This is a follow up to our first piece https://warrenstreetwealth.com/relief-is-on-the-way-a-cares-act-overview/ so if you have not yet read this first blog, please do so as this is a follow up to it.

With frequent updates from Washington and elsewhere regarding the policy response to COVID-19, we will continue to provide you with summary updates. Please reach out to us with any questions you might have.

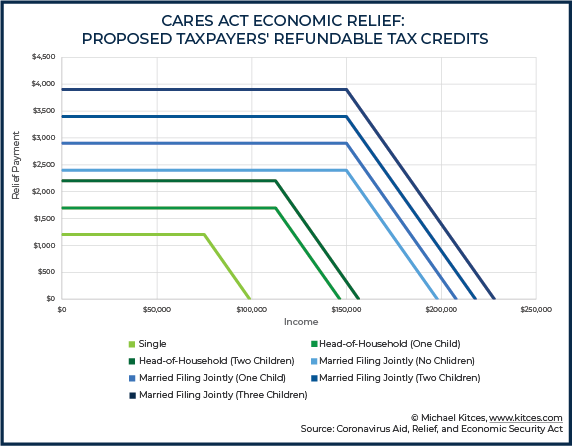

CHECKS

Many of you have received your stimulus checks via direct deposit. If not, here is some additional information.

If you did not file a 2018 or 2019 tax return, but are still eligible for a stimulus check, you can enter your information into this IRS website to receive your check:

Non-Filers: Enter Payment Info Here

If you did not request direct deposit on your 2018 or 2019 tax return, but you would like to receive your stimulus check via direct deposit, you can enter your direct deposit information on this IRS website:

Get My Payment

It has been reported that both of the websites above have experienced technical issues since being launched, so patience and perseverance may be required.

If you prefer to receive your stimulus payment by paper check, you may have to wait several weeks for the payment to arrive.

TAXES

The Treasury Department and IRS have delayed the Federal tax filing deadline for 2019 taxes to July 15, 2020.

California, along with most states (though not all), has conformed to the Federal deadline.

2020 Q1 and Q2 Federal estimated taxes are also now due July 15th.

SMALL BUSINESSES

There are several updates regarding small business relief offered in the CARES Act.

1. EIDL

Originally the CARES Act called for the SBA to offer one-time emergency grants of $10k per business through the EIDL (Economic Injury Disaster Loan) program. Many of our small business owner clients applied. Recently, the SBA released an email to EIDL grant applicants, announcing that due to high demand, they’ve limited the one-time EIDL grant to $1k per employee (with a maximum of $10k total).

2. PPP

The demand for PPP (Paycheck Protection Program) loans has been extremely high. So high, in fact, that just 14 days after the program opened, the SBA announced that it had committed all of the originally allotted $349 billion. As of Friday, April 24th, Congress and the President approved an additional $310 billion in funds for the program which offers potentially forgivable loans for small businesses and non-profits. We expect this second round of funding to go quickly, so please reach out to us for guidance if you have not yet applied. $60 billion of the new funding was specifically set aside for loans made by smaller institutions like credit unions and community banks, so we recommend considering one of these options first.

3. Main Street Lending Program

Another relief option for small to medium sized businesses (up to 10,000 employees) may be the Federal Reserve’s new Main Street Lending Program:

Main Street Lending Program

Details of the program are still being clarified, but as of this writing, here are some highlights:

- Borrowers who received SBA PPP loans are eligible to apply for the MSLP as well.

- Unlike PPP loans that can be potentially forgiven, MSLP loans do not offer a forgiveness provision.

- Current proposed terms are 4 year repayment, $1 million minimum loan size, principal and interest payments are deferred for one year, relatively low interest rates.

- Several other restrictions apply. If you are a small or medium size business owner in need of funding, please reach out to us for further discussion.

CHARITABLE GIVING AND WAYS TO HELP

Food banks around the country have seen increased demands over the last several weeks. If you are looking for a way to help, you might want to check with your local food bank.

The Red Cross is also reporting a severe blood shortage as a result of donor cancellations across the country.

This concludes our quick update. News is flowing rapidly and changes to some of this information are inevitable. We will continue to provide updates, but please contact us with any questions, comments or concerns. Wishing you health and safety during these unprecedented times.

As such, before proceeding, please consult with us and other appropriate professionals, such as your accountant, and/or estate planning attorney on any details specific to you. Please don’t hesitate to reach out to us with your questions and comments. It’s what we are here for.

Emily Balmages, CFP®, CRTP

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

If you have questions about any of this or would like to schedule a complimentary review you can Contact Us or call 714-876-6200 to book a free consultation.

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.