Eight “Best/Worst” Wealth Strategies During the Coronavirus

“The utility of living consists not in the length of days, but in the use of time.”

-Michel de Montaigne

For better or worse, many of us have had more time than usual to engage in new or different pursuits in 2020. Even if you’re as busy as ever, you may well be revisiting routines you have long taken for granted. Let’s cover eight of the most and least effective ways to spend your time shoring up your financial well-being in the time of the coronavirus.

1. A Best Practice: Stay the Course

Your best investment habits remain the same ones we’ve been advising all along. We build a low-cost, globally diversified investment portfolio with the money you’ve got earmarked for future spending. We structure it to represent your best shot at achieving your financial goals by maintaining an appropriate balance between risks and expected returns. We stick with it, in good times and bad.

2. A Top Time-Waster: Market-Timing and Stock-Picking

Why have stock markets been ratcheting upward during socioeconomic turmoil? Market theory provides several rational explanations. Mostly, market prices continuously reset according to “What’s next?” expectations, while the economy is all about “What’s now?” realities. If you’re trying to keep up with the market’s manic moves … stop. It is not a good use of your time.

3. A Best Practice: Revisit Your Rainy-Day Fund

How is your rainy-day fund doing? Right now, you may be realizing how helpful it’s been to have one, and/or how unnerving it is to not have enough. Use this top-of-mind time to establish a disciplined process for replenishing or adding to your rainy-day fund. Set up an “auto-payment” to yourself, such as a monthly direct deposit from your paycheck into your cash reserves.

4. A Top Time-Waster: Stretching for Yield

Instead of focusing on establishing adequate cash reserves, some investors try to shift their “safety net” positions to holdings that promise higher yields for similar levels of risk. Unfortunately, this strategy ignores the overwhelming evidence that risk and expected return are closely related. Stretching for extra yield out of your stable holdings inevitably renders them riskier than intended for their role. As personal finance columnist Jason Zweig observes in a recent exposé about one such yield-stretching fund, “Whenever you hear an investment pitch that talks up returns and downplays risks, just say no.”

5. A Best Practice: Evidence-Based Portfolio Management

When it comes to investing, we suggest reserving your energy for harnessing the evidence-based strategies most likely to deliver the returns you seek, while minimizing the risks involved. This is why we create a mix of stock and bond asset classes that makes sense for you; we periodically rebalance your prescribed mix (or “asset allocation”) to keep it on target; and/or we adjust your allocations as your goals change. We also ensure that we structure your portfolio for tax efficiency, and choose the ideal holdings for achieving all of the above.

6. A Top Time-Waster: Playing the Market

Some individuals have instead been pursuing “get rich quick” schemes with active bets and speculative ventures. The Wall Street Journal has reported on young, do-it-yourself investors exhibiting increased interest in opportunistic day-trading, and alternatives such as stock options and volatility markets. Evidence suggests you’re better off patiently participating in efficient markets as described above, rather than trying to “beat” them through risky, concentrated bets. Over time, playing the market is expected to be a losing strategy for the core of your wealth.

7. A Best Practice: Plenty of Personalized Financial Planning

There is never a bad time to tend to your personal wealth, but it can be especially important – and comforting – when life has thrown you for a loop. Focus on strengthening your own financial well-being rather than fixating on the greater uncontrollable world around us. To name a few possibilities, we’ve continued to proactively assist clients this year with their portfolio management, retirement planning, tax-planning, stock options, business successions, estate plans and beneficiary designations, insurance coverage, college savings plans, and more.

8. A Top Time-Waster: Fleeing the Market

On the flip side of younger investors “playing” the market, retirees may be tempted to abandon it altogether. This move carries its own risks. If you’ve planned to augment your retirement income with inflation-busting market returns, the best way to expect to earn them is to stick to your plan. What about getting out until the coast seems clear? Unfortunately, many of the market’s best returns come when we’re least expecting them. This year’s strong rallies amidst gloomy economic news illustrates the point well. Plus, selling stock positions early in retirement adds an extra sequence risk drag on your future expected returns.

Could you use even more insights on how to effectively invest any extra time you may have these days? Please reach out to us any time. We’d be delighted to suggest additional best financial practices tailored to your particular circumstances.

