Open enrollment is your annual opportunity to review and select your employee benefits for the upcoming year. While it might seem like just another task on your to-do list, the choices you make now can have a significant impact on your health and finances. Don’t simply “roll over” last year’s elections without a review. A proactive approach will ensure your benefits align with your needs and goals.

Analyzing Your Health Insurance Options

Start by assessing your current situation. Think about your health needs from the past year: how many doctor’s visits did you have? What were your prescription costs? Do you anticipate any major life changes, such as getting married or having a baby? These factors will help you choose the right plan.

Understanding Key Terms

Before diving into plan specifics, it’s crucial to understand a few key terms:

Premium: The fixed monthly cost you pay for your insurance plan.

Deductible: The amount you pay out of pocket before your insurance coverage begins.

Copay: A fixed amount you pay for a doctor’s visit or prescription after your deductible is met.

Coinsurance: A percentage of costs you pay for covered services after the deductible is met.

Out-of-Pocket Maximum: The maximum amount you will pay in a year before the plan covers 100% of costs.

Comparing Plan Types: PPO vs. HDHP

The two most common types of health plans are a Preferred Provider Organization (PPO) and a High-Deductible Health Plan (HDHP).

A PPO typically has a lower deductible but higher premiums. It also offers more flexibility for seeing out-of-network doctors. This type of plan is generally best for people who use a lot of medical services, as the costs are more predictable.

An HDHP has a higher deductible but lower premiums. While you’ll pay more upfront for care, this type of plan makes you eligible for a Health Savings Account (HSA). An HDHP is often a great choice for generally healthy individuals or those who can comfortably afford the higher upfront costs if a major health event were to occur.

To help with your decision, compare the total estimated annual cost of each plan. For example, calculate the premiums plus potential out-of-pocket costs for a year with no major health events versus a year with a major surgery. This simple exercise can reveal which plan offers the most financial sense for your situation.

Maximizing Your Tax-Advantaged Accounts

In addition to health insurance, open enrollment is your chance to enroll in or update contributions to valuable tax-advantaged accounts.

Flexible Spending Accounts (FSA)

An FSA allows you to use pre-tax dollars for qualified medical or dependent care expenses, which lowers your taxable income. The key rule to remember is “use it or lose it”—funds typically do not roll over from one year to the next. Carefully estimate your upcoming year’s expenses to avoid forfeiting any money.

Health Savings Accounts (HSA)

An HSA is a powerful financial tool with a triple tax advantage:

Contributions are pre-tax.

Funds grow tax-free.

Withdrawals for qualified medical expenses are tax-free.

Unlike an FSA, an HSA is portable, meaning the account belongs to you even if you change jobs. This makes it an excellent long-term savings tool. After age 65, you can withdraw funds for any reason without penalty, although non-medical withdrawals are subject to income tax. Remember, an HSA is only available if you are enrolled in an HDHP.

Reviewing Other Important Benefits

Don’t stop at health insurance; open enrollment is the perfect time to review your other benefits.

Retirement Contributions

Check your retirement contributions to your 401(k) or 403(b). If your employer offers a matching contribution, be sure you’re contributing at least enough to get the full match—it’s free money! Consider increasing your contribution rate by at least 1% each year. Small, consistent increases can make a huge difference over time.

Life and Disability Insurance

Life Insurance: Review your coverage needs based on your dependents and debts. Your employer may provide basic coverage, but you might need supplemental, voluntary coverage to fully protect your loved ones.

Disability Insurance: This benefit protects your income if you are unable to work due to illness or injury. Review your short-term and long-term disability options to ensure your income is protected.

Final Steps and Action Plan

Making your benefit selections requires a few final steps to ensure you’re fully prepared.

Check Beneficiaries: In case of a major life change like a marriage or divorce, update the beneficiaries on all your accounts (retirement, life insurance) to ensure your assets go to the right people.

Gather Your Information: Have all your plan documents, a list of your regular doctors, and an estimate of last year’s medical expenses ready. This information will help you make a more accurate and informed choice.

Make Your Choices and Submit: Be mindful of the deadline and submit your final selections on time.

By taking the time to review your options and make informed decisions, you can ensure your benefits package is working for you and your financial well-being. Be sure to reach out to your advisor to discuss any of these items in more detail.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-6.png11522048Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-10-02 08:56:462025-10-02 08:56:52Financial Planning for Open Enrollment: A Guide to Making Smart Choices

Retirement is a major life shift, one that impacts more than just your schedule. It can reshape your sense of identity, daily habits and even your health. In fact, research has shown that retirement can raise the risk of heart disease and other medical issues by up to 40%. The reason? Experts point to a loss of purpose and reduced social connection, both of which can take a toll on mental and physical well-being.

Without a plan for how to spend your time meaningfully, the transition can bring unexpected emotional challenges.

The Risks of Unstructured Retirement

Many retirees begin this new chapter with a “honeymoon phase”—a period marked by the novelty of free time, relaxation or long-awaited travel plans. But this initial high can eventually fade.

When the excitement of sleeping in and checking items off the bucket list wears off, retirees can find themselves facing unexpected emotional challenges. Common struggles include boredom, loss of routine, identity shifts and social isolation. In fact, 24% of older adults are considered to be socially isolated. Isolation can also have a ripple effect on health: It’s associated with a 50% increase in risk of developing dementia and increased risk of premature mortality.

Designing a Retirement with Purpose

To avoid some of the potential pitfalls of an unstructured retirement, it’s important to think carefully—and proactively—about purpose. What do you want this next phase of life to look and feel like? Beyond financial planning, consider how you’ll meet the deeper needs your pre-retirement life—including work and raising kids—may have fulfilled: structure, identity, accomplishment, social connection and a sense of meaning.

What brings you pleasure and meaning? What have you always wanted to try or learn? Pursuing these activities can provide purpose and help ensure retirement’s not just a long vacation, but a rewarding chapter of your life.

Feeling stuck here? Try asking close friends or family what they see light you up. Often, others can reflect back passions or strengths that are hard to see on your own.

Staying Connected and Active

Relationships and physical routines matter more than ever when you retire. Staying active, both physically and socially, offers measurable health benefits. Regular physical activity lowers risks, including the likelihood of dementia, heart disease, stroke and eight types of cancer.

People-centered activity is important, too. Look for ways to stay engaged, whether through volunteering, mentoring, part-time work, creative pursuits or community involvement. Older volunteers, aged 55 and up, who gave 100 hours or more each year were two-thirds less likely to report poor health than non-volunteers.

