At the core of financial literacy lies a set of values and behaviors that extend beyond mere dollars and cents. As parents, caregivers, and educators, we have the unique opportunity to shape the financial mindsets of the next generation by imparting timeless wisdom that transcends monetary transactions.

As we celebrate Financial Literacy Month this April, let’s commit to empowering our children with the knowledge, skills, and values they need to thrive in an increasingly interconnected world. Teach your children these four fundamental lessons that build financial savviness over time.

Believe in Yourself: Confidence is the cornerstone of success in any endeavor. Encourage children to believe in their abilities and to recognize the value they bring to the table. By fostering a sense of self-assurance, we empower our youth to navigate the complexities of the financial landscape with poise and resilience.

Listen to Others: Effective communication is a two-way street that involves not only speaking but also actively listening. Teach children the importance of lending an ear to others, as every voice has the potential to impart valuable insights. By honing their listening skills, children cultivate a sense of empathy and discernment that serves them well in both personal and professional spheres.

Put in the Hard Work: Success seldom comes without effort. Encourage children to embrace the virtue of hard work by involving them in household chores, encouraging academic diligence, or exploring part-time employment opportunities. By instilling a strong work ethic, we equip children with the tools they need to pursue their goals with diligence and determination.

Budget, Save, & Invest: Introduce children to the concepts of budgeting, saving, and investing in a manner that is accessible and relatable. Emphasize the connection between hard work and financial resources, illustrating how responsible financial management enables individuals to achieve their aspirations. Encourage children to set aside a portion of their earnings for savings and explore the possibilities of investment, laying the groundwork for a secure financial future.

By integrating these principles into everyday interactions and activities, you can nurture a generation of financially literate individuals who are equipped to navigate the complexities of an ever-evolving economic landscape. Together, we can pave the way for a brighter, more prosperous future for generations to come.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/03/How-to-Cultivate-Financial-Literacy-in-Children-and-Create-a-Pathway-to-Lifelong-Success.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2024-04-04 07:03:002024-03-22 11:09:40How to Cultivate Financial Literacy in Children and Create a Pathway to Lifelong Success

As a business owner, you’ve spent your life’s work growing your business, taking care of employees, managing your product or service, and looking after your people. Now, you may be getting to a point where your spouse tells you you work too much. Or perhaps you’re watching the clock more than you used to, counting down the minutes until you can head home and unplug from your “boss” responsibilities.

Whatever your reasoning, if you’re starting to ask questions like, “Do I have enough to sell?” and “Will that be enough?” then it’s time to focus on you for a change.

Why Business Owners Need Specialized Financial Planning

Business owners face a unique set of financial challenges and opportunities. Whether you are a small business owner or running a large corporation, the following considerations are critical:

Maximizing tax efficiency

Choosing the most appropriate retirement account type

Evaluating your retirement account options

Managing 401(k) and pension investments

Considering a defined benefit plan, i.e., “pension”

Aligning company benefits offerings with company goals

Our team specializes in helping business owners handle these and other issues while they’re still working. During those years, we help you work through proper planning techniques to diversify your assets, reduce risk, optimize your taxes, and offer competitive benefits. All of these steps help streamline and strengthen your business at the time — but they also set you up for a successful transition into retirement or your next business opportunity.

When you do get to the point of exiting, we help you bring all of this planning together into one critical decision: whether or not you have what you need to move on from your business and into your ideal retirement, whatever that looks like for you.

Creating a Dream Retirement

At Warren Street, we’ve helped many business owner clients over the years answer the “Do I have enough to sell?” question and develop their exit strategies accordingly.

If you choose to work with us during your own exit process, we’ll play a key role on your professional team alongside your attorney. While your attorney looks after the legal structure of the deal, we’ll handle related asset management and tax mitigation. For example, if you’re involved in an all-cash sale with multiple payments coming in the next few years, we will discuss tax deferral opportunities to add into your transition plan. Or, if you’re struggling with a go/no-go decision, we’ll conduct scenario planning to help you make an informed choice based on your current financial situation, projected future state, and personal goals.

No matter where you are in the exit planning process, we can help evaluate your current assets, investments, estate planning, and legacy goals, so you can make a clear and confident decision on what next steps are right for you.

If this sounds like you and you’re a current Warren Street client, please mention your interest to your Lead Advisor! Or, if you’re not a client but are interested in learning how we can help, schedule a complimentary introductory call with us. We hope to hear from you and look forward to exploring how we can make your post-exit dreams a reality.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/12/Do-I-Have-Enough-To-Sell.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-12-28 08:24:002024-06-03 10:46:08Do I Have Enough to Sell My Business?

Scan the financial headlines these days, and you’ll see plenty of potential action items vying for your year-end attention. Some may be particular to 2023. Others are timeless traditions. Here are our three favorite items worth tending to as 2024 approaches… plus a thoughtful reflection on how to make the most of the remaining year.