—

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

April 2019 Market Commentary

April 2019 Market Commentary

Key Takeaways

-

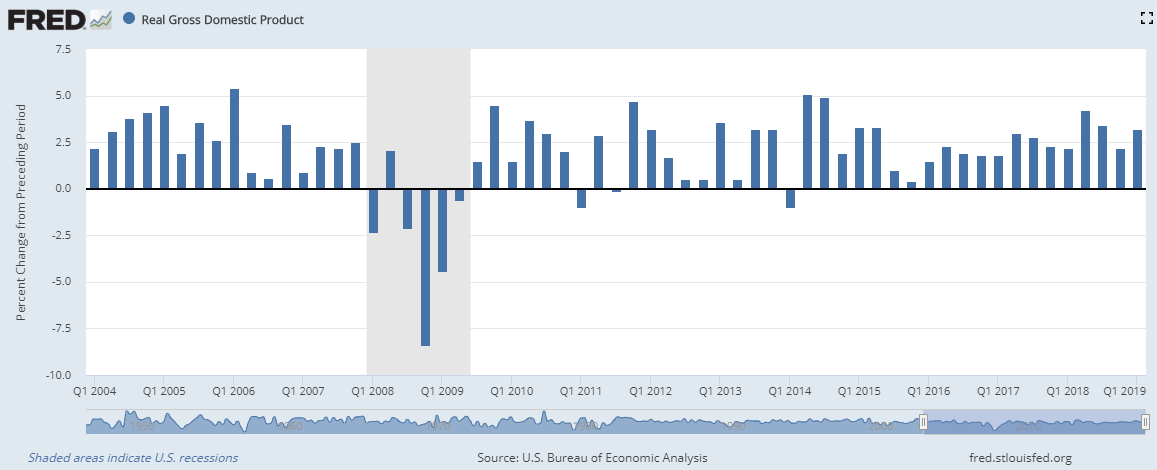

- 1st quarter GDP beat expectations at 3.2%, due in part to increasing net exports and inventories

- The U.S. stock market reached new highs as economic data and corporate earnings were stronger than expected, though stock prices of companies with disappointing results have been punished

- Despite slowing GDP in China and continuing budgetary and political challenges throughout Europe, economic growth overseas remains modestly positive

- The Conference Board’s Leading Economic Indicators Index® increased in February and March, though is expected to weaken slightly going forward; new home sales and job growth beat expectations

- Though central banks are on hold for now, interest rate ‘normalization’ will resume when inflation gains traction, which could happen later this year due to tight labor markets and rising commodity prices

- Conclusion: Enjoy the party! Global stock markets have had a good run so far, and recent earnings announcements and economic data suggest a positive environment for the rest of the year.

The death of the U.S. economy has been greatly exaggerated.

1st quarter GDP beat expectations at 3.2%, due in part to increases in net exports and inventories. This strong growth came despite the consensus view earlier in the year that the U.S. economy was nearing a recession. In fact, the U.S. economy is still benefiting from several sources of stimulus such as low interest rates, 2017 corporate tax cuts, and deregulation. While it’s unlikely we’ll see such strong GDP numbers going forward, there’s no sign yet that these supportive factors have fully played themselves out.

Time to celebrate! The U.S. economy is not dead!

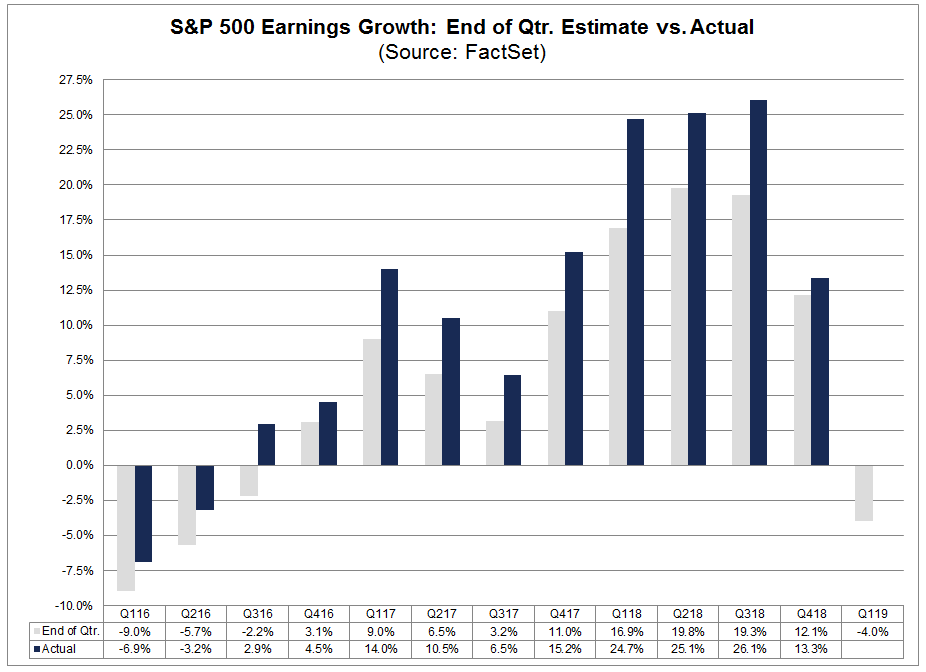

The strong GDP growth was also reflected in the U.S. stock market. As of April 26, 77% of S&P 500 companies reporting actual earnings during the 1st quarter of 2019 were higher than expected. The chart below compares projected quarterly corporate earnings (gray bar) to actual earnings (blue bar) over the past few years. Actual earnings surpassed estimated earnings in the 4th quarter of 2018 and are looking to do the same in the 1st quarter of 2019. Add to this the size of the positive surprise so far in 2019 being larger than the historical average, and you have the U.S. stock market hitting new highs in April.

But it isn’t all roses and sunshine. The U.S. stock market has rewarded upward earnings surprises for sure, but has been unusually harsh with companies reporting disappointing earnings. According to the Wall Street Journal, the stock price of companies reporting actual earnings below estimates has fallen an average of 3.5% in the two days before and after their earnings announcement, compared to a historical average decline of only 2.5%. Investors don’t seem convinced that corporate profits are going to continue to grow.

