A few years ago, ads from financial services companies asked, “What’s your number?” The “number” represented the amount of money you needed to retire comfortably. There are, of course, various approaches to estimating your retirement “number,” all of which are influenced by your goals and factors, such as your expected retirement age and the lifestyle you hope to maintain in retirement. So, while this question may have been an effective way to spark conversations about retirement, we believe that it doesn’t paint the complete picture.

Retirement isn’t just about reaching a specific monetary goal. It also involves creating a comprehensive strategy that looks to optimize your various savings vehicles, each playing a different role in your retirement income approach. It also means factoring in healthcare costs, thinking about the legacy you wish to leave, and being flexible enough to adapt to life’s unexpected twists and turns. Ultimately, your strategy needs to consider how your assets will work together to fund the retirement you envision.

An essential part of orchestrating your retirement income strategy is determining which assets to take and in which order.

There is no one-size-fits-all answer, but some general guidelines can help when you are starting to think about a withdrawal strategy.

For example, one approach to consider is withdrawing money from taxable accounts first, then tax-deferred, then tax-exempt. By using taxable money first, you can avoid paying taxes as long as possible with tax-deferred investments. And your tax-exempt accounts remain tax-exempt for a longer period. Ultimately, your decision will be influenced by a wide range of other considerations, including withdrawal fees, surrender charges, and other costs that may be associated with each specific account. But when possible, consider using the power of tax deferral and tax exemption to your advantage.

Regardless of your age or financial position, having a well-thought-out retirement strategy is one of the most critical actions you can take. If you would like to review your current strategy, please contact our office. We’re here for you!

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/02/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2026-02-06 10:58:592026-02-06 10:59:05How Much Do I Need to Retire in 2026?

If you’re a business owner, you’ll eventually step away from the company you’ve built. You might cash out to the highest bidder or work out a deal to sell the business to the next generation of your family or even to employees. The question is will you be able to make this transition on your own terms? The reality is that most business owners don’t have a clear, documented exit plan. And if you find yourself among them, you could find it leaves you in a tight spot when it’s time for you to step down.

Delaying planning your exit risks settling for a below-market sale price, losing control of choosing your successor or rushing into choices that don’t reflect your vision. Delays also leave you with little time to take steps to boost the business’s valuation and ensure business continuity. A clear exit plan helps maximize options and value. If you haven’t mapped out yours yet, there’s no time like the present. Consider these steps:

Put a Price on Your Business

Proper valuation of your business is the first step in exit planning. Some back-of-the-envelope math can provide a decent starting point. But to really understand what your business is worth, meet with a valuation expert. Besides a healthy dose of objectivity, these professionals bring market expertise and a knowledge of valuation standards. They can identify intangible sources of value you may have overlooked and help ensure your valuation passes muster with potential buyers and the IRS.

There are three main approaches to determining value:

The asset approach adds up the value of your company’s tangible and intangible assets, then subtracts liabilities.

The income approach calculates value according to your business’s expected future cash flows.

The market approach compares your business to recent sales of similar companies.

You may find one approach is more apt than another for the type of business you own, but a comprehensive valuation is likely to incorporate all three in one way or another. Bear in mind that valuation isn’t a one-time event. As your business grows and market conditions change, you’ll likely want to update your valuation.

Clarify Your Vision

Before you can build an effective exit plan, it’s necessary to clarify your goals. Be as specific as possible as you define what a successful transition looks like to you.

Some questions to keep in mind: Do you want to maximize the sale price, selling at the highest price possible? Do you intend to keep the business within your family or pass it to a handpicked successor? What are your obligations to employees? Is it important that your business maintains a consistent set of values when you’re gone? What timeline makes sense for you? How involved—if at all—do you want to be with the business after you exit?

The answers to these questions will guide the decisions that follow. They can be deeply personal, and we’re here to be a resource as you consider what’s truly important to you.

Shape Your Exit

With valuation and goals in hand, there are a range of steps you can take to support your transition. What you do will depend largely on the type of exit you’re planning. For some owners, you might make strategic adjustments to boost the value of your business, such as reducing unnecessary expenses or diversifying revenue streams to make your company more attractive to buyers.

