto Loan Interest Deduction: A temporary deduction of up to $10,000 for interest on loans for U.S.-assembled vehicles is available, subject to income phase-outs.

Increased SALT Deduction Cap: For five years, the State and Local Tax (SALT) deduction cap temporarily increases to $40,000 (from $10,000), with income-based phase-outs. This is a win for residents of high-tax states.

Enhanced Child Tax Credit: The Child Tax Credit permanently increases to $2,200 per child and will be indexed for inflation.

Business Tax Incentives: Businesses will see the reinstatement of 100% bonus depreciation and permanent Section 199A (Qualified Business Income) deduction, encouraging investment.

Estate and Gift Tax Relief: The unified credit and Generation-Skipping Transfer Tax (GSTT) exemption thresholds are permanently increased to $15 million per individual, offering substantial relief for high-net-worth individuals.

Your Action Plan: Review your current tax strategies with a financial advisor to maximize these new permanent and temporary provisions. Consider whether itemizing still makes sense for you.

Healthcare & Social Programs: A Shifting Landscape

The OBBB includes significant cuts to federal funding for vital social programs:

Medicaid Changes: Expect cuts to Medicaid funding and new work requirements for many adult beneficiaries. If you or your loved ones rely on Medicaid, be aware of potential reduced coverage or new eligibility hurdles.

SNAP (Food Assistance) Adjustments: The Supplemental Nutrition Assistance Program (SNAP) also faces federal funding cuts and expanded work requirements.

Affordable Care Act (ACA) Implications: New eligibility verification requirements are imposed for ACA marketplace coverage, and enhanced tax credits for ACA coverage are set to expire. This could lead to higher out-of-pocket premium payments for many, particularly older adults. The CBO estimates these changes could lead to a significant increase in the uninsured population.

Your Action Plan: Reassess your healthcare and benefits planning. Explore alternative options if you’re impacted by changes to Medicaid or ACA, and adjust your budget accordingly.

Retirement & Savings: New Avenues and Program Shifts

The bill introduces both opportunities and challenges for your long-term financial goals:

“Trump Accounts” for Children: A brand-new savings option for newborns. These “Trump Accounts” receive an initial federal contribution of $1,000, with parents able to contribute up to $5,000 annually. Classified as IRAs, gains are tax-deferred until age 18. This is a new consideration for long-term savings for your children.

Student Loan Program Overhaul: Federal student loan programs are undergoing significant alterations, potentially ending subsidized and income-driven repayment options. Limits are also placed on Pell Grant eligibility. Current and future students will need to adjust their education financial planning.

HSA and 529 Expansion: Good news for healthcare and education savings. Eligible uses for Health Savings Accounts (HSAs) and 529 education savings plans are expanded, offering more flexibility.

Social Security Outlook: While the bill provides some temporary tax relief for seniors, its overall impact on the national debt could accelerate the insolvency of Social Security. This is a long-term consideration for retirement planning.

Your Action Plan: Evaluate “Trump Accounts” alongside existing savings vehicles like 529 plans. If you have student loans or are planning for higher education, understand the new repayment and eligibility rules. Review how you leverage your HSA and 529 plans for maximum benefit.

Investment & Business Considerations: Adapting to Policy Shifts

The OBBB also brings changes that could influence your investment portfolio:

Clean Energy Tax Credits: Many clean energy tax credits from the Inflation Reduction Act are being phased out, which may impact investments in renewable energy and electric vehicles.

Fossil Fuel Promotion: The bill promotes increased domestic oil and gas production, which could influence investment strategies in the energy sector.

Your Action Plan: Consider how these policy shifts might affect your investment portfolio. Diversification and a long-term perspective remain key.

Overall Financial Planning Implications: A Holistic Approach

The “Big Beautiful Bill” is a game-changer. It necessitates a comprehensive review of your financial strategy.

Review Tax Strategies: Don’t miss out on new deductions!

Reassess Healthcare and Benefits Planning: Understand potential impacts on coverage and eligibility.

Evaluate Savings Options: Explore new opportunities like “Trump Accounts” and expanded HSA/529 uses.

Update Estate Plans: High-net-worth individuals should revisit their estate plans due to increased exemptions.

Adjust Investment Portfolios: Align your investments with the new economic realities. If you’re a client of ours, we’ve already done this for you.

The “One Big Beautiful Bill” is far-reaching. Given its complexity, consulting with a qualified financial advisor and tax professional is highly recommended to understand how these provisions specifically impact your unique financial situation and to adjust your plans accordingly. Schedule time with a Warren Street advisor today. .

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/07/Big-Beautiful-Bill.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-07-10 12:14:072025-07-10 12:15:13The “Big Beautiful Bill”: What It Means for Your Finances

What should you do if you’ve just received a big bonus at work, inherited some money, sold a business, or come into a financial windfall? Should you invest it all at once, even if the market feels high or low, or take a gradual approach by investing in smaller increments over time?