One indicator of this lack of trust in the strength of the economy is very low bond yields. Despite decent earnings growth and high stock prices, the yield on the 10-year Treasury bond remains very low at about 2.5%, barely above inflation. The fact that investors are willing to buy bonds at this very low yield indicates skepticism about where the global economy is headed and how quickly we’re likely to get there.

Countries outside the U.S. are also facing economic uncertainty. Europe continues to struggle with trade tariffs and political unrest, and tensions between the U.S. and China remain unsettled. The U.K. hasn’t yet figured out how to exit the European Union gracefully, Italy missed its budget deficit target (again), and business sentiment in Germany is falling.

One bright spot is stronger-than-expected first quarter growth in China. But international investors are now worried that Chinese authorities will slow the pace of policy easing and the economy will fall back. While Europe and the U.K. seem to be navigating their challenges well enough, heaven help us if the expected resolution of the U.S.-China trade talks gets derailed! Given the uncertain state of global economies, skittish investors may run for the sidelines at the slightest negative news about escalating trade tensions.

But don’t let me be a ‘Debbie Downer’! Global stock markets are doing great so far this year.

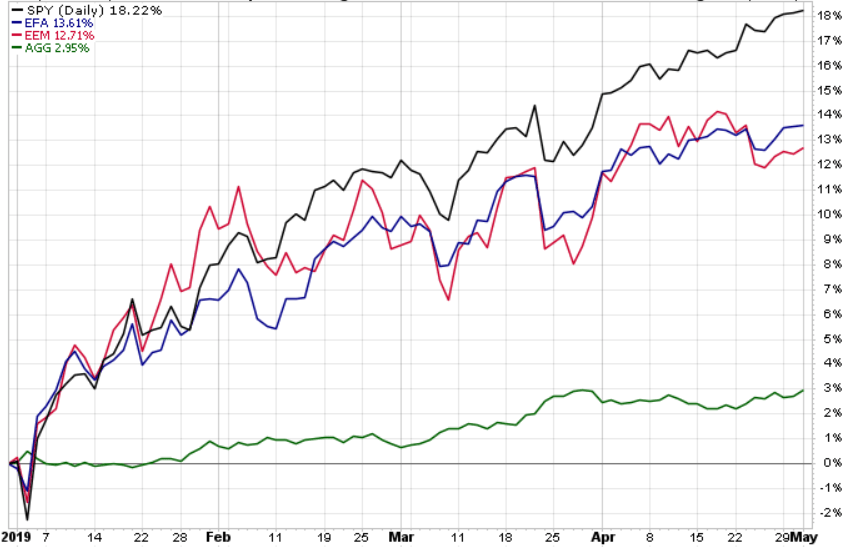

If the year ends with no more gains than we already have, the S&P 500 return for the first four months of 2019 will be in the top third of historic returns for an entire year. As you can see in the graph below, developed and emerging global markets are also having a good run in 2019 (blue and red lines). Even bond market returns are positive, as shown by the green line at the bottom of the graph.

https://stockcharts.com/h-perf/ui

There is one cautionary note on the U.S. stock market, however: higher-than-average stock valuations. According to Factset, the forward 12-month Price/Earnings ratio for S&P 500 companies has risen to 16.8. This is higher than both the 15-year and 10-year average, and a signal that the market may not have much more room to run.

So far, so good…but for how long?

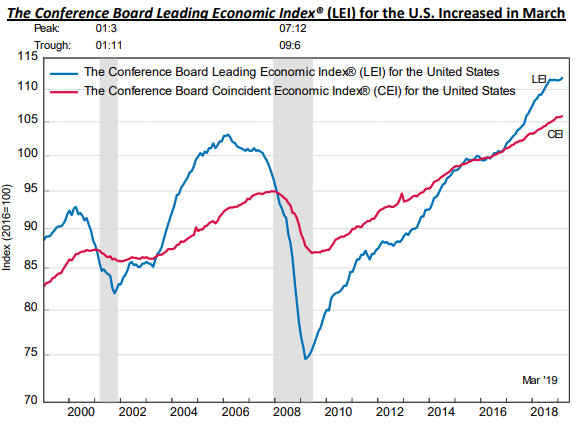

In mid-April the Conference Board announced its Leading Economic Indicators Index® (LEI) for the 1st quarter of 2019. The LEI posted a gain of 0.4% in March after increasing 0.1% in February, primarily due to strength in the labor markets, improved consumer outlook, and better-than-expected financial conditions. Eight out of the 10 LEI factors were positive in March, with 2 factors holding steady (average weekly manufacturing hours and building permits.) New home sales also rose unexpectedly in March, the third gain in a row. The three-month average sales rate is close to its best since December 2007.

Despite the recent strength in economic data, the trend in the LEI is leveling out, suggesting the U.S. economy will slow toward its long-term potential growth rate of about 2% by year end. This trend is reflected in the reduced pace of home price appreciation in March and a slight drop in labor participation.

The Fed echoed this ‘slow growth’ story in the statement released after the May 1st FOMC meeting. The committee highlighted a slowdown in household spending and business investment, as well as inflation below its 2% target, but indicated this weakness was probably “transient” and short term rates were appropriate at the current level.

All in all, the data continue to support the conclusion we’ve been talking about since late 2018 – the U.S. economy is slowing, but a recession is not imminent. In fact, the surprise that might spook investors later this year isn’t recession, but inflation.

