Get ready to have some fun in the sun! Whether you’re heading to a tropical paradise or exploring a new city, proper budgeting can make your summer trip stress-free and enjoyable. Here are some key categories to remember when planning your budget:

1. Travel

Whether you’re taking a bus, train, car, airplane, or a combination of all these, set aside a portion of your budget for travel expenses. This includes not only the main mode of transportation but also any additional costs like gas, tolls, or rideshares.

2. Accommodations

Don’t forget to budget for where you’ll be staying. Whether it’s a hotel room, vacation rental, or even a cozy cabin, make sure you allocate enough funds for your accommodations. Comfort is key to a relaxing vacation!

3. Dining

Dining out can get expensive quickly, especially if you plan to eat out for most of your meals. Be realistic and allocate a generous portion of your budget to dining. Trying new restaurants and local cuisines is one of the best parts of traveling!

4. Experiences

Life is meant for living, so don’t forget to budget for experiences. Whether you’re renting bicycles for a day of exploration or going on an exciting excursion, make sure you set aside some funds for fun activities, because life is meant for living.

By keeping these categories in mind and planning accordingly, you’ll be all set for a fantastic summer adventure. Need help planning your summer travel budget or have other financial planning needs? Reach out to us today, and let’s make your dream vacation a reality! Happy travels!

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/06/Summer-Budget-Tips-Blog.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-06-06 07:30:002024-11-07 09:18:03Planning Your Perfect Summer Trip: Budgeting Made Easy

Since our last “Meet the Team” series, we’ve welcomed two new members, Bryan Cassick and Jennifer “JB” Battles, to our Warren Street family. However, today we want to shine a spotlight on an existing team member who has recently been promoted. We had the pleasure of sitting down with Jennifer, who is now our Director of Sales & Marketing. Get to know more about Jennifer’s role, hobbies, and future goals.

In your role as Director of Sales & Marketing, how do you assist Warren Street’s clients?

I focus on client communication and strive to enhance the user experience, from your initial contact with us through your entire journey as a client. My responsibilities include managing email campaign communications, such as the quarterly newsletter you receive. Additionally, I plan and host events, including our annual client appreciation event, which is our way of thanking you for your support and loyalty.

How does Warren Street align with your personal values?

At Warren Street, we place a strong emphasis on passion. I strive to live my daily life engaged in activities that truly matter to me. I do not want to live a life that feels idle or mundane. My work is driven by genuine enthusiasm and purpose—I am here because I want to be, not because I have to be. This passion fuels my commitment to making a meaningful impact both in my role and in the lives of our clients.

What do you love most about working at Warren Street?

One of the things I appreciate most about Warren Street is the incredible flexibility, as our entire team operates remotely. Despite being spread out across the country, I feel very close to my team members, to the point where I consider them my family. We stay connected through regular activities, such as our monthly lunch club. Additionally, when we meet our annual sales goals, we celebrate with a special trip called “Path To,” where we enjoy our success together.

What is your biggest accomplishment thus far?

My biggest accomplishment is stepping into the role of Director of Sales & Marketing. It comes with many responsibilities, but I am ready to grow in this position and serve you proudly.

Who or what motivates you?

My parents are my biggest motivation. They immigrated from Vietnam without knowing any English and with zero dollars in their pockets. Despite facing immense struggles and making countless sacrifices, they worked tirelessly to create a better future and provide a better life for my sister and me. Their dedication drives me to give back even a fraction of what they’ve given me.

What are your aspirations?

I absolutely love traveling, and my dream is to visit at least 100 countries in my lifetime. I’ve already explored various countries in Southeast Asia and recently visited Iceland in March 2024. Among all the places I’ve been to thus far, Japan has been my favorite. I highly recommend everyone to experience its unique culture and beauty firsthand someday!

What are three fun facts about you?

I own over 100 plushies of Winnie the Pooh, my favorite character of all time.

I have visited 31 of the 50 states.

I have an Etsy shop with my cousin, where we sell hand-made amigurumi plushies. Follow us on Instagram @QTWorks!

Get to know our other team members, including Aileen Obedoza and Emily Balmages. Let’s congratulate Jennifer on her new role as Director of Sales & Marketing.