This is a common question we hear from clients and investors alike. It’s no surprise—deciding how to invest a significant sum of money can feel overwhelming. What if you invest it now and the market drops? Or, what if you wait and the market takes off? It’s natural to worry about making the wrong choice or missing out on potential gains.

Both investing a lump sum immediately and spreading it out over time come with their pros and cons. Let’s explore some key factors to help guide your decision.

Start with Your Goals

Before making any investment decisions, consider your financial goals.

If you need the money for short-term purposes, like upcoming college tuition, the market’s volatility could be a concern. In this case, conservative options like short-term bonds, bond funds, or CDs might be better suited to protect your funds.

For long-term goals, such as retirement, investing in the stock market may be a better choice. Despite short-term fluctuations, the market has historically trended upward over time.

Compare Lump-Sum Investing vs. Dollar-Cost Averaging

Investing a lump sum means your money is fully exposed to the market immediately, allowing you to benefit from any immediate gains if the market is rising. However, since markets are unpredictable, a downturn could occur soon after you invest.

If the risk of short-term losses makes you uneasy, dollar-cost averaging (DCA)—where you invest a fixed amount at regular intervals—might be a more comfortable approach. For instance, you could invest $12,000 by putting in $1,000 monthly over a year. This way, you buy more shares when prices are low and fewer when they’re high, helping you manage the average cost over time.

Keep in mind, though, that research shows lump-sum investing outperforms DCA 68% of the time. If maximizing returns is your main goal, lump-sum investing could be the better option. However, if you’re worried about losses and potential emotional reactions, DCA may be worth the slight reduction in expected returns.

Don’t Wait to Invest

Historically, stocks and bonds outperform cash over the long term, so it’s important to start investing as soon as possible. Holding off is essentially an attempt to time the market, which is notoriously difficult. In 2023, equity fund investor returns trailed the S&P 500 by 5.5%, largely due to market timing efforts.

Both lump-sum investing and DCA help you avoid this pitfall, letting you benefit from the market’s long-term growth. The key is choosing the strategy that aligns with your risk tolerance and long-term plan.

If you’re unsure which strategy is best for you, reach out—we’d be happy to help you decide.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/04/Lump-Sum.png12602240Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-04-17 07:16:422025-04-17 07:19:16I’ve Got a Lump Sum in Cash, Should I Invest It Right Away?

If you’re a fan of public radio’s “Marketplace” with Kai Ryssdal, you might have noticed the music they play when they “do the numbers.” On days the market is up, it’s “We’re in the Money,” and when it’s down, they play “Stormy Weather.”

These musical cues are a fun way to connect with listeners’ emotions as they hear about market highs and lows. But they also illustrate how the media often uses various tactics to evoke emotional responses, making financial news feel more dramatic. Some of these methods are lighthearted, but others can be more misleading.

Take, for example, how market volatility is reported in terms of magnitude (the number of points an index moves) versus percentage change. Wall Street Journal columnist Jason Zweig has pointed out that while both describe the same movement, focusing on magnitude can often seem more dramatic.

However, this number doesn’t reflect where the index started. The Dow had closed at 39,737.26 points on August 2. A 1,033.99-point drop represents a 2.6% decrease—a notable one-day decline, but one that feels less dramatic when expressed as a percentage.

Zweig puts it succinctly: “By focusing on the magnitude, rather than the percentage, of price changes, news organizations…make markets feel more newsworthy, and volatile, than they are,” even acknowledging that his own publication can be guilty of this practice.

Why the Difference Matters

As human beings, we are prone to emotional reactions and cognitive shortcuts that aren’t always in our best interest. When we encounter information—especially if it appears alarming—we may focus on it in unproductive ways.

The way information is framed can significantly influence our reactions. This framing bias is similar to seeing a glass as half full or half empty. In this case, a 1,000-point drop in a market index might cause panic and lead to impulsive selling or, at the very least, cause anxiety. But remembering that this “big” drop is actually a 2.6% decline can help you maintain perspective.

How to Approach Market News

What should investors do when faced with market volatility? Start by recognizing the role emotions play in processing such information. When you hear a seemingly frightening statistic, question its true impact. Does it provide complete information? Is it taken out of context or exaggerated for effect? If so, it’s wise to view it with skepticism.

Once you understand how your biases and the presentation of information can influence you, you can focus on the long-term. Historically, the market has always risen over time. Sticking to your long-term investment plan allows you to benefit from this pattern.

If you ever have questions about the market and how to align your investments with your financial goals, feel free to reach out to us. We’re here to help you make informed decisions.

Veronica Cabral

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

As we approach the end of 2024, it’s an opportune time to reflect on the year’s financial developments and consider what 2025 may bring. We believe in understanding both the past and potential future of our economic landscape, which may help inform financial decisions.

This year has brought its share of financial developments, from market fluctuations to policy changes that have shaped the economic environment. Shifts in various sectors, interest rate movements, and global events have influenced financial strategies across the board.

Looking ahead to 2025, we anticipate new opportunities and challenges in the financial world. Our team watches current trends and indicators to provide some insights for the coming year.

