As proud Tustin residents, Warren Street was thrilled to support the Tustin Public Schools Foundation at the 31st annual Dino Dash, a community walk-run event. The Tustin Public School Foundation uses proceeds from the event to support initiatives such as sports programs, robotics programs, and grants to teachers for enrichment programs.

Our Director of Financial Planning, Emily Balmages, CFP®, CRTP has participated in the event for nearly a decade with her family and views it as a highlight of her year.

Director of Financial Planning Emily Balmages and her daughter, Lola and son, Max in 2011.

“I was raised in the Tustin School District, and now my kids are receiving an education there,” Emily said. “It’s such an impressive school district — from the quality of education and diversity of the student body to the quality of teachers and staff. I’ve seen the great things these kids end up doing — personally, professionally, and in their communities.”

Director of Financial Planning Emily Balmages and her son, Zach, at the 2022 event.

Emily’s Tustin pride runs deep, and the entire Warren Street team also shares that passion for the city that we call home. This year, Emily and her son, Zach, were joined by a number of other Warren Street team members at the Dino Dash: Founding Partner and President Cary Facer and his sons, Reed and Grant, and Client Service Associate Aileen Obedoza.

The boys ran the race together, while the rest of the team manned the popular Warren Street booth (the spin-the-wheel game was a hit!). All in all, nearly 8,000 people attended the event.

Founder and President Cary Facer with Client Service Associate Aileen Obedoza.

As Founder and President Cary Facer put it, “I was blown away by the turnout and amount of people who stopped by to spin the wheel! Seeing the community come out to support all the runners reminds me why it’s so important to get involved and give back to the local community.”

Grant and Reed Facer post-race.

Grant and Reed Facer, Cary’s 10- and 8-year-old sons, agree. “I liked running with Zach and Reed. The best part was just hanging out and talking,” Grant said.

At the heart of Warren Street’s mission is to put clients first in all things, and that commitment extends to our community. We were proud to support such a meaningful mission and have a feeling we’ll be back next year!

Jennifer La

Marketing Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

You just learned that you are going to have a new baby or child join your family, by birth or adoption. It’s an exciting time! As you start to make preparations you will quickly discover that there is a seemingly endless list of things to do, items to buy, books to read, and classes to take.

Despite what the targeted ads and influencers may tell you, it doesn’t matter too much if your bundle of joy has state-of-the-art nursery gear or the trendiest stroller on the market. But there are a few financial planning considerations that will make a world of difference for your family and your child’s well-being.

1. Estate Planning

As soon as you become responsible to care for a dependent, basic estate planning documents are essential. You may think you don’t currently have an estate plan if you have not drafted a will or trust, but guess what? You actually do have an estate plan! It was written for you by federal and state law and will be administered by a court (at your estate’s expense). If you pass away you can either rely on the state’s estate plan for you, or you can have the peace of mind that comes from writing your own estate plan that is specific for your wishes and your family’s best interests.

At a minimum, all parents (or anyone with financial dependents) should have (a) a will that includes guardianship designations, (b) an advanced health care directive, and (c) a durable power of attorney. Many parents or guardians will also want to establish a trust.

In addition to drafting these documents, we also recommend making sure that you have named non-minor primary and contingent beneficiaries on all your financial accounts and life insurances. At your death, many accounts will simply pass to the named beneficiaries on file.

If you were to pass away tomorrow, your partner and/or children would most likely need additional financial support. The cost of a funeral, additional child care, extra time off work, and covering everyday expenses and bills can add up. Not to mention the desire many parents have to help with specific expenses, such as education, for a child. Life insurance can fill that gap and provide vital support and peace of mind to your family during a difficult time.

Whatever role you serve in your household, there is a cost to your absence. If you are an income-earner for your household, the loss of your income would need to be supplemented for your family. If you are the primary caretaker of children and household manager, your labor would need to be replaced. Life insurance is for everyone with dependents, no matter their income-earning or employment status.

Term life insurance is usually inexpensive and easy to obtain. We strongly recommend term life insurance for all parents or those with dependents.

3. Extra Cash Savings

The cost of having a baby is no small thing. There are baby essentials to buy, doctor’s appointments to attend, and the labor and delivery bill at the end. It can add up to thousands of dollars to bring a new life into the world, and that is without a single complication. Additional medical care, a NICU stay, or any other unexpected circumstances can compound the bill.

When you find out that you, or your partner, is pregnant, you should start making plans for your cash flow needs. Remember that so much of the next 9-12 months is unpredictable for your bank account, so having a larger-than-average cash reserve is a good idea.

Medical care and baby items are the first expenses that come to mind when planning for your new child. But it is wise to also consider what other large expenses may come up during the pregnancy and postpartum period. Your savings account during this time has to do double duty as a baby preparedness fund and an ongoing emergency fund.

Consider two of the biggest culprits for emergency fund withdrawals – home repairs and car repairs. Do you have a lingering issue with a home appliance that is going to require a repair or replacement any day? Is your old car on its last leg? Is there anything in your house or car that needs to be addressed to ensure safety for your little one? Keep in mind that these non-baby expenses can and should be part of all the other preparations.

There is no hard fast rule for how much to save for a new baby, but having easily-accessible cash in a savings account is a must. If your emergency fund is slim, it may be time to pause aggressive debt repayment plans, saving for your next vacation, or excessive spending on non-essentials and put that extra cash in savings. Once you have returned to a more predictable financial situation, you can reevaluate your budget and priorities and return to your usual emergency fund and other financial goals.

