Gold Rush of 2020

In 1848, thousands of people grabbed their shovels and crossed land and sea to Sutter’s Mill with hopes of striking gold. Almost 150 years later in 2020, a similar parallel is happening not in San Francisco, but rather in the investable market for this hot commodity.

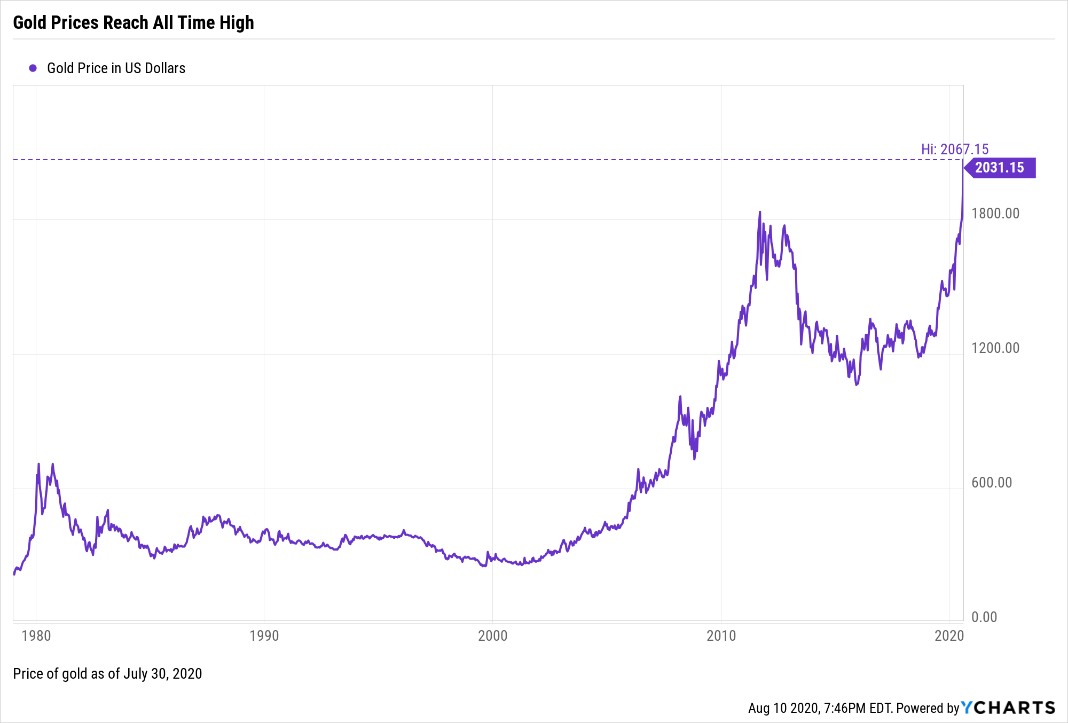

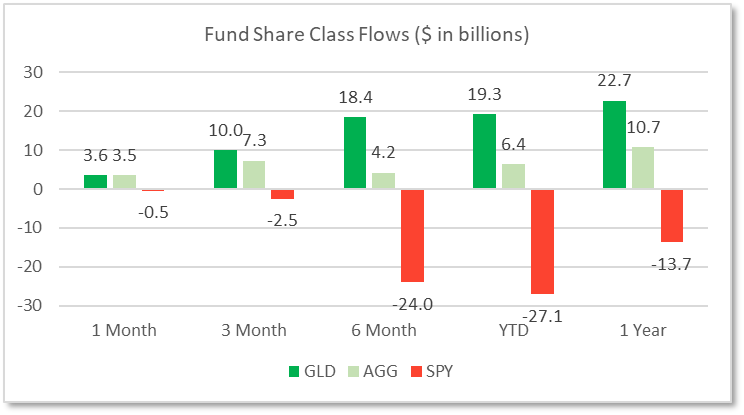

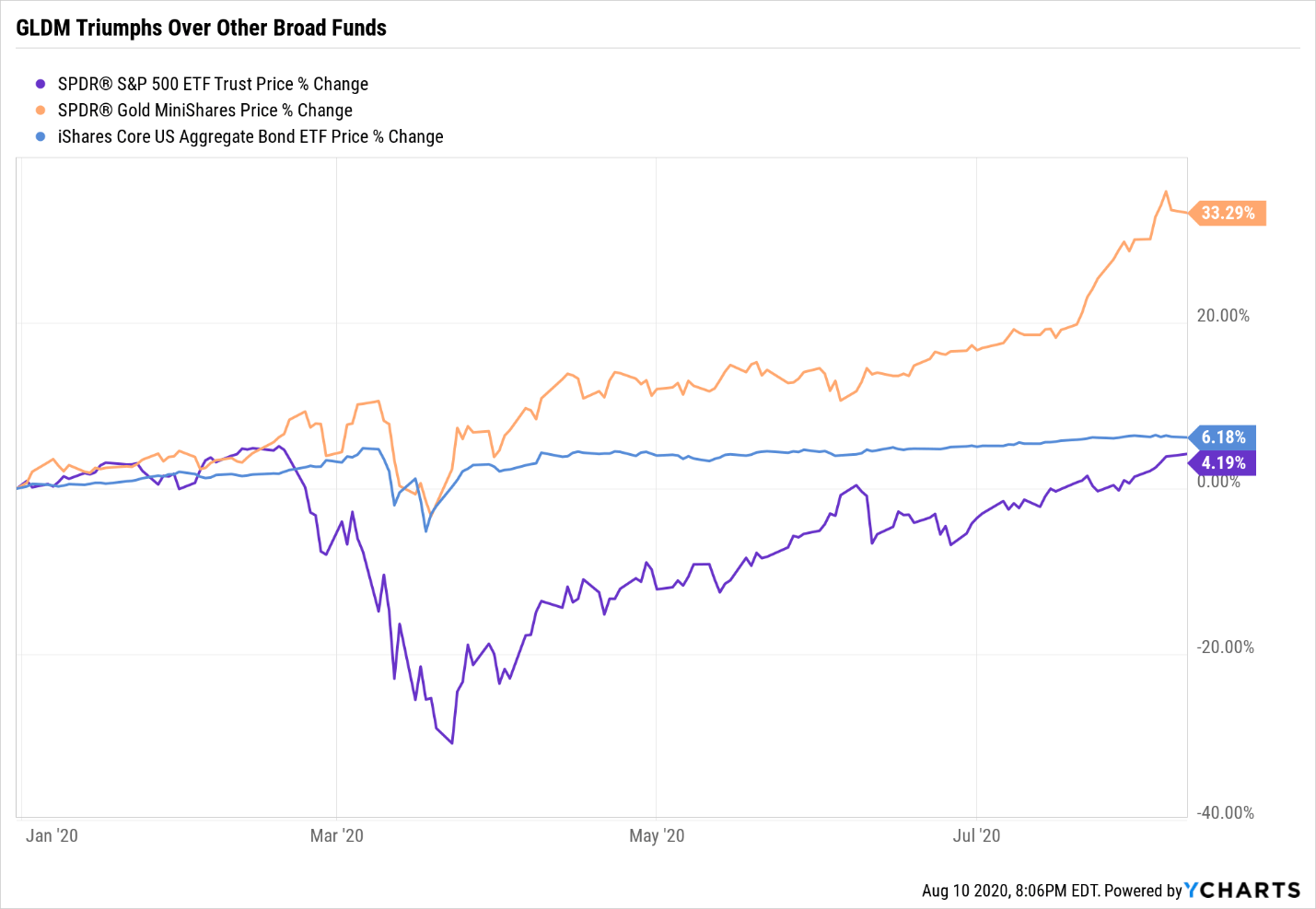

Year-to-date (YTD), gold has experienced more inflows than other broad stock and bond funds, including SPY and AGG which track the S&P 500 and Barclay’s Aggregate Bond Index, respectively. Amongst a myriad of asset classes, investors are choosing gold as their choice for safekeeping, thus driving gold prices to an all-time high. This year alone, gold is up 33.53% YTD compared to U.S. Stocks at 4.69% YTD and U.S. bonds at 7.83% YTD. But why exactly is a gold rush taking place in 2020?

