Probate is the court process used to determine who gets an inheritance. In the eyes of a financial planner, it is a court process that most clients should try to avoid for many reasons. The probate process is time-consuming, usually lasting about a year depending on how backed up the courts are. The expense for probate is very high, which includes thousands of dollars going towards attorney and court fees. Probate is also a public court event in which potential heirs can object to the ruling pretty easily, causing privacy concerns and more attorney costs. While probate can have its time and place, there are some simple ways to avoid probate.

Let’s take a look at three easy steps you can take now to keep your loved ones from having to deal with probate.

Primary Beneficiary Designations – If a 401(k) account or life insurance policy lists a primary beneficiary, the account avoids probate and passes directly to the listed beneficiary. For brokerage accounts this is usually referred to as a Transfer-On-Death (TOD) account, and for bank accounts this is referred to as a Payable-On-Death account.

Contingent Beneficiary Designations – Setting a contingent beneficiary is also an easy way to help avoid probate. The contingent beneficiary is the person(s) next in line to inherit if the primary beneficiary has already passed away at the time of the account holder’s passing.

Retitle Your Automobile & House – Don’t forget about your car and home! If your vehicle or house are listed in your name alone, they would turn into probate assets at the time of your passing. Some states have introduced TOD car and house titling as a way to avoid needing probate if the owner passes away. Also, you and your spouse should consider owning the car and house jointly with rights of survivorship, as another way to avoid probate.

These planning points provided today are just some of the easy actions you can do yourself. There are more ways to avoid probate, but they get a little more complex and depend on your personal situation.

With legal matters like this, it is always a good idea to start working with an estate planning attorney, as well as with a financial advisor. Work with a Warren Street Wealth Advisor today to get your personalized financial plan and more guidance on estate planning.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/08/Blog-Thumbnail.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2023-08-17 08:51:512024-11-07 09:21:18Probate: 3 Easy Ways to Avoid it

Ever heard of the 80/20 rule? It suggests 80% of an outcome is often the result of just 20% of the effort you put into it.

Often, by prioritizing the 20% of your efforts that make the biggest splash, you can reduce excess commotion. In that spirit, here are 3 financial best practices that pack a lot of value per “pound” of effort.

Going back to 1926 and after adjusting for inflation, U.S. stocks have delivered about 7.3% annualized returns to investors who have simply been there, earning what the markets have to offer over the long haul. Those who instead fixate on dodging in and out of hot and cold markets are expected to reduce, rather than improve their end returns. That’s because, when markets recover from a downturn, they often more than make up for the stumble quickly, dramatically, and without warning. Instead of chasing trends, simply stay invested over time.

2. Portfolio Management: Use Asset Allocation, and Don’t Monkey With the Mix

Asset allocation is about investing in appropriate percentages of security types, or asset classes, based on their risk/return “personality.” For example, given your financial goals and risk tolerances, what ratio of stocks versus bonds should you hold?

Both practical and academic analyses have found that asset allocation is responsible for a great deal of the return variability across and among different portfolios. So, to build an efficient portfolio, we advise paying the most attention to your overall asset allocation, rather than fussing over particular securities. Luckily, if you’re a client of ours we’ve already taken care of this for you.

3. Financial Planning: Do It, But Don’t Overdo It

Also in 80/20 rule fashion, an ounce of financial planning can alleviate pounds of doubt. Planning connects your resources with your values and priorities. It’s your touchstone when uncertainty eats away at your resolve. And it guides how and why you’re investing to begin with.

Here’s some good, 80/20 news: Your plan need not be elaborate or time-consuming to be effective. In The One-Page Financial Plan, author Carl Richards describes:

“Your one-page plan simply represents the three to four things that are the most important to you: some action items that need to get done along with a reminder of why you’re doing them.”

If you’d like to do more, great. But even a one-page plan will give you a huge head start. Write it down, as Richards describes. When in doubt, read what you’ve written. Is it still “you”? If so, your work is done; stick to plan. If not, consider what’s changed, and update your plan accordingly. I

Building Lifetime Wealth, 80/20 Style

Properly applied, the 80/20 rule can help minimize the time and energy you have to put into maximizing your financial well-being. Whether you’re saving for retirement, funding your kids’ college education, preparing for a wealth transfer, applying for insurance, or otherwise managing your hard-earned wealth, we can help you identify and execute these and other actions that matter the most, so you can get back to the rest of your life.

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/03/80-20-Rule-Blog.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-07-28 08:57:432024-11-07 09:21:403 Ways to Apply the 80/20 Rule to Your Financial Pursuits

Last week, the Supreme Court voted against the White House Administration’s plan to eliminate up to $10,000 of student loans for non-Pell grant recipients and up to $20,000 of loans for Pell grant recipients. This news comes just as the three-year pause on student loans is coming to an end, with loan interest accruing again in September and payments beginning in October.

The Administration plans to propose other types of aid to borrowers, such as reducing the income-driven repayment plan from 10% to 5% of disposable income and not reporting missed payments to credit rating agencies for 12 months. Still, the timeline on these proposals could take months to get approved — so it looks like it is time to prepare for paying back your student loans.

At Warren Street Wealth Advisors, we want you to take the necessary actions to feel confident about your next steps. Start with the considerations below, and feel free to reach out to your financial advisor with any questions.

1. Update your information on studentaid.gov.

Check that your current contact and billing information are up-to-date with the Education Department on studentaid.gov. If you’ve moved, for example, the Education Department will need your updated address to contact you with loan status updates.

2. Determine how much outstanding student loan debt you have.

Work with your loan provider to see how much student loan debt you have remaining and how much the monthly payments will be. Once you know how much to expect each month, it will be easier to manage your spending.

3. Factor student loan payments back into your budget.

Whether you use software to help analyze your budget or the back of an envelope to do your calculations, it is time to add up all of your expenses and compare them to your take-home pay. This will let you know if you will be running a surplus, breakeven or deficit each month going forward.

4. Explore income-driven options.

If you determine you might be at a monthly deficit with student loan payments, an income-driven repayment plan could be an option for you. However, while this option could help your monthly budget, it usually involves you paying more interest in the long-term and extends your payments well past the 10 year standard repayment plan.

5. Shore up your emergency fund.

It’s always a good idea to count your liquid cash savings, especially in a time like this. Having a three to six month emergency fund to fall back on will be important if you have a student loan bill you need to pay again. Now is a good time to start an emergency fund if you don’t have one.

These are some of the most important steps to ensure you make payments on time and know what to expect in the near future when it comes to your debt management. Please reach out if you’d like to discuss these planning points with a Warren Street advisor!

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/07/Student-Loan-Blog.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2023-07-12 09:00:002024-11-07 09:22:41It’s Time to Revisit Your Student Loans

In planning for retirement, one topic is often top of mind: whether or not Social Security will still be around when we retire.

As we covered in a related post, When Should You Take Your Social Security, most of us have been paying into the program our entire working life. We’re counting on receiving some of that money back in retirement.

But then there are those headlines, warning us that the Social Security trust fund is set to run dry around 2034.