Veronica Cabral

Director of Operations & Chief Compliance Officer, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/11/JenniferLa2022Headshot.jpg30002400Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2024-05-23 14:56:312024-05-28 07:34:44Meet the Team: Jennifer La

So much of investing is beyond our control (picking stock prices, timing market movements, and so on) that it’s nice to know there are several “power tools” that can potentially enhance overall returns. Tax-loss harvesting is one such instrument, but — like many tools — it’s best used skillfully, and only when it is the right tool for the task.

The (Ideal) Logistics

When properly applied, tax-loss harvesting is the equivalent of turning your financial lemons into lemonade by converting market downturns into tangible tax savings. A successful tax-loss harvest lowers your tax bill, without substantially altering or impacting your long-term investment outcomes.

Tax Savings

If you sell all or part of a position in your taxable account when it is worth less than you paid for it, this generates a realized capital loss. You can use that loss to offset capital gains and other income in the year you realize it, or you can carry it forward into future years. We can realize losses on a holding’s original shares, its reinvested dividends, or both. (There are quite a few more caveats on how to report losses, gains, and other income. A tax professional should be consulted, but that’s the general premise.)

Your Greater Goals

When harvesting a loss, it’s imperative that we remain true to your existing investment plan. To prevent a tax-loss harvest from knocking your carefully structured portfolio out of balance, we reinvest the proceeds of any tax-loss harvest sale into a similar position (but not one that is “substantially identical,” as defined by the IRS). Typically, we then return the proceeds to your original position no sooner than 31 days later (after the IRS’s “wash sale rule” period has passed).

The Tax-Loss Harvest Round Trip

In short, once the dust has settled, our goal is to have generated a substantive capital loss to report on your tax returns, without dramatically altering your market positions during or after the event. Here’s a three-step summary of the round trip typically involved:

Sell all or part of a position in your portfolio when it is worth less than you paid for it.

Reinvest the proceeds in a similar (not “substantially identical”) position.

Return the proceeds to the original position no sooner than 31 days later.

Practical Caveats

An effective tax-loss harvest can contribute to your net worth by lowering your tax bills. That’s why we keep a year-round eye on potential harvesting opportunities, so we are ready to spring into action whenever market conditions and your best interests warrant it.

That said, there are several reasons that not every loss can or should be harvested. Here are a few of the most common caveats to bear in mind.

Trading costs – You shouldn’t execute a tax-loss harvest unless it is expected to generate more than enough tax savings to offset the trading costs involved. As described above, a typical tax-loss harvest calls for four trades: There’s one trade to sell the original holding and another to stay invested in the market during the waiting period dictated by the IRS’s wash sale rule. After that, there are two more trades to sell the interim holding and buy back the original position.

Market volatility – When the time comes to sell the interim holding and repurchase your original position, you ideally want to sell it for no more than it cost, lest it generate a short-term taxable gain that can negate the benefits of the harvest. We may avoid initiating a tax-loss harvest in highly volatile markets, especially if your overall investment plans might be harmed if we are unable to cost-effectively repurchase your original position when advisable.

Tax planning – While a successful tax-loss harvest shouldn’t have any impact on your long-term investment strategy, it can lower the basis of your holdings once it’s completed, which can generate higher capital gains taxes for you later on. As such, we want to carefully manage any tax-loss harvesting opportunities in concert with your larger tax-planning needs.

Asset location – Holdings in your tax-sheltered accounts (such as your IRA) don’t generate taxable gains or realized losses when sold, so we can only harvest losses from assets held in your taxable accounts.

Adding Value with Tax-Loss Harvesting

It’s never fun to endure market downturns, but they are an inherent part of nearly every investor’s journey toward accumulating new wealth. When they occur, we can sometimes soften the sting by leveraging losses to your advantage. Determining when and how to seize a tax-loss harvesting opportunity, while avoiding the obstacles involved, is one more way we seek to add value to your end returns and to your advisory relationship with us. Let us know if we can ever answer any questions about this or other tax-planning strategies you may have in mind.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

At the core of financial literacy lies a set of values and behaviors that extend beyond mere dollars and cents. As parents, caregivers, and educators, we have the unique opportunity to shape the financial mindsets of the next generation by imparting timeless wisdom that transcends monetary transactions.

As we celebrate Financial Literacy Month this April, let’s commit to empowering our children with the knowledge, skills, and values they need to thrive in an increasingly interconnected world. Teach your children these four fundamental lessons that build financial savviness over time.

Believe in Yourself: Confidence is the cornerstone of success in any endeavor. Encourage children to believe in their abilities and to recognize the value they bring to the table. By fostering a sense of self-assurance, we empower our youth to navigate the complexities of the financial landscape with poise and resilience.