Source: YCharts

Data as of 8/05/2020

You may attribute the surge in gold prices to the pandemic, but mine deeper and you will find more.

Source: YCharts

Data as of 8/05/2020

Source: YCharts

Low Yield Environment: Earlier in March, the Federal Reserve cut the federal funds rate to 0 – 0.25% to stimulate the economy amid an economic crisis. As a result, treasury yields fell drastically. The 10 Year Treasury rate started the year at 1.88% and now only yields an all-time low of 0.52%, or -1.05% adjusted for inflation. Although treasuries are often used as a safe haven during uncertain times, negative real yields alongside inflation expectations might make gold a more attractive store of value.

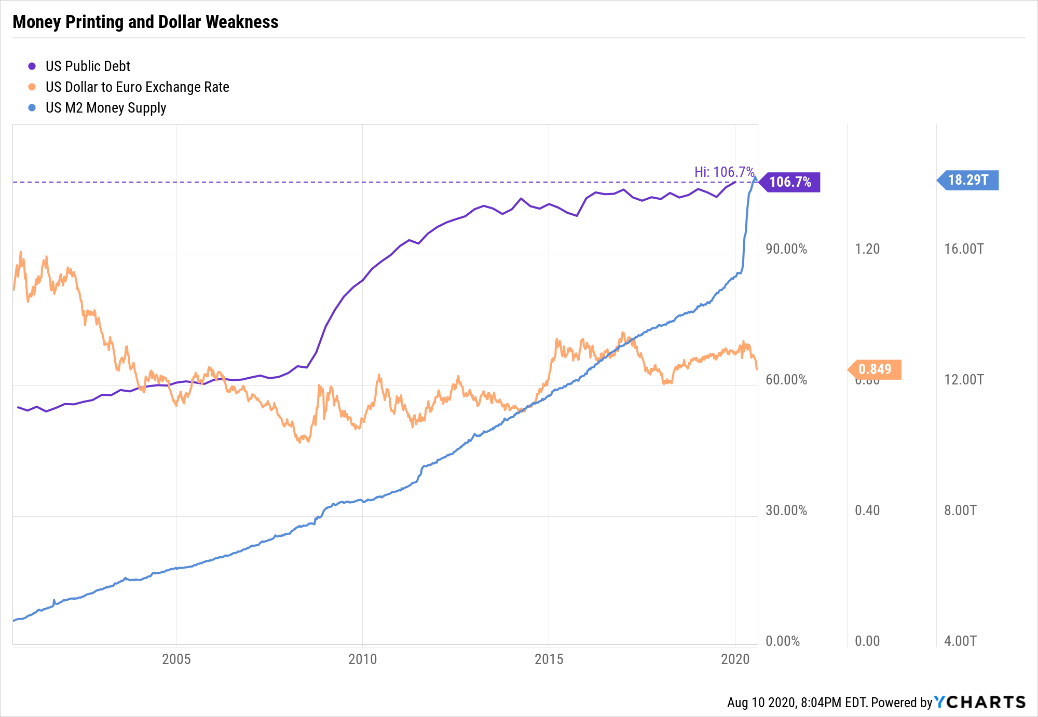

Inflation Expectations: Fiscal stimulus through a $2.2 trillion package, rapid money printing, and unprecedented quantitative easing has prompted investors to seek gold as an inflation hedge. Current levels of inflation, however, do remain low at 1.19% year-over-year relative to the Fed’s target of 2.0%, and are likely to stay low in the short term (due to aggregate demand and supply shocks). While there is no tell-all sign indicating future long-term inflation is upon us, the following is certain: whether gold investors are overreacting or whether U.S. inflation is a ticking time bomb remains to be seen.

A Weakening U.S. Dollar: With fiscal debt as a percentage of GDP and M2 Money Supply at an all-time high, confidence in the U.S. dollar is diminishing relative to other currencies including the Euro. This comes at a time where the European Union appears to maintain a tighter grasp on COVID-19 outbreaks, alongside newfound unity in the form of a centralized stimulus package and debt mutualization. Overall, supposed weakness in the U.S. dollar has turned investors towards gold to maintain the purchasing power of their greenbacks.