In this review, we’ll examine the key financial events of 2024 and their impact and potential implications. We’ll then turn our attention to 2025, offering our perspective on trends that may emerge in the coming months.

Whether you’re a long-standing client or simply interested in staying informed, we believe this overview may provide some insights for your financial strategies as we move into the new year.

Key Economic Factors in 2024

Interest Rates

During the September meeting, the Federal Reserve voted to lower interest rates by 0.5 percent, the first reduction in rates since 2020. While the pivot was long-anticipated, the size of the cut surprised many pundits following the Fed’s all-out fight against inflation launched two years ago. The move, unusual in an election year, brought the benchmark federal funds rate to a range between 4.75% and 5%. Some anticipate the Fed may adjust interest rates again in 2024.1

Inflation

The decision to trim interest rates moved the central bank into a new phase, and preventing further weakening of the U.S. labor market is now an important priority. For most of the past 2½ years, the Fed focused on fighting inflation. With the Consumer Price Index receding from 6.4% in January 2023 to 2.9% this July, the Fed pivoted attention to the softening job market. By comparison, the seasonally-adjusted unemployment rate rose to 4.2% in August, up from 3.7% in January.1

GDP Growth

Real GDP growth rose by 3.0% quarterly annualized in Q2 2024, up from 1.6% in Q1 2024. This increase was led by stronger domestic demand and a surge in inventories. The Conference Board Economic Forecast estimates a 0.8% annualized GDP growth for Q3 and 1% annualized for Q4. With the third and final Q3 GDP estimate due to be released on December 19, attention will shift to Q4 and 2025. Looking into 2025, some economists watch the Atlanta Fed’s GDPNow tool, which gives a running estimate of real GDP growth based on available economic data for the current measured quarter.2

Market Performance

Equity markets have seen strong, if uneven, performance in 2024. As of the end of October, the S&P 500 index was up 19.62% while the Dow Jones Industrial Average rose 10.81%. The tech-heavy NASDAQ increased 20.54%.3

Bonds have also shown volatility in 2024. As of October 31, the total return of the 10-Year Treasury Note was 4.28%.4

Past performance does not guarantee future results. Individuals cannot invest directly in an index. The return and principal value of financial markets will fluctuate as conditions change.

Key Takeaways

Up Markets Can Still Experience Volatility

While equity markets had strong overall performance in 2024, stocks did not go up in a straight line. There were some scary moments for investors, like April 12, when inflation and geopolitical worries saw the Dow Jones Industrial Average slide by 1.24%, the S&P 500 tumble by 1.46%, and the Nasdaq pull back by 1.62%. That bad day for the markets was dwarfed by August 5, when worries about slowing U.S. economic growth caused the Dow to fall more than 1,000 points, or 2.6%, while the broader S&P 500 lost 3% and the Nasdaq fell 3.4%.5,6

As disconcerting as these pullbacks felt at the time, stocks returned to record highs by September. An important lesson from this year is that stocks can, and often do, go down. It’s also critical to know that, on average, stocks have corrected approximately every two years, and that correction typically lasts a few months. Corrections, which are declines of between 10% and 20% from a recent high, can occur for a variety of reasons, including when unexpected news shakes investors’ confidence. Selling investments during a downturn may lock in your losses and lower your potential long-term returns.7

Don’t Fight the Fed

The past year has reinforced the influence the Federal Reserve has over the markets and investor psychology. The Fed held rates steady for much of 2024. It wasn’t until the September meeting that they made an adjustment. Markets reacted to every Fed meeting and Chairman Jerome Powell press conference. With inflation down from its highs (but not yet at the Fed’s 2% target) and employment softening, but not cratering, the Fed may have orchestrated the oft-talked-about “soft landing” for the economy. The lesson learned for next year is to pay attention to what the Fed is doing and remember the old Wall Street saying, “Don’t fight the Fed.”

Markets Shift Focus in an Instant

We all know that stocks can be volatile, but we only seem to care when they are volatile on the downside. Those 24 hours of angst between August 5 and 6, when the Dow dropped more than 1,000 points due in part to angst over the Bank of Japan boosting interest rates at a time when investors were borrowing the yen on the cheap to buy higher-risk stocks and derivatives. I doubt many of us had “Bank of Japan” on our radar, but market psychology can shift abruptly from “it’s all good” to “the sky is falling” without much justification. Focus can flip from concerns over an overheating economy to fears of a job-crushing recession on a dime. One lesson we hope you take away from 2024 is not to let emotions control your investment decisions. A solid financial strategy should be designed to withstand short-term market moves and keep you on track toward your long-term financial goals.9

Artificial Intelligence (AI) is Here to Stay

AI has been a major market story in 2023 and 2024 and shows no signs of slowing. While AI has been advancing for decades, innovations in machine learning have found exciting and extraordinary new use cases in areas from healthcare to manufacturing. One popular chatbot jump-started the current AI interest, reaching 100 million monthly active users just two months after its launch, making it the fastest-growing consumer application in history.8