Listen to Others: Effective communication is a two-way street that involves not only speaking but also actively listening. Teach children the importance of lending an ear to others, as every voice has the potential to impart valuable insights. By honing their listening skills, children cultivate a sense of empathy and discernment that serves them well in both personal and professional spheres.

Put in the Hard Work: Success seldom comes without effort. Encourage children to embrace the virtue of hard work by involving them in household chores, encouraging academic diligence, or exploring part-time employment opportunities. By instilling a strong work ethic, we equip children with the tools they need to pursue their goals with diligence and determination.

Budget, Save, & Invest: Introduce children to the concepts of budgeting, saving, and investing in a manner that is accessible and relatable. Emphasize the connection between hard work and financial resources, illustrating how responsible financial management enables individuals to achieve their aspirations. Encourage children to set aside a portion of their earnings for savings and explore the possibilities of investment, laying the groundwork for a secure financial future.

By integrating these principles into everyday interactions and activities, you can nurture a generation of financially literate individuals who are equipped to navigate the complexities of an ever-evolving economic landscape. Together, we can pave the way for a brighter, more prosperous future for generations to come.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/03/How-to-Cultivate-Financial-Literacy-in-Children-and-Create-a-Pathway-to-Lifelong-Success.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-04-04 07:03:002024-03-22 11:09:40How to Cultivate Financial Literacy in Children and Create a Pathway to Lifelong Success