Does this mean you should grab what you can, as soon as you’re able? Let’s explain why we agree with Social Security specialist Mary Beth Franklin, who suggests the following:

“While there may be good reasons to file for reduced Social Security benefits early, claiming Social Security prematurely out of fear is a bit like selling stocks in a down market: All you’ve guaranteed is that you’ve locked in a loss. And if future benefit cuts did materialize, the benefits of those who claimed as soon as possible would be reduced even further.”

While we don’t expect Social Security to go bust, we do expect it will need to change in the years ahead. As its trustees have reported:

“Social Security is not sustainable over the long term at current benefit and tax rates … [and] trust fund reserves will be depleted by 2034.”

But let’s unpack this statement. First, “depleted” does not mean the Social Security Administration is going to turn out the lights and go home. It means it could run out of trust fund reserves by then, which are used to top off the total amount spent on Social Security benefits. There are still payroll taxes and other sources to cover more than 77% of the program’s payouts. So, worst case, if we did nothing but wait for the reserves to run out, we’d be forced to make hard choices about an approximate 23% shortfall starting around 2034.

Admittedly, Social Security is between a rock and a hard place. Nobody wants to lose benefits they’ve been counting on or spend significantly more to maintain the status quo. But if we don’t do something to shore up the program’s reserves, our options will likely only worsen.

In this context, the political will to reform Social Security seems strong, and bipartisan. As Buckingham Strategic Partners retirement planning specialist Jeffrey Levine has observed:

“My gut sense is that practically no politician in America would ultimately be happy having to explain to voters why they let Social Security collapse on their watch … That’s not a great message to have to bring to voters, especially older voters who show up at the polls in the greatest numbers.”

As members of Congress wrangle over the “best” (or least abhorrent) solutions for their constituents, they have been submitting proposals behind the scenes, and the Social Security Administration has been weighing in on the estimated effect for each.

Time will tell which proposals become legislated action, but the range of possibilities essentially falls into two broad categories: We can pay more in, or we can take less out.Most likely, we’ll need to do a bit of both.

Possible Ways to Pay More In

To name a few ways to replenish Social Security’s reserves, Congress could:

Raise the cap on wages subject to Social Security tax: As of 2023, earnings beyond $160,200 per year are not subject to Social Security tax. There’s been talk of increasing this cap, eliminating it entirely, or reinstating it for income beyond certain high-water marks.

Increase the Social Security tax rate for some or all workers: Currently, employers and employees each pay in 6.2% of their wages, for a total 12.4% up to the aforementioned wage cap. (This does not include an additional Medicare tax, which is not subject to the wage cap.) As cited in a September 2022 University of Maryland School of Public Policy report, “73% (Republicans 70%, Democrats 78%) favored increasing the payroll tax from 6.2 to 6.5%.”

Increase the tax on Social Security payouts, and direct those funds back into the program: Currently, if your “combined income” exceeds $44,000 on a joint return ($34,000 on an individual return), up to 85% of your Social Security benefit is taxable, as described here. Anything is possible, but taxing retirees more heavily seems less politically palatable than some of the other options.

Identify new funding sources: For example, one recent bipartisan proposal would establish a dedicated “sovereign-wealth fund,” seeded with government loans. Presumably, it would be structured like an endowment fund, with an investment time horizon of forever. In theory, its returns could augment more conservatively invested Social Security trust fund reserves. Other proposals have explored a range of potential new taxes aimed at filling the gap.

Options for Taking Less Out

We could also cut back on Social Security spending. Some of the possibilities here include:

Reducing benefits: Payouts could be cut across the board, or current bipartisan conversations seem focused on curtailing wealthier retirees’ benefits.

Extending the full retirement age: There are proposals to extend the full retirement age for everyone, or at least for younger workers. This would effectively reduce lifetime payouts received, no matter when you start drawing benefits.

Tinkering with COLAs: There are also bipartisan conversations about replacing the benchmark used to calculate the Cost-of-Living Adjustment (COLA), which might lower these annual adjustments in some years.

These are just a few of the possibilities. Some would impact everyone. Others are aimed at higher earners and/or more affluent Americans. It’s anybody’s guess which proposals make it through the political gamut, or what form they will take if they do.

Should You Take Your Social Security Early?

So, given the uncertainties of the day, should you start drawing benefits sooner than you otherwise would? An objective risk/reward analysis helps guide the way.

Many investors feel “safer” taking their Social Security as soon as possible, to avoid losing what seems like a bird in the hand. However, the appeal of this approach is often fueled by deep-seated loss aversion. Academic insights suggest we dislike the thought of losing money about twice as much as we enjoy the prospect of receiving more of it. Thus, we tend to cringe more over a potential loss of promised benefits than we factor in the substantial rewards we stand to gain by waiting. Put another way:

You’re not reducing your financial risks by taking Social Security early. You’re only changing which risks you’re taking. In exchange for an earlier and more assured payout, you’re also accepting a permanent, cumulative cut to your ongoing benefits.

If this still seems like a fair trade-off, consider that Social Security is one of the few sources of retirement income ideally structured to offset three of retirement’s greatest risks:

Life expectancy risk: In an annuity-like fashion, Social Security is structured to continue paying out, no matter how long you and your spouse live.

Inflation risk: The payouts are adjusted annually to keep pace with inflation.

Market risk: Even in bear markets, Social Security keeps paying, with no drop in benefits.

In short, if you are willing and able to wait a few extra years to receive a permanently higher payout, you can expect to better manage all three of these very real retirement risks over time.

This is not to say everyone should wait until their Full Retirement Age or longer to start taking Social Security. When is the best time for you and your spouse to start drawing benefits? Rather than hinging the decision on uncontrollable unknowns, we recommend using your personal circumstances as your greatest guide. Consider the retirement risks that most directly apply to you and yours, and chart your course accordingly.

But you don’t have to go it alone. Please be in touch if we can assist you with your Social Security planning, or with any other questions you may have as you prepare for your ideal retirement.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/04/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2023-05-11 08:28:422024-11-07 09:23:22Why We Believe Social Security Will Endure

Ever since President Franklin D. Roosevelt signed the 1935 Social Security Act, most Americans have pondered this critical question as they approach retirement:

“When should I (or we) start taking my (or our) Social Security?”

And yet, the “right” answer to this common query remains as elusive as ever. It depends on a wide array of personal variables, including how the unknowable future plays out.

No wonder many families find themselves in a quandary when it comes to taking their Social Security benefits. Let’s take a closer look at how to find the right balance for you.

Social Security Planning: A Balancing Act

For Social Security planning purposes, you reach full retirement age (FRA) between ages 66–67, depending on the year you were born. However, you can generally begin drawing Social Security benefits as early as age 62 (with the lowest available monthly starting payments) or as late as age 70 (for the highest available monthly starting payments).

Retirees are often advised to wait at least until their full retirement age, if not until age 70 to begin taking Social Security. In raw dollars, waiting to take your Social Security often works out to be the best deal for many families. Plus, these days, many of us choose to work well into our 60s, 70s, and beyond. Some analyses have even factored in the cost of spending down other assets while you wait, rather than using them for continued investment growth. The conclusion is the same.