With stronger than expected economic data so far in 2019, is inflation around the corner?

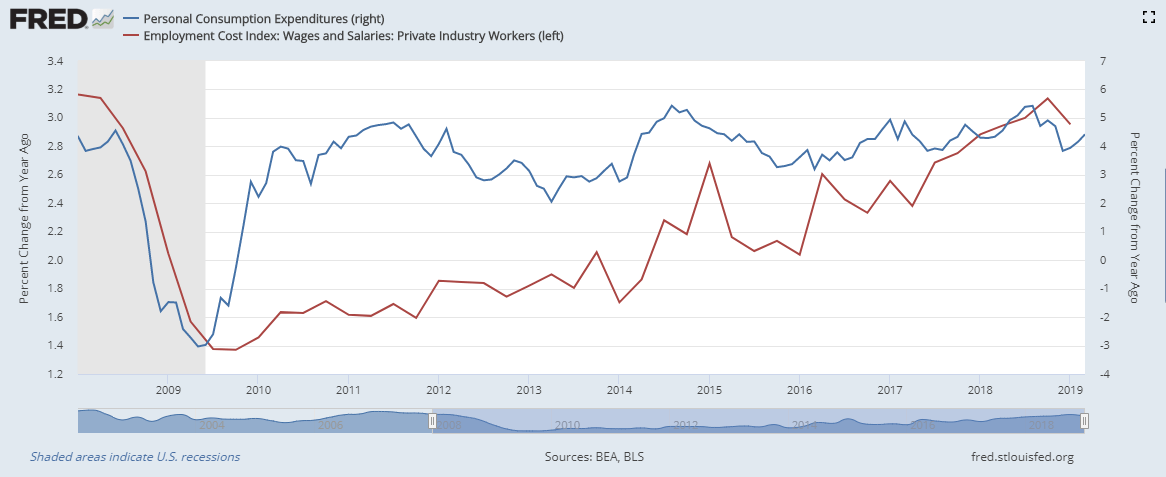

The tight labor market and increasing commodity prices might catch up with us later this year. As shown on the graph below, the cost of personal consumption has fallen recently but ticked up again in March (blue line). The Employee Compensation Index increased 0.7% for the quarter, though the 12-month growth rate slowed a bit (red line.) And the job report released in early May reported non-farm payrolls up 263,000, while the unemployment rate fell to 3.6%, the lowest level since 1969. It’s reasonable to expect higher wages to boost consumer purchases going forward, which may enable businesses to pass the increased labor cost on to consumers.

If you add increasing commodity prices such as oil (red line) and copper (blue line) to the rising wage trend, we may finally see the increase in inflation many of us have been watching for during the past few years of the economic recovery.

What is the end result? If commodity prices remain high and sales of goods and services absorb price pressure from increased labor and input costs (inflation), the Fed may have to revisit its mission to ‘normalize’ interest rates to keep the U.S. economy from overheating later this year. Market participants aren’t expecting this. Investors tend to react badly when caught by surprise, so we’re keeping a close watch on the data in the hope of being one step ahead of the crowd when the time comes to head for the exits.

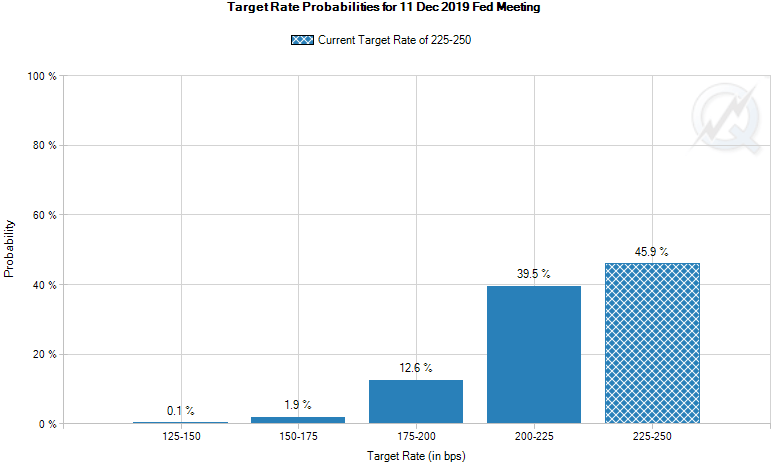

Source: https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

Conclusion: Enjoy the ride! (for now)

While we can’t predict when the party will end, that’s no reason not to enjoy ourselves in the meantime. A higher proportion of people are participating in the workforce than at any time since the 2008-2009 recession. Wages are rising, political tensions are easing, corporate profits aren’t as bad as feared, and interest rates remain low. What’s not to like?!

Just keep an eye out for warning lights as we get closer to the end of the year.

ASSET CLASS and SECTOR RETURNS as of APRIL 2019

Source: Morningstar Direct

Source: S&P Dow Jones Indices

Marcia Clark, CFA, MBA

Marcia Clark, CFA, MBA

Senior Research Analyst

Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.

DISCLOSURES

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications.

Form ADV available upon request 714-876-6200

Case Study: Start Retirement on Vacation

Case Study – Start Retirement on Vacation

Learn how we helped a client retire early, without penalty, move out-of-state, and get their desired income level by constructing a strong financial plan.