4. Know Your Legal Rights and State Benefits

The state that you work in may have specific laws that require your employer to provide a certain amount of leave for pregnancy-related disability and/or bonding with a new child. Your state may also have paid leave or disability pay available for pregnancy and the postpartum leave period. You should carefully research your legal rights as a worker in your state and be familiar with all the benefits available to you.

In California, there are three laws or resources available to support you during pregnancy and postpartum and to bond with a new child: the Family and Medical Leave Act (FMLA), Paid Family Leave (PFL), and State Disability Insurance. FMLA legally protects the ability of eligible employees to take up to 12 workweeks of unpaid leave a year. PFL provides up to 8 weeks of payments for lost wages due to time off work to bond with a new child. State Disability Insurance may provide payments during pregnancy and postpartum recovery if you are unable to work.

Visit the following state websites to learn more about these California benefits:

On top of any legally-required paid or unpaid leave, your employer likely has their own company policies related to family leave. Ask your HR representative for all the information you can get about these policies. Start making a plan for how you (and your partner, if applicable) will take leave and how you will bridge any gaps in income during this time.

Your ability to negotiate paid or unpaid leave depends on various factors, but many employers are becoming more family friendly. Talk with a trusted supervisor or manager about your options. Don’t be afraid to negotiate and ask for what you need in terms of additional paid time off, schedule flexibility, or extended leave.

– – –

Are you expecting a little one? First – congratulations! If you feel like now is the time to get the support of a financial professional for your growing family, contact Warren Street for a one hour consultation.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/11/New-Parents-FP-Blog-Thumbnail.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-11-10 08:21:002024-11-07 09:27:45Essential Financial Planning for Expecting Parents

Welcome to our current edition of “Meet the Team.” We sat down with Emily Balmages, Director of Financial Planning at Warren Street, to learn more about her role, hobbies, and goals for the future. Join us in getting to know Emily below!

In your role as Director of Financial Planning, how do you assist Warren Street’s clients?

In collaboration with the rest of the team, I help families organize their finances. We proactively work to help them find ways they can grow their assets and portfolios, while saving on taxes.

Most importantly, our team is here to make sure clients have a professional in their corner, looking after the big-picture of their financial lives. Our goal is to take financial management off their plates, so they can focus on doing things they enjoy — whether that’s traveling, running their own business, spending more time with loved ones, or enjoying the retirement that they have worked so hard to save for. Clients can trust us to watch over the financial aspects of their lives. Most of my clients have spent the bulk of their lives working hard to get to the point where they can retire – I want to help them enjoy it!

On a personal level, as director, it’s my job to make sure we consistently deliver a high-quality experience to clients. That means keeping our team educated on industry happenings and tax law changes; managing our network of professional partners (CPAs, attorneys, and insurance agents); and researching emerging technology solutions.

How does Warren Street align with your personal values?

The top core value at Warren Street is putting our clients’ best interests first. This aligns perfectly with my personal value of “Do the right thing, no matter what,” even if it’s hard, even if it’s scary. I try to live by that rule in my personal life — and that commitment extends seamlessly into my professional life at Warren Street, where we are all Fiduciaries committed to acting in our clients’ best interests.

Another personal value of mine that I share with Warren Street is how family-oriented our group is. We are all 100% committed to our work but also 100% committed to our families, and that’s something I value a lot. Every leader here wants each person to succeed in their job, while still having a strong family life.

What do you love most about working at Warren Street?

For one, I love my clients! Often our relationships extend beyond financial conversations and we get to become close friends. I also love that I get to work with the incredible Warren Street team — truly hardworking, thoughtful, generous people.

Who or what motivates you?

I was raised by wonderful parents. They were always so dependable, generous, and considerate of the people around them. I am very inspired to reach that same level in both a personal and professional capacity.

I’m also passionate about financial literacy: simplifying financial advice to help families and individuals understand financial topics. It’s my goal to help people feel confident about their financial situations and the decisions they’re making — especially when going through life transitions such as a retirement, birth, marriage, divorce, or death. Those events can be a shock to our lives and a shock to our financial goals. Knowing I can help people weather those storms is incredibly motivating.

What are three fun facts about you?

I can juggle. My dad taught me when I was very young. It’s a rite of passage in my family that the kids learn to juggle at a young age!

We go to the UC Berkeley family camp in the Sierras — Lair of the Golden Bear — every year. I’ve attended since my childhood and I enjoy continuing the tradition with my family.

My 19-year-old daughter and I became weightlifting partners during the pandemic, and we love it! We go three days a week and have a lot of fun with it.

What are your aspirations?

Professionally, I aspire to carry on Cary and Blake’s momentum with the firm, continuing to scale and grow Warren Street while still providing client-focused service, based on relationships.

Personally, my husband and I are on a mission to try every brewery in Orange County (recommendations welcome). 🙂

Have questions about your finances? Emily will be happy to meet with you and address any questions you may have. Click here to schedule a complimentary consultation with her.