1. Bolster Your Cash Reserves

With some high yield savings options currently offering ~5%+ annual interest rates, your fallow cash is finally able to earn a nice little bit while it sits. Sweet! Two thoughts here:

Mind Where You’ve Stashed Your Cash: If your cash savings is still sitting in low- or no-interest accounts, consider taking advantage of the attractive rates available in other options. If you’re unsure where to start, we can help you figure out whether a high yield savings account, a CD, or treasury bonds may make sense for you. Your cash savings typically includes money you intend to spend within the next year or two, as well as your emergency, “rainy day” reserves.

Put Your Cash in Context: While current rates across many accounts are appealing, don’t let this distract you from your greater investment goals. Even at today’s higher rates, your cash reserves are eventually expected to lose their spending power in the face of inflation. Today’s rates don’t eliminate this issue … remember, inflation is also on the high side, so that 5% isn’t as amazing as it may seem. Once you have your cash stashed in those high-interest savings accounts, you’re likely better off allocating your remaining assets into your investment portfolio—and leaving the dollars there for pursuing your long game.

2. Polish Your Portfolio

While we don’t advocate using your investment reserves to chase money market rates, there are still plenty of other actions you can take to maintain a tidy portfolio mix. For this, it’s prudent to perform an annual review of how your investments are growing. Year-end is as good a milestone as any for this activity. For example, you can:

Rebalance: In 2023, year-to-date stock returns may warrant rebalancing back to plan, especially if you can do so within your tax-sheltered accounts. If you are an existing Warren Street client, this is already being handled on your behalf.

Relocate: With your annual earnings coming into focus, you may wish to shift some of your investments from taxable to tax-sheltered accounts, such as traditional or Roth IRAs, HSAs, and 529 College Savings Plans. For many of these, you have until next April 15, 2024 to make your 2023 contributions. But you don’t have to wait if the assets are available today, and it otherwise makes tax-wise sense.

Redirect: Year-end can also be a great time to redirect excess wealth toward personal or charitable giving. Whether directly or through a Donor Advised Fund, you can donate highly appreciated investments out of your taxable accounts and into worthy causes. You stand to reduce current and future taxes, and your recipients get to put the assets to work right away.

3. Minimize Your Taxes

Speaking of taxes, there are always plenty of ways to manage your current and lifetime tax burdens—especially as your financial numbers and various tax-related deadlines come into focus toward year-end. For example:

RMDs and QCDs: Retirees and IRA inheritors should continue making any obligatory Required Minimum Distributions (RMDs) out of their IRAs and similar tax-sheltered accounts. With the 2022 Secure Act 2.0, the penalty for missing an RMD will no longer exceed 25% of any underpayment, rather than the former 50%. But even 25% is a painful penalty if you miss the December 31 deadline. If you’re charitably inclined, you may prefer to make a year-end Qualified Charitable Distribution (QCD), to offset or potentially eliminate your RMD burden.

Harvesting Losses … and Gains: Depending on market conditions and your own portfolio, there may still be opportunities to perform some tax-loss harvesting in 2023, to offset current or future taxable gains from your account. As long as long-term capital gains rates remain in the relatively low range of 0%–20%, tax-gain harvesting might be of interest as well. Work with your tax-planning team to determine what makes sense for you. If you are an existing Warren Street client, we will automatically tax loss harvest for you.

How else can we help you tend to your 2023 plans and till the soil for 2024? Please be in touch for additional ideas and best-practice advice.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/11/Finacial-Practices-2023.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-11-28 08:15:162024-11-07 09:20:043 Financial Best Practices for Year-End 2023

Nobody wants to make investment mistakes. And yet, we’re human; mistakes happen. Here’s how to minimize the ones that matter the most, and make the most of the ones that remain.

Bad Decisions vs. Bad Outcomes

First, let’s define what we’re talking about:

Investment mistakes happen when you make bad decisions, regardless of whether the outcome is good or bad.

Bad decisions are the ones a rational investor would not make. For example:

Failing to spread your risks around: Concentrating in too few securities, instead of diversifying across many, and many types of investments.

Confusing speculating with investing: Chasing or fleeing hot trends, instead of structuring your total portfolio to capture expected market growth over time.

Taking on too much or too little investment risk for your circumstances: Investing too conservatively or too aggressively for your financial goals and risk tolerances.

Overlooking taxes: Spending more than necessary to participate in the market’s expected long-term growth.

Succumbing to harmful behavioral biases: Acting on gut feel over rational resolve.

These common investment mistakes share a recurring theme: By making wise decisions about that which you can control, you can best prepare for that which you cannot.

Damage Control

Consider auto insurance as an analogy with similar controllable choices and random risks. From hail storms to hit-and-runs, misfortunes happen. They are not your fault; they are not your mistake. But you insure against them anyway, since they can still generate a substantial loss.