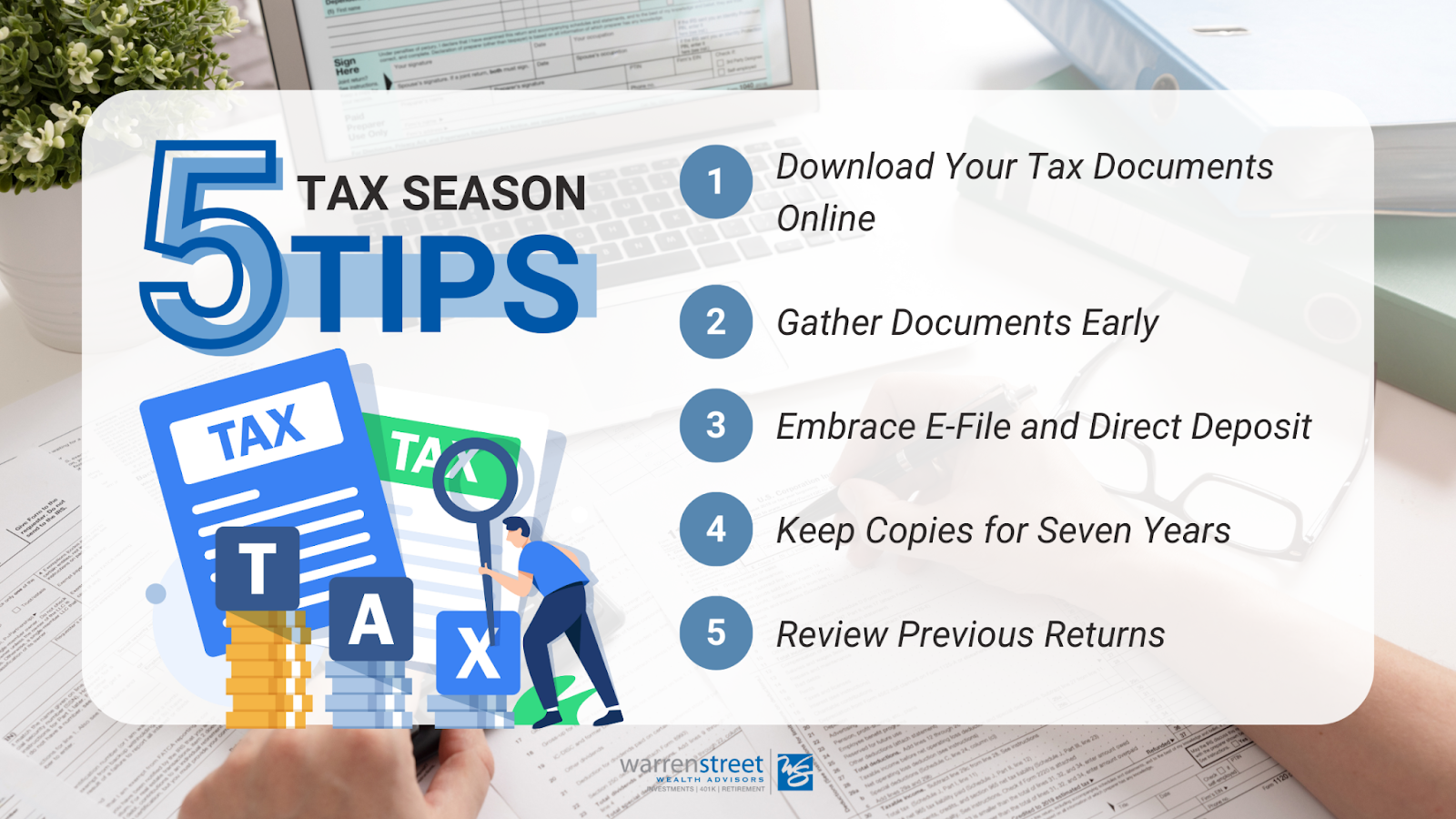

Tax season is upon us, and while it may not be everyone’s favorite time of the year, being well-prepared can make the process much smoother. To help you navigate the complexities of tax filing, here are our top 5 tax season tips:

1. Download Your Tax Documents Online

In the digital age, many financial institutions issue tax documents exclusively online, skipping the traditional postal route. As you gear up for tax season, ensure that you’ve received a tax form from every expected institution. Log in to your online accounts and download the necessary documents. Stay proactive and make sure nothing slips through the cracks.

2. Gather Documents Early

Most tax documents are available by mid-February, so start gathering them early. This proactive approach gives you ample time to review the information, identify any discrepancies, and seek clarification from the issuing institution if necessary. Being ahead of the game can significantly reduce stress as the filing deadline approaches.

3. Embrace E-File and Direct Deposit

E-filing and direct deposit have become the preferred methods for both filing returns and receiving or paying tax refunds. The IRS can be sluggish when it comes to processing paper mail, leading to delays in refunds or acknowledgments. Save time and expedite the process by opting for electronic filing and direct deposit for a more efficient and secure experience.

4. Keep Copies for Seven Years

Once your tax return is filed, keep copies of your tax returns and all supporting documents for a minimum of seven years. This ensures that you have a comprehensive record of your financial history in case of audits, inquiries, or future financial planning.

5. Review Previous Returns

Look out for specific items such as Capital Loss Carryforwards and Form 8606 (IRA Basis). If you’ve changed tax preparers or tax software in recent years, there’s a chance that crucial information may have been overlooked. Rectify any discrepancies and ensure that your current return reflects the most accurate and up-to-date financial information

By incorporating these top 5 tax season tips into your filing routine, you’ll not only streamline the process, but also gain confidence in the accuracy of your returns. So, gear up, gather those documents, and tackle tax season with ease!

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/02/Mastering-Tax-Season-Top-5-Tips-for-a-Smooth-Filing-Process.png10801080Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2024-03-04 08:11:002024-02-29 08:35:49Mastering Tax Season: Top 5 Tips for a Smooth Filing Process

Quality Time. Acts of Service. Words of Affirmation. Physical touch. You may know your primary love language, an unofficial classification of the different ways people express and receive love. But have you heard of Money Scripts®?

Money scripts®, a term first coined by financial psychologist Brad Klotz, are the often-unconscious ideas and attitudes we have about money. They are:

Learned in childhood

Passed down through generations

Only partial truths

Responsible for many financial outcomes

For many people, discovering and exploring their money script® is a valuable step toward improving their financial well-being. Plus, the more you understand your own attitude toward money, the better you are able to explore how your beliefs and assumptions impact your relationships with others. No one money script® is good or bad; the important thing is to understand your primary script and manage it in a healthy way.

Read on to discover your primary money script® and explore some ideas for how you can work with it to develop a healthy approach to managing your finances.

#1: Money Avoidance

People with this money script may view money as inherently evil or negative, and they may go to great lengths to avoid discussions about finances. You might be a money avoider if you’ve thought things like:

Rich people are greedy.

I feel guilty about having money.

People with less money usually have better character than wealthy people.

Money stresses me out, and I’d rather just not think about it.

Unhealthy Money Avoidance:

When not addressed, people with this money script may ignore financial statements, overspend, or enable others financially.