If your plan involves transferring the business to a family member or a long-time employee, the sooner you identify them, the better. That way you’ll have plenty of lead time to train them in the leadership skills necessary to provide a smooth handoff. Depending on your situation, you might consider a sale, a gift or a combination of the two. Be aware that gifts to family members above the lifetime gift and estate tax exemption ($15 million for individuals in 2026) might trigger gift taxes. Meanwhile, sales to employees could trigger capital gains taxes. If your business is structured as an S corp or C corp, you might consider an employee stock ownership plan (ESOP), which could defer or even eliminate capital gain taxes if structured properly.

Seeking an external buyer? Preparation is equally as important. In addition to boosting your valuation, you’ll need to organize your financial records, legal documents, contracts, employee agreements and operational procedures. One thing to consider is the type of deal structure that works best for you: Would you like to be paid over time or in one lump sum? And would you like to exit the company immediately or would you be open to staying on in an advisory capacity to help the new owner learn the ropes?

Begin the process of finding and vetting buyers early. These could be industry competitors, investment groups or individual entrepreneurs who may be a good fit. A business broker can help you identify potential buyers and spread the word through their network.

Charting the Future

For many business owners, exit planning rarely tops the to-do list. After all, there are plenty of day-to-day demands competing for attention, let alone the fact that it can be difficult for owners to think about the day they’ll no longer lead the company they built. Yet the most successful exits are those planned in advance, allowing owners to optimize value, identify an ideal buyer or successor, and prepare their employees for a smooth transition.

If you’d like to start a conversation about exit planning, we’d be happy to help you explore your options, develop a strategy that meets your financial goals and protects your legacy. here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/11/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-11-07 08:52:472025-11-07 08:52:58Business Exit Strategies on Your Terms

Retirement is a major life shift, one that impacts more than just your schedule. It can reshape your sense of identity, daily habits and even your health. In fact, research has shown that retirement can raise the risk of heart disease and other medical issues by up to 40%. The reason? Experts point to a loss of purpose and reduced social connection, both of which can take a toll on mental and physical well-being.

Without a plan for how to spend your time meaningfully, the transition can bring unexpected emotional challenges.

The Risks of Unstructured Retirement

Many retirees begin this new chapter with a “honeymoon phase”—a period marked by the novelty of free time, relaxation or long-awaited travel plans. But this initial high can eventually fade.

When the excitement of sleeping in and checking items off the bucket list wears off, retirees can find themselves facing unexpected emotional challenges. Common struggles include boredom, loss of routine, identity shifts and social isolation. In fact, 24% of older adults are considered to be socially isolated. Isolation can also have a ripple effect on health: It’s associated with a 50% increase in risk of developing dementia and increased risk of premature mortality.

Designing a Retirement with Purpose

To avoid some of the potential pitfalls of an unstructured retirement, it’s important to think carefully—and proactively—about purpose. What do you want this next phase of life to look and feel like? Beyond financial planning, consider how you’ll meet the deeper needs your pre-retirement life—including work and raising kids—may have fulfilled: structure, identity, accomplishment, social connection and a sense of meaning.

What brings you pleasure and meaning? What have you always wanted to try or learn? Pursuing these activities can provide purpose and help ensure retirement’s not just a long vacation, but a rewarding chapter of your life.

Feeling stuck here? Try asking close friends or family what they see light you up. Often, others can reflect back passions or strengths that are hard to see on your own.

Staying Connected and Active

Relationships and physical routines matter more than ever when you retire. Staying active, both physically and socially, offers measurable health benefits. Regular physical activity lowers risks, including the likelihood of dementia, heart disease, stroke and eight types of cancer.

People-centered activity is important, too. Look for ways to stay engaged, whether through volunteering, mentoring, part-time work, creative pursuits or community involvement. Older volunteers, aged 55 and up, who gave 100 hours or more each year were two-thirds less likely to report poor health than non-volunteers.