AI is being seen as the most innovative technology of the 21st century and has the potential to both enhance and disrupt major industries. Innovations in electricity and personal computers unleashed investment booms of as much as 2% of U.S. GDP as the technologies were adopted into the broader economy. Now, investment in artificial intelligence is ramping up quickly and could eventually have an even bigger impact on GDP, according to Goldman Sachs Economics Research.10

The AI lesson to take away from 2024 is that AI is not just focused on a handful of companies. Company interest in AI has already increased rapidly, with more than 16% of enterprises in the Russell 3000 mentioning the technology on earnings calls, up from less than 1% in 2016.10

Asset Allocation is Essential

Asset allocation is an approach to help manage, but not eliminate, investment risk in the event that security prices decline. The strategy involves spreading your investments across a wide range of assets to spread the risk associated with concentrating too heavily on any single investment. Simply put, diversification is the “don’t keep all your eggs in one basket” approach to portfolio construction.

Asset allocation is more than choosing a single investment, like one that is based on the S&P 500 stock index. One of the more significant and concerning trends in recent years has been the rise of market-cap-weighted indexes, which has led to increased concentration in just a few dominant stocks, mostly in the technology sector. Due to their outsized market capitalizations, these stocks, dubbed “The Magnificent 7,” may make up a disproportionate part of some investor portfolios. Another lesson from 2024 is that the downside can be significant when heavily concentrated stocks pull back simultaneously.11

Emergency Preparedness is Always Critical

The year 2024 has shown us that unexpected economic downturns or crises can impact investors without warning. You should consider having an emergency fund to cover living expenses so you aren’t forced to make short-term decisions that could impact your long-term goals. You should also work with a financial professional to discuss risk management strategies that can keep you moving toward your goals.

Prepare for What You Can, Don’t Overreact to What You Can’t

With the presidential election now behind us, potential tax and regulation policy transitions remain. Politically speaking, implementing policy goals and regulations is more challenging than making pledges. Be ready to shift strategies for you, your loved ones, and your heirs if necessary. In other areas, there may be little you can do other than to try not to overreact to what comes down from Washington. Working with financial, tax, and estate professionals can help you navigate what may happen in 2025 and beyond.

Applying Lessons and Looking Forward to 2025

As we reflect on the financial landscape of 2024, it’s clear that the market continues to evolve in response to global events, technological advancements, and economic policies. The lessons from this past year underscore the importance of maintaining a balanced, long-term perspective with your personal finances.

To summarize the key takeaways from 2024:

Market volatility remains a constant, emphasizing the need for diversified portfolios.

The Federal Reserve’s decisions continue to impact market dynamics.

Emerging technologies, particularly AI, are reshaping industries and potentially creating new investment opportunities.

Global events can rapidly shift market focus, reinforcing the value of a well-structured financial strategy.

Looking ahead to 2025, we anticipate continued evolution in the financial sector and are committed to staying on top of these changes and providing you with timely insights and guidance. Our team is dedicated to helping you navigate the complexities of the financial world and working towards your long-term goals.

We will continue to monitor key economic indicators, policy changes, and market trends, sharing our analysis through our regular blog posts and communications. Our aim is to provide you with the information and support you need to make informed financial decisions in the coming year and beyond.

Remember, personal finance is a collaborative effort. While we provide the insights, your personal goals and circumstances are at the heart of every strategy we develop. We encourage you to reach out to us with any questions or concerns as we move into 2025.

Thank you for your continued trust in our team. We look forward to guiding you through another year of financial opportunities and challenges.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

3. Yahoo.com, October 31, 2024. The S&P 500 Composite Index is an unmanaged group of securities considered to be representative of the stock market in general. Past performance does not guarantee future results. Individuals cannot invest directly in an index. The return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost.

4. Yahoo.com, October 31, 2024. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

If you’re like most people, you need your investments to grow to achieve the life you want. Fortunately, there’s a simple yet powerful tool that can help you achieve that growth: compounding. Compounding is the process of earning returns on your past investment returns.

The Wonders of Compounding

Compounding can help your portfolio grow exponentially over time. Here’s a simplified example:

You invest $10,000 and earn a 10% return in the first year. By the end of the year, you have an additional $1,000, totaling $11,000. If you keep it invested and earn another 10% return the next year, your 10% return now produces $1,100 rather than $1,000.

The more your investments grow, the more you can reinvest for further growth.