Veronica Torres

Director of Operations & Chief Compliance Officer, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

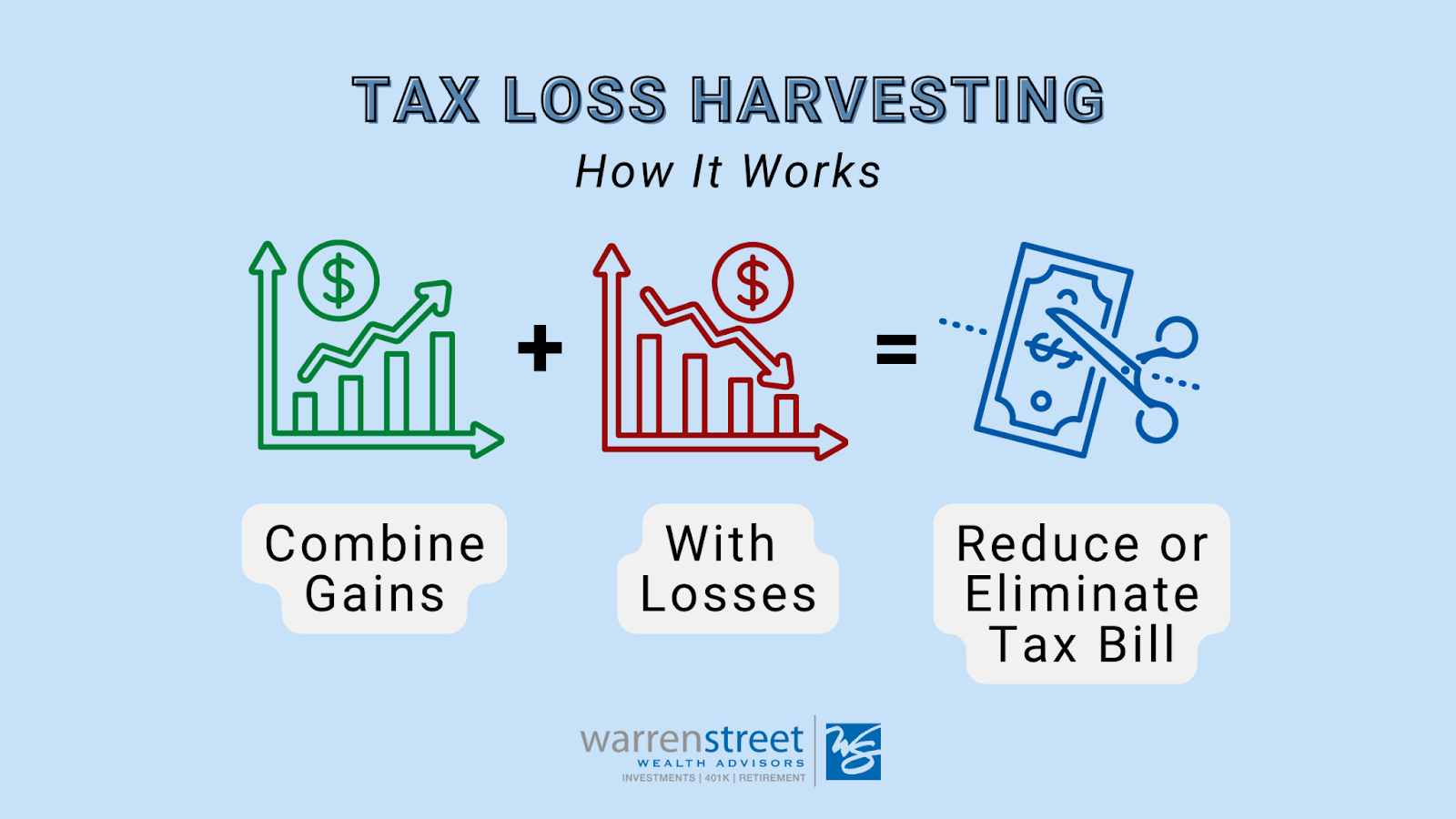

When we invest money, our main objective is to see the money grow. When we think about market losses and downturns, we may think of painful periods where we watch our account balances decrease instead of grow. While market losses are never fun, they are unfortunately a part of the normal investment life cycle. However, when market volatility hands us losses, there are some options to make lemonade out of lemons.

What is tax loss harvesting?

Tax loss harvesting is the process of selling securities while they are at a loss, realizing that loss for tax purposes, and then redeploying that money into another investment (such as a different stock, bond, or mutual fund). The IRS does not allow you to sell an investment at a loss, receive the tax benefit, and then immediately reinvest those proceeds into the exact same security right away. Selling a security and re-purchasing it within the same 30-day window is called a “Wash Sale.” You can avoid triggering the Wash Sale rule by investing in something similar but different enough to avoid having the rule apply.

While most people will tend to do this only once at year end, this is actually something that can be done at any time in the year with no limit as to how frequently you do so. With custom indexing and commission-free trading, frequent tax loss harvesting has become more achievable than ever. In years of high volatility, frequently harvesting tax losses can have a big impact on your tax bill.

Keep in mind that for this strategy to work, you must have capital invested in a taxable, non-retirement brokerage account. Your 401(k) and IRA are not eligible for tax loss harvesting.

How does it benefit you?

In years of extreme volatility, you may be able to accumulate a large amount of tax losses in a short period of time. These losses can then be used to offset future capital gains. If you end up with more tax losses than you have gains to offset them in any given year, you can use the losses to offset up to $3,000 of ordinary income on your tax return.