Healthy Money Avoidance:

Work to pay attention to money at least at a high-level; you don’t have to monitor every penny, but general budgeting and having a financial plan can go a long way in helping you reach your future goals.

–

#2: Money Focus/Worship

Is money on your mind 24/7? Does money seem like the ultimate key to happiness? If so, you may be “worshiping” money without even realizing it. This might be your money script if you’ve had thoughts like:

I could never have enough money.

If I buy this, I will be happy (i.e, “retail therapy”).

My problems would all go away if I just made a little more money.

My family will understand if I put in extra hours so I can bring home more money.

Unhealthy Money Focus:

The higher people score on Money Focus, the more likely they are to have low net worth or credit card debt. If you find yourself constantly spending in search of happiness, it might be time to make some changes.

Healthy Money Focus:

Our society puts money on a pedestal. Still, it’s important to recognize that money does not equal happiness. Work on flexing your gratitude muscle, perhaps by keeping a gratitude journal. Make time for activities and people you love. And when you feel the impulse to make a purchase, ask yourself, do I really need this item, or am I just buying it for the sake of buying something?

–

#3: Money Status

This money script is similar to #2, but instead of equating money to happiness, a Money Status mentality links money and self-worth. People with this money script view themselves as more “worthy” when they have a lot of money. They may be at risk of overspending and buying flashy, expensive items to prove their status.

You might have a “Money Status” money script if you’ve thought things like:

This shirt/Apple Watch/car/purse is worth the splurge, because it’s “on brand” for me.

I like gambling – it helps me make more money to support my lifestyle.

It’s acceptable to hide purchases from my partner; they wouldn’t understand why I need these things.

Unhealthy Money Status:

In an unhealthy state, people with this money script are at risk for excessive spending, gambling, and financial dependency on others. They may have been raised in a socioeconomic class that prioritized appearances, and might carry that unconscious mindset into their adult lives.

Healthy Money Status:

The key is balance. If you want to treat yourself sometimes, that’s acceptable, but not at the expense of hiding things from your partner or spending money you don’t have. Work on addressing the reasons behind your need to spend, and talk about your spending strategies with your partner.

–

#4: Money Vigilance

On paper, these are the “gold star” money script students. Still, too much of an extreme is never healthy, and it’s possible to be too vigilant. You might have a “Money Vigilance” money script if you’ve thought things like:

If you can’t buy it in cash, don’t buy it.

Hard work equals financial reward.

You can never save enough for a rainy day.

I’d rather save for a rainy day and my future than spend money on experiences now.

Unhealthy Money Vigilance:

When people are too focused and anxious about their finances, it can keep them from enjoying their present lives. While this money script can emphasize frugality and saving, it can also lead to excessive stress and anxiety that could have been alleviated by financial planning and management.

Healthy Money Vigilance:

Set aside a piece of your budget that is for using now on fun purchases. It’s great to save for the future, but spending on some things you can enjoy now will go a long way in helping you feel a sense of enjoyment and gratitude. Work with a trusted advisor or partner to set a specific time to think about and discuss finances, and focus on living in the moment.

–

By now, you probably have a sense for your own money script. Discuss it with your partner, and talk about what’s similar or different to the way you view money. You might be making assumptions about the other person’s viewpoint without even realizing it, and understanding each other can go a long way in helping you make decisions about money together in the future. Plus, it can be a fun bonding experience over a date night if you approach it with a lighthearted attitude! Let us know your results.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/10/Money-Script-Blog.png10801080Warren Street Teamhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgWarren Street Team2024-02-13 08:01:002024-11-07 09:19:30You May Know Your Love Language, but What’s Your Money Script?

As a business owner, you’ve spent your life’s work growing your business, taking care of employees, managing your product or service, and looking after your people. Now, you may be getting to a point where your spouse tells you you work too much. Or perhaps you’re watching the clock more than you used to, counting down the minutes until you can head home and unplug from your “boss” responsibilities.

Whatever your reasoning, if you’re starting to ask questions like, “Do I have enough to sell?” and “Will that be enough?” then it’s time to focus on you for a change.

Why Business Owners Need Specialized Financial Planning

Business owners face a unique set of financial challenges and opportunities. Whether you are a small business owner or running a large corporation, the following considerations are critical:

Maximizing tax efficiency

Choosing the most appropriate retirement account type

Evaluating your retirement account options

Managing 401(k) and pension investments

Considering a defined benefit plan, i.e., “pension”

Aligning company benefits offerings with company goals

Our team specializes in helping business owners handle these and other issues while they’re still working. During those years, we help you work through proper planning techniques to diversify your assets, reduce risk, optimize your taxes, and offer competitive benefits. All of these steps help streamline and strengthen your business at the time — but they also set you up for a successful transition into retirement or your next business opportunity.

