Probate is the court process used to determine who gets an inheritance. In the eyes of a financial planner, it is a court process that most clients should try to avoid for many reasons. The probate process is time-consuming, usually lasting about a year depending on how backed up the courts are. The expense for probate is very high, which includes thousands of dollars going towards attorney and court fees. Probate is also a public court event in which potential heirs can object to the ruling pretty easily, causing privacy concerns and more attorney costs. While probate can have its time and place, there are some simple ways to avoid probate.

Let’s take a look at three easy steps you can take now to keep your loved ones from having to deal with probate.

Primary Beneficiary Designations – If a 401(k) account or life insurance policy lists a primary beneficiary, the account avoids probate and passes directly to the listed beneficiary. For brokerage accounts this is usually referred to as a Transfer-On-Death (TOD) account, and for bank accounts this is referred to as a Payable-On-Death account.

Contingent Beneficiary Designations – Setting a contingent beneficiary is also an easy way to help avoid probate. The contingent beneficiary is the person(s) next in line to inherit if the primary beneficiary has already passed away at the time of the account holder’s passing.

Retitle Your Automobile & House – Don’t forget about your car and home! If your vehicle or house are listed in your name alone, they would turn into probate assets at the time of your passing. Some states have introduced TOD car and house titling as a way to avoid needing probate if the owner passes away. Also, you and your spouse should consider owning the car and house jointly with rights of survivorship, as another way to avoid probate.

These planning points provided today are just some of the easy actions you can do yourself. There are more ways to avoid probate, but they get a little more complex and depend on your personal situation.

With legal matters like this, it is always a good idea to start working with an estate planning attorney, as well as with a financial advisor. Work with a Warren Street Wealth Advisor today to get your personalized financial plan and more guidance on estate planning.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/08/Blog-Thumbnail.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2023-08-17 08:51:512024-11-07 09:21:18Probate: 3 Easy Ways to Avoid it

Last week, the Supreme Court voted against the White House Administration’s plan to eliminate up to $10,000 of student loans for non-Pell grant recipients and up to $20,000 of loans for Pell grant recipients. This news comes just as the three-year pause on student loans is coming to an end, with loan interest accruing again in September and payments beginning in October.

The Administration plans to propose other types of aid to borrowers, such as reducing the income-driven repayment plan from 10% to 5% of disposable income and not reporting missed payments to credit rating agencies for 12 months. Still, the timeline on these proposals could take months to get approved — so it looks like it is time to prepare for paying back your student loans.

At Warren Street Wealth Advisors, we want you to take the necessary actions to feel confident about your next steps. Start with the considerations below, and feel free to reach out to your financial advisor with any questions.

1. Update your information on studentaid.gov.

Check that your current contact and billing information are up-to-date with the Education Department on studentaid.gov. If you’ve moved, for example, the Education Department will need your updated address to contact you with loan status updates.

2. Determine how much outstanding student loan debt you have.

Work with your loan provider to see how much student loan debt you have remaining and how much the monthly payments will be. Once you know how much to expect each month, it will be easier to manage your spending.

3. Factor student loan payments back into your budget.

Whether you use software to help analyze your budget or the back of an envelope to do your calculations, it is time to add up all of your expenses and compare them to your take-home pay. This will let you know if you will be running a surplus, breakeven or deficit each month going forward.

4. Explore income-driven options.

If you determine you might be at a monthly deficit with student loan payments, an income-driven repayment plan could be an option for you. However, while this option could help your monthly budget, it usually involves you paying more interest in the long-term and extends your payments well past the 10 year standard repayment plan.

5. Shore up your emergency fund.

It’s always a good idea to count your liquid cash savings, especially in a time like this. Having a three to six month emergency fund to fall back on will be important if you have a student loan bill you need to pay again. Now is a good time to start an emergency fund if you don’t have one.

These are some of the most important steps to ensure you make payments on time and know what to expect in the near future when it comes to your debt management. Please reach out if you’d like to discuss these planning points with a Warren Street advisor!

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/07/Student-Loan-Blog.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2023-07-12 09:00:002024-11-07 09:22:41It’s Time to Revisit Your Student Loans

Tax planning for your retirement savings is also important. To help with that, you can typically choose between two account types as you save for retirement: Traditional IRA or employer-sponsored plans, or Roth versions of the same.

All Things Roth

Either way, your retirement savings grow tax-free while they’re in your accounts. The main difference is whether you pay income taxes at the beginning or end of the process. For Roth accounts, you typically pay taxes up front, funding the account with after-tax dollars. Traditional retirement accounts are typically funded with pre-tax dollars, and you pay taxes on withdrawals.

That’s the intent, anyway. To fill in a few missing links, the SECURE 2.0 Act:

Eliminates Required Minimum Distributions for employer-sponsored Roth accounts, such as Roth 401(k)s and Roth 403(b)s, to align with individual Roth practices (2024)

Establishes Roth versions of SEP and SIMPLE IRAs (2023)

Lets employers make contributions to traditional and Roth retirement accounts (2023)

Lets families potentially move 529 plan assets into a Roth IRA (2024 – as described above)

There’s one thing that’s not changed, although there’s been talk that it might: There are still no restrictions on “backdoor Roth conversions” and similar strategies some families have been using to boost their tax-efficient retirement resources.