You also do all you can to minimize your “at fault” errors. You don’t drive while impaired. You keep your vehicle in safe repair. You observe traffic laws. None of these sound decisions guarantee success, but they appreciably increase the odds you’ll remain accident-free.

As an investor, you can take a similar approach:

Mistake-free investing does not guarantee success. Rather, it improves your odds for happy outcomes, while softening the blow if misfortune strikes.

It’s worth noting, even if you make all the right investment decisions for all the right reasons, random misfortune can still strike. If it does, it would be a mistake to decide your prudent investment strategy was to blame. It would be an even worse mistake to abandon that strategy because you’ve encountered the equivalent of a market hit-and-run. This would be like dropping your insurance coverage because it didn’t prevent the accident to begin with.

The Upside of Making Investing Mistakes

“I’ve failed over and over and over again in my life. And that is why I succeed.” — Michael Jordan

As just about any star athlete will tell you, the path to success is paved with errors. The same can be said about investing. The occasional misguided decision may even be good for you as an investor—especially if it’s made when the stakes are smaller and time is on your side.

The point is, if you’ve made investment mistakes in the past, don’t beat yourself up over them, or make more mistakes trying to “fix” the past (such as deciding you’ll never invest again after being burned by the market). Often, your best move is to identify which investment mistakes were involved, embrace the lessons learned, and give yourself permission to move on.

Admittedly, if you made an investment that didn’t pay off as you hoped for, it may be hard to know just what went wrong. Was it you, the whims of the market, or both?

Among our chief roles as a financial advisor is to help you sort out investment errors from market misfortunes, so you can move forward with greater resolve. Sometimes, this means adjusting your portfolio to reflect evolving personal financial goals or targets. Often, it means convincing you to stay the course with your already-solid plan. Either way, your future is not yet written. Reach out to us today if we can help you make the most of your next steps.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/10/Financial-Quick-Takes-Making-Mistakes-Blog.png10801080Warren Street Teamhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgWarren Street Team2023-10-19 07:35:242024-11-07 09:20:50Financial Quick Takes: Making Mistakes

Ever heard of the 80/20 rule? It suggests 80% of an outcome is often the result of just 20% of the effort you put into it.

Often, by prioritizing the 20% of your efforts that make the biggest splash, you can reduce excess commotion. In that spirit, here are 3 financial best practices that pack a lot of value per “pound” of effort.

Going back to 1926 and after adjusting for inflation, U.S. stocks have delivered about 7.3% annualized returns to investors who have simply been there, earning what the markets have to offer over the long haul. Those who instead fixate on dodging in and out of hot and cold markets are expected to reduce, rather than improve their end returns. That’s because, when markets recover from a downturn, they often more than make up for the stumble quickly, dramatically, and without warning. Instead of chasing trends, simply stay invested over time.

2. Portfolio Management: Use Asset Allocation, and Don’t Monkey With the Mix

Asset allocation is about investing in appropriate percentages of security types, or asset classes, based on their risk/return “personality.” For example, given your financial goals and risk tolerances, what ratio of stocks versus bonds should you hold?

Both practical and academic analyses have found that asset allocation is responsible for a great deal of the return variability across and among different portfolios. So, to build an efficient portfolio, we advise paying the most attention to your overall asset allocation, rather than fussing over particular securities. Luckily, if you’re a client of ours we’ve already taken care of this for you.

3. Financial Planning: Do It, But Don’t Overdo It

Also in 80/20 rule fashion, an ounce of financial planning can alleviate pounds of doubt. Planning connects your resources with your values and priorities. It’s your touchstone when uncertainty eats away at your resolve. And it guides how and why you’re investing to begin with.

Here’s some good, 80/20 news: Your plan need not be elaborate or time-consuming to be effective. In The One-Page Financial Plan, author Carl Richards describes:

“Your one-page plan simply represents the three to four things that are the most important to you: some action items that need to get done along with a reminder of why you’re doing them.”

If you’d like to do more, great. But even a one-page plan will give you a huge head start. Write it down, as Richards describes. When in doubt, read what you’ve written. Is it still “you”? If so, your work is done; stick to plan. If not, consider what’s changed, and update your plan accordingly. I

Building Lifetime Wealth, 80/20 Style

Properly applied, the 80/20 rule can help minimize the time and energy you have to put into maximizing your financial well-being. Whether you’re saving for retirement, funding your kids’ college education, preparing for a wealth transfer, applying for insurance, or otherwise managing your hard-earned wealth, we can help you identify and execute these and other actions that matter the most, so you can get back to the rest of your life.

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/03/80-20-Rule-Blog.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-07-28 08:57:432024-11-07 09:21:403 Ways to Apply the 80/20 Rule to Your Financial Pursuits

In planning for retirement, one topic is often top of mind: whether or not Social Security will still be around when we retire.