Spending more time with family is a high priority for many retirees and can be a great way to fulfill social needs. But make sure that vision is shared. Open conversations with loved ones about time together, expectations and boundaries can help align plans and avoid disappointment down the road.

The Retirement Identity Shift

In many ways, it’s hard to define what retirement is. After all, it’s not a single moment but a series of transitions. For instance, rather than an abrupt shift to not working at all, you may consider bridge employment—usually part-time work in a temporary position or as a consultant in your field or in a different industry. This can offer a gradual shift into retirement, providing continued income and engagement as you adjust.

As your vision for retirement evolves, keep us in the loop. We’d love to hear what you’re planning—and we’re here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-5.png11522048Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-09-26 07:38:002025-10-07 16:02:46The Power of Purpose in Retirement

As summer winds down, your thoughts may drift toward a final escape. Whether your idea of a perfect getaway is one last trip to a pristine beach, fishing in a mountain lake, or playing the back nine between pickleball matches, many of our clients have come to us over the years with the same question—should I buy a vacation home or just continue to rent?

As financial professionals, our answer is, “It depends.”

Renting a house for a week or two can be less expensive and time-consuming than buying a vacation property. Renting is a short-term commitment, while buying a second home often requires an ongoing investment of time and money. Renting allows you to choose different vacation destinations every year without maintenance and upkeep concerns. However, buyers can decide to rent out the property when they’re not there.

We caution our clients to consider the pros and cons before making decisions. While we aren’t real estate experts, we’ve compiled some information that you may find helpful.

Buying A Vacation Home

Non-Financial Considerations Many financial considerations must be pondered with a vacation property. Will you buy it outright or take out a mortgage? Are you interested in renting it when you’re not there? Will it impact your cash flow? There are also many nonfinancial issues you may want to consider, the most important being how a second home will affect your lifestyle.

Here are a few more aspects to consider before signing on the dotted line:

How Much Time Will You Spend There?1 If you only intend to spend a few weeks a year there, is renting a better choice? The expense and hassle of owning a second home may not be worth it unless you stay a few months each year to enjoy the place. Over time, you can develop friendships and become part of the community, making your second house more of a home.

How Does a Second Home Fit Into Your Travel Patterns?1 By owning a vacation home, you may spend less time traveling to other locations. Consider whether focusing vacation time on one location fits your desired travel patterns. For example, if you believe you’ll be happy spending all your free time in Florida, then buying may be right for you. However, you may feel tied down to one place if you like to travel the world.

Will a Second Home Increase Your Stress?1 Before buying, be aware of the potential stress of owning a second home. Like your primary residence, you’ll need to deal with utilities, maintenance, repairs, and other considerations. While you may find these issues worth the benefits of owning a vacation home, you should enter ownership with your eyes wide open.

Will Purchasing a Vacation Home Enhance Your Experiences and Relationships?1 If your vacation home becomes a hub for family and friends to visit and for you to engage in social activities and adventures with them, owning a second home can increase your happiness. Clients who enjoy their vacation homes the most tend to create memories through experiences with family and friends at their second homes. On the other hand, buying a vacation home primarily as a relaxing retreat may not add much to your overall happiness—despite the weather and scenery.

What Are the Potential Advantages of Buying a Vacation Property2 There are many good reasons to buy a vacation home. After considering the aforementioned nonfinancial factors, it may be the right course of action for you and your family. Here are some potential benefits:

Possible Real Estate Appreciation: One potential advantage to buying a vacation property is that the value of the real estate may increase over time. Of course, there are no guarantees, and your property could lose value.

Renting Costs for Your Vacation: Owning a property in a vacation spot means you won’t need to pay for weekly accommodations.

Perhaps Generate Rental Income: Another benefit to buying a vacation property is the opportunity to generate rental income. If you choose a vacation home in a bustling short-term rental market, you may have the chance to rent out your place when you’re not in town.

Convenience: Owning a vacation home can be more convenient than arranging short-term rentals. It’s also more familiar, comfortable, and allows you to host friends and family.

Retirement: A vacation home can be part of your retirement strategy. Some clients have used their second homes in later life and moved in permanently.

Potential Disadvantages of Buying a Vacation Property

Of course, where there are pros, there are cons. While we don’t want to rain on anyone’s parade, as financial professionals, we strive to provide a fair and balanced view. So, here are some of the potential downsides of buying a vacation property:

Money Management: Buying a property can be costly, especially a second home in an expensive vacation area. In addition to initial costs, there are also ongoing maintenance and other costs. If money is an issue, buying another house may not be your best choice.2

Financing: If you cannot self-finance your purchase, financing a vacation home can be challenging because of different mortgage requirements. A higher credit score and a larger down payment are often required to qualify for a mortgage. So, if you are not paying in cash, expect a more complicated financing experience than purchasing a primary residence.2

Property Management: If you plan to generate rental income when you’re not using your vacation home, you may want to hire a property manager to find renters, collect rent, and clean the place. This could add up to 15% of the rental income.2

Inconsistent Rental Income: Rental income often depends on the season or certain times of the year. There are usually seasonal periods when no one might rent. Vacation property rental income is impacted directly by the destination and its popular times, which can affect income.2

Lack of Disaster Aid: FEMA disaster assistance is limited to your primary home, i.e., where you live for more than six months out of the year. Second homes or vacation homes used as vacation rentals don’t qualify for FEMA assistance. Thus, if hurricanes, wildfires, or floods destroy or damage your second home, you must rely on other options.3

Markets for Luxury Second Homes

While demand for luxury second homes rose during the pandemic, you may think that today’s relatively high interest rates, tight inventory, and uncertain economic environment would’ve damaged the market. They haven’t.4

Despite the numerous challenges hitting residential real estate, the luxury housing market has remained strong. According to The Agency’s 2025 Red Paper, the number of U.S. homes selling for $1 million-plus increased by 5.2% in the first half of 2024, while the median price for high-end properties rose by 14.2%. Compared with the broader market, in which overall home sales fell by 12.9%, the median price increased by just 5% over the same period.4

With more cash on hand and fewer financial constraints, wealthy homebuyers are often less reliant on loans. According to The Agency’s report, homebuyers paid cash for nearly half of all luxury homes sold in the first quarter of 2024.4 So, if you’re in the market for a high-end second home, you’re in good company.