You will be able to carry forward an unlimited amount of these losses into future tax years until you’ve been able to use them up.

Tax loss harvesting can be especially useful for investors who might have highly concentrated company stock with a large amount of unrealized gains, or other legacy investments that they’ve been holding onto to avoid a large tax impact. These tax losses can be used to help decrease single stock risk and sell off legacy assets with little to no tax impact.

What are the next steps?

If you are a Warren Street client, we are already doing this for you (as applicable). For clients with larger taxable brokerage accounts invested in our custom indexing strategy, you will likely see tax loss harvesting happening on a more frequent basis.

All in all, seeing losses reported on your Form 1099 form is not necessarily a bad thing. While your long term objective remains the same in terms of seeking growth, taking advantage of short term volatility through tax loss harvesting can lead to a nice tax perk that can aid in your overall financial return on investments in the long run.

If you have any questions or would like to speak with one of our advisors for complimentary portfolio review, you can schedule a consultation here.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/09/Blog-Thumbnail.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2022-09-22 08:08:002022-09-22 18:19:31Tax Loss Harvesting: How to Make the Most Out of Market Volatility

Welcome to our current edition of “Meet the Team.” We sat down with Veronica Cabral, Director of Operations and Chief Compliance Officer at Warren Street, to learn more about her role, hobbies, and goals for the future. Join us in getting to know Veronica below!

In your role as Director of Operations and Chief Compliance Officer, how do you assist Warren Street’s clients?

I manage all our business processes and workflows on the backend, so our associates and advisors have a streamlined process when serving our clients.

In my new role as Chief Compliance Officer, I also keep an eye on everything compliance-related to make sure we have the right systems and programs in place to protect our clients.

How does Warren Street align with your personal values?

At Warren Street, we have a really big emphasis on putting clients’ best interests first and always being transparent and honest. I try to lead a similar life personally with my family and friends. I like to try to put others first and consider how my actions affect them. I’m also really big on being open, honest, and transparent. I carry those values back and forth between work and my personal life.

What do you love most about working at Warren Street?

What I love most is the flexibility I’ve had with my role. What I mean by that is at a really large corporation, I might have gotten boxed into a specific role. Because we are a smaller firm, I’ve been able to grow and take on many responsibilities quickly. I really appreciate the flexibility and trust that Cary and Blake have placed in me to explore and not just stay comfortable.

What is your biggest accomplishment thus far?

Professionally, taking on the role of Chief Compliance Officer. It’s definitely a lot of responsibility, but I’m thankful for the trust that’s been placed in me.

Personally, my biggest accomplishment has been my husband and I buying our house!

Who or what motivates you?

I was born in Mexico, so my parents came here when I was two. Knowing that they left what was super comfortable for them back home to come here to fight for a better life motivates me to honor their sacrifice. I want to make sure that we are always getting better with every generation. My family and husband both motivate me every day to be my best for them.

What are your aspirations?

Professionally, I’d love to stay at Warren Street and continue to grow with the company.

Personally, I hope to build on my Vee Make Cents brand, expanding the platform and formalizing educational programs that empower young women to get more comfortable with money.

What are three fun facts about you?

1. I was born in Mexico, and Spanish was my first language. I’m still fluent. I didn’t start learning English until kindergarten, and I wasn’t immersed in an English classroom until third grade.