As we covered in a related post, When Should You Take Your Social Security, most of us have been paying into the program our entire working life. We’re counting on receiving some of that money back in retirement.

But then there are those headlines, warning us that the Social Security trust fund is set to run dry around 2034.

Does this mean you should grab what you can, as soon as you’re able? Let’s explain why we agree with Social Security specialist Mary Beth Franklin, who suggests the following:

“While there may be good reasons to file for reduced Social Security benefits early, claiming Social Security prematurely out of fear is a bit like selling stocks in a down market: All you’ve guaranteed is that you’ve locked in a loss. And if future benefit cuts did materialize, the benefits of those who claimed as soon as possible would be reduced even further.”

While we don’t expect Social Security to go bust, we do expect it will need to change in the years ahead. As its trustees have reported:

“Social Security is not sustainable over the long term at current benefit and tax rates … [and] trust fund reserves will be depleted by 2034.”

But let’s unpack this statement. First, “depleted” does not mean the Social Security Administration is going to turn out the lights and go home. It means it could run out of trust fund reserves by then, which are used to top off the total amount spent on Social Security benefits. There are still payroll taxes and other sources to cover more than 77% of the program’s payouts. So, worst case, if we did nothing but wait for the reserves to run out, we’d be forced to make hard choices about an approximate 23% shortfall starting around 2034.

Admittedly, Social Security is between a rock and a hard place. Nobody wants to lose benefits they’ve been counting on or spend significantly more to maintain the status quo. But if we don’t do something to shore up the program’s reserves, our options will likely only worsen.

In this context, the political will to reform Social Security seems strong, and bipartisan. As Buckingham Strategic Partners retirement planning specialist Jeffrey Levine has observed:

“My gut sense is that practically no politician in America would ultimately be happy having to explain to voters why they let Social Security collapse on their watch … That’s not a great message to have to bring to voters, especially older voters who show up at the polls in the greatest numbers.”

As members of Congress wrangle over the “best” (or least abhorrent) solutions for their constituents, they have been submitting proposals behind the scenes, and the Social Security Administration has been weighing in on the estimated effect for each.

Time will tell which proposals become legislated action, but the range of possibilities essentially falls into two broad categories: We can pay more in, or we can take less out.Most likely, we’ll need to do a bit of both.

Possible Ways to Pay More In

To name a few ways to replenish Social Security’s reserves, Congress could:

Raise the cap on wages subject to Social Security tax: As of 2023, earnings beyond $160,200 per year are not subject to Social Security tax. There’s been talk of increasing this cap, eliminating it entirely, or reinstating it for income beyond certain high-water marks.

Increase the Social Security tax rate for some or all workers: Currently, employers and employees each pay in 6.2% of their wages, for a total 12.4% up to the aforementioned wage cap. (This does not include an additional Medicare tax, which is not subject to the wage cap.) As cited in a September 2022 University of Maryland School of Public Policy report, “73% (Republicans 70%, Democrats 78%) favored increasing the payroll tax from 6.2 to 6.5%.”

Increase the tax on Social Security payouts, and direct those funds back into the program: Currently, if your “combined income” exceeds $44,000 on a joint return ($34,000 on an individual return), up to 85% of your Social Security benefit is taxable, as described here. Anything is possible, but taxing retirees more heavily seems less politically palatable than some of the other options.

Identify new funding sources: For example, one recent bipartisan proposal would establish a dedicated “sovereign-wealth fund,” seeded with government loans. Presumably, it would be structured like an endowment fund, with an investment time horizon of forever. In theory, its returns could augment more conservatively invested Social Security trust fund reserves. Other proposals have explored a range of potential new taxes aimed at filling the gap.

Options for Taking Less Out

We could also cut back on Social Security spending. Some of the possibilities here include:

Reducing benefits: Payouts could be cut across the board, or current bipartisan conversations seem focused on curtailing wealthier retirees’ benefits.

Extending the full retirement age: There are proposals to extend the full retirement age for everyone, or at least for younger workers. This would effectively reduce lifetime payouts received, no matter when you start drawing benefits.

Tinkering with COLAs: There are also bipartisan conversations about replacing the benchmark used to calculate the Cost-of-Living Adjustment (COLA), which might lower these annual adjustments in some years.

These are just a few of the possibilities. Some would impact everyone. Others are aimed at higher earners and/or more affluent Americans. It’s anybody’s guess which proposals make it through the political gamut, or what form they will take if they do.

Should You Take Your Social Security Early?

So, given the uncertainties of the day, should you start drawing benefits sooner than you otherwise would? An objective risk/reward analysis helps guide the way.