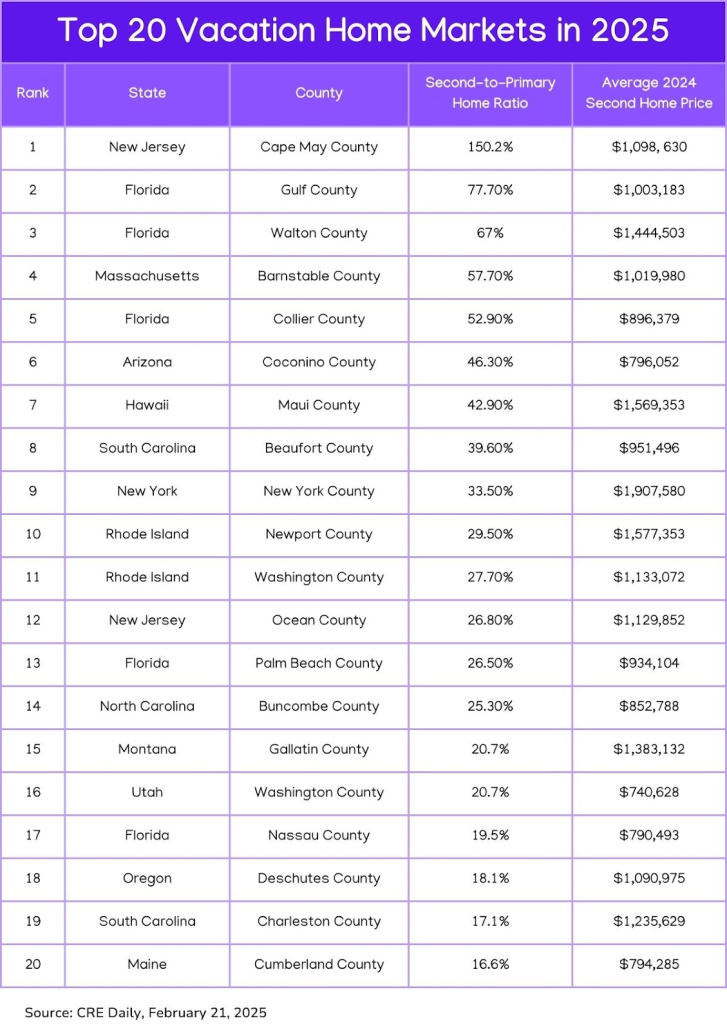

Real estate company Pacaso analyzed the markets with the most significant year-over-year growth in luxury second-home transactions from 2023 to 2024 and average prices for second homes. They believe these second-home destinations could see more growth this year.4

As you’ll see in the chart below, Cape May County, New Jersey, with its Victorian charm and sandy beaches, ranked as the top spot for second home purchases in 2025, with Gulf County, Florida, coming in as a distant runner-up.4

Suppose you’re looking for a second home selling at under $1 million. Washington County, Utah, near Zion National Park; Coconino County, Arizona, near Flagstaff; and Cumberland County in south-central Maine along the coast are popular locations.4

Insurance Considerations for Second Homes

Unless you have the resources to “self-insure,” you might want to consider homeowners insurance to protect your real estate purchase. Second home insurance is a specialized policy designed to cover properties that are not your primary residence. Policies differ because a second home may have additional risks not associated with your primary residence.

Standard homeowners’ insurance for a full-time residence costs an average of $1,754 per year, but you might pay more for a second home insurance policy. For example, American Family estimates that vacation home policies are typically two to three times more expensive than home insurance for a full-time residence.5

The additional risks that cause second home insurance to be higher include:6

Vacancy Periods: Unoccupied homes are more vulnerable to theft or damage.

Location-Based Risks: Coastal or mountainous properties may face specific hazards like hurricanes, floods, or wildfires.

Higher-End Property: If your second home is a luxury property, consider high-value property insurance.

Rental Use: If you rent to others, you may face additional liability concerns, such as tenant-caused damages and liability for injuries sustained by renters or their guests.

Banks will require that your second home be insured if you take out a mortgage. If you are paying cash, the insurance coverage you want, if any, is up to you. If you seek coverage, you should evaluate risks, compare providers, and determine if the policy aligns with your needs and property usage.

Including a Vacation Home in Your Estate

If you buy a vacation home, consider what happens to the property after you’re gone. If a family vacation home is part of your estate, you should put the time and effort into outlining your intentions for the next generation. Your heirs should know what they’re getting and the time, effort, and resources they’ll need to put into the property to keep it functioning well. You know your family’s dynamics and that not all of your heirs will have that same level of interest or involvement in the family vacation home. Thus, be mindful of this and flexible when creating your strategy.7

Consider working with your financial professional and estate team to determine the best way to transfer your vacation home based on your situation. Here are a few choices you may want to evaluate:7

Sell the house outright or gift it to one or more of your children.

Establish a trust in which one or more trustees are responsible for owning and maintaining the property. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional familiar with the relevant rules and regulations.

Form an LLC or other legal entity where your heirs will be owners and follow specific governance rules and operating agreements in how the property is used.

As financial professionals, we can offer insights into how your vacation house may contribute to your overall estate strategy.

Tax Implications of Owning a Second Home

As we mentioned before, we’re not tax experts, but we work with people who are. We’re outlining some general information, but it’s not a replacement for real-life advice. Consult your tax, legal, and accounting professionals for more specifics regarding your second home.

If your second home is a residential home, you may be able to deduct mortgage interest up to $750,000 as long as the second home is the one that secures the loan. If your mortgage on your second home originated before Dec. 16, 2017, you can deduct up to $1 million in mortgage interest. You also can deduct state and local property taxes––up to $10,000 combined for all real estate taxes between your homes.8

If you rent your property for 14 days or less during the year, you may not need to report this as income to the IRS.8

If you rent your second home for more than 14 days a year, the IRS considers it an investment property. If your second home is an investment property, you might be able to deduct mortgage interest or real estate taxes on your personal income tax return. Still, you may be able to deduct those costs against your rental business income.8

When you sell your second home, you must be aware that you may not receive the same capital gains tax deduction when selling your primary residence – $250,000 for single filers and $500,000 for married.8

Renting a Vacation Home

If you have gone through all the pros and cons of buying a vacation home and are leaning toward renting, this approach also has two sides. Let’s start with the positives.

Potential advantages of renting a vacation home2

Little Responsibility: If you choose to rent a vacation home, your only responsibility is to leave the house the same way you found it. None of the property maintenance or utilities fall onto a short-term renter to take care of, which means you can enjoy your holiday and then dump your garbage on the way out, turn out the lights, and lock the door behind you.

Variety of Options: Renting vacation homes means renting a different home anywhere you go. You won’t be limited to revisiting the same place over and over. Instead, you can change locations each time you go on vacation and experiment with the type of property to see what you enjoy best – in town or out, kid-friendly or over 55, nightlife or peace and quiet, etc.