When most people think of working with a financial advisor for retirement, people think about investment management strategies. Having someone whom they could trust and feel confident in handling their money. Believe us, having trust and confidence in someone to handle your money correctly is a big piece of the puzzle when choosing an advisor.

However, a good financial advisor brings more to the table than their investment strategy. They should bring some financial planning knowledge that can help you retire smoothly and utilize as much of your retirement benefits as possible, and that is exactly what we want to share in this case study.

We worked with a client who planned on retiring towards the end of the year. They had done a great job saving, had plenty of assets to retire, and they were counting down the days to their December retirement date.

It was hard to not get wrapped up in their excitement because it is such an exhilarating time, but we wanted to make sure we had done all the due diligence on their benefits package. During our research, we learned how their vacation time worked which gave our client an incredible start to

retirement.

At this particular job, vacation time was reset as of the first of the year, so on January 1st, our client earned 6 weeks of paid vacation time. If you retire with vacation days left over, then you will get paid based off of how much of that time you “accrued”. For example, if you worked 6 months out of the year, then you would be able to get one-half of the unused vacation time paid out.

With our client planning on retiring so close to the new year, we advised them to delay their retirement a couple weeks, take vacation time the first 6 weeks of the new year, and be able to enjoy the full value of the benefit. The client even gets to collect a couple of paychecks to start their retirement.

By doing a bit of digging, we were able to get them more benefit than they had believed available and a great start to retirement. You want an advisor who is competent when it comes to building an investment strategy, but you also want to make sure your advisor is looking into every avenue possible to get you the benefits you have earned.

It would have been easy to tell the client to go ahead and retire, but it’s not about doing what is easy for the client.

It is about doing what is right and in the client’s best interest.

Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance, strategy, and results of your portfolio. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark. Nothing in this commentary is a solicitation to buy, or sell, any securities, or an attempt to furnish personal investment advice. We may hold securities referenced in the blog and due to the static nature of the content, those securities held may change over time and trades may be contrary to outdated posts.

Rate Watch 2018 – August

Rate Watch 2018 – August – SCE Grandfathered Pension

August’s rate is typically used for Edison’s official grandfathered pension plan interest rate. Where did it land, and how does that impact your pension?

Welcome to another edition of Rate Watch as we track the interest rate that is vital to the grandfathered pension at Southern California Edison.

The most important month of the year for grandfathered pension holders is upon us. August is typically used to set the grandfathered pension interest rate for the following plan year. Let’s take a look at where the rate it at:

These are not current plan rates for Southern California Edison’s pension plan, they are minimum present value third segment rates from the IRS. Official plan rates are derived from the minimum present value segment rates table (https://www.irs.gov/retirement-plans/minimum-present-value-segment-rates). Plan rate changes are made by Southern California Edison on an annual basis.

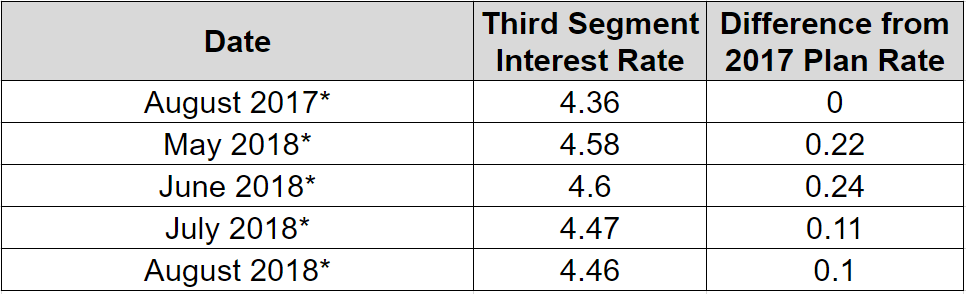

August came in at 4.46 and 0.10 higher than the current plan rate. Very simply, this means that your lump sum payout value will be higher with the 2018 plan value as opposed to the 2019 value.

Again, simply put, if you are grandfathered and thinking about retiring soon, then it might be in your best interest to retire and take the 2018 value to get a higher lump sum payout.

Since the difference in potential rates is small, the change in value is probably not great enough to heavily influence a decision to retire now or continue working, but it is something that should be capitalized on if retirement is on the horizon.

If you are unsure on how to request your paperwork or the timing to make sure you receive the 2018 pension rate, then contact us for a free retirement consultation, and we can show you how you can retire with confidence.

Joe Occhipinti

Joe Occhipinti

Wealth Advisor

Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.

Case Study: Retire Early, Without Penalty

Case Study – Retire Early, Without Penalty

Learn how we helped a client retire early, without penalty, move out-of-state, and get their desired income level by constructing a strong financial plan.

[emaillocker id=5188]

[/emaillocker]

Blake Street CFA, CFP®

Blake Street CFA, CFP®

Founding Partner

Chief Investment Officer

Warren Street Wealth Advisors

Blake Street is an Investment Advisor Representative of Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented.

Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance, strategy, and results of your portfolio. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark. Nothing in this commentary is a solicitation to buy, or sell, any securities, or an attempt to furnish personal investment advice. We may hold securities referenced in the blog and due to the static nature of the content, those securities held may change over time and trades may be contrary to outdated posts.