Many investors feel “safer” taking their Social Security as soon as possible, to avoid losing what seems like a bird in the hand. However, the appeal of this approach is often fueled by deep-seated loss aversion. Academic insights suggest we dislike the thought of losing money about twice as much as we enjoy the prospect of receiving more of it. Thus, we tend to cringe more over a potential loss of promised benefits than we factor in the substantial rewards we stand to gain by waiting. Put another way:

You’re not reducing your financial risks by taking Social Security early. You’re only changing which risks you’re taking. In exchange for an earlier and more assured payout, you’re also accepting a permanent, cumulative cut to your ongoing benefits.

If this still seems like a fair trade-off, consider that Social Security is one of the few sources of retirement income ideally structured to offset three of retirement’s greatest risks:

Life expectancy risk: In an annuity-like fashion, Social Security is structured to continue paying out, no matter how long you and your spouse live.

Inflation risk: The payouts are adjusted annually to keep pace with inflation.

Market risk: Even in bear markets, Social Security keeps paying, with no drop in benefits.

In short, if you are willing and able to wait a few extra years to receive a permanently higher payout, you can expect to better manage all three of these very real retirement risks over time.

This is not to say everyone should wait until their Full Retirement Age or longer to start taking Social Security. When is the best time for you and your spouse to start drawing benefits? Rather than hinging the decision on uncontrollable unknowns, we recommend using your personal circumstances as your greatest guide. Consider the retirement risks that most directly apply to you and yours, and chart your course accordingly.

But you don’t have to go it alone. Please be in touch if we can assist you with your Social Security planning, or with any other questions you may have as you prepare for your ideal retirement.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/04/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2023-05-11 08:28:422024-11-07 09:23:22Why We Believe Social Security Will Endure

Ever since President Franklin D. Roosevelt signed the 1935 Social Security Act, most Americans have pondered this critical question as they approach retirement:

“When should I (or we) start taking my (or our) Social Security?”

And yet, the “right” answer to this common query remains as elusive as ever. It depends on a wide array of personal variables, including how the unknowable future plays out.

No wonder many families find themselves in a quandary when it comes to taking their Social Security benefits. Let’s take a closer look at how to find the right balance for you.

Social Security Planning: A Balancing Act

For Social Security planning purposes, you reach full retirement age (FRA) between ages 66–67, depending on the year you were born. However, you can generally begin drawing Social Security benefits as early as age 62 (with the lowest available monthly starting payments) or as late as age 70 (for the highest available monthly starting payments).

Retirees are often advised to wait at least until their full retirement age, if not until age 70 to begin taking Social Security. In raw dollars, waiting to take your Social Security often works out to be the best deal for many families. Plus, these days, many of us choose to work well into our 60s, 70s, and beyond. Some analyses have even factored in the cost of spending down other assets while you wait, rather than using them for continued investment growth. The conclusion is the same.

However, you’re not “many families.” You’re your family. Your personal and practical circumstances may mean this general rule of thumb won’t point to your best choice. Following are some of the most common factors that may influence whether to start taking Social Security sooner or later.

Alternative Income Sources: First, and perhaps most obviously, if you have few or no alternative income sources once your paychecks stop, you may not have the luxury of waiting. You may need to start taking Social Security as soon as possible.

Life Expectancy: If you’re considering the benefits of waiting until age 70 to take Social Security, remember that this strategy assumes you live to at least the average age someone your age and gender is likely to reach. Even if you can afford to wait, you’ll want to factor in whether your health, lifestyle, and family history justify doing so.

Estate Planning: Have you placed a high or low priority on leaving as much as possible to your heirs and/or favorite charities after you pass? Your preferences here may influence how, and from where you’ll spend down your inheritable estate, which in turn may influence the timing of your Social Security enrollment.

Employment: How likely is it you’ll keep working until your FRA? Once you reach it, you can collect full Social Security benefits, even if you’re still working. But until then, your earnings may reduce your Social Security benefits.

Marital Status: If you’re married, one of you has probably paid in more to Social Security. One is likely to live longer. You may retire at different times, and your ages probably differ. All these factors can complicate the equation. You’ll want to consider the timing, rules, and outcomes under various scenarios—such as when and whether to take Social Security as an earner, the spouse of an earner, the widow or widower of an earner, or an ex-spouse of an earner—while also factoring in whether you and/or your spouse are still working prior to your FRAs, as described above. Ideal start dates for one scenario may not be ideal for another.

Other Circumstances: Beyond your marital status, there are other factors that may influence your timing decisions if they apply to you—such as if you’re a business owner, you live abroad, you qualify for Social Security Disability, or your children qualify for Social Security benefits under your account.

Income Taxes: We find many pre-retirees don’t realize that up to 85% of their Social Security income may be taxable. Your annual Social Security income also figures into your modified adjusted gross income (MAGI), which can push you past thresholds for incurring Medicare surcharges (beginning at age 65, based on your MAGI from two years prior). Bottom line, broad tax planning may influence your timing as well.

Degrees of Control

Clearly, there’s a lot to think about when deciding when to start taking Social Security. Whether you’re going it alone or with a financial planner, here’s one piece of advice that should help:

Control what you can. Let go of what you can’t.