Cost Considerations: Renting a vacation home can be a more affordable way to go on various vacations in many areas. After all, you will not pay a mortgage, maintenance fees, or other charges.

Disadvantages of Renting a Vacation Home

Anyone who has rented a vacation home knows that there are some downsides. Here are a few of them:

Cost: In 2024, the expected average daily rate for U.S. vacation rentals is $326.9 This number will fluctuate based on the type of home you rent. A luxury rental could be significantly higher.

Not Your Space: When renting a vacation property, you live in someone else’s home. For many people, it’s never as comfortable as staying in a place you own. You may find problems with the house, it may not have all the features you are accustomed to, and you may need a learning curve to figure out how to use everything from the TV to the thermostat.2

Availability: You may need to book your vacation homes well in advance during peak seasons. Chances are you want to go away at the same time of year, but others have the same idea. Availability can be problematic if you book too late or the area is extremely popular.2

Inconvenient: Renting a vacation home can be a hassle. You have to choose the home, make sure it’s available when you want, and then go through the booking process with the owner, the property manager, or a third-party website. If anything accidentally breaks during your stay, you’ll also be liable to cover it. There can also be unexpected fees that drive up the price.2

Make Your Decision Carefully

I’m sure you’ve gone on vacation to a terrific location and fallen in love with it. The experience might have been so wonderful that you thought about buying a home to spend more time there. That’s how the time-share industry became so popular in the 1970s and 80s—catering to impulse buyers.

However, it’s important to remember that while you might be swayed by the most enjoyable aspects of your vacation, you should consider the negative factors that owning a second home can bring. Between costs, extra work of taking care of another property, and the impact on your other travel habits, owning a vacation home can have drawbacks. You also may want to factor in how being away could impact your relationships back home.

Before you commit to buying a vacation property, you might want to consider living there for a month or two first. Spending an extended amount of time in a rental property at your intended vacation home location may provide you with a more realistic view of the area.

There is no right or wrong answer on whether to buy or rent a vacation home. Please take the time to weigh the pros and cons thoroughly before deciding. Please do not hesitate to contact us if we can help or just be an impartial sounding board.

Veronica Cabral

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/Buy-vs-Rent.png10801080Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2025-09-04 10:39:142025-09-04 10:39:19Is It Smarter to Buy or Rent a Second Home?

The earlier you start investing, the better. You’ve likely heard this advice before, and hopefully it’s helped you make some smart financial moves. But there’s one group that may not yet know this bit of investing wisdom: the kids in your life.

Whether you have kids, grandkids, or nieces and nephews, these youngsters have an enormous asset on their side: time. Helping them get an early start with investing can give them a huge financial boost. The good news is that there are a lot of ways you can help set up the next generation for financial success. Let’s explore some options.

529 Plans: A Great Tool for Future Education Costs

With rising education costs, 529 plans are often the first type of investment account that parents open for their children. It makes sense. They’re one of the best tools available for long-term education savings.

You probably already know the main benefits: tax-deferred investment growth, tax-free withdrawals for qualified education expenses and no federal contribution limits (though gift tax may apply beyond annual contributions of $19,000 for 2025). Friends and family can contribute, and funds can be used for a growing range of expenses: college, of course, but also up to $10,000 per year for K–12 tuition. And excess funds can be rolled over to another family member, used to pay for grad school or even used to pay off student loans.

Custodial Accounts: More Flexibility but Less Control

But what if you want to help your child invest toward future expenses not covered by a 529 plan, like car repairs, travel or the down payment on a house? That’s where custodial accounts might be appropriate. UGMA (Uniform Gifts to Minors Act) and UTMA (Uniform Transfers to Minors Act) accounts are typically easier to set up than a trust and can accomplish some of the same goals.

Custodial accounts let you invest in a variety of assets in a child’s name, including stocks, bonds, mutual funds and even real estate. UTMA accounts also let you hold complex assets like art and intellectual property. There are no contribution limits, and the funds can be used for anything that benefits the child while they’re still a minor. However, your child takes complete control over the account when they reach adulthood (usually age 18–21, depending on the state). At that point, they can use the funds for any purpose.

Note that investment earnings may be subject to the so-called kiddie tax. For 2025, that means the first $1,350 of unearned income is tax-free, the next $1,350 is taxed at the child’s marginal rate, and anything above that may be taxed at the parent’s marginal tax rate. Another word of caution: Custodial accounts are considered the child’s asset, which may impact financial aid eligibility more than a 529 plan would.

Roth IRAs: Even Kids Can Start Saving for Retirement

If you’re thinking even longer-term, you can help your kids start saving for retirement by opening a custodial Roth IRA on their behalf. Roth IRAs allow them to enjoy decades of tax-free investment growth and tax-free withdrawals in retirement.

To fund any IRA, the child must have earned income—such as from babysitting gigs or slinging ice cream over the summer. Those contributions cannot exceed their total earnings or the $7,000 annual limit (for 2025), whichever is lower. Then, once the child reaches adulthood (usually 18–21, depending on the state), they can transfer those savings to a new account to keep building a bright financial future.

One of the best financial gifts you can give a child isn’t just money—it’s knowledge. And opening an investment account is an opportunity to introduce your family to some of the most important concepts in personal finance.

You can start by talking to your kids about budgeting, saving and what it means to invest. Review account statements with them to highlight the power of compounding and the benefits of tax deferral. Use the target-date portfolios in a 529 plan to teach your kids about the value of diversification. Bring them into decisions when picking investments for a custodial account or Roth IRA. It’s a great chance to discuss the long-term advantages of choosing broader market exposure over trying to pick single stocks.

The earlier a child understands how money and investing works, the better their odds for achieving long-term financial goals. We’re here to help you give them that head start—whether it’s setting up accounts, discussing financial strategies or sharing more ideas for teaching kids about money.

Veronica Cabral

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/08/Kid-Investing.png10801080Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2025-08-04 07:25:582025-10-07 16:08:58How Can I Give My Kids a Head Start on Investing?

The “One Big Beautiful Bill Act” (OBBBA), signed July 4, 2025, is poised to significantly impact nearly every aspect of your financial life. From your tax bill to your healthcare and your children’s future savings, understanding the nuances of this bill is crucial for effective financial planning.

Here’s a breakdown of what the OBBB means for you:

Tax Planning: More in Your Pocket, But Mind the Details

The OBBB makes permanent many of the individual income tax rates and brackets from the 2017 Tax Cuts and Jobs Act (TCJA), providing long-term clarity. But there’s more:

Expanded Standard Deduction: The standard deduction sees a permanent expansion, making tax filing simpler for many and potentially reducing the need to itemize.