However, you’re not “many families.” You’re your family. Your personal and practical circumstances may mean this general rule of thumb won’t point to your best choice. Following are some of the most common factors that may influence whether to start taking Social Security sooner or later.

Alternative Income Sources: First, and perhaps most obviously, if you have few or no alternative income sources once your paychecks stop, you may not have the luxury of waiting. You may need to start taking Social Security as soon as possible.

Life Expectancy: If you’re considering the benefits of waiting until age 70 to take Social Security, remember that this strategy assumes you live to at least the average age someone your age and gender is likely to reach. Even if you can afford to wait, you’ll want to factor in whether your health, lifestyle, and family history justify doing so.

Estate Planning: Have you placed a high or low priority on leaving as much as possible to your heirs and/or favorite charities after you pass? Your preferences here may influence how, and from where you’ll spend down your inheritable estate, which in turn may influence the timing of your Social Security enrollment.

Employment: How likely is it you’ll keep working until your FRA? Once you reach it, you can collect full Social Security benefits, even if you’re still working. But until then, your earnings may reduce your Social Security benefits.

Marital Status: If you’re married, one of you has probably paid in more to Social Security. One is likely to live longer. You may retire at different times, and your ages probably differ. All these factors can complicate the equation. You’ll want to consider the timing, rules, and outcomes under various scenarios—such as when and whether to take Social Security as an earner, the spouse of an earner, the widow or widower of an earner, or an ex-spouse of an earner—while also factoring in whether you and/or your spouse are still working prior to your FRAs, as described above. Ideal start dates for one scenario may not be ideal for another.

Other Circumstances: Beyond your marital status, there are other factors that may influence your timing decisions if they apply to you—such as if you’re a business owner, you live abroad, you qualify for Social Security Disability, or your children qualify for Social Security benefits under your account.

Income Taxes: We find many pre-retirees don’t realize that up to 85% of their Social Security income may be taxable. Your annual Social Security income also figures into your modified adjusted gross income (MAGI), which can push you past thresholds for incurring Medicare surcharges (beginning at age 65, based on your MAGI from two years prior). Bottom line, broad tax planning may influence your timing as well.

Degrees of Control

Clearly, there’s a lot to think about when deciding when to start taking Social Security. Whether you’re going it alone or with a financial planner, here’s one piece of advice that should help:

Control what you can. Let go of what you can’t.

What do we mean by that? There are many known factors you can include in your Social Security planning. You know your marital status. You can access your Social Security account and/or use a calculator to estimate your benefits. You can make educated guesses about your life expectancy, how long you’ll work, and so on. Also, if you’ve delayed taking Social Security past your FRA, you may be able to change your mind … to a point. You can file to collect up to six months of retroactive benefits if you end up needing the income sooner than planned.

You can use all of this planning information and more to make reasonable assumptions and timely decisions about when to take your Social Security.

After that, we recommend going easy on yourself if (or more realistically, when) some of your plans don’t go as planned. Come what may, you’ve done your best. Instead of channeling energy into regretting good decisions, use it to make judicious adjustments whenever new assumptions arise. By consistently focusing on what we know rather than what we hope or fear, we remain best positioned to shift course as warranted in the face of adversity.

Whether you’re planning to file for Social Security or you’re already drawing it, we appreciate the opportunity to help you and your family make good choices about when, and how to manage your available options. We hope you’ll contact us today to learn more.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2023/01/When-Should-You-Take-Your-Social-Security.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2023-03-30 08:02:002024-11-07 09:23:46When Should You Take Your Social Security?

To say the least, there has been plenty of political, financial, and economic action this year — from rising interest rates to elevated inflation to ongoing market turmoil.

How will all the excitement translate into annual performance in our investment portfolios? The answer remains to be seen. But, while we wait to find out, here are five action items worth tending to before 2022 is a wrap.

Revisit Your Cash Reserves

Where is your cash stashed these days? After years of offering essentially zero interest in money markets, savings accounts, and similar platforms, some banks are now offering higher interest rates to savers.

Shop around: If you have significant cash saved up, now may be a good time to compare rates on cash accounts. We can help if you need guidance exploring the options.

Put Your Money to Work

If you’re sitting on more cash than you need in your emergency reserve, you may be able to put it to even better use under current conditions. Consider the following:

Lighten your debt load: Carrying high-interest debt is a threat to your financial well-being, especially in times of rising rates. Consider paying off credit card balances or other debts. Avoid accruing new debt during the holiday season.

Invest: Reach out to your lead advisor to determine what your opportunities are to put some cash to work in the markets.

Make Some Smooth Tax-Planning Moves

Another way to save more money is to pay less in taxes. Here are a couple of year-end ideas:

It’s still harvest season: Market downturns often present opportunities to engage in tax-loss harvesting by selling taxable shares at a loss, and promptly reinvesting the proceeds in a similar (but not identical) fund. You can then use the losses to offset taxable gains, without significantly altering your investment mix. If you have a non-retirement brokerage account with us, we’ve already been doing this on your behalf.

Maximize tax opportunities: Make sure you are taking advantage of your 401(k) and other tax-deferred investment opportunities. With only a few paychecks left in 2022, you’ll want to make sure your contributions are optimized.

Check Up on Your Healthcare Coverage

As year-end approaches, make sure you and your family have made the most of your healthcare coverage. Take a moment to examine all your benefits. For example, if you have a Health Savings Account (HSA), have you funded it for the year? If you have a Flexible Spending Account (FSA), have you spent any balance you cannot carry forward? If you’ve already met your annual deductible, are there additional covered expenses worth incurring before the meter resets in 2023? If you’re eligible for free annual wellness exams or other benefits, have you used them?

Get Set for 2023

Why wait for 2023 to start anew? Year-end can be an ideal time to take stock of where you stand and consider what you’d like to achieve in the year ahead.

Audit your household interests: What has changed, and what hasn’t? Have you shifted careers or decided to retire? Added new hobbies or encountered personal setbacks? How might these and other significant life events alter your ideal investment allocations, cash-flow requirements, insurance coverage, or estate plan?

How Can We Help?

How else can we help you wrap 2022 and position you and your loved ones for the year ahead?

Whether it’s helping you manage your investment portfolio, optimizing your tax planning, considering your cash reserves, weighing insurance offerings, or assessing any other components that contribute to your financial well-being, we stand ready to assist — today, and through the years ahead.

Cary Facer

Partner Emeritus, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/12/Best-Practices-for-Year-End-2022-Blog-Thumbnail.png10801080Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2022-12-16 08:30:212024-11-07 09:26:51Five Financial Best Practices for Year-End 2022

If you’re talking with friends about market volatility, pessimists may say “downward is the only way forward,” but optimists like us will continue to share the sentiment that “We Will Prevail,” which is based on our assessment of history, data, and our go-forward market outlook.

For those of you who caught that subtle reference from the movie Inception, maybe you’re getting a taste for how big of a cinephile I am. For those who didn’t – no sweat; let’s wrap up this series of blog releases by assessing the first quarter’s market performance.

Before diving in, it’s important to note the macroeconomic trends that are primarily driving market risk: 1) the tightening of financial conditions and 2) the war in Eastern Europe. The Federal Reserve and other Central Banks are raising interest rates to calm inflation. Meanwhile, Russia’s invasion of Ukraine has had knock-on effects economically, particularly in Europe. With that in mind, see below for how markets are ending the first quarter.