What do we mean by that? There are many known factors you can include in your Social Security planning. You know your marital status. You can access your Social Security account and/or use a calculator to estimate your benefits. You can make educated guesses about your life expectancy, how long you’ll work, and so on. Also, if you’ve delayed taking Social Security past your FRA, you may be able to change your mind … to a point. You can file to collect up to six months of retroactive benefits if you end up needing the income sooner than planned.

You can use all of this planning information and more to make reasonable assumptions and timely decisions about when to take your Social Security.

After that, we recommend going easy on yourself if (or more realistically, when) some of your plans don’t go as planned. Come what may, you’ve done your best. Instead of channeling energy into regretting good decisions, use it to make judicious adjustments whenever new assumptions arise. By consistently focusing on what we know rather than what we hope or fear, we remain best positioned to shift course as warranted in the face of adversity.

Whether you’re planning to file for Social Security or you’re already drawing it, we appreciate the opportunity to help you and your family make good choices about when, and how to manage your available options. We hope you’ll contact us today to learn more.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/01/When-Should-You-Take-Your-Social-Security.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-03-30 08:02:002024-11-07 09:23:46When Should You Take Your Social Security?

To say the least, there has been plenty of political, financial, and economic action this year — from rising interest rates to elevated inflation to ongoing market turmoil.

How will all the excitement translate into annual performance in our investment portfolios? The answer remains to be seen. But, while we wait to find out, here are five action items worth tending to before 2022 is a wrap.

Revisit Your Cash Reserves

Where is your cash stashed these days? After years of offering essentially zero interest in money markets, savings accounts, and similar platforms, some banks are now offering higher interest rates to savers.

Shop around: If you have significant cash saved up, now may be a good time to compare rates on cash accounts. We can help if you need guidance exploring the options.

Put Your Money to Work

If you’re sitting on more cash than you need in your emergency reserve, you may be able to put it to even better use under current conditions. Consider the following:

Lighten your debt load: Carrying high-interest debt is a threat to your financial well-being, especially in times of rising rates. Consider paying off credit card balances or other debts. Avoid accruing new debt during the holiday season.

Invest: Reach out to your lead advisor to determine what your opportunities are to put some cash to work in the markets.

Make Some Smooth Tax-Planning Moves

Another way to save more money is to pay less in taxes. Here are a couple of year-end ideas:

It’s still harvest season: Market downturns often present opportunities to engage in tax-loss harvesting by selling taxable shares at a loss, and promptly reinvesting the proceeds in a similar (but not identical) fund. You can then use the losses to offset taxable gains, without significantly altering your investment mix. If you have a non-retirement brokerage account with us, we’ve already been doing this on your behalf.

Maximize tax opportunities: Make sure you are taking advantage of your 401(k) and other tax-deferred investment opportunities. With only a few paychecks left in 2022, you’ll want to make sure your contributions are optimized.

Check Up on Your Healthcare Coverage

As year-end approaches, make sure you and your family have made the most of your healthcare coverage. Take a moment to examine all your benefits. For example, if you have a Health Savings Account (HSA), have you funded it for the year? If you have a Flexible Spending Account (FSA), have you spent any balance you cannot carry forward? If you’ve already met your annual deductible, are there additional covered expenses worth incurring before the meter resets in 2023? If you’re eligible for free annual wellness exams or other benefits, have you used them?

Get Set for 2023

Why wait for 2023 to start anew? Year-end can be an ideal time to take stock of where you stand and consider what you’d like to achieve in the year ahead.

Audit your household interests: What has changed, and what hasn’t? Have you shifted careers or decided to retire? Added new hobbies or encountered personal setbacks? How might these and other significant life events alter your ideal investment allocations, cash-flow requirements, insurance coverage, or estate plan?

How Can We Help?

How else can we help you wrap 2022 and position you and your loved ones for the year ahead?

Whether it’s helping you manage your investment portfolio, optimizing your tax planning, considering your cash reserves, weighing insurance offerings, or assessing any other components that contribute to your financial well-being, we stand ready to assist — today, and through the years ahead.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/12/Best-Practices-for-Year-End-2022-Blog-Thumbnail.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2022-12-16 08:30:212024-11-07 09:26:51Five Financial Best Practices for Year-End 2022

You just learned that you are going to have a new baby or child join your family, by birth or adoption. It’s an exciting time! As you start to make preparations you will quickly discover that there is a seemingly endless list of things to do, items to buy, books to read, and classes to take.

Despite what the targeted ads and influencers may tell you, it doesn’t matter too much if your bundle of joy has state-of-the-art nursery gear or the trendiest stroller on the market. But there are a few financial planning considerations that will make a world of difference for your family and your child’s well-being.