Spending more time with family is a high priority for many retirees and can be a great way to fulfill social needs. But make sure that vision is shared. Open conversations with loved ones about time together, expectations and boundaries can help align plans and avoid disappointment down the road.

The Retirement Identity Shift

In many ways, it’s hard to define what retirement is. After all, it’s not a single moment but a series of transitions. For instance, rather than an abrupt shift to not working at all, you may consider bridge employment—usually part-time work in a temporary position or as a consultant in your field or in a different industry. This can offer a gradual shift into retirement, providing continued income and engagement as you adjust.

As your vision for retirement evolves, keep us in the loop. We’d love to hear what you’re planning—and we’re here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-5.png11522048Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-09-26 07:38:002025-10-07 16:02:46The Power of Purpose in Retirement

Welcome back to A Few Minutes with Marcia. My name is Marcia Clark, senior research analyst at Warren Street Wealth Advisors.

Today we’re going to spend a few minutes considering the pros and cons of the Federal Reserve Open Market Committee holding short-term interest rates steady at its June meeting. Most of my comments today are based on the FOMC announcement published on June 19, the press conference with Chairman Jerome Powell shortly thereafter, and remarks by Federal Reserve Governor Lael Brainard on June 21st.

Watch:

On June 19, the Federal Reserve Open Market Committee announced its decision to keep short-term interest rates unchanged at 2.25%-2.5%. Did they make a mistake?

To answer this question, let’s put ourselves in the shoes of the Fed and attempt to base our opinion on the available data. The Fed should reduce rates if they see the economy struggling. Is that what they see?

During a speech in Cincinnati on June 21st, Fed Governor Lael Brainard stated his assessment that the most likely path for the economy remains solid. He noted strength in consumer spending and consumer confidence, as well as unemployment at a 50-year low.

He did note a few areas of concern: cautious business investment due to policy uncertainty, slow growth overseas, and muted inflation.

Mr. Brainard said: “The downside risks, if they materialize, could weigh on economic activity. Basic principles of risk management in a low neutral rate environment with compressed conventional policy space would argue for softening the expected path of policy when risks shift to the downside.” But what does he mean by ‘compressed conventional policy space’?

The Fed has limited room to maneuver because interest rates are already low, and inflation and employment have not responded to changes in interest rates as predictably as they have in the past.

On the plus side, this means the labor market can strengthen a lot without an acceleration in inflation

On the other hand, this low sensitivity along with already low interest rates gives the Fed less ability to buffer the economy in a downturn

If the Fed doesn’t get their interest rate call right, the economy could begin to spiral too far up or too far down.

Let’s take a deeper look at why low interest rates present a challenge for the Fed.

In the past, the Federal Reserve has cut interest rates 4 to 5 percentage points in order to combat past recessions

The chart on slide 6 shows the current Fed Funds rate sitting at less than half where it was before the last two recessions.

Clearly there is less room to run if a recession hits

The chart also shows GDP beginning to stabilize at the end of 2016. With GDP on a more steady path, back in 2017 the Fed started raising short-term interest rates toward a more normal level in order to have some ‘dry powder’ for the next recession.

How did we get to this delicate balance point?

In December 2018, the Fed said more rate hikes were appropriate given the strengthening economy. The stock market reacted badly as at the same time trade talks with China were going nowhere and portions of the Treasury yield curve were inverted. Recession fears were on everyone’s mind.

In March 2019, Federal Reserve officials reassure markets that they will be “patient” with increasing short-term interest rates. To quote the FOMC statement after the March meeting: “the case for raising rates has weakened…” Notice that they didn’t say the case for cutting rates has strengthened.

And in June, the FOMC held interest rates steady and stated that the current level of interest rates is consistent with its mission to promote full employment and price stability. In its post-meeting statement, the committee said that the timing and size of future adjustments will be based on economic conditions relative to these two objectives.

After the announcement, both stocks and bonds reacted positively to the decision, with the stock market indexes touching new highs before falling back a bit at the end of the week.

Commentators speculated that the markets reacted well because a rate cut could be imminent. Equally likely, however, is that the markets reacted to the lack of a rate hike and prospects that a recession is not around the corner.