Speaking of RMDs

Not surprisingly, the government would prefer you eventually start spending your tax-sheltered retirement savings, or at least pay taxes on the income. That’s why there are rules regarding when you must start taking Required Minimum Distributions (RMDs) out of your retirement accounts. That said, both SECURE Acts have relaxed and refined some of those RMD rules.

Extended RMD Dates (2023): the original SECURE Act postponed when you must start taking taxable RMDs from your retirement account—from 70 ½ to 72. The SECURE 2.0 Act extends that deadline further. If you were born between 1951–1959, you can now wait until age 73. If you were born after that, it’s age 75.

Reduced Penalties (2023): If you fail to take an RMD, the penalty is reduced from a whopping 50% of the distribution to a slightly more palatable 25%. Also, the penalty may be further reduced to 10% if you fix the error within a prescribed correction window.

Aligned RMD Rules for Personal and Employer-based Roth Accounts (2024): As mentioned above, RMDs have been eliminated from employer-based Roth accounts. If you’ve already been taking them, you should be able to stop doing so in 2024.

Enhanced RMDs for Surviving Spouses (2024): If you are a widow or widower inheriting your spouse’s retirement plan assets, you will be able to elect to determine your RMD date as if you were your spouse. This provision can work well if your spouse was younger than you. As described here: “RMDs for the [older] surviving spouse would be delayed until the deceased spouse would have reached the age at which RMDs begin.”

An Addendum For Charitable Donors

One good thing hasn’t changed with SECURE 2.0: Even though RMD dates have been extended as described, you can still make Qualified Charitable Distributions (QCDs) out of your retirement accounts beginning at age 70 ½, and the income is still excluded from your taxable adjusted gross income, as well as from Social Security tax and Medicare surcharge calculations. Plus, beginning in 2024, the maximum QCD you can make (currently $100,000) will increase with inflation. Also, with quite a few caveats, you will have a one-time opportunity to use a QCD to fund certain charitable trusts or annuities.

Next Steps

How else can we help you incorporate SECURE 2.0 Act updates into your personal financial plans? The landscape is filled with rabbit holes down which we did not venture, with caveats and conditions to be explored. And there are a few provisions we didn’t touch on here. As such, before you proceed, we hope you’ll consult with us or others (such as your accountant or estate planning attorney) to discuss the details specific to you.

Come what may in the years ahead, we look forward to serving as your guide through the ever-evolving field of retirement planning. Please don’t hesitate to reach out to us today with your questions and comments.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

It can be hard to save for your future retirement when current expenses loom large. We advise proceeding with caution before using retirement savings for any other purposes, but SECURE 2.0 does include several new provisions to help families strike a balance.

Student Loan Payments Count as Elective Deferrals (2024): If you’re paying off student debt and trying to save for retirement, your student loan payments will qualify as elective deferrals in your company plan. This means, whether you contribute to your company retirement plan or you make student loan payments, your employer can use either to make matching contributions to your retirement account.

Transferring 529 Plan Assets to a Roth IRA (2024): This one is subject to a number of qualifying hurdles, but SECURE 2.0 establishes a path for families to transfer up to $35,000 of untapped 529 college saving plan assets into the beneficiary’s Roth IRA. With proper planning, this may help families “seed” their children’s or grandchildren’s retirement savings with their unspent college savings.

New Emergency Saving Accounts Linked to Employer Plans (2024): SECURE 2.0 has established a new employer-sponsored emergency savings account, which would be linked to your retirement plan account. Unless you are a “highly compensated employee” (as defined by the Act), you can use the account to save up to $2,500, with your contributions counting toward matching funds going into your main retirement plan account.

Relaxed Emergency Plan Withdrawals (2024): SECURE 2.0 relaxes the ability to take a modest emergency withdrawal out of your retirement plan. Essentially, as long as you self-certify that you need the money, you can take up to $1,000 in a calendar year, without incurring the usual 10% penalty for early withdrawal. Once you’ve taken an emergency withdrawal, there are several hurdles before you’re eligible to take another one.

Additional Exceptions to the 10% Retirement Plan Withdrawal Penalty (Varied): SECURE 2.0 has established new exceptions to the 10% penalty otherwise incurred if you tap various retirement accounts too soon. For example, there are several new types of public safety workers who can access their company retirement plans penalty-free after age 50. Various exceptions are also carved out if you’re terminally ill or a domestic abuse victim, or if you use the assets to pay for long-term care insurance. The Act also has modified how retirement plan assets are to be used for Qualified Disaster Recovery Distributions. Many of the new exceptions are fairly specific, so check the fine print before you proceed.

Relaxed Emergency Loans from Retirement Plans (2023): If you end up living in a Federally declared disaster area, SECURE 2.0 also increases your ability to borrow up to 100% of your vested plan balance up to $100,000, with a more generous pay-back window.

Expanded Eligibility for ABLE Accounts (2026): ABLE accounts help disabled individuals save for disability expenses, while still collecting disability benefits. Before, you had to be disabled before age 26 to establish an ABLE account. That age cap increases to 46.

A Tax Break for Disabled First Responders (2027): If you are a first responder collecting on a service-connected disability, at least a portion of your disability payments will remain tax-free, even once you reach full retirement age and begin taking a retirement pension.