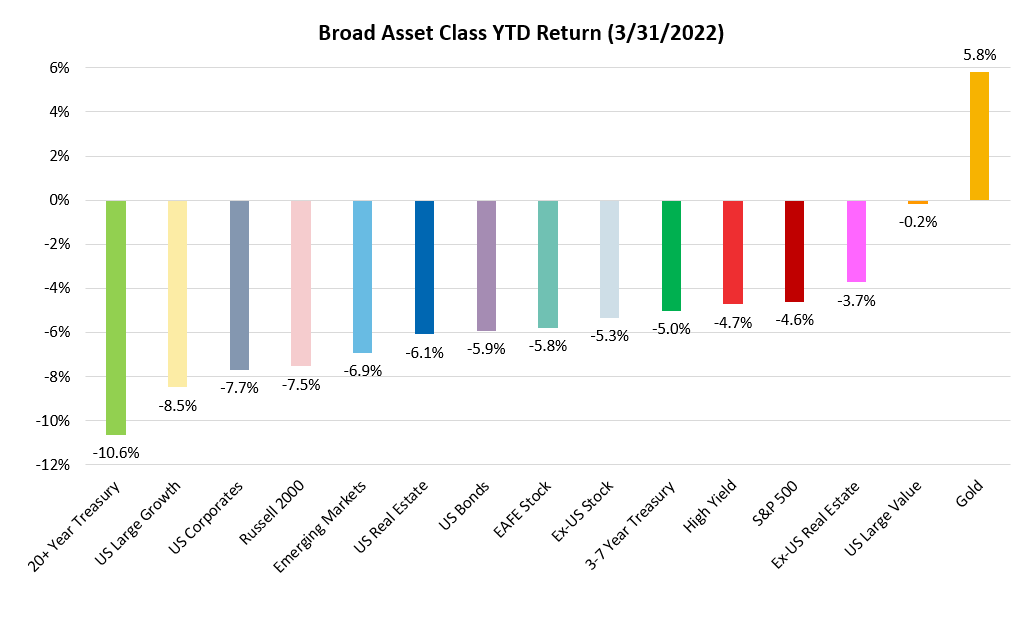

Exhibit A – Asset Class Performance in 2022

Source: YCharts

The Laggards

Looking at Exhibit A, bonds, followed by US Large Growth names (i.e., AMZN, AAPL), and international stocks (i.e., emerging markets and Europe stocks) are lagging.

Bonds Begrudgingly Behind: recent bond volatility can be attributed to inflation and rising interest rates. Inflation diminishes the purchasing power of a bond’s interest payments, while interest rate hikes apply downward price pressure on the value of a bond (you can now find a similar bond in the market yielding a higher rate).

Growth Names Falter: This asset class includes larger companies that are typically more expensive (e.g., Amazon, Apple), with stock prices that are highly dependent on future earnings growth. However, rising interest rates are raising the cost of borrowing, which depletes the value of a company’s future cash flows and are skewing growth names to the downside.

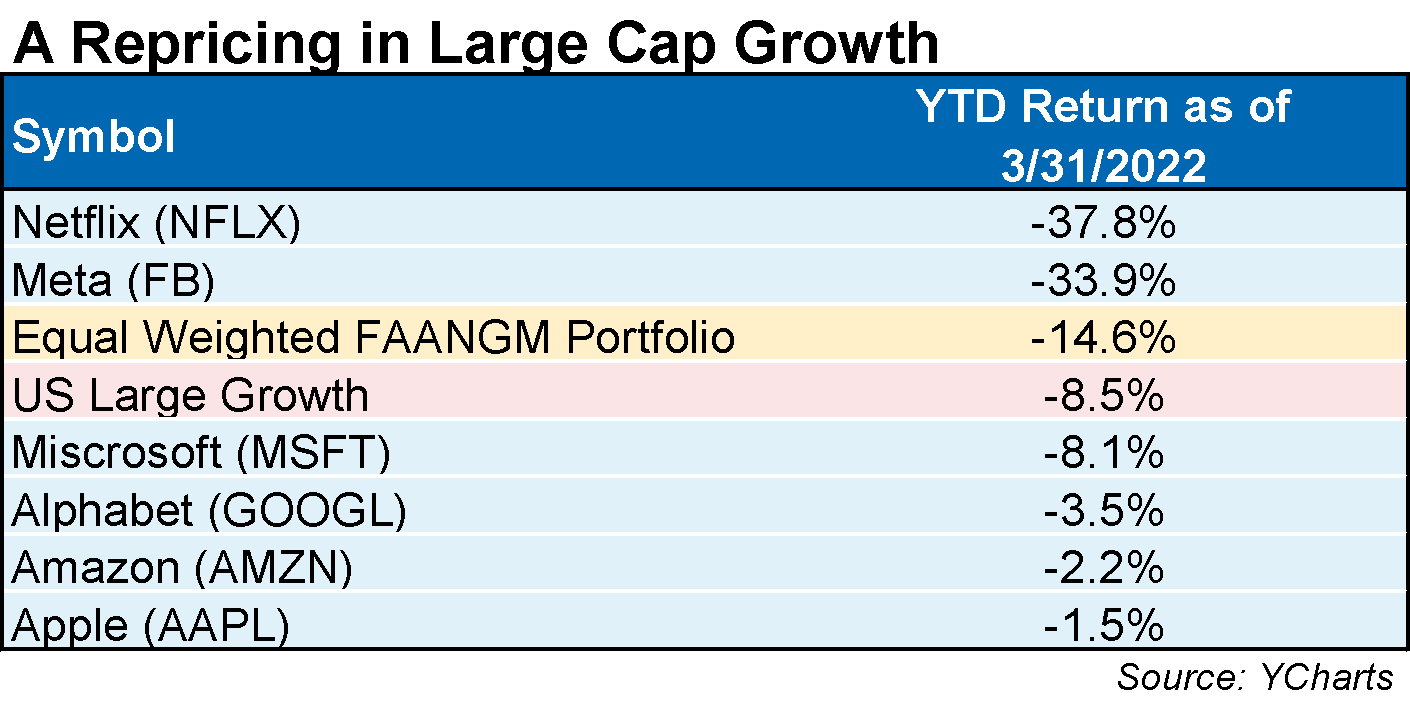

Exhibit B – How Are Big Tech Stocks Doing?

International Stocks Give Up Ground: At the start of the year, international stocks including European, Australian, and Far East (EAFE) and Emerging Markets (e.g., China, Brazil) equities outperformed domestic markets. US markets were being punished for an overweight to growthier names amid interest rate hikes. Most recently, the Russian invasion of Ukraine has dampened investor appetite for the international scene, overturning the region’s initial outperformance.

Exhibit C – The Race Between International and the US

Source: YCharts

Leaders

Gold Shines Bright: After a lackluster 2021, gold regained its shine this past quarter. Geopolitical uncertainty, coupled with a distrust of central banks to tame inflation, has resulted in sizable outperformance from the precious metal.