During a press conference after the announcement, Fed chairman Jerome Powell responded to a question by saying that being independent of political pressure or market sentiment has served the country well and would do so in the future. He stated that the FOMC will react to data and trends that are sustainable rather than individual data points that can be volatile.

But despite all the evidence, as we approach the end of June an astonishing 100% of futures investors are betting on a rate cut in July. These investors are wrong.

Why am I so sure they won’t cut rates when commentators and the futures market clearly think differently?

You may have heard the expression ‘pushing on a string’. What this means is that applying force to something with no rigidity won’t have any impact – the string absorbs the force and the force doesn’t go any further. This is the current situation with monetary policy.

Imagine pushing a sofa across your carpeted living room versus pushing a mattress across the same room.

Once the feet of the sofa get out of the dent they made in the carpet, the sofa will move fairly easily. That’s because the sofa is rigid – when you apply force at one end, the sofa moves away from the force.

But a mattress is much more resistant to shifting. That’s because much of the force you apply is absorbed by the cushioning already in the mattress. The mattress will often bend before it will move. The force doesn’t go anywhere or accomplish anything.

The current U.S. economy is like the mattress in this example. The U.S. economy has plenty of available capital and interest rates are already low. Reducing the Fed Funds target from 2.375% to 2.00% is unlikely to accomplish much other than encouraging unwise borrowing and ultimately sparking inflation.

Yes, bad things can happen to our economy and the Fed needs to guard against a recession. But a recession overseas is much more likely than in the U.S., and no U.S. recession has ever been caused by a recession overseas. Dropping interest rates to ease market concerns or satisfy political sentiment is not the Fed’s mandate and would be counterproductive.

Barring some catastrophic political event or natural disaster, the U.S. economy is unlikely to falter between now and mid-July.

Recognizing the Fed’s dual mandate of stable prices and full employment are both being met at the current level of short-term interest rates, right now the downside risk of lowering rates outweighs the potential stimulus benefit. The FOMC should keep the Fed Funds rate steady when they meet in July.

This has been ‘A Few Minutes with Marcia’. I hope you are a bit clearer on how to assess the likelihood of Fed policy decisions going forward. As always, comments and questions are welcome!

Marcia Clark, CFA, MBA Senior Research Analyst Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.

DISCLOSURES

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications.

Form ADV available upon request 714-876-6200

https://warrenstreetwealth.com/wp-content/uploads/2018/12/nick-fewings-647669-unsplash.jpg26884032Marcia Clarkhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgMarcia Clark2019-07-08 23:36:112019-08-09 20:28:39Did the Fed make a mistake? – “A Few Minutes with Marcia”