Temporary Deductions (2025-2028): Get ready for some new, but temporary, tax breaks.

No Tax on Tips/Overtime: If you earn qualified tip income (up to $25,000) or overtime premium pay (up to $12,500 for individuals, $25,000 for joint filers), you may be able to deduct it. Keep an eye on income phase-outs.

Senior Tax Deduction: Individuals 65 and older meeting income thresholds ($75,000 single, $150,000 joint) can claim an additional $6,000 deduction, aiming to offset federal taxes on Social Security.

Auto Loan Interest Deduction: A temporary deduction of up to $10,000 for interest on loans for U.S.-assembled vehicles is available, subject to income phase-outs.

Increased SALT Deduction Cap: For five years, the State and Local Tax (SALT) deduction cap temporarily increases to $40,000 (from $10,000), with income-based phase-outs. This is a win for residents of high-tax states.

Enhanced Child Tax Credit: The Child Tax Credit permanently increases to $2,200 per child and will be indexed for inflation.

Business Tax Incentives: Businesses will see the reinstatement of 100% bonus depreciation and permanent Section 199A (Qualified Business Income) deduction, encouraging investment.

Estate and Gift Tax Relief: The unified credit and Generation-Skipping Transfer Tax (GSTT) exemption thresholds are permanently increased to $15 million per individual, offering substantial relief for high-net-worth individuals.

Your Action Plan: Review your current tax strategies with a financial advisor to maximize these new permanent and temporary provisions. Consider whether itemizing still makes sense for you.

Healthcare & Social Programs: A Shifting Landscape

The OBBB includes significant cuts to federal funding for vital social programs:

Medicaid Changes: Expect cuts to Medicaid funding and new work requirements for many adult beneficiaries. If you or your loved ones rely on Medicaid, be aware of potential reduced coverage or new eligibility hurdles.

SNAP (Food Assistance) Adjustments: The Supplemental Nutrition Assistance Program (SNAP) also faces federal funding cuts and expanded work requirements.

Affordable Care Act (ACA) Implications: New eligibility verification requirements are imposed for ACA marketplace coverage, and enhanced tax credits for ACA coverage are set to expire. This could lead to higher out-of-pocket premium payments for many, particularly older adults. The CBO estimates these changes could lead to a significant increase in the uninsured population.

Your Action Plan: Reassess your healthcare and benefits planning. Explore alternative options if you’re impacted by changes to Medicaid or ACA, and adjust your budget accordingly.

Retirement & Savings: New Avenues and Program Shifts

The bill introduces both opportunities and challenges for your long-term financial goals:

“Trump Accounts” for Children: A brand-new savings option for newborns. These “Trump Accounts” receive an initial federal contribution of $1,000, with parents able to contribute up to $5,000 annually. Classified as IRAs, gains are tax-deferred until age 18. This is a new consideration for long-term savings for your children.

Student Loan Program Overhaul: Federal student loan programs are undergoing significant alterations, potentially ending subsidized and income-driven repayment options. Limits are also placed on Pell Grant eligibility. Current and future students will need to adjust their education financial planning.

HSA and 529 Expansion: Good news for healthcare and education savings. Eligible uses for Health Savings Accounts (HSAs) and 529 education savings plans are expanded, offering more flexibility.

Social Security Outlook: While the bill provides some temporary tax relief for seniors, its overall impact on the national debt could accelerate the insolvency of Social Security. This is a long-term consideration for retirement planning.

Your Action Plan: Evaluate “Trump Accounts” alongside existing savings vehicles like 529 plans. If you have student loans or are planning for higher education, understand the new repayment and eligibility rules. Review how you leverage your HSA and 529 plans for maximum benefit.

Investment & Business Considerations: Adapting to Policy Shifts

The OBBB also brings changes that could influence your investment portfolio:

Clean Energy Tax Credits: Many clean energy tax credits from the Inflation Reduction Act are being phased out, which may impact investments in renewable energy and electric vehicles.

Fossil Fuel Promotion: The bill promotes increased domestic oil and gas production, which could influence investment strategies in the energy sector.

Your Action Plan: Consider how these policy shifts might affect your investment portfolio. Diversification and a long-term perspective remain key.

Overall Financial Planning Implications: A Holistic Approach

The “Big Beautiful Bill” is a game-changer. It necessitates a comprehensive review of your financial strategy.

Review Tax Strategies: Don’t miss out on new deductions!

Reassess Healthcare and Benefits Planning: Understand potential impacts on coverage and eligibility.

Evaluate Savings Options: Explore new opportunities like “Trump Accounts” and expanded HSA/529 uses.

Update Estate Plans: High-net-worth individuals should revisit their estate plans due to increased exemptions.

Adjust Investment Portfolios: Align your investments with the new economic realities. If you’re a client of ours, we’ve already done this for you.

The “One Big Beautiful Bill” is far-reaching. Given its complexity, consulting with a qualified financial advisor and tax professional is highly recommended to understand how these provisions specifically impact your unique financial situation and to adjust your plans accordingly. Schedule time with a Warren Street advisor today. .

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/07/Big-Beautiful-Bill.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-07-10 12:14:072025-07-10 12:15:13The “Big Beautiful Bill”: What It Means for Your Finances

Summer break is here, and many young people will be working at a summer job or internship. While earning a paycheck is exciting, it can also be an excellent time to consider opening a Roth IRA and contributing a portion of their summer earnings. Not only does this jump-start retirement savings from an early age, but it can also serve as a positive learning experience about the principles of saving, investing, and cultivating long-term wealth.

The Roth IRA offers a unique combination of tax advantages and flexibility, making it an excellent choice for young savers.

Here are a few key benefits:

Tax-free growth: Roth IRA contributions are made with after-tax dollars, so your child won’t pay taxes (and perhaps penalties) until they make withdrawals.

Penalty-free withdrawals of contributions at any time: Your child can withdraw up to the amount of their total contributions at any time, for any reason, without paying taxes or penalties.

Early withdrawals of earnings: If your child withdraws amounts that exceed their contributions before age 59½ or before the account has been open for five years, they may face taxes and a 10% early withdrawal penalty on the earnings portion of the withdrawal.

Exceptions to early withdrawal penalties: Your child can withdraw funds before age 59½ or before the account has been open for five years for several reasons (keep in mind that you may be able to avoid penalties but not taxes on any earnings), including:

Funds can be used for qualified higher education expenses. 🎓

First-time home purchase (up to a $ 10,000 lifetime limit.)