The Retirement Handbook

The Retirement Handbook (click to download)

Retirement is coming soon, and you should be excited. However, you might have so many questions and concerns about retirement that you’re more nervous than anything else.

We get it.

At Warren Street Wealth Advisors, we’ve helped countless people, from families to business owners, plan for their retirement and reach their financial goals. We put together this Retirement Handbook to help you on your way to a successful retirement.

1. Have a Plan

Nothing else on this list matters if you don’t have a personalized financial plan.

Having a plan not only lays out the destination, but it shows you the steps you need to take along the way. It’s your roadmap to a successful retirement.

2. No Seriously, Have a Plan

Having a plan is half the battle.

You can be tax savvy and an investment genius, but if you don’t have a plan for retirement or any financial goal, chances are you’ll miss the mark.

3. Say “Goodbye” to Debt

Excess debt is the biggest destroyer of retirement dreams.

If you have excess debt, then formulate a plan to eliminate it as soon as possible. It’s not the end of the world, but it might be time to roll up your sleeves and get to work.

Imagine how rewarding it will be once you have freed yourself from excess debt.

4. Budget it Out

Targeting your annual expenses is key to understanding if you have enough money to retire.

It’s no fun to build a budget. We get it.

However, knowing where your money is going on a monthly basis may help you identify where you can save. Get rid of the stuff you hate and keep more of the things you love. Love your bowling league? Keep it. Hate your cable or phone bill? Shop it around or eliminate it all together.

Not sure where to start with your budget? No problem. Download our retirement toolkit and utilize the Budget Template to help get you started.

5. Build Up Emergency Savings

We’re always optimistic about the future, but sometimes life takes surprising and difficult turns. Wise financial planning means being prepared for those situations.

Having cash available can help you through some of these hard times. Maybe the car breaks down or you need to find a new job. Having six months of cash on hand in a savings account can help out and keep you prepared for life’s ups and downs.

6. Save ’til it Hurts.

401(k). 403(b). 457(b). IRA. SEP. Simple. Deferred Comp. Roth.

Max it out.

Are you putting money aside for the long term? Does your employer have a 401(k) program? Do you have a personal investment account you contribute to?

Whatever it is, make sure you continue to think long-term for that beautiful retirement you’ve been dreaming of.

7. Wait Until Full Retirement Age to Take Social Security

There are all kinds of articles out there about what to do about your Social Security. Let us boil it all down: you don’t have to take it at 62!

When we build a financial plan, we calculate all options for optimizing Social Security, no matter how many times we do it, one thing becomes clear every time: it’s usually best to wait until your full retirement age to take Social Security.

There is also plenty of evidence to support wait until age 70 too as the 32% increase in benefit can be worth the wait. It’s ultimately your decision, and we suggest weighing your options before committing to collecting a 25-30% reduced benefit at age 62.

8. Have a Plan

Yep. Said it again.

If you’re not sure where to start with your financial plan, that’s OK. We can help.

Schedule a free consultation to talk through your finances and take the first step toward building a confident retirement.

Warren Street Wealth Advisors LLC. is a Registered Investment Advisor. The information posted here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this commentary is a solicitation to buy, or sell, any securities, or an attempt to furnish personal investment advice. We may hold securities referenced in the blog and due to the static nature of content, those securities held may change over time and trades may be contrary to outdated posts.

The Retirement Handbook: Southern California Edison Edition

The Retirement Handbook: Southern California Edison Edition

Retirement is just around the corner, and you should be excited. But some of us have many questions and concerns about retirement causing us to feel more nervous than anything else.

We understand these feelings.

At Warren Street Wealth Advisors, we’ve helped hundreds of Southern California Edison retirees navigate this crucial time. In the process, we’ve learned about SCE’s retirement and employee benefits programs inside and out. We’ve put together our Southern California Edison Retirement Handbook as a guide for you.

1. Have a Plan

Nothing else on this list matters if you don’t have a personalized financial plan.

A personalized financial plan is the roadmap to your comfortable retirement. You can know your benefits inside-out and be clever about taxes and investments, but if you don’t have a roadmap for navigating your retirement, you’ll never feel confident along the way.

2. Seriously, Have a Plan

Having a plan is essential for any major life transition, and navigating your retirement with wisdom and confidence is certainly part of a major life transition!

OK, let’s move on…

3. Plan to Retire Around October

If you are grandfathered into the old SCE pension formula, then you should plan to retire around October. This will allow you to choose which year’s plan rate provides you with the better benefit (Learn more HERE).

It’s important to know that you have a choice, review your options, then decide whether to retire on December 1st or January 1st – whichever projection pays the higher benefit.

If you are not grandfathered, retiring at the end of the year is still a great idea, especially if you need to take a large distribution pre-59 ½.

You are not forced to take your final distribution at retirement. You can wait until January 1st, request your final distribution, and then take a direct payment to avoid penalties using the “55 rule” if you are 55 years or older. This will also allow you to defer the income tax to the following year’s tax return.

This might seem complicated, but it’s a normal process for our clients who retired early.

4. Retire After 55 But Before 59 1/2 Without Paying Penalties.

Here’s a scenario we see all the time: you’re 57. You want to retire. You don’t want to wait until 59 ½ to do it. But you know that there’s a 10% federal tax penalty and a 2.5% California state tax penalty if you take the money out of your IRA before 59 ½. So are you stuck? Nope.