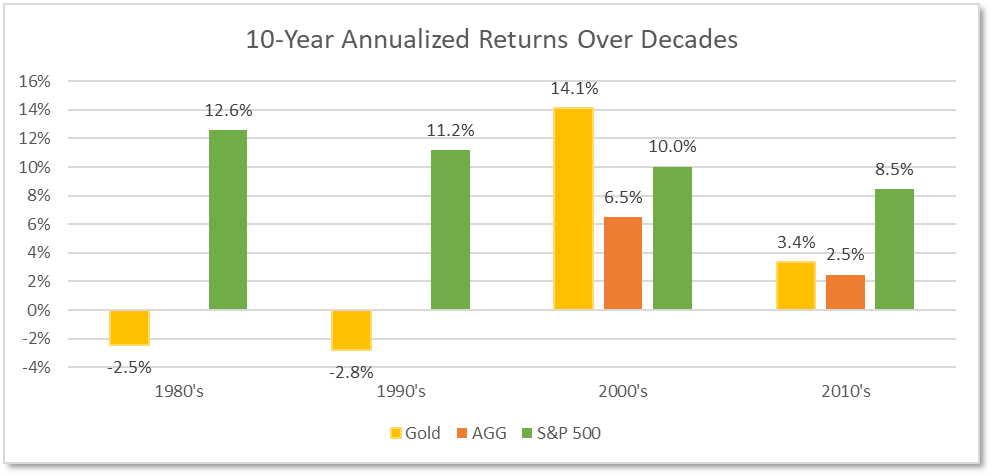

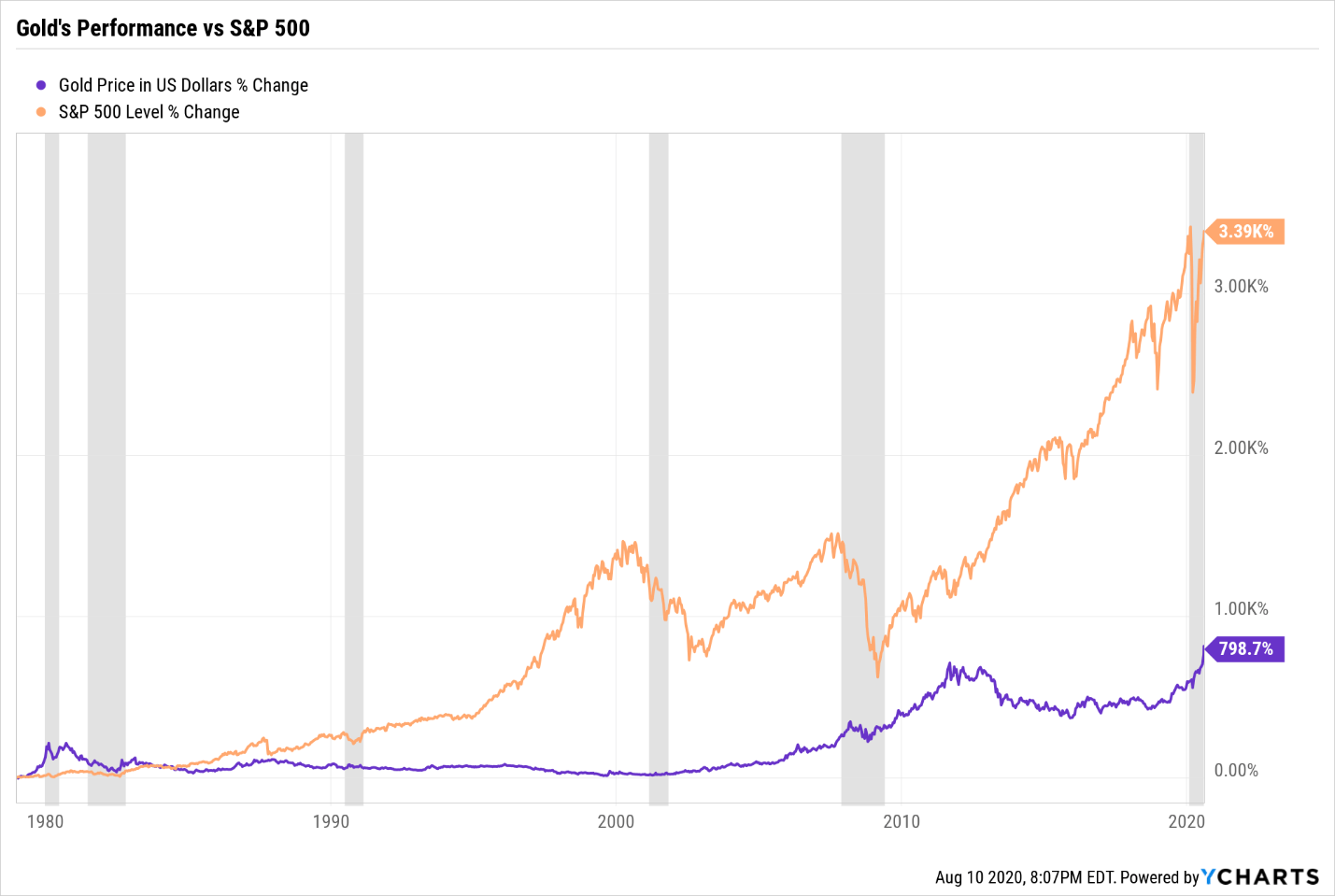

With this context, it seems like anyone would jump at the chance to own gold; but to avoid grabbing a handful of pyrite (fool’s gold), let’s evaluate gold’s performance and properties as an asset class. During the 1980’s and 1990’s, gold yielded less than ideal returns. In the late 2000’s, the metal’s performance accelerated as investor confidence faltered during the Great Recession, but subsequently dipped in the 2010’s when the U.S. economy proceeded onto its longest economic expansion.

Source: YCharts

Data spanning 1/01/1980 to 12/31/2019

Based on history, we can draw two conclusions: 1) gold’s volatile nature indicates that its current run may not be sustainable over long periods of time and 2) gold’s performance suffers when investors regain confidence and begin to adopt a risk-on posture. To see gold’s performance coming out of recessions, see Appendix A. (link)

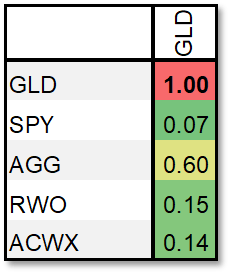

5-Year Correlation Matrix (Rolling Monthly Returns)

Data as of 8/07/2020

Source: YCharts

Gold generates zero passive income, so why do investors hold it? One reason is simply because it’s different and provides a diversification benefit. This metal exhibits less correlation compared to broader asset classes, meaning it simply behaves differently. A correlation of 1 indicates that the assets’ return behaviors are identical, while a correlation of -1 means they move in completely opposite directions. Given gold’s weaker correlations, it is likely to thrive when stocks or other asset classes experience large drawdowns. In other words, gold zigs while others zag.

Having understood the nuances of gold as investable asset and its diversification benefit over a long-time horizon, Warren Street Wealth Advisors previously made the decision to maintain gold exposure through Gold Minishares (GLDM) in our Diversifiers sleeve. Our investment strategies are now reaping the benefits of gold’s recent rally and allow for different courses of action. For example, with current gold prices bid up relative to historical levels, we can trim profits to invest in cheaper assets classes with higher potential for appreciation. This in essence, is buying low and selling high.

Gold prices will likely stay in the headlines and continue to gain traction in coming months. Regardless, we encourage you to start with your long-term asset allocation in mind and refrain from overthinking market entry/exit timing on any specific asset class. Preventing permanent capital impairment and building portfolios for your short term and long-term needs remains our top priority. We will diligently tax loss harvest and perform recurring rebalances along the way to take advantage of tactical long-term opportunities we see appropriate. That to us, is striking gold in 2020.

Appendix A:

Phillip Law

Portfolio Analyst, Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.