If your child becomes disabled. ♿

For certain emergency expenses. 🏥

If your child is unemployed, they can use a withdrawal to help pay for health insurance premiums. 🩺

The flexibility and withdrawal choices for a Roth IRA can make it an attractive choice for young savers who may need access to their money in the future while still providing a powerful tool for long-term wealth building.

Keep in mind that with a Roth IRA, to qualify for the tax and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be made under certain other circumstances, such as in the examples we listed above. The original Roth IRA owner is not required to take minimum annual withdrawals.

Eligibility requirements

To contribute to a Roth IRA, your child must have earned income from a job, and the maximum contribution for 2024 is $7,000 or the total of their earned income, whichever is less. You can open and manage the account until they reach the age of majority in your state.

One more thing: They may need help filling out their Form W-4

If your child makes less than $14,600 in 2024, they may want to claim an exemption from withholding on their W-4 form by writing “Exempt” on line 4(c) of the form.

Here’s why:

Standard deduction: For the 2024 tax year, the standard deduction for a single filer is $14,600. If your child’s total income for the year is less than this amount, they won’t owe any federal income tax.

Claiming exemption: If your child expects to owe no federal income tax for the year and wants to have no tax withheld from their paycheck, they can write “Exempt” on line 4(c) of Form W-4. This means their employer won’t withhold any federal income tax from their paychecks.

Remember that if your child claims exemption, Social Security and Medicare taxes may still be withheld from their paychecks. Also, if their situation changes and they owe federal income tax for the year, they may face underpayment penalties.

Our ideas in this letter are for informational purposes only and are not a replacement for real-life advice. Consider consulting your tax, legal, and accounting professionals if you have questions about completing Form W-4.

If you’d like to discuss opening a Roth IRA for your child or grandchild, feel free to contact us. And feel free to share this with anyone you think might be interested.

Wishing you and your family a wonderful start to the summer!

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/06/Kick-start-Your-Childs-Financial-Journey-with-Roth-IRAs.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2025-06-23 10:09:592025-06-23 10:20:44Kick-start Your Child’s Financial Journey with Roth IRAs

Watching your child earn a college diploma is a proud moment for any parent. It also marks another great moment: No more tuition bills. But after all the saving and planning you’ve done, what if there’s still money left over in your child’s 529 plan? Fortunately, you’ve got plenty of options. Here’s a list of strategies to make the most of those surplus education savings.

Keep Paying for School

If your newly minted graduate is pursuing a higher degree, that’s an easy way to spend down the balance in their 529 plan. These funds can be used to cover the same types of qualified educational expenses for graduate programs.

Name a New Beneficiary

If grad school isn’t in your child’s future, the most straightforward option for surplus funds is to assign the 529 account to a new beneficiary. You can change beneficiaries with no penalties or tax consequences, but the person must be related to the original beneficiary by blood, marriage, or adoption. That definition is broader than it sounds: For example, it includes in-laws, first cousins, first cousins’ spouses, and stepparents. You can even name yourself as the new beneficiary and spend the funds on your own continued education.

Repay Student Loans

If your graduate has taken on student loan debt, you can use 529 funds to help pay it down, subject to a lifetime limit of $10,000. You can also use up to $10,000 per sibling to repay their loans, which you can do without changing the beneficiary.

A few things to bear in mind: Most, but not all, student loans qualify. Private student loans must meet several criteria to be included in the program. For example, they must have been used solely for qualified education expenses for a degree or certificate program at an institution eligible for Title IV federal student aid. And they can’t be personal loans from a family member or a loan from a retirement plan.

Also, 529 plans are run by states, and their rules don’t always align perfectly with federal legislation. We can help you check your 529 to see whether withdrawals for student loan payments will trigger any state tax penalties.

Roll Over Funds Into a Roth IRA

The SECURE 2.0 Act of 2022 added a brand-new option for unused 529 funds. If your 529 plan is at least 15 years old, you can transfer up to $35,000 into a Roth IRA in the beneficiary’s name with no taxes or penalties.

The biggest limitation with this option is that rollovers are subject to the annual $7,000 Roth contribution limit. (If the beneficiary is 50 or older, that amount rises to $8,000.) You also can’t roll over more than the income earned by the beneficiary in that tax year. Any other contributions made to your beneficiary’s traditional or Roth IRA will reduce the amount you can roll over that year.

Take the Money…and the Penalty

If you spend 529 funds on nonqualified expenses, you’ll be charged federal income tax and a 10% penalty on the earnings portion of your withdrawal. While doing so isn’t always ideal, it is an option—and sometimes, it may be the best one. For example, if you face a pressing financial need and your only other choice is to take on high-interest debt, paying the taxes and penalties on a nonqualified 529 withdrawal may be less expensive in the long run.

It’s also possible that the earnings portion is small enough to render the penalty insignificant. Let’s say you had $500 dollars left in the account, with contributions accounting for $420. In that case, only $80 would be subject to taxes and penalties. You might decide it’s worth taking the hit to be able to close the account and move on.

The bottom line is that 529 college savings plans have more flexibility than you might think. Reach out, and we will gladly help you weigh all the options for leftover funds. Congratulations to all the recent grads out there—and to the parents who helped foot their tuition bills.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/06/529-Plans.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2025-06-17 07:35:002025-11-17 09:13:48What to Do With a 529 Balance

Statistics show that nearly 33% of Americans have faced some identity theft attempts in their lives, and experts estimate there is a new case of identity theft every 22 seconds. As financial professionals, one of our primary goals is to help our clients create a financial strategy and protect their wealth. In today’s digital age, identity theft threatens your finances, so it’s crucial to understand the risks and take proactive measures.1

This blog aims to equip you with practical strategies for protecting your personal and financial information with the goal of maintaining your financial well-being.