Next Steps

If you missed the first part of the blog series, we discussed key provisions in the newly enacted SECURE 2.0 Act of 2022, including updates that impact (1) savers/investors and (2) employers/plan sponsors. Check in next week for the last part of this blog series, where we share tax planning tips under this new Act.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Who doesn’t enjoy tying up year-end loose ends? The original SECURE Act was signed into law on December 20th, 2019. Its “sequel,” the SECURE 2.0 Act, was similarly enacted at year-end on December 29th, 2022.

Both pieces of legislation seek to reform how Americans prepare for retirement while juggling current spending needs. How, when, or will each of us retire? How can government incentives, regulations, and safety nets help more people safely do so—or at least not get in the way?

These are questions we’ve been asking as a nation for decades, across shifting socioeconomic climates. Throughout, a hard truth remains:

Employers and the government play a role in helping you save for and spend in retirement, but much of the preparation ultimately falls on you.

Neither the original SECURE Act nor SECURE 2.0 has fundamentally changed this reality. SECURE 2.0 has, however, added far more motivational carrots than punishing sticks. Its guiding goal is right there in the name: Setting Every Community Up for Retirement Enhancement (SECURE). Following is an overview of its key components.

Note: Implementation for each SECURE 2.0 provision varies from being effective immediately, to ramping up in future years. A few even apply retroactively. Many of its newest programs won’t effectively roll out until 2024 or later, giving us time to plan. We’ve noted with each provision when it’s slated to take effect.

Saving More, Saving Better: Individual Savers

First, key provisions include several updates to encourage individual savers:

Expanded Auto-Enrollment Requirements (2025): Because you’re more likely to save more if you’re automatically added to your company retirement plan program, auto-enrollment will be required for additional new retirement plans. Even with auto-enrollment, you can still opt out individually. Also, the Act has made a number of exceptions to the rules, including, as described here, “employers less than 3 years old, church plans, governmental plans, SIMPLE plans, and employers with 10 or fewer employees.”

Higher Catch-Up Contributions (2024–2025): To accelerate retirement saving as you approach retirement age, SECURE 2.0 Act has increased annual “catch-up” contribution allowances for many retirement accounts (i.e., extra amounts allowed beyond the standard contribution limits); and, importantly, tied future increases to inflation. However, in many instances, the updates also require high-wage-earners ($145,000/year or higher) to direct their catch-up contributions to after-tax Roth accounts.

Faster Plan Participation for Part-Time Employees (2024): If you’re a long-term, part-time employee, the SECURE Act of 2019 made it possible for you to participate in your employer’s retirement plan. With SECURE 2.0, you’ll be eligible to participate after 2 years instead of 3 years (after meeting other requirements).

Saver’s Match for Low-Income Savers (2027): A Saver’s Credit for low-income families will be replaced by a more accessible Saver’s Match for those whose income levels qualify. While the credit offsets income on a tax form, the match will be a direct contribution into your retirement account, of up to $1,000 in government-paid matching funds.

An Expanded Contribution Window for Sole Proprietors (2024): If you’re a sole proprietor, you’ll be able to establish a Solo 401(k) through the current year’s Federal income tax filing date, and still fund it with prior-year contributions.

Potential Tax Error “Do Overs” (2025): To err is human, and often unintentional. As such, SECURE 2.0 has directed the IRS to apply an existing Employer Plans Compliance Resolutions System (EPCRS) to employer-sponsored plans and to IRAs. The details are to be developed, but as described here, the intent is to set up a system in which “most inadvertent failures to comply with tax-qualification rules would be eligible for self-correction.”

Finding Former Plans (2024): It can be hard for company plan sponsors to keep in touch with former employees—and vice-versa. SECURE 2.0 has tasked the Dept. of Labor with hosting a national “lost and found” database to help you search for plan administrator contact information for former employees’ plans, in case you’ve left any retirement savings behind.

Saving More, Saving Better: Employers

There also are provisions to help employers offer effective retirement plan programs:

Better Retirement Plan Start-Up Incentives (2023): Small businesses can take retirement plan start-up credits to offset up to 100% of their plan start-up costs (versus a prior 50% cap). Also, businesses with no retirement plan can apply for start-up credits if they join a Multiple Employer Plan (MEP)—and this one applies retroactively to 2020.

A New “Starter 401(k)” Plan (2024): The Starter 401(k) provides small businesses that lack a 401(k) plan a simpler path to establishing one. Features will include streamlined regulatory and reporting requirements; auto-enrollment for all employees starting at 3% of their pay; a $6,000 annual contribution limit, rising with inflation; and a deferral-only structure, meaning the plan does NOT permit matching employer contributions.

Expanded SIMPLE Plan Contributions (2024): Under certain conditions, SECURE 2.0 allows for additional employer contributions to, and higher participant contribution limits for SIMPLE IRA plans.

New Household Employee Plans (2023): Families can establish SEP IRA plans for their household employees, such as nannies or housekeepers.

Small Perks (2023): Until now, employers were prohibited from offering even small incentives to encourage employees to step up their retirement savings. Now, de minimis perks are okay, such as a gift card when a participant increases their deferral amount.