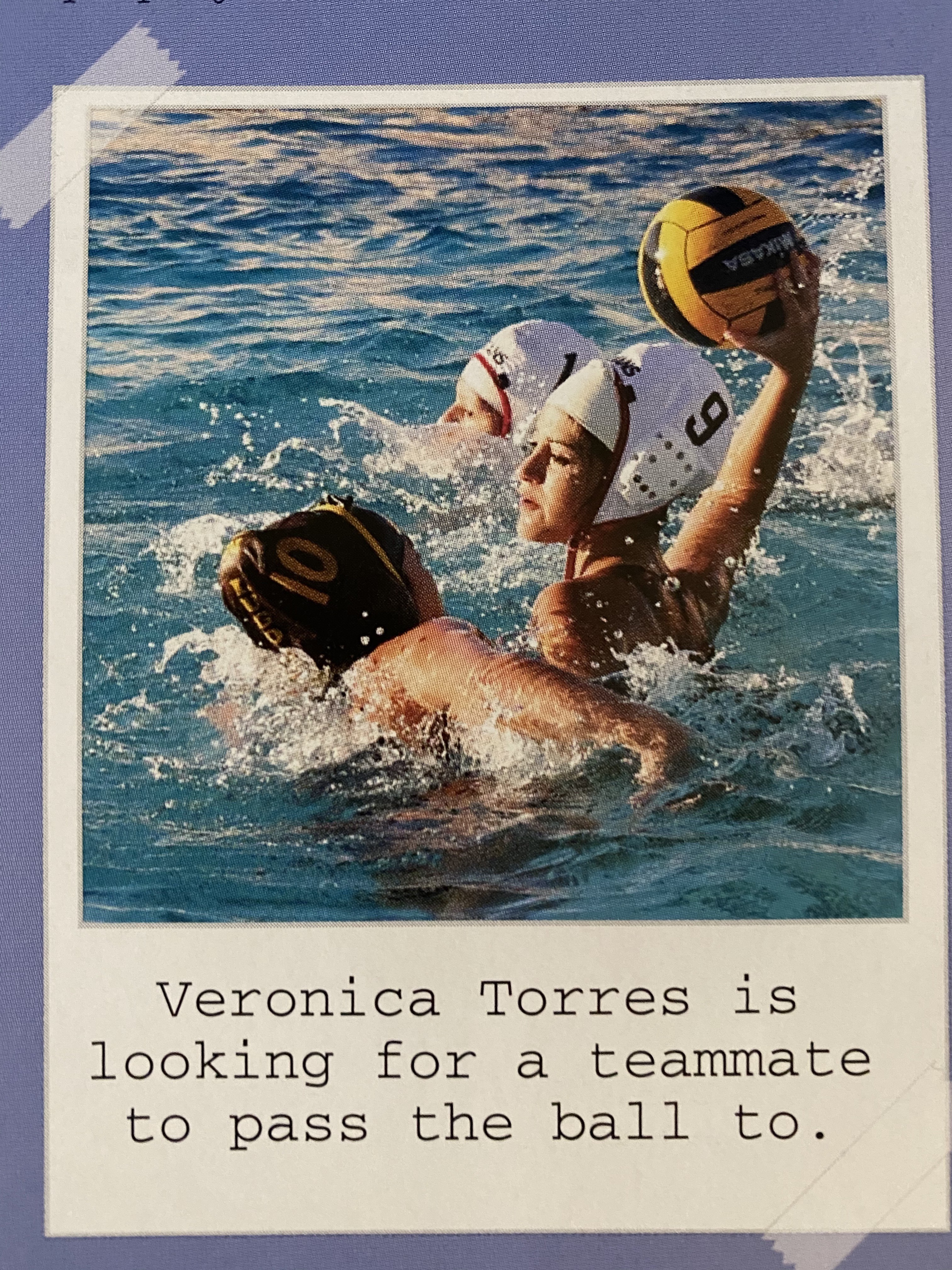

2. I played water polo in high school. (I started swimming first, which is normally done in reverse order!) I was one of the smallest girls on the team, but I tried to keep up.

3. My husband and I just spent six months on a new home build. We currently have no decor, so all suggestions are welcome!

If you would like an introduction to Warren Street, but only speak Spanish, Veronica can join calls to help translate and address any of your questions. Click here to schedule a complimentary consultation with her.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2020/01/Veronica-Torres-scaled.jpg25602048Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2022-08-29 08:30:002024-06-03 10:47:50Meet the Team: Veronica Cabral