There are a lot of moving parts to this process, but we can take advantage of IRS rules like 72(t) distributions or the previously mentioned “55 rule” to ensure our clients do everything possible to avoid paying penalties.

5. Take Advantage of Your Medical Subsidy

Did you know that you are eligible for a retiree medical subsidy? The most common subsidies are 50% and 85%. When you retire, Edison will pay either 50% or 85% of your current medical insurance premium as a “continuation benefit” in retirement. Simply put, what you pay today is what you’ll pay in retirement. Of course, this is as long as you reach your required benefit milestone.

Unsure what your benefit is? You can call EIX Benefits to ask what benefit you have and at what age you’ll receive it. Call 866-693-4947.

Medical expenses are a huge cost for retirees, knowing what portion is covered by your employer is critical to planning a successful retirement.

6. Say “Goodbye” to Credit Card Debt

If you have credit card debt, then it’s time for a plan, a budget, and some hard work.

Debt can be intimidating, but you can pay it off! One of our favorite things is a client freeing themselves from the stress of mounting credit card debt. You may just need some help and a plan.

7. If Eligible, Plan for Your Sick Time Payout

Your sick time payout can be a significant amount and can be a boost into retirement, especially if you’re retiring early. You can run a pension projection online that will include a calculation of your accrued sick time payout . This will provide you more clarity about how much money you’ll start with when you retire, and it could help bridge the gap to 59 ½.

8. Build and Keep a Budget

We get it: it’s no fun to build a budget, but it’s the first step to discovering what retirement will look like.

Get rid of the stuff you don’t use and keep what makes you happy! Not sure where to start? No problem, use our Retirement Tool Kit to make it easy.

9. Build Up 6-Months Worth of Emergency Savings

We’re always optimistic about the future, but sometimes life takes surprising and difficult turns. Wise financial planning means being prepared for those situations.

We recommend that you save at least 6-months worth of living expenses in case of an emergency. Need $4,000/month to live? Then have around $24,000 in savings & checking. Now, you’re prepared for the ups and downs that life can throw at us at any age.

10. Weigh All Your Options on Social Security

There is a lot of information out there about what to do with Social Security. Let me boil it all down: you don’t have to take it at 62! When we build a financial plan for a client, we calculate all options for optimizing Social Security.

It’s ultimately your decision, we suggest weighing your options before committing to collecting the 25-30% reduced benefit at age 62.

11. Invest for Retirement

Max out your 401(k). Diversify your investments. Consider hiring a pro.

Make sure your investments are retirement ready. Do you have too much cash? Too much of a single stock? If you have ESOP shares, are you getting the most tax efficiency with them?

If you’re unsure, then having a team on your side can help you get the most out of your plan and make sure your investments match your goals and objectives.

12. Have a Plan

You didn’t think this was going to end without one more reminder, did you? If you’re not sure where to start with your financial plan, that’s OK: we can help.

Schedule a free consultation to talk through your finances and take the first step toward building a confident retirement.

Warren Street Wealth Advisors LLC. is a Registered Investment Advisor. The information posted here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this commentary is a solicitation to buy, or sell, any securities, or an attempt to furnish personal investment advice. We may hold securities referenced in the blog and due to the static nature of content, those securities held may change over time and trades may be contrary to outdated posts.

The Retirement Handbook: El Segundo Refinery Edition

The Retirement Handbook: El Segundo Refinery Edition

Retirement is just around the corner, and you should be excited. But some of us have many questions and concerns about retirement causing us to feel more nervous than anything else.

We understand these feelings.

At Warren Street Wealth Advisors, we’ve helped many El Segundo Refinery employees navigate this crucial and confusing time, so we put together our Retirement Handbook: El Segundo Refinery Edition.

1. Have a Plan

Nothing else on this list matters if you don’t have a personalized financial plan.

A personalized financial plan is the roadmap to your comfortable retirement. You can know your benefits inside-out and be clever about taxes and investments, but if you don’t have a roadmap for navigating your retirement, you’ll never feel confident along the way.

2. Seriously, Have a Plan

Having a plan is essential for any major life transition, and navigating your retirement with wisdom and confidence is certainly part of a major life transition!

OK, let’s move on…

3. Make Sure Your Retirement Timing is Correct

Eligibility for annual bonuses, vacation days, or vacation payouts should all be considered as you decide when to retire from the company.

Properly timing your retirement date could give you access to more vacation days or eligibility for an annual company bonus. This could all add up to a healthy sum and this should be looked at prior to deciding upon a firm retirement date.

4. Want to Retire Early?

We see it all the time. You’re 57, you want to retire. You don’t want to wait until you’re 59½ to do it, but you know that there’s penalties if you take the money out early. So are you stuck?

Some companies have provisions in their plans that allow flexibility around taking withdrawals which help getting around penalties.

At WSWA, we use these rules to help our clients avoid penalties.

5. Budget for Medical Expenses

Make sure you are budgeting for medical coverage in retirement. A quick call to your benefits department can give you a projection of what your retirement medical benefit would cost in retirement.

A spouse may have a better or more affordable medical plan if they are still working. Be sure to examine all of your options.