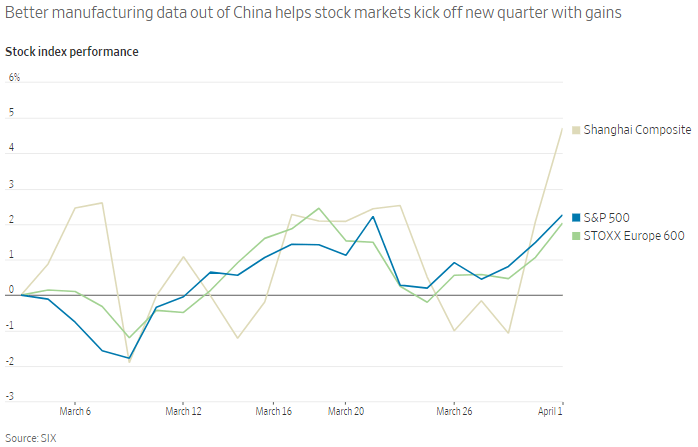

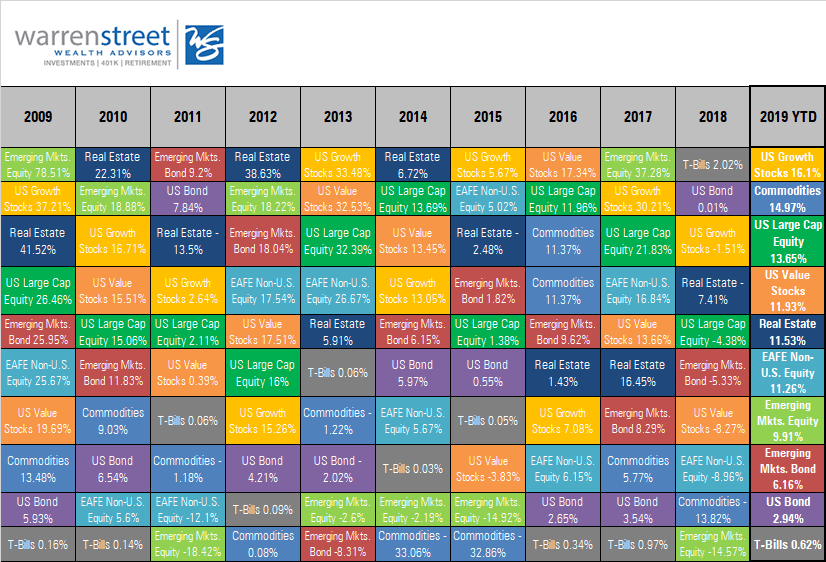

The rally in U.S. stocks slowed in March but still posted the best 1st quarter in recent memory at 13.65%, though stock markets remain volatile as investors seem to overreact to fears of the Fed increasing interest rates too much or not increasing rates at all

A slightly better-than-expected jobs report for March helped calm fears about mixed economic data in the U.S., supporting the Fed’s decision to keep short-term interest rates low for the foreseeable future

The OECD lowered its forecast for European GDP growth to a paltry 1.0% in 2019 and 1.2% in 2020; German government bonds fell into negative territory after the ECB reported weak manufacturing data

Overall, improved labor conditions, lower headline inflation, and accommodative monetary policy should help support real income growth and household spending in most developed countries

Conclusion: Recent market swings seem driven more by fear than by fundamentals. Economic data isn’t great, but the data doesn’t support a forecast for a global recession; U.S. markets are likely to hang on to gains until or unless weakness in the economy becomes more clear.

Is the U.S. economy getting better? Or getting worse?

The S&P 500 had its best 1st quarter return in recent memory, yet the Federal Reserve Bank kept interest rates low to avoid derailing the economy. Which of these forward-looking indicators is correct? To answer this question, let’s start at the beginning. You may have learned in school that GDP – the primary measure of economic strength – is simply the value of all goods and services sold in a country over a given period of time. In essence, GDP represents the value of business transactions. These transactions flow into company financial statements and impact the ability of these companies to pay dividends or launch new ventures. This increased cash flow is recognized by investors, who become willing to pay more for shares of those businesses in the stock market, pushing stock prices up. If the economy is up, stock prices are up too.

Easy, right? All the dominoes line up and we understand how the market works…or maybe not?