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/01/Secure-Act-2.0-Summary-for-Individuals-and-Employers.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2023-01-09 09:25:002023-01-18 09:01:04Secure Act 2.0: Summary for Individuals and Employers

You just learned that you are going to have a new baby or child join your family, by birth or adoption. It’s an exciting time! As you start to make preparations you will quickly discover that there is a seemingly endless list of things to do, items to buy, books to read, and classes to take.

Despite what the targeted ads and influencers may tell you, it doesn’t matter too much if your bundle of joy has state-of-the-art nursery gear or the trendiest stroller on the market. But there are a few financial planning considerations that will make a world of difference for your family and your child’s well-being.

1. Estate Planning

As soon as you become responsible to care for a dependent, basic estate planning documents are essential. You may think you don’t currently have an estate plan if you have not drafted a will or trust, but guess what? You actually do have an estate plan! It was written for you by federal and state law and will be administered by a court (at your estate’s expense). If you pass away you can either rely on the state’s estate plan for you, or you can have the peace of mind that comes from writing your own estate plan that is specific for your wishes and your family’s best interests.

At a minimum, all parents (or anyone with financial dependents) should have (a) a will that includes guardianship designations, (b) an advanced health care directive, and (c) a durable power of attorney. Many parents or guardians will also want to establish a trust.

In addition to drafting these documents, we also recommend making sure that you have named non-minor primary and contingent beneficiaries on all your financial accounts and life insurances. At your death, many accounts will simply pass to the named beneficiaries on file.

If you were to pass away tomorrow, your partner and/or children would most likely need additional financial support. The cost of a funeral, additional child care, extra time off work, and covering everyday expenses and bills can add up. Not to mention the desire many parents have to help with specific expenses, such as education, for a child. Life insurance can fill that gap and provide vital support and peace of mind to your family during a difficult time.

Whatever role you serve in your household, there is a cost to your absence. If you are an income-earner for your household, the loss of your income would need to be supplemented for your family. If you are the primary caretaker of children and household manager, your labor would need to be replaced. Life insurance is for everyone with dependents, no matter their income-earning or employment status.

Term life insurance is usually inexpensive and easy to obtain. We strongly recommend term life insurance for all parents or those with dependents.

3. Extra Cash Savings

The cost of having a baby is no small thing. There are baby essentials to buy, doctor’s appointments to attend, and the labor and delivery bill at the end. It can add up to thousands of dollars to bring a new life into the world, and that is without a single complication. Additional medical care, a NICU stay, or any other unexpected circumstances can compound the bill.

When you find out that you, or your partner, is pregnant, you should start making plans for your cash flow needs. Remember that so much of the next 9-12 months is unpredictable for your bank account, so having a larger-than-average cash reserve is a good idea.

Medical care and baby items are the first expenses that come to mind when planning for your new child. But it is wise to also consider what other large expenses may come up during the pregnancy and postpartum period. Your savings account during this time has to do double duty as a baby preparedness fund and an ongoing emergency fund.

Consider two of the biggest culprits for emergency fund withdrawals – home repairs and car repairs. Do you have a lingering issue with a home appliance that is going to require a repair or replacement any day? Is your old car on its last leg? Is there anything in your house or car that needs to be addressed to ensure safety for your little one? Keep in mind that these non-baby expenses can and should be part of all the other preparations.

There is no hard fast rule for how much to save for a new baby, but having easily-accessible cash in a savings account is a must. If your emergency fund is slim, it may be time to pause aggressive debt repayment plans, saving for your next vacation, or excessive spending on non-essentials and put that extra cash in savings. Once you have returned to a more predictable financial situation, you can reevaluate your budget and priorities and return to your usual emergency fund and other financial goals.

4. Know Your Legal Rights and State Benefits

The state that you work in may have specific laws that require your employer to provide a certain amount of leave for pregnancy-related disability and/or bonding with a new child. Your state may also have paid leave or disability pay available for pregnancy and the postpartum leave period. You should carefully research your legal rights as a worker in your state and be familiar with all the benefits available to you.

In California, there are three laws or resources available to support you during pregnancy and postpartum and to bond with a new child: the Family and Medical Leave Act (FMLA), Paid Family Leave (PFL), and State Disability Insurance. FMLA legally protects the ability of eligible employees to take up to 12 workweeks of unpaid leave a year. PFL provides up to 8 weeks of payments for lost wages due to time off work to bond with a new child. State Disability Insurance may provide payments during pregnancy and postpartum recovery if you are unable to work.

Visit the following state websites to learn more about these California benefits:

On top of any legally-required paid or unpaid leave, your employer likely has their own company policies related to family leave. Ask your HR representative for all the information you can get about these policies. Start making a plan for how you (and your partner, if applicable) will take leave and how you will bridge any gaps in income during this time.

Your ability to negotiate paid or unpaid leave depends on various factors, but many employers are becoming more family friendly. Talk with a trusted supervisor or manager about your options. Don’t be afraid to negotiate and ask for what you need in terms of additional paid time off, schedule flexibility, or extended leave.