You can pull a couple key levers to make the most of compounding. Using these strategies wisely can significantly boost your savings:

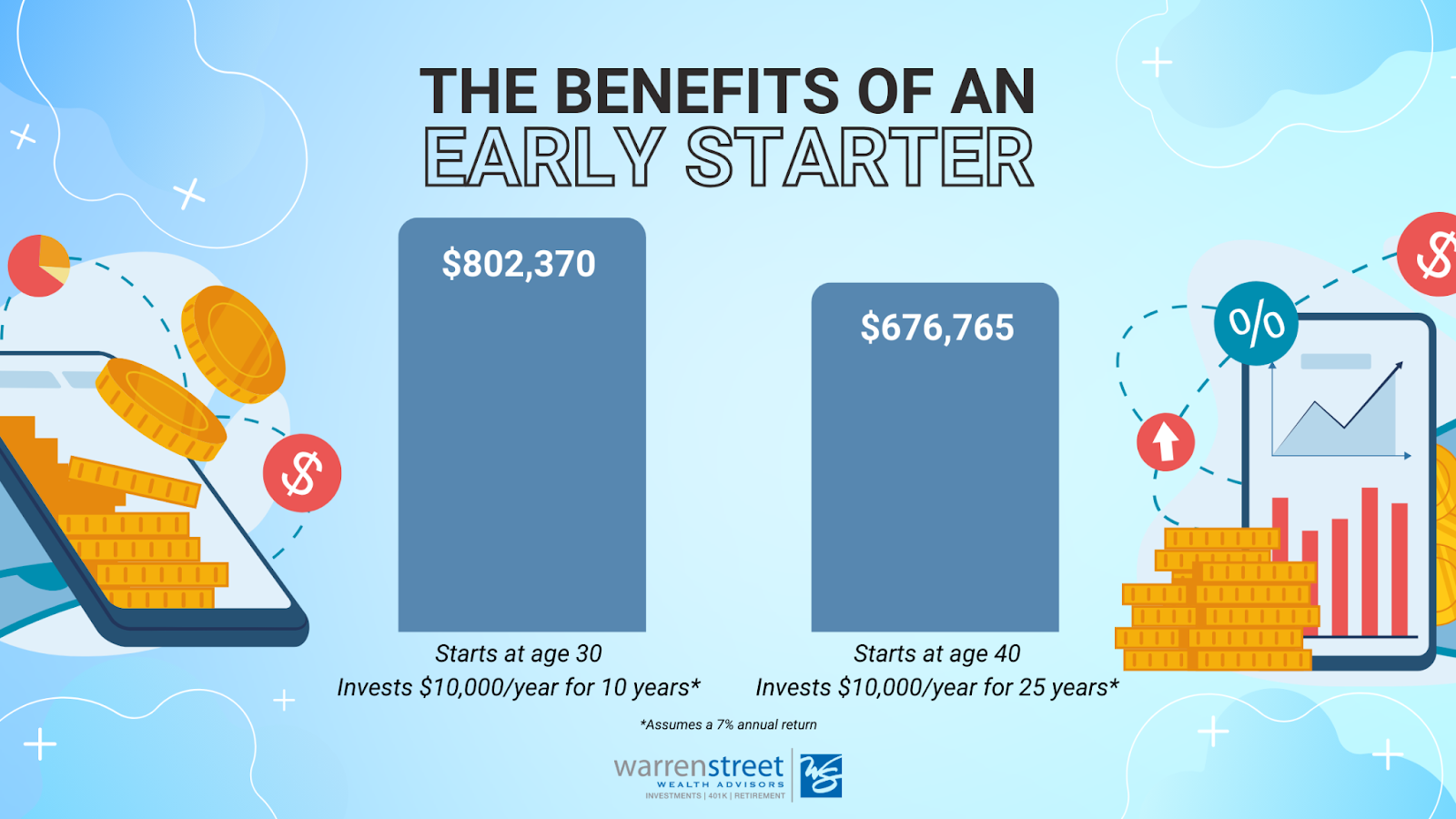

Give It Time

Time allows your investments to snowball. The longer you let your returns compound, the greater the snowball effect. Here’s an example why:

Investor 1: Starts at age 30, invests $10,000 annually for 10 years, earning a 7% annual return. They contribute a total of $100,000 and then stop adding money but let it grow.

Portfolio value at age 65: $802,370

Investor 2: Starts at age 40, invests $10,000 annually for 25 years, earning a 7% annual return. They contribute a total of $250,000.

Portfolio value at age 65: $676,765

Despite contributing $150,000 more, Investor 2 ends up with about $125,000 less than Investor 1. Starting early makes a huge difference.

Make the Most of Tax Advantages

Taxes can reduce compounding’s power. In a taxable account, interest, dividends, and capital gains trigger taxes that lower your annual return. Lower returns mean less money to grow the next year.

However, in tax-advantaged accounts like a 401(k), traditional IRA, or Roth IRA, you don’t pay taxes on gains while the money is in the account. This allows all your gains to keep working for you.

Traditional 401(k) and IRA: You contribute pre-tax money, it grows tax-deferred, and withdrawals after age 59 ½ are taxed at normal income tax rates.

Roth IRA: You contribute after-tax money, it grows tax-free, and withdrawals after age 59 ½ and a 5-year holding period are tax-free.