The most common types of identity theft are1:

Credit card fraud

Government documents or benefits fraud

Loan or lease fraud

How Identity Theft Impacts Your Finances

The financial hardships caused by identity theft can last for months or even years after your personal information is exposed. Depending on the type of data identity thieves obtain, the recovery process can involve several hurdles. Victims often need to dispute fraudulent activities in their credit files and work to restore their good credit. This may include cleaning up and making changes to compromised bank accounts.2

If an identity thief uses your Social Security number to obtain employment, you may need to work with the Social Security Administration. Similarly, if you become a victim of tax refund identity theft or an identity thief’s income makes it appear you are under-reporting your income, you may need to work with the IRS.2

Identity theft involving sensitive, personally identifiable information like your Social Security number can have long-lasting effects. Thieves may wait months or even years to use your information, or they might sell it on the dark web, requiring you to stay vigilant indefinitely. Legal fees and other costs could add to the financial impact if your identity theft issue is complex. Some victims even need to seek government assistance during recovery, highlighting the potential magnitude of identity theft hardships.2

Steps You Can Take to Help Protect Yourself

It can be difficult for victims to deal with identity security issues because bad actors are becoming more sophisticated all the time. You can use technology-enabled safeguards to help protect your identity and personal data, such as antivirus protection software, password managers, identity theft protection, virtual personal networks, and two-factor authentication on devices and accounts. There are also other actions you can take to help manage the risk of becoming a victim, including:

1. Check your mail often.

A low-tech way criminals can steal your identity is to simply take bank or credit card statements, utility bills, health care or tax forms, or pre-approved credit card offers out of your mailbox. So, don’t let your mail sit uncollected too long. Also, if you are going away, have a trusted neighbor bring in your mail or put your mail on hold with the post office.3

2. Review credit card and bank statements regularly.

By reviewing your credit card and bank statements, you may be able to spot any suspicious activity. Thieves with your credit card number or bank account information could make small purchases to see if they can get away with it. These transactions can go unnoticed. Thieves may try to make large purchases if they get away with minor ones.3

3. Freeze your credit.

In some cases, you may want to consider freezing your credit file so no one can look at or request your credit report. That means no one can open an account, apply for a loan, or get a new credit card while your credit is frozen. Remember, a credit freeze applies to you as well. To get started, contact each of the three major credit reporting agencies. In some instances, credit freezes are free and won’t impact your credit score.3

4. Don’t use the same password twice.

According to the Federal Trade Commission (FTC), secure passwords are longer, more complex, and unique. Many people use the same password for multiple accounts, which could be problematic. You should consider creating different passwords for various accounts and avoid using information related to your identity, such as the last four digits of your Social Security number, your birthday, your initials, or parts of your name.3

The FBI and the National Institute of Standards and Technology have issued guidelines stating that passwords should consist of at least 15 characters because these are more difficult for a computer program or hacker to crack. Regarding security questions, the FTC’s guidelines suggest questions that only you can answer; avoid information that could be available online, such as your ZIP code, city of birth, or mother’s maiden name.3

5. Consider shredding documents with personal information.

As stated earlier, not all identity theft is high-tech. Old-fashioned dumpster diving might sound like a thing of the past, but it still happens. Consider buying a household shredder and destroying sensitive paperwork, such as credit card and bank statements, utility bills, and other documents containing personally identifiable information.3

6. Opt out of prescreened credit card offers.

Credit card companies often send prescreened offers to open new accounts, and criminals can intercept these mailed or emailed offers and open accounts in your name. One way to help avoid a potential identity theft issue is to opt out of receiving these offers.2

Day-to-Day Security Best Practices

Small steps can make a big difference when it comes to keeping your information safe. Here are a few suggestions, starting with cleaning out your wallet.

1. Keep your Social Security card at home in a safe location—not in your wallet.

Those nine digits can help an identity thief to obtain loans or credit card accounts in your name. A bad actor could also use your Social Security number with the IRS.

2. Leave checks and deposit slips at home.

Consider leaving checks and deposit slips at home. These items may contain more information than you think, including your name, address, bank name, routing number, and account number.

3. Shred and trash any password cheat sheets.

Scraps of paper with sensitive information, such as PINs and passwords, can be risky, so dispose of any you have in your wallet after noting them in a password manager at home

4. Limit the number of credit cards in your wallet.

It may be best to limit the number of credit cards in your wallet. The same goes for excess cash and gift cards.

5. Bypass the PIN at the gas pump.5

One of the most common schemes is when criminals install a skimming device directly over the credit card slot at a gas pump. These skimmers capture and store your card data when you insert or swipe your card. If something looks off, don’t use that pump. Also, if you use a debit card to pay for your gas, bypass the PIN if possible and use your zip code instead. That may prevent someone from stealing your PIN using a pinhole camera.

Dispose of Old Devices Safely

Improper disposal of old digital devices is a key but often overlooked aspect of identity theft. Simply deleting files may not be enough on some digital devices, as thieves may be able to recover the data. Therefore, safe disposal is critical. Many communities have secure electronics recycling events where devices can be disposed of. However, it’s important to note that different devices and storage media types may require different disposal methods.

Identity Theft Protection Services

Identity theft protection services offer a range of features designed to detect identity theft, alert you to identity theft, and help you recover from identity theft. These services typically monitor credit reports, dark web activity, and public records for signs of fraudulent use of personal information. When suspicious activity is detected, they alert the user and provide next steps. While these services can be helpful, their effectiveness can vary. However, these services can be a valuable first step for those who lack the time or expertise to monitor their credit and personal information.

What to Do if Your Identity Has Been Stolen

You may not know that you have been a victim of identity theft immediately when it happens, but there are warning signs you can look out for, such as:6

Bills for items you did not buy

Debt collection calls for accounts you did not open

Information on your credit report for accounts you did not open

Denials of loan applications

Mail stops coming to or is missing from your mailbox

If you are a victim of identity theft, you may want to place fraud alerts or security freezes on your credit reports. A fraud alert requires creditors to verify your identity before opening a new account, issuing an additional card, or increasing the credit limit on an existing account based on a consumer’s request.

Pro tip: When you place a fraud alert on your credit report at one of the nationwide credit reporting companies, it must notify the others.7

Protecting your identity is an integral part of maintaining your overall financial health. As financial professionals, we believe safeguarding your personal information can be as crucial as making sound investment decisions. By implementing these preventive measures and staying vigilant, you can help manage the risk of becoming a victim of identity theft. Remember, your financial security encompasses every aspect of your financial life.

If you have any concerns about identity theft or would like to discuss how it fits into your broader financial strategy, don’t hesitate to contact us. We’re here to help provide you with information that can help improve your personal finances.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

This blog is for informational purposes only and is not a replacement for real-life advice. We encourage you to consult your tax, legal, and accounting professionals if you believe identity theft involves using your tax records.2

What should you do if you’ve just received a big bonus at work, inherited some money, sold a business, or come into a financial windfall? Should you invest it all at once, even if the market feels high or low, or take a gradual approach by investing in smaller increments over time?

This is a common question we hear from clients and investors alike. It’s no surprise—deciding how to invest a significant sum of money can feel overwhelming. What if you invest it now and the market drops? Or, what if you wait and the market takes off? It’s natural to worry about making the wrong choice or missing out on potential gains.

Both investing a lump sum immediately and spreading it out over time come with their pros and cons. Let’s explore some key factors to help guide your decision.