Value Names Triumph: While US Large Growth suffers from tighter financial conditions, investors are paying more attention to company profitability. US Large Value typically consists of companies that are larger, have a long-standing business model, and proven profitability. Examples include Target, Walmart, and Disney.

S&P 500 Recovers: After a weak start to the year (at one point being down 12% year-to-date), the S&P 500 has largely regained lost ground. Although the expectation of rate hikes remains a risk to the broader index, domestic markets have been favorable given a relatively unthreatening economic impact from the Eastern European war.

Takeaways, Portfolio Impact and Our Game Plan

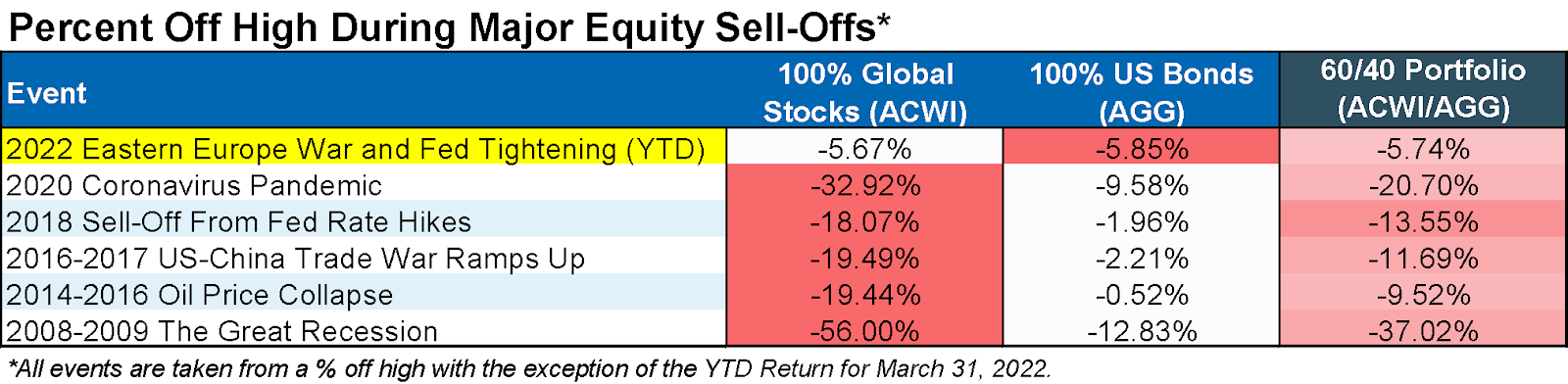

Takeaways – Is the 60/40 Portfolio Dead? A 60/40 portfolio has long been coveted as the standard for a “moderate” risk investor, with a 60% allocation to stocks and a 40% allocation to bonds. The bond allocation is meant to mitigate volatility during downturns, but with today’s largely challenged bond environment, the asset class has not cushioned investors during this recent equity sell-off.

Source: YCharts

Exhibit C includes the annual returns of a 60/40 portfolio, the global stock index (Ticker: ACWI), and the passive bond index (Ticker: AGG). Over the years, bonds have served as a protector against equity volatility, capturing a fraction of an equity market drawdown. However, thus far in 2022, bonds are selling off more than equities. Therefore, investors should not expect to receive similar risk-adjusted returns they did in the past for a traditional 60/40 portfolio – at least in the near term.

Portfolio Impact – Thinking Outside the Box: With the 60/40 structure in jeopardy and bonds to endure some short-term pain, a different approach should be considered. Enter Warren Street’s Real Assets sleeve – or what we like to call “Diversifiers” – which consist of real assets that typically benefit from inflation (i.e., gold, natural resources, and real estate).

Last summer, after acknowledging the adverse circumstances of the bond realm, Warren Street proceeded to underweight bonds and overweight diversifiers within blended models on top of initiating a position in a commodities fund. This trade has rewarded our portfolios and cushioned the bond and equity sleeves amid the most recent 2022 sell-off.

Our Game Plan – An International Resurgence: With Diversifiers outpacing stocks, our team rebalanced real assets into equity weakness, effectively selling high and buying low. We will continue to monitor momentum within Diversifiers and the bond landscape before returning to our neutral weights.

The looming question remains on our equity strategy, which incurred relative underperformance attributed to our overseas exposures. Although Russia’s military invasion overturned initial outperformance against domestic markets (see Exhibit C), we believe there is significant headroom for an international equity resurgence should the war abate.

Albeit still unpredictable, Ukrainian resistance is increasing the probability for a ceasefire. Couple that with the pandemic transitioning to an endemic, a US market that is more sensitive to central bank reserve tightening and attractive valuations overseas, we continue to remain optimistic about our clients being rewarded for their patience and for avoiding home-country bias.

Conclusion

You’ll hear us say it time and time again: control what you can control. Throughout this quarter, our team has tax-loss harvested in accounts amid sell-offs, rebalanced diversifiers into equity weakness, and thoroughly assessed the impact of conditions #1 and #2 mentioned above in our portfolios.

Outside of portfolio strategy, we’ve made strides in uploading more content on socials, blogs, and video formats to upkeep communications beyond our client meetings. We encourage you to read recent blog releases pertaining to the war in Ukraine and to give us a follow on social media.

Ultimately, the movie inception is about planting an idea and allowing it to grow. I’m no extractor or architect of dreams, but let me attempt to fortify my parting idea once more: “We Will Prevail.”

Phillip Law, Portfolio Analyst

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/04/Blog-Thumbnail-1.png10801080Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2022-04-06 08:30:002024-11-07 09:31:32Part 3: A Lookback at Q1 and Portfolio Impact

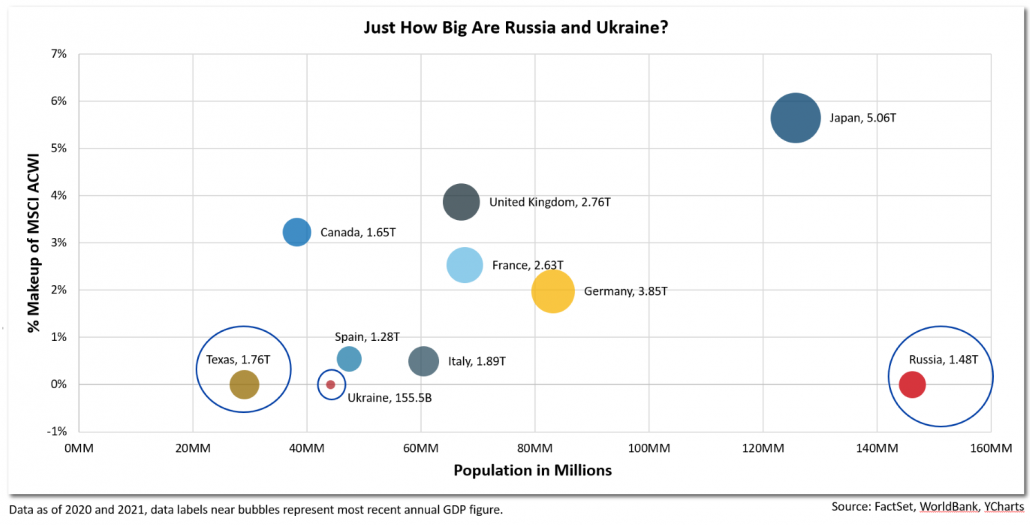

With news outlets centered on Eastern Europe, it is easy to miss the bigger economic picture both globally and domestically. For a broader assessment, it helps to understand how Russia fits into the global economy. Prior to the invasion, the Kremlin represented just 3.11% of global GDP.