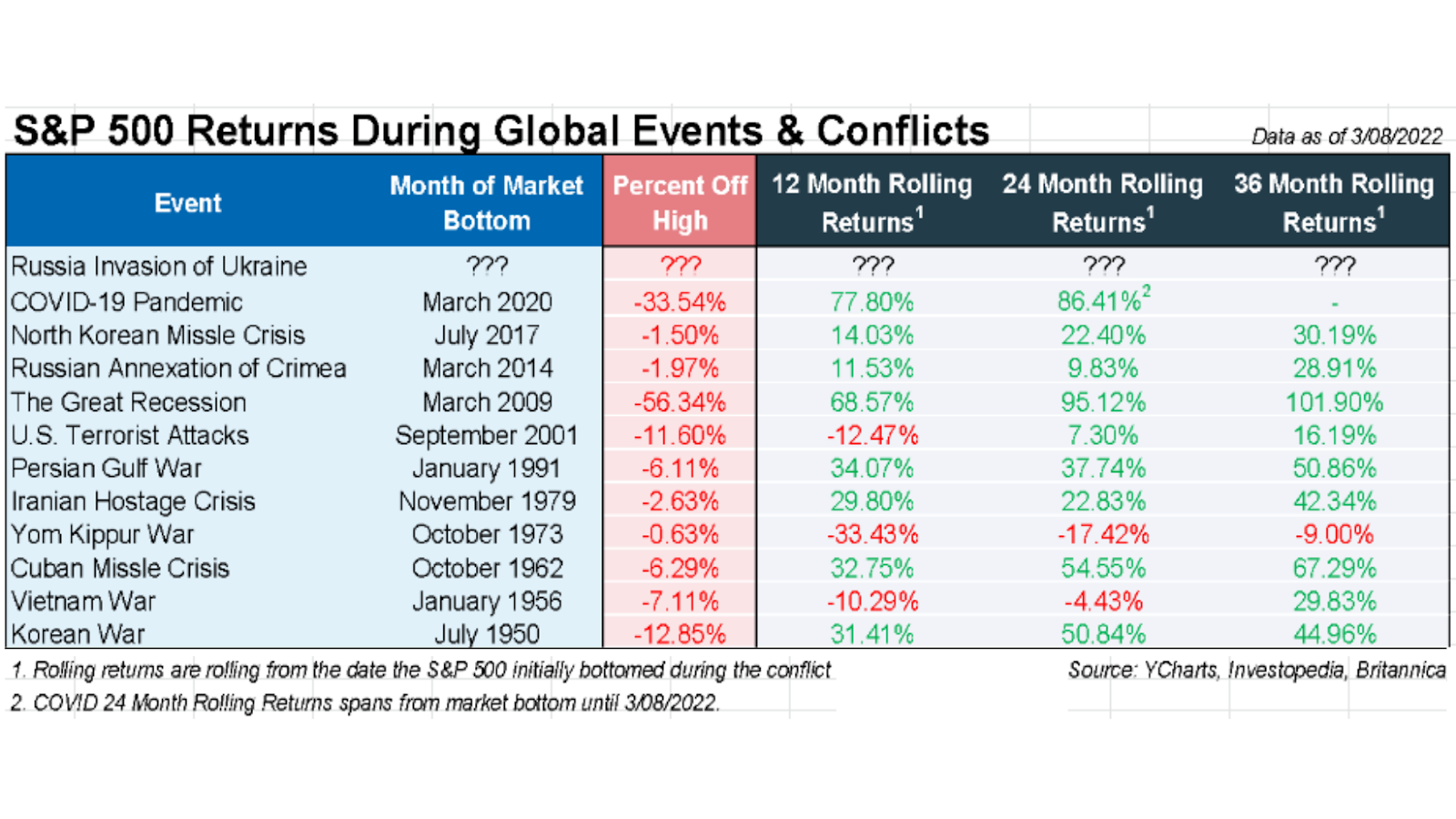

Market downturns are an expected part of investing, but they can be painful and nerve-racking nonetheless. Investors often want to take action or make changes during these times. Predicting which way the market will move in the short term is nearly impossible; short-term changes usually work against us. Below you will find some actions that you can take during a market pullback that will often yield positive results.

Here are some potential actions to take during a market downturn:

Continue to invest. Market downturns may provide an opportunity to buy into the market at a lower entry point. Consider increasing your savings and investing rate during this time.

Tax loss harvesting. Loss harvesting is a way to turn lemons into lemonade. Loss harvesting allows investors to take advantage of their portfolio losses by realizing the losses and using them to reduce taxable income.

Hold off on large withdrawals. Wait until the market recovers to make larger-than-usual portfolio withdrawals.

Overall financial planning check-up. Now is a good time to take care of any financial planning items that have been lingering on your to-do list. Check your beneficiaries, review your estate documents, and review your insurance coverage. The market is not in your control, so take a minute to review and manage anything that is in your control.

Check your 401(k) allocation and contributions. Make sure you are on track to receive any company matching contributions.

Roth conversions. Roth conversions are case-by-case specific, but generally speaking periods of market volatility may create opportunities for Roth conversions. The idea is to convert funds from a Regular to a Roth IRA while your account value is low, decreasing the amount of tax generated from the conversion. Assuming the market eventually recovers, your newly converted Roth dollars will appreciate tax free (assuming you meet all the other criteria necessary for Roth tax treatment). This scenario works best when you are in a low tax bracket and have the cash to pay tax on the conversion.

Rebalance your portfolio. Rebalancing your portfolio often forces you to sell high and buy low, even during periods of market downturn. By rebalancing during volatility, you are selling the funds that have held up better (typically bonds and other diversifiers), and reinvesting into the areas that have pulled back. This forces you to “buy the dip.” If/when the weaker parts of your portfolio recover, you participate more fully.

Reevaluate your risk level. Market corrections provide an opportunity to increase your risk level (i.e., your stock exposure) and to take advantage of lower stock prices. Typically these periods are not a good time to lower risk by selling stocks unless your goals and/or investment time horizon has changed.

Usually the best action is no action. If you’re not in a position to save more, sticking to your long-term allocation and plan is likely the best way to weather market turbulence. Market corrections will continue to happen over the course of your investing life. While overall the long term trend tends to be upward, corrections will typically happen every few years. During turbulent times, emotional decision-making often works against us.

The chart below illustrates how the S&P 500 has performed after a variety of global events and conflicts since 1950. You can see that in most cases, the market has had strong performance in the years following a crisis.

Please feel free to reach out to us if you have any questions. If you would like to speak with one of our advisors for complimentary portfolio review, you can schedule a consultation here.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/08/Action-Market-Blog-Thumbnail.png10801080Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2022-08-09 08:30:002024-11-07 09:29:15Actions to Take in a Market Downturn

Ever wonder where the “Warren” in “Warren Street” came from? It’s actually the middle name of Founding Partner Cary Facer (“Street” is the last name of Blake, our other founding partner).

Cary has long been a face of the firm, but there’s much more to him than his “Founding Partner and Wealth Advisor” title alone. Get to know Cary as we discuss everything from motivations to challenges in the interview below! And be sure to check out our other team member introductions.

Why did you decide to start Warren Street?

I started Warren Street Wealth Advisors out of frustration. After three years at a large financial firm, I realized how heavily these firms push their own products on clients, creating a major conflict of interest. I went independent so I could have the creative control needed to find financial solutions that truly helped my clients.

How does Warren Street align with your personal values?

Open, honest, transparent. Nothing to hide. I’ve always lived my life that way, and I strive to foster that environment every day at Warren Street. Clients should be able to share openly and honestly what’s on their hearts and minds, so we can all build a culture of trust in the work we do together.

What makes Warren Street unique?

Being independent not only allows us to do what we truly believe is in clients’ best interest, but it also allows creative flexibility. We do much more than investing and financial planning for our clients. We host March Market Madness, we send our clients a pound of See’s chocolates every holiday, and we just introduced Warren the Whale, our mascot! Whales are a symbol of transformation, reminding clients they have the power to transform their lives in extraordinary ways. Plus, he makes for a good stress ball to squeeze in difficult moments.