– – –

Are you expecting a little one? First – congratulations! If you feel like now is the time to get the support of a financial professional for your growing family, contact Warren Street for a one hour consultation.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/11/New-Parents-FP-Blog-Thumbnail.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-11-10 08:21:002024-11-07 09:27:45Essential Financial Planning for Expecting Parents

When we invest money, our main objective is to see the money grow. When we think about market losses and downturns, we may think of painful periods where we watch our account balances decrease instead of grow. While market losses are never fun, they are unfortunately a part of the normal investment life cycle. However, when market volatility hands us losses, there are some options to make lemonade out of lemons.

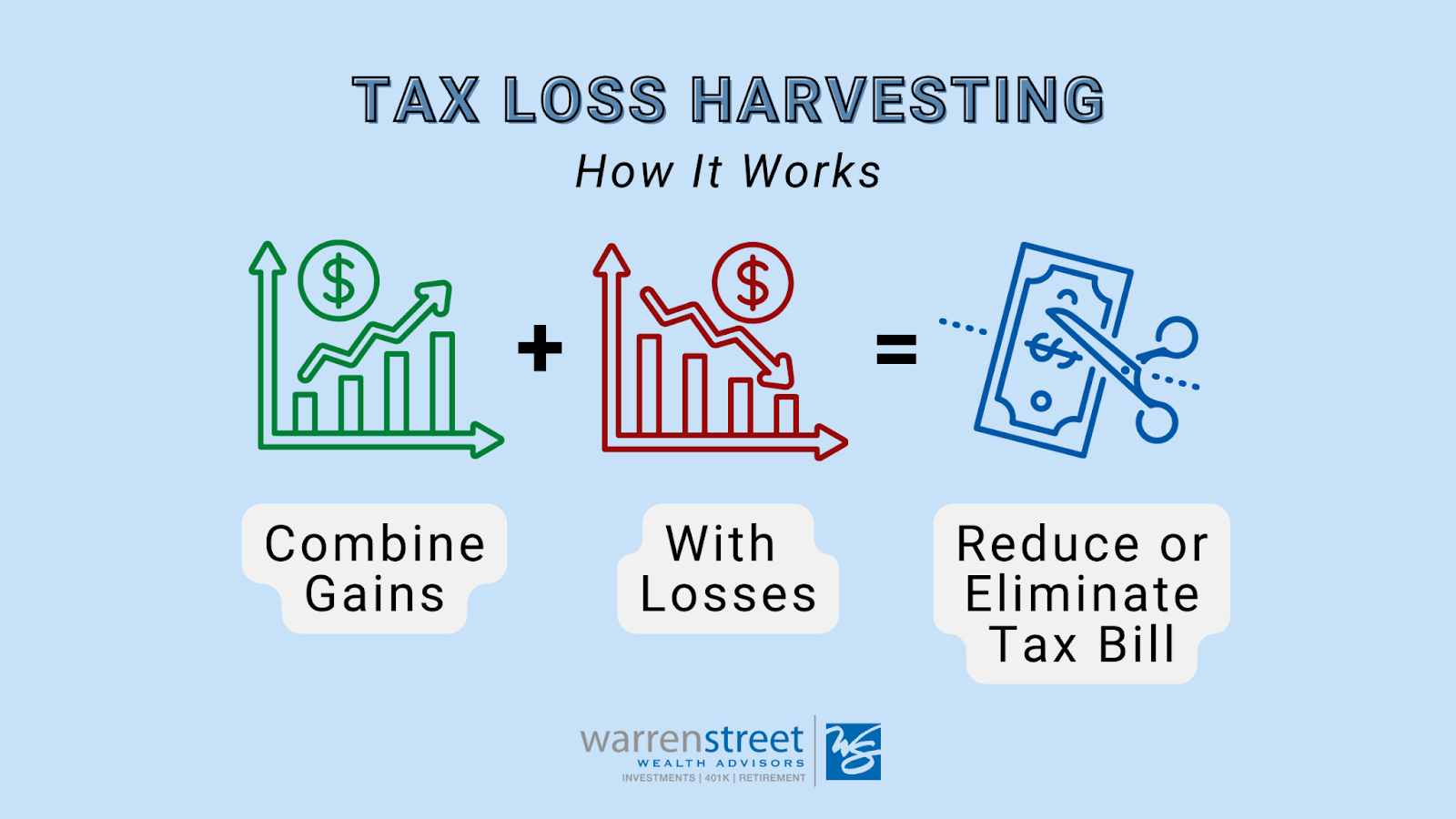

What is tax loss harvesting?

Tax loss harvesting is the process of selling securities while they are at a loss, realizing that loss for tax purposes, and then redeploying that money into another investment (such as a different stock, bond, or mutual fund). The IRS does not allow you to sell an investment at a loss, receive the tax benefit, and then immediately reinvest those proceeds into the exact same security right away. Selling a security and re-purchasing it within the same 30-day window is called a “Wash Sale.” You can avoid triggering the Wash Sale rule by investing in something similar but different enough to avoid having the rule apply.

While most people will tend to do this only once at year end, this is actually something that can be done at any time in the year with no limit as to how frequently you do so. With custom indexing and commission-free trading, frequent tax loss harvesting has become more achievable than ever. In years of high volatility, frequently harvesting tax losses can have a big impact on your tax bill.

Keep in mind that for this strategy to work, you must have capital invested in a taxable, non-retirement brokerage account. Your 401(k) and IRA are not eligible for tax loss harvesting.

How does it benefit you?