To further illustrate, Exhibit A and Exhibit B portray the size of Russia’s economy, population, and percent makeup of the global stock market compared to other countries. Looking at Exhibit A, Russia has the largest population of this subset, yet its economy (the size of the bubble) is smaller than Texas. Thus, the war’s direct effect on global growth was already limited even before indices deemed Russia as “uninvestable” or before western parties imposed sanctions.

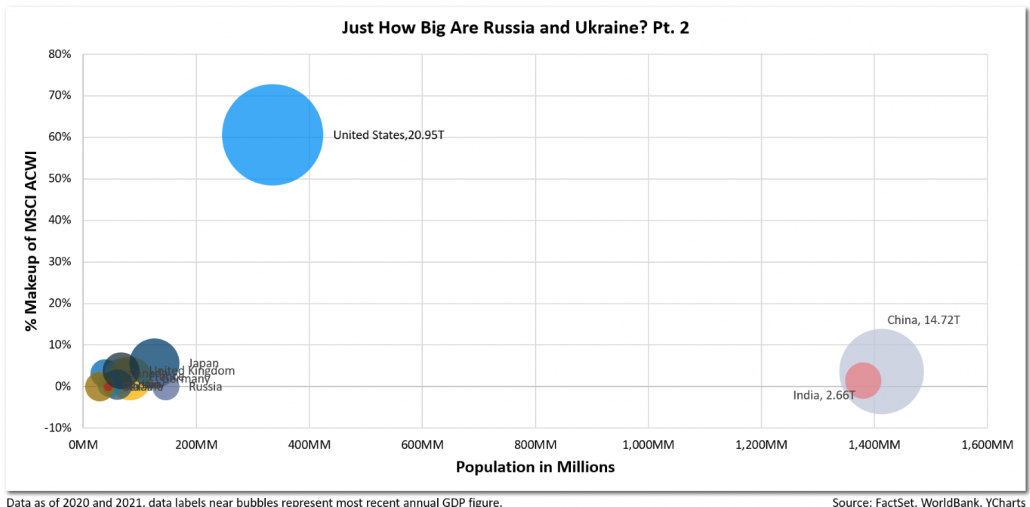

Exhibit A – Russia’s Economy is Smaller Than TexasExhibit B – Russia is Miniscule compared to the US, China, and India

Zooming out in Exhibit B, you can assess just how small Russia is relative to the United States and its Asian neighbors China and India.

The State of the West

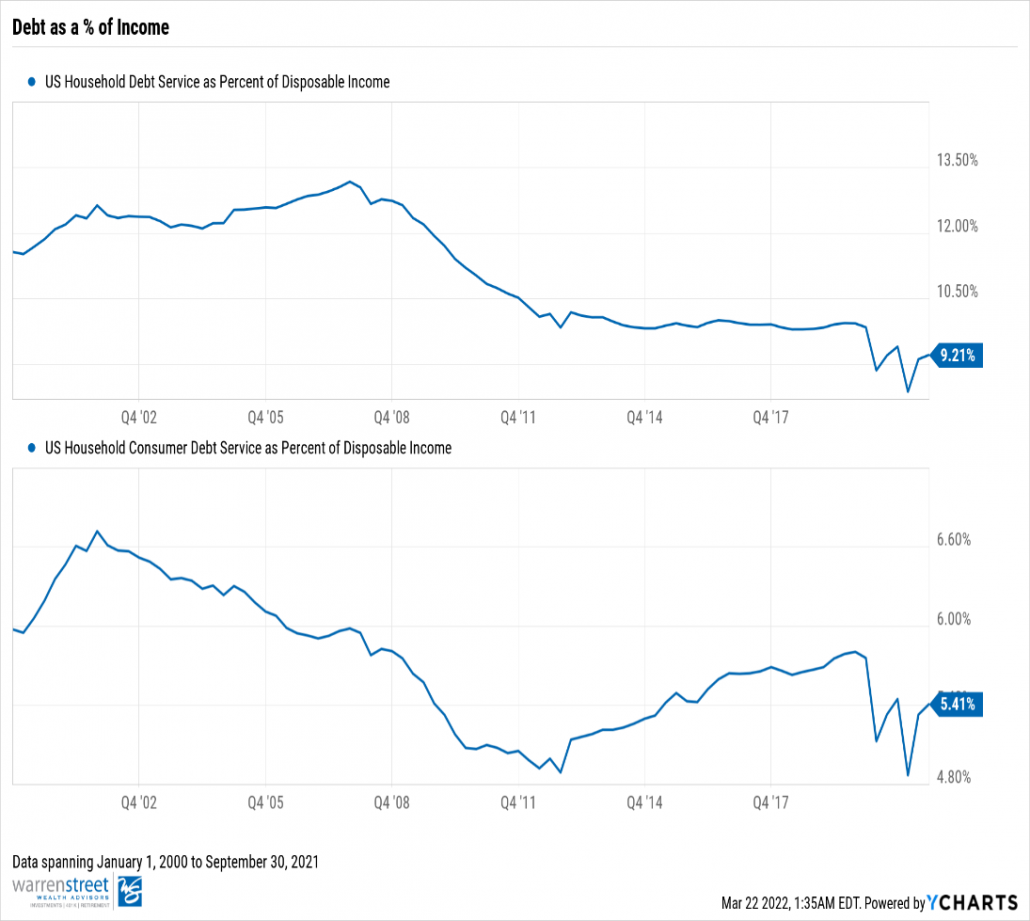

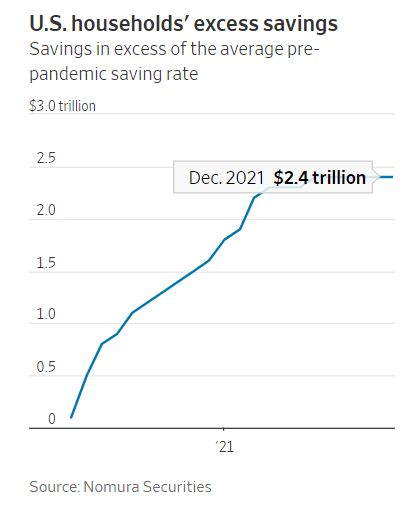

Before discussing other nations, let’s cover our home turf. Within the United States, we have successfully fended off the Omicron wave. COVID-19 data is trending in the right direction, pandemic related pressures (i.e., labor market, car prices) are slowly easing (Exhibit C), and consumer balance sheets are rock-solid (Exhibit D).

Exhibit C: The Labor Market is Loosening, and Inventories are BuildingExhibit D.1: Debt as a % of Consumer Incomes

Exhibit D.2: Consumers Have a Record $2.4T in “Excess Savings”

Although the threats of additional COVID-19 variants and prolonged inflation linger, our economy is expected to produce above-trend economic growth (see Exhibit E). In fact, economists remain optimistic about the US economy, with the median 2022 real gross domestic product forecast only revised 0.10% downwards after the invasion of Ukraine.