What do you love most about working at Warren Street?

I love seeing our team thrive. There’s not a better feeling than hearing that a team member’s success at work has impacted their personal life for the better.

What is your biggest accomplishment thus far?

I’d have to say starting Warren Street with Blake and finding success in a quick six years. It hasn’t all been roses, but it’s been real. Having a successful business partner is no different than having a successful marriage. It takes commitment, honesty, and a willingness to say difficult things. If you look at how successful our team is, it’s a sign as to the passion and trust we place in each other, and in them.

Who or what motivates you?

My two kids. I have two boys, ages 9 and 8, and all I try to do is be a good role model for them and their peers. I coach just about anything I can for two reasons: (1) to spend quality time with them and (2) to help and mentor other kids who are struggling in life or need a healthy outlet.

I also love motorsports and have gotten back into racing competitively. Everyone thinks they’re a good driver until they race. When I started… I was a terrible driver and made all kinds of mistakes. The weird part was, I enjoyed being terrible at it. It’s so humbling. At 40, I could easily stick to things I’m great at, but I enjoy grinding my way up through extremely difficult challenges. It’s one of the most difficult things I’ve ever done and I’m always motivated to be better.

What are three fun facts about you?

I started racing BMX when I was five years old.

Having been born into a vegetarian family, I didn’t eat meat for 39 years. I recently started eating meat and let me say, I’m busy making up for it.

I recently realized I can still run a five-minute mile (shoutout to my coaches at Hit the Mark Fitness)!

For more than 15 years, Cary has helped many retirees maximize their retirement. He has hosted over 130 retirement planning workshops to help more individuals secure a financial future for themselves.

If you’re interested in meeting Cary in person, register here for an in-person event (including dinner!) or schedule a complimentary consultation to discuss your financial goals. We look forward to hearing from you!

Veronica Torres

Director of Operations, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Series I bonds offer a low-risk, interest-earning addition to your portfolio. As part of a well-diversified portfolio strategy, now may be a good time to put some additional cash into I bonds and take advantage of an attractive interest rate.

What is a Series I bond?

A Series I bond is issued by the US Treasury. The bond accrues interest monthly until it reaches 30 years or you cash it, whichever comes first.

An I bond has two interest rates – the fixed rate and the inflation rate. These two rates combine to determine a bond owner’s actual rate of return, called the composite rate. A new rate will be set every six months based on the fixed rate and on inflation.

The US Treasury limits the composite rate to no less than 0%, meaning the rate of return on I bonds will never be negative.

What’s the benefit?

The composite rate on Series I bonds is currently 9.62% (annualized). Though the interest rate is variable and will change over time, purchasing I bonds now guarantees that you will earn this interest rate until October 2022 when the new rate is set for the next 6 months.

Are there risks?

An I bond is considered an extremely low risk investment. However, the ultimate rate of return is variable and not guaranteed beyond the current 6-month rate. The current interest rate is high because inflation is higher than usual – if Federal Reserve policy reduces inflation the inflation rate for I bonds will also decrease.

Note that an I bond cannot be redeemed for at least one year after purchase, and any redemption between years 1 and 3 does not receive the interest from the three months prior to redemption.

How do I buy a Series I bond?

Visit treasurydirect.gov to purchase electronic I bonds. An I bond must be purchased directly by the investor; it is not something your advisor can add to your portfolio for you. Series I bonds purchased electronically come in any amount to the penny for $25 or more. Paper I bonds can be purchased using your federal income tax refund. The amount of a bond purchased is limited to $10,000 per person per year.

Are I bonds right for me?

Determining what investments are the best fit for you depends on several factors: your age, the timeline for when you need to withdraw from investments, your comfort with risk, and your overall financial health. If you have some cash that is not part of your basic emergency fund and you do not need it in the next 1-3 years, I bonds may be a good choice. However, as with all investing decisions, we recommend consulting with your financial advisor to determine if I bonds are the best fit for your unique situation.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/06/Series-I-Bond-Blog-Thumbnail.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-06-16 08:00:002024-11-07 09:30:00Series I Bonds: Are They Right For You?

Young adults, or anyone new to managing their own finances, often feel stuck when they think about money. In an age of unlimited access to information, advice, and opinions, deciding what to prioritize can feel paralyzing. At some point, all of us have asked the question “Where do I start?”

To help answer that question, we have identified three priorities for young adults to build a solid financial foundation. Individual circumstances will almost certainly require adaptation, so these three points are intentionally general and flexible so that you can apply them to your situation.

1. Identify Your Goals

Good financial planning requires goals or targets. There is no singular definition of financial success; your needs, wants, and wishes determine what a successful path looks like.

Like all goals, financial goals should be realistic, flexible, and measurable. Goals may include paying off debt, retiring by a specific age, starting a business, buying a home, supporting loved ones, or any other specific expenses that are important to you.

Attach a dollar amount to your goals. If you are not sure how much you might need for a certain goal, there are often simple online tools that can help, such as retirement calculators (like these from SmartAsset and NerdWallet) or home affordability calculators (like these from NerdWallet andZillow).

You may not know all the specifics of a certain goal. For example, when retirement is 20 or 30 years down the road, you might not be able to identify exactly how much income you will need from your investments. Don’t let uncertainty deter you from setting the goal! You can start with an estimate and continue to refine it as your plans take shape.