In years of extreme volatility, you may be able to accumulate a large amount of tax losses in a short period of time. These losses can then be used to offset future capital gains. If you end up with more tax losses than you have gains to offset them in any given year, you can use the losses to offset up to $3,000 of ordinary income on your tax return.

You will be able to carry forward an unlimited amount of these losses into future tax years until you’ve been able to use them up.

Tax loss harvesting can be especially useful for investors who might have highly concentrated company stock with a large amount of unrealized gains, or other legacy investments that they’ve been holding onto to avoid a large tax impact. These tax losses can be used to help decrease single stock risk and sell off legacy assets with little to no tax impact.

What are the next steps?

If you are a Warren Street client, we are already doing this for you (as applicable). For clients with larger taxable brokerage accounts invested in our custom indexing strategy, you will likely see tax loss harvesting happening on a more frequent basis.

All in all, seeing losses reported on your Form 1099 form is not necessarily a bad thing. While your long term objective remains the same in terms of seeking growth, taking advantage of short term volatility through tax loss harvesting can lead to a nice tax perk that can aid in your overall financial return on investments in the long run.

If you have any questions or would like to speak with one of our advisors for complimentary portfolio review, you can schedule a consultation here.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/09/Blog-Thumbnail.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2022-09-22 08:08:002022-09-22 18:19:31Tax Loss Harvesting: How to Make the Most Out of Market Volatility

Estate planning is one of the most important things you can do to protect your family and your assets. It ensures that your assets and belongings go exactly where you want them and saves your family an immense amount of stress, pain, and cost. Still, estate planning often becomes an afterthought, something that’s a “long way off” or “not a top priority right now.”

The good news is that estate planning isn’t as complicated as it sounds. You can establish the key documents you need with much less effort or investment than you might think. In my 33 years of advising Chevron employees, here are the most common mistakes I’ve seen and the steps you can take to avoid them.

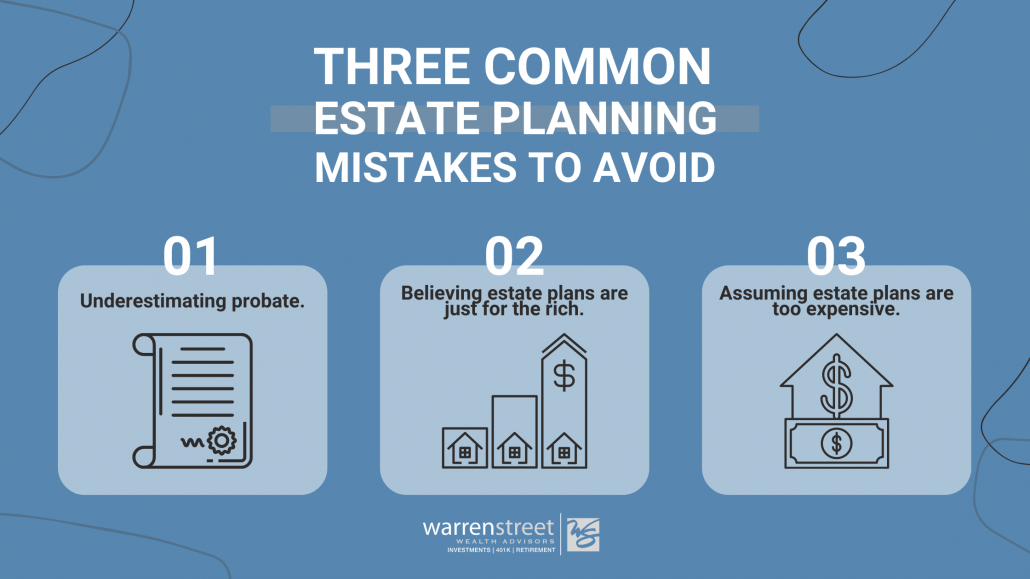

1. Underestimating probate.

Too often, people put off estate planning because they don’t realize the alternative. If you didn’t have key estate documents in place, and something were to happen to you, all of your assets would go to probate. That is basically a simple way of saying the government would decide for you — in a very long, expensive, and public way — what to do with your assets.

I’ve seen probate negatively impact already grieving families who don’t have the bandwidth or money to deal with the probate process. It makes everything much simpler for your surviving family to have all of your documents in place, so they can focus on things that matter instead of the cost and process of dividing up your assets.

2. Believing estate plans are just for the rich.

Estate planning might sound fancy, but estate plans are not just for the wealthy. The six estate planning documents everyone should have include: 1) Will/trust, 2) Durable power of attorney, 3) Beneficiary designations, 4) Letter of intent, 5) Healthcare power of attorney, and 6) Guardianship designations. Beneficiary and guardianship designations are particularly critical for those with minor children, as they allow you to decide who would look after them.

A will or trust should be one of the core components of every estate plan, regardless of the amount of assets. These documents ensure that your assets go exactly where you want them. A durable power of attorney sets whom you would want to make decisions for you if you were unable to (otherwise, it would be up to the courts) — and the same principle applies to the healthcare power of attorney. Your letter of intent streamlines asset distribution and can also include wishes for your funeral. Beneficiary and guardianship designations state your wishes for your children and other beneficiaries.