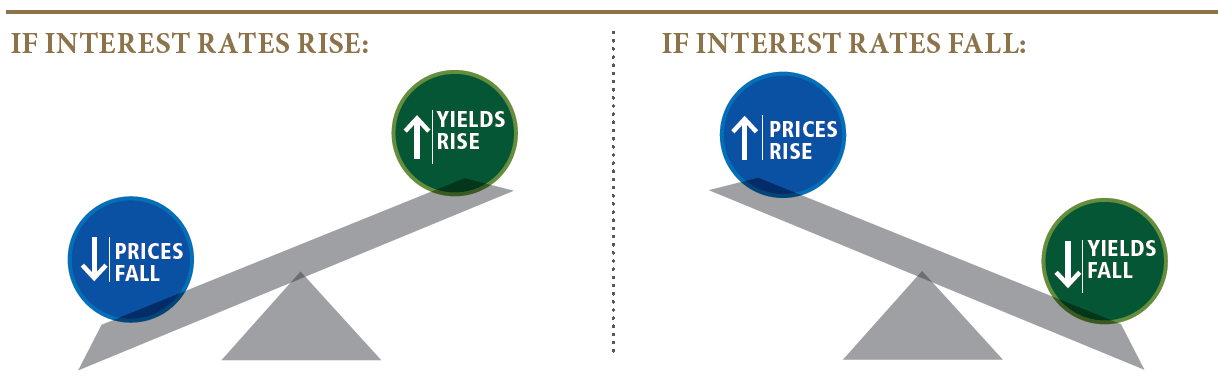

Here is the conundrum: stock prices are a ‘leading economic indicator’ because investors buy today expecting gains in the future. Interest rates are also leading indicators because investors need to forecast future interest rates – which typically move up and down with economic activity – before they’re willing to tie up their money for 10 or 20 years. Stock and bond prices don’t usually go up together.

If interest rates go up, prices of existing fixed-rate bonds go down in order to compete with new bonds issued with higher coupon (interest) rates. But rising interest rates usually indicate more demand for funds, which is often associated with a strong economy, which means more profits, and consequently higher stock prices.

The upshot of all this is when stock prices go up, bond prices are usually flat or negative. Conversely, when stock prices go down, bond prices are usually positive as investors sell volatile stocks and seek safer assets such as government bonds.

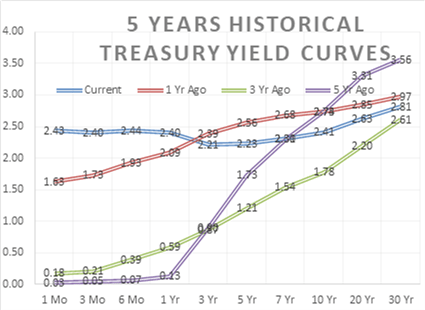

As you can see from the chart above, bond prices as represented by the long-term Treasury ETF (ticker ‘TLT’ – blue line) usually go up when stock prices go down (represented by the Dow Jones Industrial Average – black line), and vice versa. This effect was particularly dramatic during the 4th quarter of 2018.

Despite the strong start for stocks in 2019, if you look back 6-months from October to March, bonds have been among the best performing asset classes. Bonds may not be sexy, but they sure are welcome when markets get rough! But wait – look at the red box in February and March. Bond and stock prices are moving together. Why??

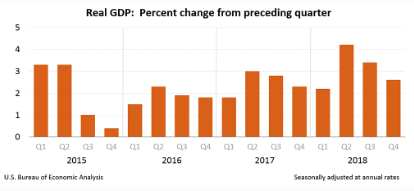

The charts below from the Bureau of Economic Analysis may hold some of the answers. In a nutshell, the problem is Change. And I don’t mean the kind of change you find in your sofa cushions…

Chart 1: The U.S. economy is growing, but slower than in recent quarters.

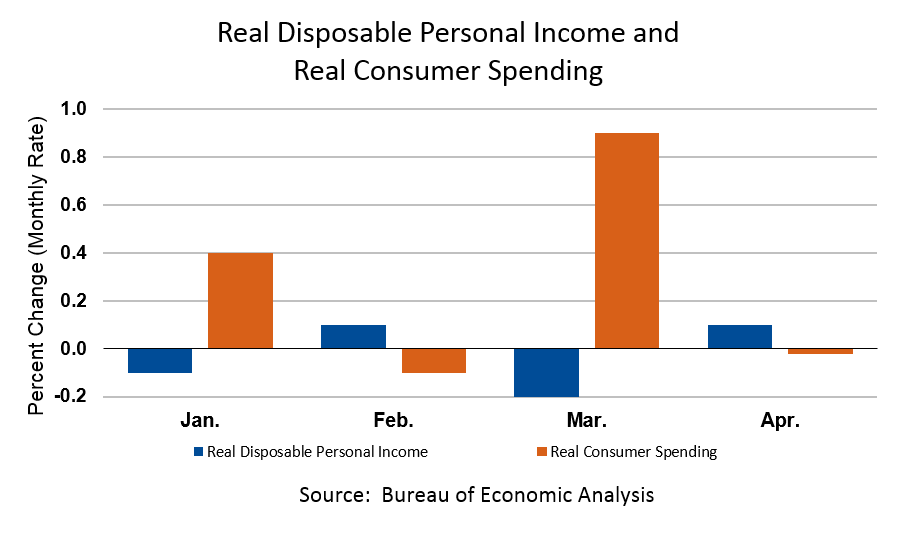

Consumer spending takes a breath after spiking in April

Chart 2: Disposable income is increasing, but consumer spending is down.