When you do get to the point of exiting, we help you bring all of this planning together into one critical decision: whether or not you have what you need to move on from your business and into your ideal retirement, whatever that looks like for you.

Creating a Dream Retirement

At Warren Street, we’ve helped many business owner clients over the years answer the “Do I have enough to sell?” question and develop their exit strategies accordingly.

If you choose to work with us during your own exit process, we’ll play a key role on your professional team alongside your attorney. While your attorney looks after the legal structure of the deal, we’ll handle related asset management and tax mitigation. For example, if you’re involved in an all-cash sale with multiple payments coming in the next few years, we will discuss tax deferral opportunities to add into your transition plan. Or, if you’re struggling with a go/no-go decision, we’ll conduct scenario planning to help you make an informed choice based on your current financial situation, projected future state, and personal goals.

No matter where you are in the exit planning process, we can help evaluate your current assets, investments, estate planning, and legacy goals, so you can make a clear and confident decision on what next steps are right for you.

If this sounds like you and you’re a current Warren Street client, please mention your interest to your Lead Advisor! Or, if you’re not a client but are interested in learning how we can help, schedule a complimentary introductory call with us. We hope to hear from you and look forward to exploring how we can make your post-exit dreams a reality.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/12/Do-I-Have-Enough-To-Sell.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-12-28 08:24:002024-06-03 10:46:08Do I Have Enough to Sell My Business?

Scan the financial headlines these days, and you’ll see plenty of potential action items vying for your year-end attention. Some may be particular to 2023. Others are timeless traditions. Here are our three favorite items worth tending to as 2024 approaches… plus a thoughtful reflection on how to make the most of the remaining year.

1. Bolster Your Cash Reserves

With some high yield savings options currently offering ~5%+ annual interest rates, your fallow cash is finally able to earn a nice little bit while it sits. Sweet! Two thoughts here:

Mind Where You’ve Stashed Your Cash: If your cash savings is still sitting in low- or no-interest accounts, consider taking advantage of the attractive rates available in other options. If you’re unsure where to start, we can help you figure out whether a high yield savings account, a CD, or treasury bonds may make sense for you. Your cash savings typically includes money you intend to spend within the next year or two, as well as your emergency, “rainy day” reserves.

Put Your Cash in Context: While current rates across many accounts are appealing, don’t let this distract you from your greater investment goals. Even at today’s higher rates, your cash reserves are eventually expected to lose their spending power in the face of inflation. Today’s rates don’t eliminate this issue … remember, inflation is also on the high side, so that 5% isn’t as amazing as it may seem. Once you have your cash stashed in those high-interest savings accounts, you’re likely better off allocating your remaining assets into your investment portfolio—and leaving the dollars there for pursuing your long game.

2. Polish Your Portfolio

While we don’t advocate using your investment reserves to chase money market rates, there are still plenty of other actions you can take to maintain a tidy portfolio mix. For this, it’s prudent to perform an annual review of how your investments are growing. Year-end is as good a milestone as any for this activity. For example, you can:

Rebalance: In 2023, year-to-date stock returns may warrant rebalancing back to plan, especially if you can do so within your tax-sheltered accounts. If you are an existing Warren Street client, this is already being handled on your behalf.

Relocate: With your annual earnings coming into focus, you may wish to shift some of your investments from taxable to tax-sheltered accounts, such as traditional or Roth IRAs, HSAs, and 529 College Savings Plans. For many of these, you have until next April 15, 2024 to make your 2023 contributions. But you don’t have to wait if the assets are available today, and it otherwise makes tax-wise sense.

Redirect: Year-end can also be a great time to redirect excess wealth toward personal or charitable giving. Whether directly or through a Donor Advised Fund, you can donate highly appreciated investments out of your taxable accounts and into worthy causes. You stand to reduce current and future taxes, and your recipients get to put the assets to work right away.