Other major economies (particularly in Europe) are more at risk for an economic slowdown attributed to higher energy prices (i.e., over $120/barrel for Brent Crude driven), or what we call “pain –at –the– pump.”

Although Europe derives 40%+ of its natural gas from Russia and Ukraine, we expect that new measures targeting energy independence and militaristic efforts will have positive long-standing effects on European growth despite interim road bumps. For some near-term perspective, European nations are still expected to grow GDP above their long-term forecasts in 2022 (see Exhibit E).

Exhibit E: How Much Are Our Economies Expected to Grow in 2022?

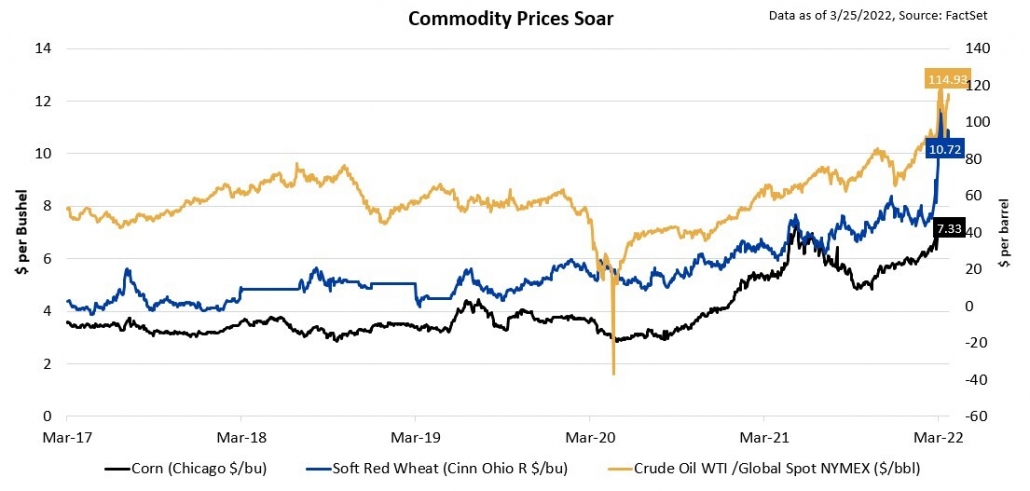

Commodity Chaos – Not to be Overlooked

Although the war’s direct effect on global growth is likely to be meager, indirect pressures on commodity prices are a larger concern, as they may diminish the purchasing power of disposable incomes. Russia is the world’s second largest oil producer behind the US, and accounts for 12% of global production. Also, Russia and Ukraine make –up 25% of global wheat exports, 33% of global corn trade, and 80% of sunflower oil production.

What happens if sanctions are imposed, or if nations surrender agricultural practices to fight on the battlefield? The price of electricity in your factories will rise. Middle eastern nations reliant on wheat imports (i.e., Egypt and Lebanon) must ration appropriately. Chinese-grown hogs – which feed on corn – are more expensive to raise. Lastly, the price of that bag of Ruffles (made from sunflower oil) is expected to increase.

Exhibit F: Commodity Prices Are Rising

Where Do We Go from Here?

Could this lead to inflation? Yes – we have already seen commodity prices surge exponentially. Does this mean that the US economy will fall to its knees? The probability of that is very low.

After all, two-thirds of our nation’s economy is consumption-driven, and with consumers looking healthy and a central bank easing the economy into a higher rate environment, it is hard to envision a full-scale economic disaster unfolding. Even if we run into a recession, perhaps it will be much smaller than our recent lived experiences of the Great Recession and the Great Lockdown (2020 COVID-19 Pandemic).

Our European neighbors will be more vulnerable over the next three months, especially with an energy embargo on Russia still on the table. However, between German Chancellor Olaf Scholz mobilizing its military (for the first time in 20 years), renewed sentiment on energy independence, and a newfound unity amongst the entire West, the European economy is exuberating a different luster and willingness to grow than it did in previous years. Should this war abate, we believe Europe could resume course towards full recovery and investors with allocations will be rewarded.

A Stronger West, Once the War is Put to Rest

Ultimately, our sentiment from part 1 of this series that “We Will Prevail” has not changed. We have endured many instances of short-term pain and come out victorious. This time is no different. I am confident that our economies – particularly the West — will emerge stronger and more united after this war is put to rest.

Stay tuned in part 3 where we discuss asset class performance and portfolio impact!

Phillip Law, Portfolio Analyst

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/03/Social-Graphics-1.png10801080Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2022-03-25 09:00:002022-12-08 09:13:49Part 2: Assessing War and the State of the Global Economy

“There are decades where nothing happens; and there are weeks where decades happen.”

– Vladimir Lenin

The words of Lenin, who led the Russian Revolution in 1917, are ringing true in his own country over 100 years later. Russian Prime Minister Vladimir Putin’s decision to invade Ukraine took the world, and financial markets, by storm. For investors, initial instincts may prompt feelings of worry, and rightfully so.

After all, homes are collapsing, buildings are burning, and civilians are being displaced in what publications are calling the biggest war in Europe since 1945. First and foremost, we empathize with the human concerns and humanitarian disaster resulting from Russia’s full-scale invasion of Ukraine. We believe that a broad understanding of the market’s relationship with geopolitical crises, the state of the global economy, and the war’s impact on broad asset classes will help investors navigate this turbulent time.

This series will aim to address the concerns that arise for investors and global markets during such times.

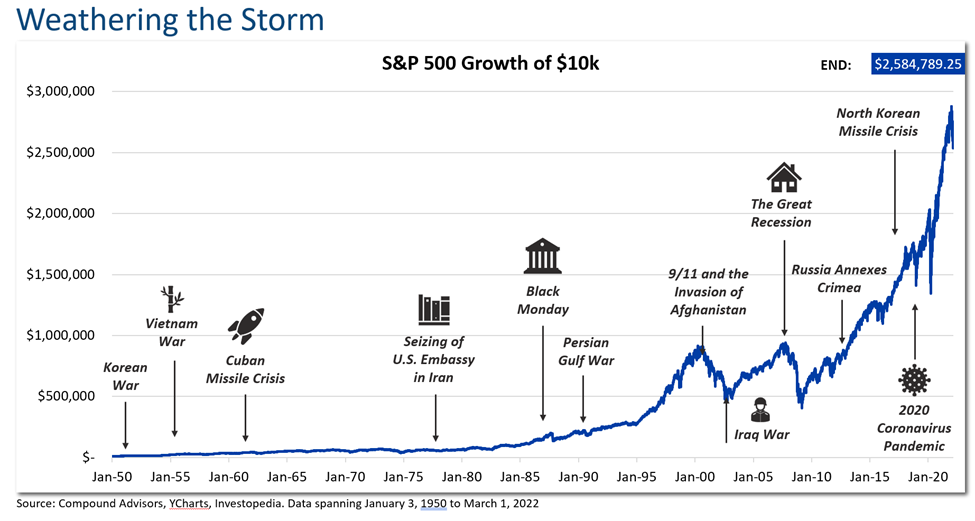

Weathering the Storm

In an era where G20 nations are accustomed to diplomacy, the impact of war on markets may seem foreign. However, we can turn to history to help distinguish relationships between capital returns and warfare. Below is a chart showing the growth of $10,000 invested in the S&P 500 since 1950, overlayed with a myriad of events.