3. Assuming estate plans are too expensive.

Having your assets go through probate is actually far messier and more expensive than creating an estate plan. How much more expensive? The average cost for probate and attorney fees for a $1MM estate is $46,000. The fee to set up an estate plan, on the other hand, averages just a few thousand dollars. That’s a drop in the bucket compared to probate, not to mention you also save your family time and stress by outlining everything in advance.

Most importantly, an estate plan leaves nothing to chance or guessing. Estate documents make it exceedingly clear whom you would like to take care of your children, get ownership of your house, inherit your money, etc. You can also detail how inheritance should occur (at specific ages, in specific percentages over time, etc.).

For more detail on how to set up your estate plan, join Warren Street and Hunsberger Dunn for a “Will, Trusts, & Estate Planning Webinar”Sept. 27. We’ll break down how to know if you need a living trust, best practices for creating wills and trusts, and more! Estate planning can seem convoluted, but we’re here for you to help make it as streamlined as possible.

–

Have questions about your Chevron retirement plan? Len is an expert in Chevron benefits and would be happy to meet with you. Click here to schedule a complimentary consultation with him.

Len Hanson

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/09/Blog-Thumbnail-1.png10801080Len Hansonhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgLen Hanson2022-09-16 08:30:002022-09-16 08:43:10Chevron Employees: Avoid These Common Estate Planning Mistakes

Market downturns are an expected part of investing, but they can be painful and nerve-racking nonetheless. Investors often want to take action or make changes during these times. Predicting which way the market will move in the short term is nearly impossible; short-term changes usually work against us. Below you will find some actions that you can take during a market pullback that will often yield positive results.

Here are some potential actions to take during a market downturn:

Continue to invest. Market downturns may provide an opportunity to buy into the market at a lower entry point. Consider increasing your savings and investing rate during this time.

Tax loss harvesting. Loss harvesting is a way to turn lemons into lemonade. Loss harvesting allows investors to take advantage of their portfolio losses by realizing the losses and using them to reduce taxable income.

Hold off on large withdrawals. Wait until the market recovers to make larger-than-usual portfolio withdrawals.

Overall financial planning check-up. Now is a good time to take care of any financial planning items that have been lingering on your to-do list. Check your beneficiaries, review your estate documents, and review your insurance coverage. The market is not in your control, so take a minute to review and manage anything that is in your control.

Check your 401(k) allocation and contributions. Make sure you are on track to receive any company matching contributions.

Roth conversions. Roth conversions are case-by-case specific, but generally speaking periods of market volatility may create opportunities for Roth conversions. The idea is to convert funds from a Regular to a Roth IRA while your account value is low, decreasing the amount of tax generated from the conversion. Assuming the market eventually recovers, your newly converted Roth dollars will appreciate tax free (assuming you meet all the other criteria necessary for Roth tax treatment). This scenario works best when you are in a low tax bracket and have the cash to pay tax on the conversion.

Rebalance your portfolio. Rebalancing your portfolio often forces you to sell high and buy low, even during periods of market downturn. By rebalancing during volatility, you are selling the funds that have held up better (typically bonds and other diversifiers), and reinvesting into the areas that have pulled back. This forces you to “buy the dip.” If/when the weaker parts of your portfolio recover, you participate more fully.

Reevaluate your risk level. Market corrections provide an opportunity to increase your risk level (i.e., your stock exposure) and to take advantage of lower stock prices. Typically these periods are not a good time to lower risk by selling stocks unless your goals and/or investment time horizon has changed.

Usually the best action is no action. If you’re not in a position to save more, sticking to your long-term allocation and plan is likely the best way to weather market turbulence. Market corrections will continue to happen over the course of your investing life. While overall the long term trend tends to be upward, corrections will typically happen every few years. During turbulent times, emotional decision-making often works against us.