6. Say “Goodbye” to Credit Card Debt

If you have credit card debt, then it’s time for a plan, a budget, and some hard work.

Debt can be intimidating, but you can pay it off! One of our favorite things is a client freeing themselves from the stress of mounting credit card debt. You may just need some help and a plan.

7. Build Up 6-Months Worth of Emergency Savings

We’re always optimistic about the future, but sometimes life takes surprising and difficult turns. Wise financial planning means being prepared for those situations.

We recommend that you save at least 6-months worth of living expenses in case of an emergency. Need $4,000/month to live? Then have around $24,000 in savings & checking. Now, you’re prepared for the ups and downs that life can throw at us at any age

8. Build and Keep a Budget

We get it: it’s no fun to build a budget, but it’s the first step to knowing what retirement looks like.

Get rid of the stuff you don’t use and keep what makes you happy! Not sure where to start? No problem, use our Retirement Tool Kit to make it easy.

9. Weigh All Your Options on Social Security

There is a lot of information out there about what to do with Social Security. Let me boil it all down: you don’t have to take it at 62! When we build a financial plan for a client, we calculate all options for optimizing Social Security.

It’s ultimately your decision, we suggest weighing your options before committing to collecting the 25-30% reduced benefit at age 62.

10. Invest for Retirement

Max out your 401(k). Diversify your investments. Consider hiring a pro.

Make sure your investments are retirement ready. Do you have too much cash? Too much of a single stock? If you have ESOP shares, are you getting the most tax efficiency with them?

If you’re unsure, then having a team on your side can help you get the most out of your plan and make sure your investments match your goals and objectives.

11. Have a Plan

You didn’t think this was going to end without one more reminder, did you? If you’re not sure where to start with your financial plan, that’s OK: we can help.

Schedule a free consultation to talk through your finances and take the first step toward building a confident retirement.

Warren Street Wealth Advisors LLC. is a Registered Investment Advisor. The information posted here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this commentary is a solicitation to buy, or sell, any securities, or an attempt to furnish personal investment advice. We may hold securities referenced in the blog and due to the static nature of content, those securities held may change over time and trades may be contrary to outdated posts.

Rate Watch 2018 – July

Rate Watch 2018 – July

We are only a couple month away from the August segment rate announcement. Where could rates land for SCE grandfathered pension holders as we head into the fall?

Welcome to another edition of Rate Watch as we track the interest rate that is vital to the grandfathered pension at Southern California Edison. If you’ve missed any of our previous articles, you can find them here:

Rate Watch 2018 – May & June

Rate Watch 2018 – April

Rate Watch 2018 – March

Rate Watch 2018 – February

June’s posting puts us 2 months away from August’s rate which is typically used by Southern California Edison for the grandfathered pension plan. If you are eyeballing retirement soon, then it is essential to understand where the rate is now and where it could be going. Here is the latest:

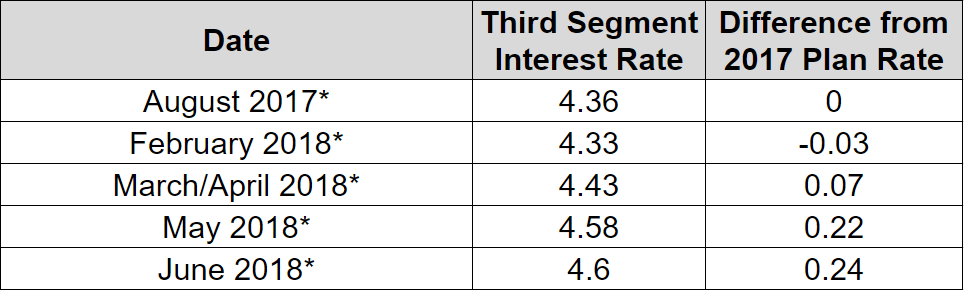

*These are not current plan rates for Southern California Edison’s pension plan, they are minimum present value third segment rates from the IRS. Official plan rates are derived from the minimum present value segment rates table (https://www.irs.gov/retirement-plans/minimum-present-value-segment-rates) . Plan rate changes are made by Southern California Edison on an annual basis.

July at 4.60 puts us nearly 25 points above the current plan rate and would drive your current lump sum value down if you took your pension in 2019.

Nominally, nothing has really changed month-to-month, but there has also not been much going on that would drastically press the rates higher over the time period. The most important thing to note would be inflation slowly on the rise as we continue to be in an environment of historically low rates.

For those in the grandfathered pension plan and who believe they are on the brink of retirement, it is more important now than ever to begin putting a plan in place and seeing what your retirement looks like. Knowing how your assets weigh against your liabilities, how much you might need every year in retirement, and if you have the assets to accomplish everything you want are important answers to have before you have your final day of work.

If the official rate was announced today, then it may make sense to take your pension in the current plan year due to the fact that as rates increase, lump sum values decrease.

If you are just unsure of what your retirement looks like, then feel free to contact us for a free phone call or meeting. We have helped 100’s of SCE employees retire and numerous grandfathered pension holders weigh their options out to give themselves the best possible outcome and start to retirement.

Joe Occhipinti

Wealth Advisor

Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. Information contained herein does not involve the rendering of personalized investment advice, but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.