Control What You Can

Like most things in life, investing has many uncontrollable elements, so focus on what you can control. Start early, stay invested for the long term, and use tax-advantaged accounts to maximize compounding and work towards your long-term goals.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/08/Compounding-Return-Basics-101.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-10-17 07:35:002024-10-15 06:58:33How Compound Returns Work: A Guide to Growing Your Money

A small slice of equity compensation can boost your income, while a larger slice might bring a significant financial windfall. However, luck and careful management play crucial roles. Balancing the risks and rewards of your equity compensation is essential. Understanding how it fits into your overall financial plan can help you maximize benefits and avoid concentration risk—the danger of having too much wealth in one stock.

Equity Compensation Basics

Equity compensation comes in various forms, such as stock options, restricted stock units, or employee stock purchase plans. The equity package you receive might come with a vesting schedule, which determines how quickly you’re able to take ownership of your shares. For companies, these vesting schedules accomplish an important goal: They help keep you around longer.

Understanding every part of your equity compensation package is essential. This includes vesting rules, types of shares, expiration dates for exercising stock options, and tax implications. Missing an expiration date can mean losing the chance to buy company stock at a discount, and knowing the tax details can help you manage your tax burden and retain more of your hard-earned equity. While you don’t need to master every detail, it’s crucial to understand your equity compensation offer.

At Warren Street, we guide clients through the wealth-building potential of their executive compensation packages. We help you maximize opportunities, integrate the package with your broader financial goals, and collaborate with other resources. For example, your company’s HR department or benefits administrator can provide details, your accountant can advise on taxes, and a lawyer can help with legal aspects and estate planning related to your equity compensation.

Understanding the Risks of Equity Compensation

One downside of equity compensation is that it can tie up a large portion of your wealth in a single stock. This is known as concentration risk.

Not all risk is bad. In fact, a foundational part of investing is taking on risk in exchange for potentially higher returns. This is systemic risk—the risk inherent in the financial markets at large. However, concentration risk means your wealth is closely tied to one company’s performance, posing significant danger if the company faces issues like scandals or competitive disruptions.

Relying on your employer for income and savings can be risky. If the company performs poorly, you could lose both your job and a significant part of your wealth. For example, during the 2020 pandemic, ridesharing company stock prices tended to lose value as ridership plummeted. These companies laid off thousands of workers, and employees lost both jobs and equity value.

“But” you may counter, “I know my own company, and I’m confident its future is bright.” This is a common reaction—and may be a sign you’re falling into a common behavioral tendency known as familiarity bias. It can lead you to the false assumption that your own company is safer, and your familiarity may actually be keeping you from making a level-headed investment decision. Instead, lean on objective data and research rather than feelings to inform your investment decisions.

Solving Concentration Risk

Minimize concentration risk by diversifying, carefully divesting company shares, and investing in broad market funds. This approach smooths out volatility, maximizes long-term returns, and manages systemic risks.

If you work for a privately held company, selling your shares can be more tricky—and perhaps not possible. In that case, we can help you explore options to reduce risk. For example, that may mean building a larger emergency fund to give you more protection from the unexpected or exploring financial strategies to hedge your equity position.

No matter your equity compensation package, you don’t have to navigate its complexities alone. Contact us to discuss your options and maximize your financial potential.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/08/Equity-Compensation-Opportunities-Risks.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-09-05 08:07:002024-11-07 09:16:54Equity Compensation: Benefits and Risks You Need to Know

In the first installment of our Young Investor’s Guide to Building a Financial Future, we looked at avoiding credit card debt to set you off to a healthy start, the benefits of investing over the long term and the advantages of doing so in a retirement account, such as a 401(k) or IRA.

In the second part of this two-part series, we discuss three more investment concepts every young investor may want to embrace:

The importance of diversification

The dangers of market timing and stock picking

The benefits of investing according to a plan that fits your personal goals

Get Diversified

Short-term market swings can challenge even the most resilient investors. However, history shows that over the long term, markets tend to smooth out and trend upward. Diversifying your investments involves spreading risk across various types of assets, not just increasing the number of holdings.

While this may make intuitive sense, many investors come to us believing they are well-diversified when they are not. They often hold numerous stocks or funds across multiple accounts, yet upon examination, their portfolios are heavily skewed towards large U.S. companies or narrow market sectors. Diversification is effective because various investments respond differently to market shifts. When one falters, others may thrive, balancing overall portfolio performance. However, if holdings are too similar, the benefits of diversification diminish over time.

In short:

Investing in a wide range of assets from different sectors, sizes, and geographies can create a robust portfolio that is better equipped to handle market fluctuations over time.

Avoid Speculating

Focusing on broad market indices helps avoid detrimental speculative behaviors that can harm long-term returns.

Market timing—buying and selling stocks based on breaking news and short-term market movements—often turn out poorly. Because you’re typically buying into hot trends and selling when conditions are scary, you end up buying when prices are high or selling when prices are low. In both cases, that behavior can significantly impact savings and hinder financial goals

In fact, research consistently shows that investors’ attempts at market timing generally underperform broader indices like the S&P 500, with average equity fund investors trailing by approximately 5.5% in 2023 due to poor timing decisions according to a long-running annual survey of investor behavior by DALBAR.