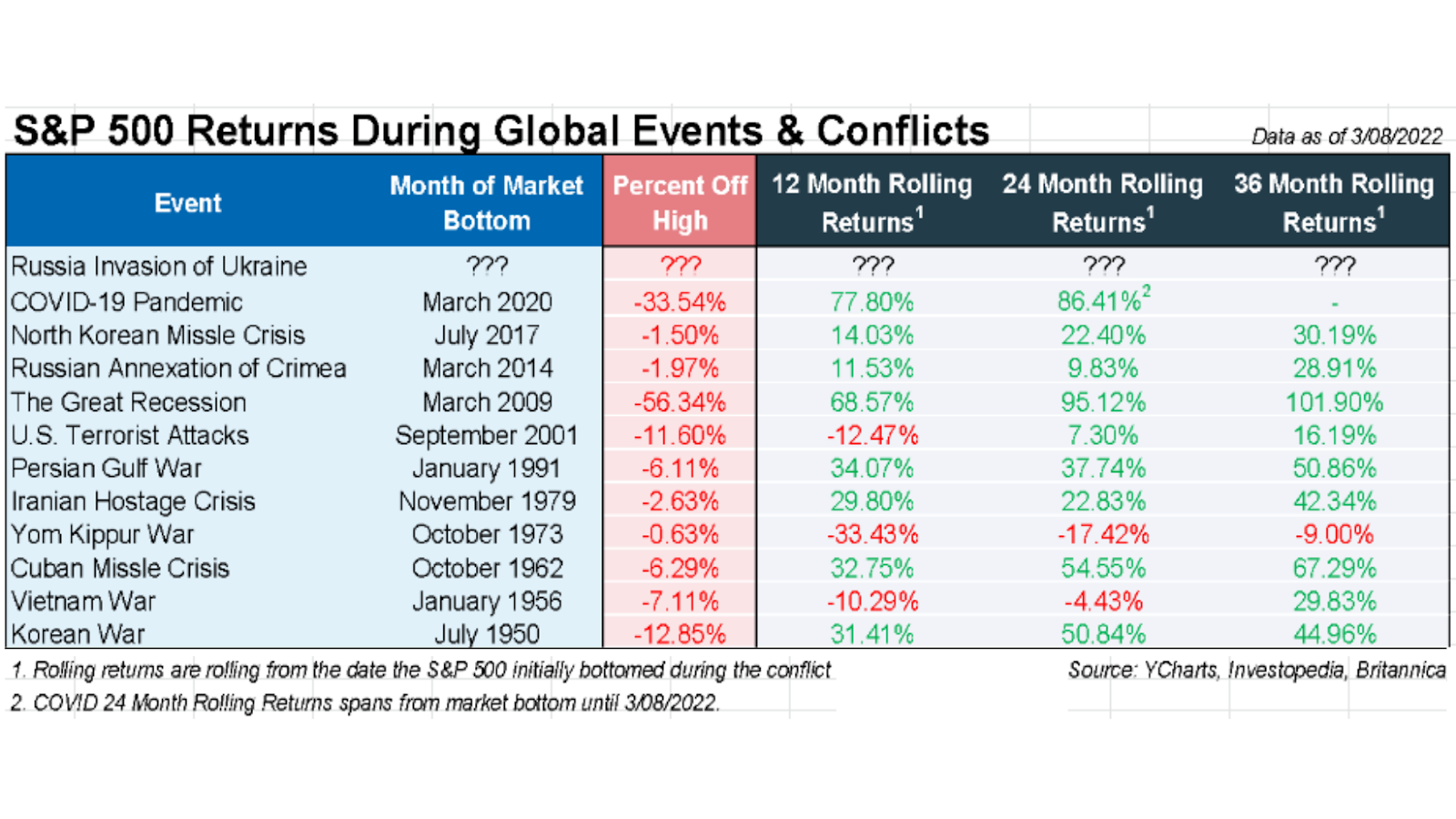

The chart below illustrates how the S&P 500 has performed after a variety of global events and conflicts since 1950. You can see that in most cases, the market has had strong performance in the years following a crisis.

Please feel free to reach out to us if you have any questions. If you would like to speak with one of our advisors for complimentary portfolio review, you can schedule a consultation here.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/08/Action-Market-Blog-Thumbnail.png10801080Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2022-08-09 08:30:002024-11-07 09:29:15Actions to Take in a Market Downturn

Series I bonds offer a low-risk, interest-earning addition to your portfolio. As part of a well-diversified portfolio strategy, now may be a good time to put some additional cash into I bonds and take advantage of an attractive interest rate.

What is a Series I bond?

A Series I bond is issued by the US Treasury. The bond accrues interest monthly until it reaches 30 years or you cash it, whichever comes first.

An I bond has two interest rates – the fixed rate and the inflation rate. These two rates combine to determine a bond owner’s actual rate of return, called the composite rate. A new rate will be set every six months based on the fixed rate and on inflation.

The US Treasury limits the composite rate to no less than 0%, meaning the rate of return on I bonds will never be negative.

What’s the benefit?

The composite rate on Series I bonds is currently 9.62% (annualized). Though the interest rate is variable and will change over time, purchasing I bonds now guarantees that you will earn this interest rate until October 2022 when the new rate is set for the next 6 months.

Are there risks?

An I bond is considered an extremely low risk investment. However, the ultimate rate of return is variable and not guaranteed beyond the current 6-month rate. The current interest rate is high because inflation is higher than usual – if Federal Reserve policy reduces inflation the inflation rate for I bonds will also decrease.

Note that an I bond cannot be redeemed for at least one year after purchase, and any redemption between years 1 and 3 does not receive the interest from the three months prior to redemption.

How do I buy a Series I bond?

Visit treasurydirect.gov to purchase electronic I bonds. An I bond must be purchased directly by the investor; it is not something your advisor can add to your portfolio for you. Series I bonds purchased electronically come in any amount to the penny for $25 or more. Paper I bonds can be purchased using your federal income tax refund. The amount of a bond purchased is limited to $10,000 per person per year.

Are I bonds right for me?

Determining what investments are the best fit for you depends on several factors: your age, the timeline for when you need to withdraw from investments, your comfort with risk, and your overall financial health. If you have some cash that is not part of your basic emergency fund and you do not need it in the next 1-3 years, I bonds may be a good choice. However, as with all investing decisions, we recommend consulting with your financial advisor to determine if I bonds are the best fit for your unique situation.

Kirsten C. Cadden, CFP®

Associate Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/06/Series-I-Bond-Blog-Thumbnail.png10801080Kirsten C. Cadden, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgKirsten C. Cadden, CFP®2022-06-16 08:00:002024-11-07 09:30:00Series I Bonds: Are They Right For You?