1. Estate Planning

As soon as you become responsible to care for a dependent, basic estate planning documents are essential. You may think you don’t currently have an estate plan if you have not drafted a will or trust, but guess what? You actually do have an estate plan! It was written for you by federal and state law and will be administered by a court (at your estate’s expense). If you pass away you can either rely on the state’s estate plan for you, or you can have the peace of mind that comes from writing your own estate plan that is specific for your wishes and your family’s best interests.

At a minimum, all parents (or anyone with financial dependents) should have (a) a will that includes guardianship designations, (b) an advanced health care directive, and (c) a durable power of attorney. Many parents or guardians will also want to establish a trust.

In addition to drafting these documents, we also recommend making sure that you have named non-minor primary and contingent beneficiaries on all your financial accounts and life insurances. At your death, many accounts will simply pass to the named beneficiaries on file.

If you were to pass away tomorrow, your partner and/or children would most likely need additional financial support. The cost of a funeral, additional child care, extra time off work, and covering everyday expenses and bills can add up. Not to mention the desire many parents have to help with specific expenses, such as education, for a child. Life insurance can fill that gap and provide vital support and peace of mind to your family during a difficult time.

Whatever role you serve in your household, there is a cost to your absence. If you are an income-earner for your household, the loss of your income would need to be supplemented for your family. If you are the primary caretaker of children and household manager, your labor would need to be replaced. Life insurance is for everyone with dependents, no matter their income-earning or employment status.

Term life insurance is usually inexpensive and easy to obtain. We strongly recommend term life insurance for all parents or those with dependents.

3. Extra Cash Savings

The cost of having a baby is no small thing. There are baby essentials to buy, doctor’s appointments to attend, and the labor and delivery bill at the end. It can add up to thousands of dollars to bring a new life into the world, and that is without a single complication. Additional medical care, a NICU stay, or any other unexpected circumstances can compound the bill.

When you find out that you, or your partner, is pregnant, you should start making plans for your cash flow needs. Remember that so much of the next 9-12 months is unpredictable for your bank account, so having a larger-than-average cash reserve is a good idea.

Medical care and baby items are the first expenses that come to mind when planning for your new child. But it is wise to also consider what other large expenses may come up during the pregnancy and postpartum period. Your savings account during this time has to do double duty as a baby preparedness fund and an ongoing emergency fund.

Consider two of the biggest culprits for emergency fund withdrawals – home repairs and car repairs. Do you have a lingering issue with a home appliance that is going to require a repair or replacement any day? Is your old car on its last leg? Is there anything in your house or car that needs to be addressed to ensure safety for your little one? Keep in mind that these non-baby expenses can and should be part of all the other preparations.

There is no hard fast rule for how much to save for a new baby, but having easily-accessible cash in a savings account is a must. If your emergency fund is slim, it may be time to pause aggressive debt repayment plans, saving for your next vacation, or excessive spending on non-essentials and put that extra cash in savings. Once you have returned to a more predictable financial situation, you can reevaluate your budget and priorities and return to your usual emergency fund and other financial goals.

4. Know Your Legal Rights and State Benefits

The state that you work in may have specific laws that require your employer to provide a certain amount of leave for pregnancy-related disability and/or bonding with a new child. Your state may also have paid leave or disability pay available for pregnancy and the postpartum leave period. You should carefully research your legal rights as a worker in your state and be familiar with all the benefits available to you.

In California, there are three laws or resources available to support you during pregnancy and postpartum and to bond with a new child: the Family and Medical Leave Act (FMLA), Paid Family Leave (PFL), and State Disability Insurance. FMLA legally protects the ability of eligible employees to take up to 12 workweeks of unpaid leave a year. PFL provides up to 8 weeks of payments for lost wages due to time off work to bond with a new child. State Disability Insurance may provide payments during pregnancy and postpartum recovery if you are unable to work.

Visit the following state websites to learn more about these California benefits:

On top of any legally-required paid or unpaid leave, your employer likely has their own company policies related to family leave. Ask your HR representative for all the information you can get about these policies. Start making a plan for how you (and your partner, if applicable) will take leave and how you will bridge any gaps in income during this time.

Your ability to negotiate paid or unpaid leave depends on various factors, but many employers are becoming more family friendly. Talk with a trusted supervisor or manager about your options. Don’t be afraid to negotiate and ask for what you need in terms of additional paid time off, schedule flexibility, or extended leave.

– – –

Are you expecting a little one? First – congratulations! If you feel like now is the time to get the support of a financial professional for your growing family, contact Warren Street for a one hour consultation.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/11/New-Parents-FP-Blog-Thumbnail.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-11-10 08:21:002024-11-07 09:27:45Essential Financial Planning for Expecting Parents

Estate planning is one of the most important things you can do to protect your family and your assets. It ensures that your assets and belongings go exactly where you want them and saves your family an immense amount of stress, pain, and cost. Still, estate planning often becomes an afterthought, something that’s a “long way off” or “not a top priority right now.”