3. Minimize Your Taxes

Speaking of taxes, there are always plenty of ways to manage your current and lifetime tax burdens—especially as your financial numbers and various tax-related deadlines come into focus toward year-end. For example:

RMDs and QCDs: Retirees and IRA inheritors should continue making any obligatory Required Minimum Distributions (RMDs) out of their IRAs and similar tax-sheltered accounts. With the 2022 Secure Act 2.0, the penalty for missing an RMD will no longer exceed 25% of any underpayment, rather than the former 50%. But even 25% is a painful penalty if you miss the December 31 deadline. If you’re charitably inclined, you may prefer to make a year-end Qualified Charitable Distribution (QCD), to offset or potentially eliminate your RMD burden.

Harvesting Losses … and Gains: Depending on market conditions and your own portfolio, there may still be opportunities to perform some tax-loss harvesting in 2023, to offset current or future taxable gains from your account. As long as long-term capital gains rates remain in the relatively low range of 0%–20%, tax-gain harvesting might be of interest as well. Work with your tax-planning team to determine what makes sense for you. If you are an existing Warren Street client, we will automatically tax loss harvest for you.

How else can we help you tend to your 2023 plans and till the soil for 2024? Please be in touch for additional ideas and best-practice advice.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/11/Finacial-Practices-2023.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-11-28 08:15:162024-11-07 09:20:043 Financial Best Practices for Year-End 2023

Open enrollment season is upon us, with most plans allowing individuals and families to make changes to their 2024 benefit enrollments this fall. Now is the best time to make sure you are optimizing your benefits.

Consider Your Health Insurance Options – When was the last time you reviewed your health insurance options? A lot can happen in a year, and each life change may mean your current health care plan may no longer be the best option. Whether you are on employer coverage, exchange coverage, or Medicare, we can help you review your options.

Pro tip: If your medical plan allows it, consider utilizing a health care tax-advantaged account like an Health Savings Account (HSA) or Flexible Spending Account (FSA).

Explore All Available Benefits – Many employer and retiree plans offer additional benefits beyond traditional health care options. Exploring these alternative benefits to see if any are applicable to your situation can save you time and money. Don’t forget about vision, dental, life, disability, excess liability and any other unique insurance being offered to you. This will ensure you are taking full advantage of the benefits available to you.

Pro tip: Employer-sponsored life and disability insurance can be cost effective and easy to obtain compared to buying your own private policies.

If you are looking for guidance, Warren Street is available to assist in interpreting your health care and benefits package information as part of the 2024 open enrollment season. Let us know how we can help!

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/09/Open-Enrollment-2023.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2023-09-21 08:12:002024-11-07 09:22:10It’s Open Enrollment Season: Here’s How to Optimize Your Benefits

Probate is the court process used to determine who gets an inheritance. In the eyes of a financial planner, it is a court process that most clients should try to avoid for many reasons. The probate process is time-consuming, usually lasting about a year depending on how backed up the courts are. The expense for probate is very high, which includes thousands of dollars going towards attorney and court fees. Probate is also a public court event in which potential heirs can object to the ruling pretty easily, causing privacy concerns and more attorney costs. While probate can have its time and place, there are some simple ways to avoid probate.

Let’s take a look at three easy steps you can take now to keep your loved ones from having to deal with probate.

Primary Beneficiary Designations – If a 401(k) account or life insurance policy lists a primary beneficiary, the account avoids probate and passes directly to the listed beneficiary. For brokerage accounts this is usually referred to as a Transfer-On-Death (TOD) account, and for bank accounts this is referred to as a Payable-On-Death account.

Contingent Beneficiary Designations – Setting a contingent beneficiary is also an easy way to help avoid probate. The contingent beneficiary is the person(s) next in line to inherit if the primary beneficiary has already passed away at the time of the account holder’s passing.

Retitle Your Automobile & House – Don’t forget about your car and home! If your vehicle or house are listed in your name alone, they would turn into probate assets at the time of your passing. Some states have introduced TOD car and house titling as a way to avoid needing probate if the owner passes away. Also, you and your spouse should consider owning the car and house jointly with rights of survivorship, as another way to avoid probate.

These planning points provided today are just some of the easy actions you can do yourself. There are more ways to avoid probate, but they get a little more complex and depend on your personal situation.

With legal matters like this, it is always a good idea to start working with an estate planning attorney, as well as with a financial advisor. Work with a Warren Street Wealth Advisor today to get your personalized financial plan and more guidance on estate planning.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/08/Blog-Thumbnail.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2023-08-17 08:51:512024-11-07 09:21:18Probate: 3 Easy Ways to Avoid it