Start with Your Goals

Before making any investment decisions, consider your financial goals.

If you need the money for short-term purposes, like upcoming college tuition, the market’s volatility could be a concern. In this case, conservative options like short-term bonds, bond funds, or CDs might be better suited to protect your funds.

For long-term goals, such as retirement, investing in the stock market may be a better choice. Despite short-term fluctuations, the market has historically trended upward over time.

Compare Lump-Sum Investing vs. Dollar-Cost Averaging

Investing a lump sum means your money is fully exposed to the market immediately, allowing you to benefit from any immediate gains if the market is rising. However, since markets are unpredictable, a downturn could occur soon after you invest.

If the risk of short-term losses makes you uneasy, dollar-cost averaging (DCA)—where you invest a fixed amount at regular intervals—might be a more comfortable approach. For instance, you could invest $12,000 by putting in $1,000 monthly over a year. This way, you buy more shares when prices are low and fewer when they’re high, helping you manage the average cost over time.

Keep in mind, though, that research shows lump-sum investing outperforms DCA 68% of the time. If maximizing returns is your main goal, lump-sum investing could be the better option. However, if you’re worried about losses and potential emotional reactions, DCA may be worth the slight reduction in expected returns.

Don’t Wait to Invest

Historically, stocks and bonds outperform cash over the long term, so it’s important to start investing as soon as possible. Holding off is essentially an attempt to time the market, which is notoriously difficult. In 2023, equity fund investor returns trailed the S&P 500 by 5.5%, largely due to market timing efforts.

Both lump-sum investing and DCA help you avoid this pitfall, letting you benefit from the market’s long-term growth. The key is choosing the strategy that aligns with your risk tolerance and long-term plan.

If you’re unsure which strategy is best for you, reach out—we’d be happy to help you decide.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/04/Lump-Sum.png12602240Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-04-17 07:16:422025-04-17 07:19:16I’ve Got a Lump Sum in Cash, Should I Invest It Right Away?

Tax season isn’t the most joyful time of year, but it’s certainly one of the most important. With the filing deadline fast approaching, here’s a rundown of the latest tax updates to help you maximize deductions, avoid penalties and keep more of your hard-earned money. Plus, we’re keeping an eye on the big tax changes that might be passed down in Washington later this year.

A couple of quick notes before we dive in. If you tend to file your own taxes, you may be able to file for free, thanks to the expansion of the IRS Direct File program. Previously a pilot program, it’s now available in 25 states, giving more people access to an easy and cost-free way to submit their returns. Check the website to see if you are eligible.

Note: There’s been a bit of confusion about the Direct File program with the head of the new Department of Government Efficiency, Elon Musk, posting on social media that it had been “deleted.” However, as of now, the website is still live.

More taxpayers are facing IRS penalties for underpayment, often due to freelance income where taxes aren’t automatically withheld. If you’re facing a penalty for underpayment, take the opportunity this tax season to adjust your withholding on W-4 forms if you’ve underpaid. If you earn income outside of an employer, make a plan to get those estimated payments in on time.

Inflation-Adjusted Tax Changes

Some things in life are certain: death, taxes … and annual adjustments due to inflation. The IRS has once again made incremental shifts to income thresholds for tax brackets. You may find yourself in a different bracket this year, potentially changing how much you pay in income and capital gains taxes.

The standard deduction has also gone up, making it even more attractive for most filers to skip itemizing and opt for the automatic deduction:

$14,600 for single filers and those married filing separately

$21,900 for heads of household

$29,200 for married couples filing jointly

Additional deductions apply for seniors (65+), with $1,550 extra per person for joint filers and $1,950 extra for single filers

IRA contribution limits: $7,000, with an additional $1,000 catch-up contribution for those 50+

401(k) contribution limits: $23,000, with a $7,500 catch-up contribution for those 50+

While 401(k) contributions for 2024 are closed (unless you are self-employed), you can still make 2024 contributions to an IRA until April 15, 2025. And if you’re thinking long-term, now’s a great time to kickstart your 2025 contributions.

Health Savings Accounts (HSAs)

For those enrolled in a high-deductible health plan (HDHP), HSAs remain one of the best ways to save on taxes while covering medical expenses. Contribution limits have increased to $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up for those 55+.

Gift and Estate Tax Exemptions

If you’re planning to pass on wealth to loved ones, here’s what you should know:

The annual gift tax exclusion is $18,000 per recipient in 2024, increasing to $19,000 in 2025.

While it’s too late to make a tax-free gift for 2024, major changes could be coming in 2026 when current exemptions are set to expire.

Bought an EV? Don’t Forget to Report It

Electric vehicles are becoming increasingly popular. In fact, the number of EVs on the road rose more than 65% in 2024. Government incentives are a key factor driving adoption, including up to $7,500 in tax credits buyers may take right at the dealership. If you were one of them, the IRS requires that you prove eligibility for this discount by reporting your purchase on your tax returns. To do so, you’ll need to file Form 8936, Clean Vehicle Credits, and provide your vehicle’s VIN.

Selling Online? Expect a 1099-K

Gig sellers and casual resellers, beware of IRS reporting obligations. If you sold goods online in 2024 on platforms like eBay, StubHub, or Etsy, you may receive a 1099-K tax form if your sales exceeded $5,000. Previously, the threshold to receive a 1099-K was $20,000, but that threshold is dropping drastically. In 2025, it’s scheduled to fall to $2,500.

What’s Coming in 2025 and Beyond?

One of the biggest potential tax shake-ups in recent years is on the horizon: The first Trump Administration’s Tax Cuts and Jobs Act (TCJA) of 2017 is set to expire after 2025. This means major changes could be coming, including:

A decrease in the standard deduction

A reduction in the estate tax exemption by half

Tax brackets and rates reverting to higher pre-TCJA levels

A reduction in the Child Tax Credit from $2,000 per child in 2025 to $1,000 per child in 2026.

Eliminating the $10,000 cap on state and local tax (SALT) deductions

Change to the alternative minimum tax income threshold.

The current administration appears ready to act, suggesting it will work with Congress to extend the TCJA. However, nothing will be certain until changes are made to the tax law.

With so many possible changes in play, staying ahead of tax law updates is more important than ever. We can help you keep an eye on legislative developments and adjust your planning as necessary to make the most of your tax situation. Reach out with any questions you might have. ether a disaster plan of your own, reach out and we can help.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/03/Tax-Consideration-for-2024.png10801080Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-03-17 09:44:502025-03-17 09:47:57Tax Considerations for 2024: What You Need to Know Before Filing