Exhibit A1

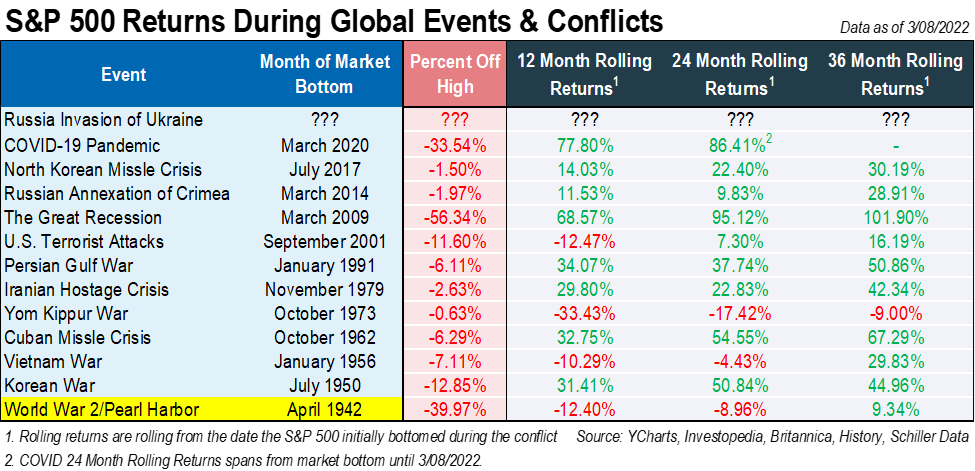

Looking back, the S&P 500 grappled with numerous instances of geopolitical turmoil, nationwide systemic meltdowns, and a global pandemic. Despite these vulnerabilities, notice the trend and direction of that initial $10k: it consistently recovers and grows over time Furthermore, Exhibit B features returns 12, 24, and 36 months after the market bottomed in each war.

Exhibit B

These charts convey two things:

Despite volatile periods, investors have generally been rewarded for putting their capital at risk.

Human beings are incredibly resilient. We’ve lived through arduous events, gritted our teeth, and made it to the other side.

Some people are comparing this conflict to World War II, but we disagree given that the battle is regionally contained and the US is unlikely to become directly involved. The conflict can, and likely will, get worse. But the probability of another world war is low.

The outcome of Russia’s invasion is difficult to predict. Whether Putin succeeds in establishing a puppet government in Kyiv or a ceasefire is negotiated, we have faith that humankind will persevere and that capital will continue to seek the most efficient allocators, leading to long-term positive returns. In other words, we will prevail.

Phillip Law, Portfolio Analyst

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Footnotes & Sources:

Chart is not log-scaled and thus understates market return volatility.

https://warrenstreetwealth.com/wp-content/uploads/2022/03/Blog-Thumbnail.png10801080Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2022-03-17 09:00:002022-06-30 11:08:28Part 1: We Will Prevail

The 2021 calendar year might be over, but that doesn’t necessarily mean that you’re out of luck if you want to make any last-minute tax moves before you file your 2021 return.

While your options may be somewhat limited after December 31st has passed, below are five options to think about as you get ready to file your 2021 taxes.

Traditional IRA

You may still be able to make an IRA contribution for 2021, even as late as April 18th. In order to receive a deduction for your contribution, you’ll want to review your 2021 AGI (Adjusted Gross Income), ideally with a professional. The income limit phase-out range starts at $66,000 for individuals and $105,000 for married joint filers, with exceptions to these limits being available if you do not have access to a 401K or other retirement plan through work.

Another scenario where an IRA contribution can be beneficial is for a recent retiree. Some retirees will receive earned income from their previous employer in the calendar year following their retirement in the form of a prorated bonus or otherwise. This earned income allows the retiree to make an IRA contribution and take the deduction. If this applies to you, be sure to contact your advisor to discuss your options.

If you decide to make an IRA contribution, the maximum amount for 2021 is $6,000 per individual, or $7,000 for individuals age 50 and older.

SEP IRA & Small Business Plans

If you are self-employed you may be able to make a last-minute contribution to a retirement plan as well. The most common type of self-employed retirement plan is a SEP IRA, but depending on your tax situation, a Solo 401K, Defined Benefit plan, or other types of retirement plan may be beneficial for you.

The contribution limit for a SEP IRA in 2021 is $58,000, with no income limitations being applied. That said, the amount you will be able to contribute will be dictated by your self-employment income for the year, so work with your advisor and your tax professional to make sure the contributions are done properly to ensure you are maximizing the tax savings.

Roth IRA

If you are interested in a different type of tax-advantaged retirement savings vehicle, a Roth IRA may better suit your needs. While it does not provide an immediate tax deduction, it does allow you to invest funds in a tax-advantaged manner for the long term. If you meet the requirements at distribution time, all withdrawals will be tax-free.

There are income limits for who can contribute to a Roth IRA. AGI limits start at $125,000 for individuals and $198,000 for joint filers in 2021.

Contribution limits for a Roth IRA are the same as a Traditional IRA – $6,000 per individual, or $7,000 for individuals age 50 and over. This contribution limit is an aggregate for both IRA account types, so between a traditional IRA and a Roth IRA you cannot contribute more than the annual limit in total.

Charitable Contributions & Deductions from 2021

2021 is the last year (pending future legislation) for the “above the line” charitable deduction. In other words, 2021 will be the last year that you will be able to take a deduction for a charitable contribution you made without having to itemize all of your deductions on Schedule A.

In 2021 you can deduct up to $300 per individual, or $600 for joint filers for charitable contributions without itemizing.

If you made charitable contributions in 2021, now is the time to dig up those receipts and provide them to your tax professional.

If you think you may be able to itemize your deductions, be sure to also include mortgage interest, state taxes paid (property, sales, & income), and medical expenses in the information you provide to your tax preparer.

Health Savings Account Contribution

If you participated in an HSA-eligible “high-deductible health plan” in 2021, you may be eligible to make a tax-deductible contribution to a Health Savings Account for 2021 up to the 2021 tax filing deadline (April 18, 2022). Contribution limits are $3,600 for individuals and $7,200 for families, with a $1,000 catch-up contribution available for taxpayers age 55 and older. Contributions to HSAs are tax-deductible and withdrawals are tax-free if the funds are used for qualified medical expenses.

In conclusion, there are still some strategies that can be utilized when it comes to filing your 2021 taxes. If you have yet to make a decision on any of the above, there is still time before you file your return.

If you are interested in learning more about any of the above or taking any action, be sure to reach out to your advisor at Warren Street to get the conversation started.

Justin Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2022/02/Blog-Thumbnail-1.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2022-02-24 08:30:002022-06-30 11:03:115 Options for Last Minute 2021 Tax Moves