2. Basic Financial Housekeeping: Cash Flow and Emergency Fund

Cash flow refers to money coming in and money going out. At a minimum, you should know what your income is each month and generally what expenses you have. Don’t worry about making changes at first; just write the information down so you know where you are starting. Then you can start tracking your spending and getting an idea of areas where you may need to make changes.

A basic emergency fund should cover three to six months of expenses. This money should be kept easily accessible in cash — a regular bank savings account, a high-yield savings account, or an online savings account are all great options. When you use some of this money for an unforeseen necessary expense (such as a car repair, covering your bills during a time of unemployment, or a hospital bill), work to replenish your fund once you are able.

3. Establish a Habit of Consistent Investing

Once you have taken care of your basic financial housekeeping, it is time to look to the future. Even if your goals are still just far-off estimates, establishing good habits now will pay off when it is time to get more specific.

Below are a few examples of investment accounts that might fit your situation:

401(k) or 403(b) plan: If your employer and/or your spouse’s employer offers a 401(k) or 403(b) plan, you can contribute pre-tax dollars and possibly receive contributions from your employer. It’s as close as you can get to free money!

IRA or Roth IRA: An IRA is a retirement savings account that is independent of your employer. You can contribute up to a set annual maximum and potentially receive tax benefits. Tax deductions and the ability to contribute to a Roth IRA have some conditions, so check the current IRS rules.

Individual or Joint brokerage account: A brokerage account is an investment account that is not specifically for retirement. There are no tax deductions for contributions you make, but there are also no rules about when you can access money in the account. This is a good option for general investing that may be used for anything. There are also no contribution limits for brokerage accounts, so if you are already contributing the maximum to a 401(k) or IRA, a brokerage account can allow for additional long-term savings.

Keep It Simple

There is an endless supply of financial advice floating around, and knowing what advice to follow can be overwhelming. When in doubt, keep it simple! Focusing on these three starting points will allow you to tune out all the noise and set you up for financial success.

Do you feel like you are ready for steps 4, 5, and 6 in your financial plan? Maybe it’s time to work with a pro. Contact us at Warren Street Wealth Advisors to learn more about how we can help you achieve your financial goals.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/05/YoungAdults.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-05-12 09:00:002024-11-07 09:30:29Three Financial Priorities for Young Adults

Having a comfortable retirement doesn’t necessarily mean leaving The Golden State behind.

In our California-based advising firm we often see clients who would like to move out of the state at retirement (or sooner). There are plenty of reasons to re-settle, and if your only reason is “I want to” then that is good enough for us. But the retirement of your dreams doesn’t necessarily mean you need to pack up and move. Call us biased…but we love The Golden State!

The State Tax Problem

A major concern for Californians is taxes. Our top state tax bracket is the highest in the nation. However, a retiree’s taxable income is not often in the highest bracket. The tax rates for most middle (and even upper-middle) class taxpayers are comparable to, and sometimes lower than, those in several other states.

To illustrate: in 2021 a single California taxpayer’s taxable income between $61,215 and $375,221 will be taxed at 9.3%. Compare that to a nice midwestern state like Minnesota. Their very top tax bracket is 9.85%, but it starts at taxable income over $166,041. So if your taxable income is between $166,041 and $375,221, you will pay similar state taxes whether you are in California or Minnesota.

Let’s look at a more realistic retirement income. Taxable income in retirement for an average married couple might be around $85,000. In California, their effective state tax rate for 2021 would be about 2.40%. If the couple decided to move to Arizona (a low tax state) in retirement, their effective state tax rate would be about 1.87%. That’s a difference of just $450 per year. Uprooting and moving states to save $450 in a year may not really be worth it!

It is true that state taxes are much lower in many other states. There are even states with no state income tax. But these states offset their lack of income tax with sales tax, property taxes, and other local taxes. The bottom line is: no state is going to let you put down roots for free. While California certainly is not the most taxpayer friendly state, for a large portion of residents the higher tax brackets are not going to be a factor.

Quality of Life in California

Two major considerations for quality of life are staying physically active and staying socially engaged. We know that a sedentary, perpetually isolated lifestyle is bad for your health. The mild-to-warm weather in California means your favorite activities can usually continue year-round, keeping you moving and socializing consistently throughout your life.

California has something for everyone. Do you prefer vibrant evenings out in the city or quiet mountain escapes? Yoga on the beach? Pickleball in the suburbs? Hiking in the desert? It’s all here.

Why Warren Street Loves CA

Why else does our team love California? When asked “What are some reasons a person might want to retire in California?” here is what we had to say:

“Many job prospects for those who want to have a part-time retirement living.”

“On the tax note, Prop 13 and Prop 19 can keep CA property taxes low.”

“Good access to medical care and good doctors in most of CA.”

“Diverse population and diverse cultures in CA.”

“California is a great hub for entertainment and tourism.”

“Home to multiple beaches, national parks, etc.”

“CA is the largest municipal bond market by issuance.”

“In-N-Out.”

Every state has something great to offer. Above all, we love to see our clients happy and living their best life – before and after retirement.

Do you want to continue your California dream after you retire? Or do you want to try somewhere new? Whatever your goals, Warren Street is here to help you make them reality.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/04/Blog-Thumbnail.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-04-21 08:00:002024-11-07 09:30:51Perks of a California Retirement