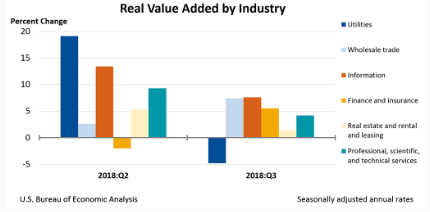

Chart 3: Companies are adding value to GDP, but at a slower pace than previously.

The economic data is okay, but clearly slowing from the strong levels of 2017-2018. Does ‘slowing’ economic activity mean a recession is around the corner? I don’t think so, and many commentators are coming around to this view. What’s really moving the market, then? In addition to economic fundamentals, the stock market seems to be overreacting to the possibility of interest rates going up…or going down. Does being afraid of both situations make any sense? Probably not.

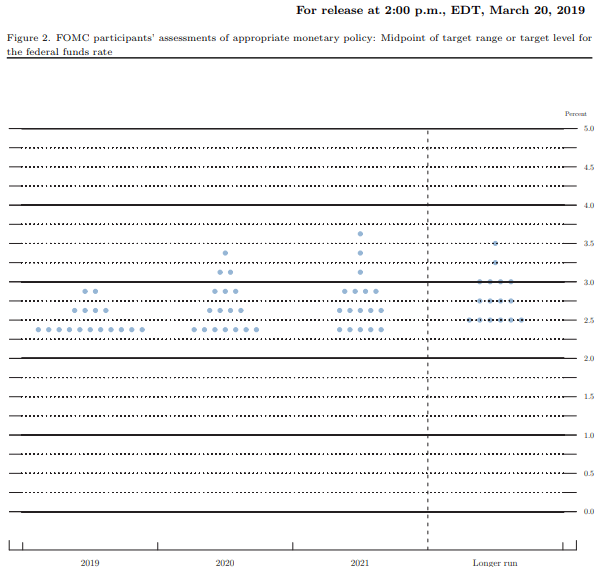

If the Fed increases rates too aggressively, they could indeed stall the economy. But we should take comfort in the persistent ‘data dependent’ stance of the Fed. They have no intention of being aggressive with interest rate hikes, so the stock market should probably find something else to worry about. In fact, institutional investors seem to agree that short-term rates are going nowhere any time soon. Federal Funds futures contracts are predicting the Fed will decrease rates by the end of 2019, though the Fed’s own ‘dot plot’ shows a possibility of one rate increase by the end of the year.