Similarly, stock picking can reduce diversification and increase concentration risk, where a few stocks can heavily influence your portfolio’s performance. Investors are typically rewarded for taking on systematic risk, or risk inherent to the entire market. Concentration risk is not systematic. It is specific to individual stocks and doesn’t reliably yield rewards. Holding a significant portion of your portfolio in a few stocks exposes you to outsized impacts; for example, a single company’s bankruptcy could lead to substantial losses.

It’s also exceedingly difficult to pick stocks that will outperform the broader market over time. In 2023, over 70% of companies in the S&P 500 Index underperformed the index. These results vary from year to year. But since a handful of companies often drive most of the stock market’s returns, choosing just when to sell the future losers and buy the next big winners can end up becoming an impossible—and often losing—game.

In short:

Timing the market can lead you to buy stocks when they’re expensive and lock in losses by selling during downturns. When it comes to stock picking, it’s exceedingly difficult to pick single stocks that will be winners, and holding concentrated stock positions can introduce uncompensated risk to your portfolio. Instead, build a diversified portfolio as part of your long-term financial plan.

Follow a Plan That Fits Your Goals

So how should you divide up your diversified investments? Start with your asset allocation, which is how your portfolio is spread among asset classes including stocks, bonds and cash. Then base your asset allocation on your personal goals, tolerance for risk and the length of time you have to invest.

In short:

Build your portfolio based on your personal goals, risk tolerance and time horizon rather than chasing or fleeing hot or cold investments or focusing on generalized rules of thumb.

Interested in learning more about how to take the first steps toward meeting your personal financial goals? Reach out to set up a time, and let’s talk.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/06/Young-Investor-Guide-Part-2.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-08-01 09:05:172024-08-01 09:05:22Young Investor’s Guide to Building a Financial Future—Part 2: Investing for Your Goals

The future looks bright for younger investors. A 2024 analysis by the Investment Company Institute found that, adjusted for inflation, Gen Zers have nearly three times more retirement assets than Gen Xers did at the same age. This shift is largely due to improvements in the retirement system, such as 401(k)s and employee stock purchase plans.

For new investors, getting started can be overwhelming. With so much information out there, it can be hard to know where to start. The good news is that understanding a few basic principles can set you on the path to a healthy financial future.

In this first of a two-part series, we’ll cover three key concepts for young investors:

Getting started on the right foot by avoiding debt

Embracing the power of long-term investing

Making the most of tax-advantaged accounts

Avoid the Vicious Cycle of Credit Card Debt

Debt impacts your financial life, reducing money available for future growth. Every dollar spent on paying down a credit card bill or car loan is one less dollar that can grow for your future. Minimizing bad debt is essential for a strong financial future.

Not all debt is bad. Low-interest student loans and reasonable mortgages can be beneficial as you can follow a career path or build equity. However, high-interest credit card debt can quickly become expensive and hinder your ability to save and invest.

Credit card debt is particularly harmful due to high interest rates, often around 20% or more. If you carry a balance, interest accrues, and making only minimum payments means your debt grows over time. For example, let’s say you have $1,000 in debt on a credit card with a 20% interest rate. If you only make minimum payments of 2%, it will take you 195 months—more than 16 years—just to pay off this single debt. In that time, you will have paid $2,126.15 in interest—more than double the amount of your original debt.

In short:

Use high-interest debt cautiously and pay off your credit card balance quickly. This avoids debt cycles and frees up cash for saving and investing.

Stay Invested for the Long Haul

As a young investor, you may have limited funds, but you have plenty of time. Decades until retirement mean your modest investments can grow significantly.

This growth is due to compounding returns—earning returns on your returns. The longer your money is invested, the more it benefits from exponential growth. In tax-advantaged retirement accounts, these benefits are magnified as tax-deferred and tax-free growth allows even more money to compound over time.

In short:

The longer you stay invested, the more your investments can grow exponentially, thanks to compounding returns.

Make the Most of Tax-Advantaged Retirement Accounts

The government incentivizes saving for the future by offering substantial tax benefits through retirement savings plans like 401(k)s and individual retirement accounts (IRAs).

Employer-sponsored plans such as 401(k)s allow you to contribute pretax income, with a maximum contribution of $23,000 in 2024. Additionally, many employers match your contributions, essentially offering free money. Contribute enough to receive these matches to maximize your benefits.

During tax season, neither your contributions nor your employer’s contributions are taxed as income, and investments within the account grow tax-deferred. You won’t have to pay any taxes until you start taking withdrawals from that account, encouraging the growth of your savings through compounding. Eventual withdrawals are taxed at ordinary income tax rates and withdrawing before age 59½ may incur a 10% penalty on top of regular taxes.

If you want to save even more, consider traditional IRAs, which also permit pre-tax contributions (up to $7,000 in 2024). Like 401(k)s, investments in traditional IRAs grow tax-deferred, with withdrawals taxed as ordinary income.