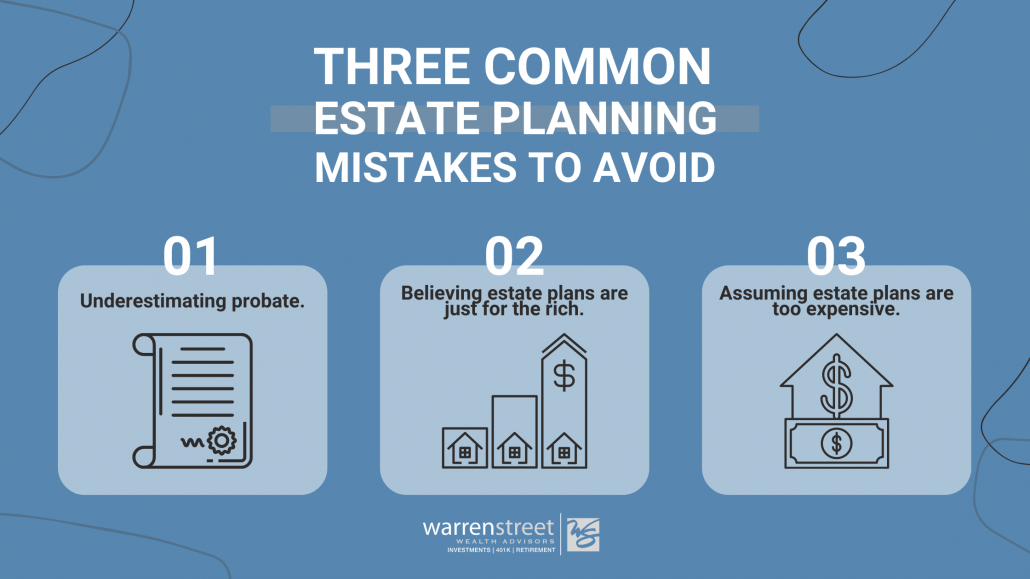

The good news is that estate planning isn’t as complicated as it sounds. You can establish the key documents you need with much less effort or investment than you might think. In my 33 years of advising Chevron employees, here are the most common mistakes I’ve seen and the steps you can take to avoid them.

1. Underestimating probate.

Too often, people put off estate planning because they don’t realize the alternative. If you didn’t have key estate documents in place, and something were to happen to you, all of your assets would go to probate. That is basically a simple way of saying the government would decide for you — in a very long, expensive, and public way — what to do with your assets.

I’ve seen probate negatively impact already grieving families who don’t have the bandwidth or money to deal with the probate process. It makes everything much simpler for your surviving family to have all of your documents in place, so they can focus on things that matter instead of the cost and process of dividing up your assets.

2. Believing estate plans are just for the rich.

Estate planning might sound fancy, but estate plans are not just for the wealthy. The six estate planning documents everyone should have include: 1) Will/trust, 2) Durable power of attorney, 3) Beneficiary designations, 4) Letter of intent, 5) Healthcare power of attorney, and 6) Guardianship designations. Beneficiary and guardianship designations are particularly critical for those with minor children, as they allow you to decide who would look after them.

A will or trust should be one of the core components of every estate plan, regardless of the amount of assets. These documents ensure that your assets go exactly where you want them. A durable power of attorney sets whom you would want to make decisions for you if you were unable to (otherwise, it would be up to the courts) — and the same principle applies to the healthcare power of attorney. Your letter of intent streamlines asset distribution and can also include wishes for your funeral. Beneficiary and guardianship designations state your wishes for your children and other beneficiaries.

3. Assuming estate plans are too expensive.

Having your assets go through probate is actually far messier and more expensive than creating an estate plan. How much more expensive? The average cost for probate and attorney fees for a $1MM estate is $46,000. The fee to set up an estate plan, on the other hand, averages just a few thousand dollars. That’s a drop in the bucket compared to probate, not to mention you also save your family time and stress by outlining everything in advance.

Most importantly, an estate plan leaves nothing to chance or guessing. Estate documents make it exceedingly clear whom you would like to take care of your children, get ownership of your house, inherit your money, etc. You can also detail how inheritance should occur (at specific ages, in specific percentages over time, etc.).

For more detail on how to set up your estate plan, join Warren Street and Hunsberger Dunn for a “Will, Trusts, & Estate Planning Webinar”Sept. 27. We’ll break down how to know if you need a living trust, best practices for creating wills and trusts, and more! Estate planning can seem convoluted, but we’re here for you to help make it as streamlined as possible.

–

Have questions about your Chevron retirement plan? Len is an expert in Chevron benefits and would be happy to meet with you. Click here to schedule a complimentary consultation with him.

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/09/Blog-Thumbnail-1.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2022-09-16 08:30:002022-09-16 08:43:10Chevron Employees: Avoid These Common Estate Planning Mistakes