Alternatively, there is one other account: Roth IRAs. Unlike traditional IRAs, Roth IRA contributions are after-tax, meaning contributions aren’t tax-deductible, but withdrawals in retirement are tax-free. This arrangement is advantageous, especially for younger investors in lower income tax brackets, as investments grow tax-free. After your account has been open for five years, you can access your principal contributions penalty-free. However, withdrawing investment gains before age 59½ may incur penalties. Nonetheless, it’s essential to view retirement funds as a last-resort resource and prioritize long-term saving goals over short-term needs.

In short:

Maximize contributions to retirement plans to leverage their tax-sheltered growth. and take full advantage of employer matching contributions to optimize benefits.

Next up, we’ll take a look at the importance of building a diversified investment portfolio, why speculating can harm your long-term prospects, and how to build an investment plan that meets your individual goals.

Interested in learning more about how to take the first steps toward meeting your personal financial goals? Reach out to set up a time, and let’s talk.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/06/Young-Investor-Guide-Part-1.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-07-11 08:43:132024-08-01 09:04:48Young Investor’s Guide to Building a Financial Future—Part 1: Where Do You Start?

So much of investing is beyond our control (picking stock prices, timing market movements, and so on) that it’s nice to know there are several “power tools” that can potentially enhance overall returns. Tax-loss harvesting is one such instrument, but — like many tools — it’s best used skillfully, and only when it is the right tool for the task.

The (Ideal) Logistics

When properly applied, tax-loss harvesting is the equivalent of turning your financial lemons into lemonade by converting market downturns into tangible tax savings. A successful tax-loss harvest lowers your tax bill, without substantially altering or impacting your long-term investment outcomes.

Tax Savings

If you sell all or part of a position in your taxable account when it is worth less than you paid for it, this generates a realized capital loss. You can use that loss to offset capital gains and other income in the year you realize it, or you can carry it forward into future years. We can realize losses on a holding’s original shares, its reinvested dividends, or both. (There are quite a few more caveats on how to report losses, gains, and other income. A tax professional should be consulted, but that’s the general premise.)

Your Greater Goals

When harvesting a loss, it’s imperative that we remain true to your existing investment plan. To prevent a tax-loss harvest from knocking your carefully structured portfolio out of balance, we reinvest the proceeds of any tax-loss harvest sale into a similar position (but not one that is “substantially identical,” as defined by the IRS). Typically, we then return the proceeds to your original position no sooner than 31 days later (after the IRS’s “wash sale rule” period has passed).

The Tax-Loss Harvest Round Trip

In short, once the dust has settled, our goal is to have generated a substantive capital loss to report on your tax returns, without dramatically altering your market positions during or after the event. Here’s a three-step summary of the round trip typically involved:

Sell all or part of a position in your portfolio when it is worth less than you paid for it.

Reinvest the proceeds in a similar (not “substantially identical”) position.

Return the proceeds to the original position no sooner than 31 days later.

Practical Caveats

An effective tax-loss harvest can contribute to your net worth by lowering your tax bills. That’s why we keep a year-round eye on potential harvesting opportunities, so we are ready to spring into action whenever market conditions and your best interests warrant it.

That said, there are several reasons that not every loss can or should be harvested. Here are a few of the most common caveats to bear in mind.

Trading costs – You shouldn’t execute a tax-loss harvest unless it is expected to generate more than enough tax savings to offset the trading costs involved. As described above, a typical tax-loss harvest calls for four trades: There’s one trade to sell the original holding and another to stay invested in the market during the waiting period dictated by the IRS’s wash sale rule. After that, there are two more trades to sell the interim holding and buy back the original position.

Market volatility – When the time comes to sell the interim holding and repurchase your original position, you ideally want to sell it for no more than it cost, lest it generate a short-term taxable gain that can negate the benefits of the harvest. We may avoid initiating a tax-loss harvest in highly volatile markets, especially if your overall investment plans might be harmed if we are unable to cost-effectively repurchase your original position when advisable.

Tax planning – While a successful tax-loss harvest shouldn’t have any impact on your long-term investment strategy, it can lower the basis of your holdings once it’s completed, which can generate higher capital gains taxes for you later on. As such, we want to carefully manage any tax-loss harvesting opportunities in concert with your larger tax-planning needs.

Asset location – Holdings in your tax-sheltered accounts (such as your IRA) don’t generate taxable gains or realized losses when sold, so we can only harvest losses from assets held in your taxable accounts.

Adding Value with Tax-Loss Harvesting

It’s never fun to endure market downturns, but they are an inherent part of nearly every investor’s journey toward accumulating new wealth. When they occur, we can sometimes soften the sting by leveraging losses to your advantage. Determining when and how to seize a tax-loss harvesting opportunity, while avoiding the obstacles involved, is one more way we seek to add value to your end returns and to your advisory relationship with us. Let us know if we can ever answer any questions about this or other tax-planning strategies you may have in mind.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.