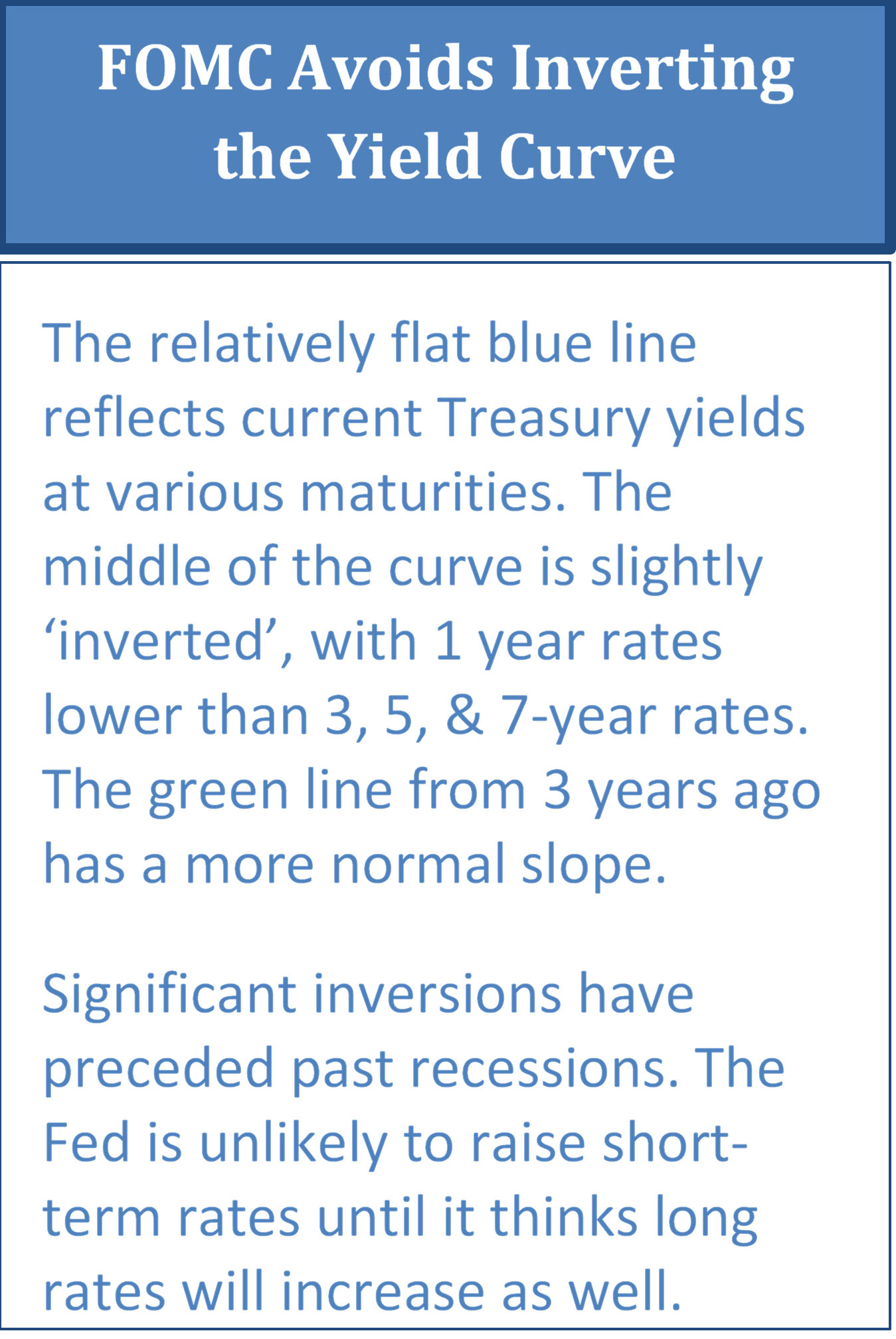

The Fed is also cautious about raising short-term rates too quickly and causing the Treasury yield curve to become ‘inverted’. An inverted yield curve is one where short-term interest rates are higher than longer term rates. This isn’t normal! Investors and lenders usually require higher rates to lock up their money for a longer period of time. An inverted curve is usually driven by…here’s that word again…Change.

The yield curve can invert under three basic scenarios:

The Fed is aggressively increasing short-term interest rates to cool down an overheated economy

Investors are demanding less return for longer maturities because they believe inflation, and consequently future interest rates, will be lower than they are currently

Differing supply and demand pressures on the short and long portions of the yield curve, sometimes driven by interest rate differentials between the U.S. and other developed countries

An inverted yield curve has preceded many recessions in the past few decades, which is why it makes people uncomfortable. But the inversion has happened as much as 2 years before the recession, so I’m not sure that the curve is actually predicting anything. It’s more helpful to analyze the economic situation driving the curve shape, rather than drawing conclusions from the curve alone. You might take comfort in knowing that post-inversion recessions have only happened when the 10-year Treasury yield was at least 0.50% below the Fed Funds rate, which we’re nowhere near. Right now my money is on Option #3 – a supply demand imbalance, not an imminent recession. Nonetheless, the current Treasury curve is slightly inverted between the 1 year and 5 year maturities and the Fed doesn’t want it to get worse and spook investors.

Source: Morningstar.com

It doesn’t make much sense for investors to be afraid of interest rates going up and also afraid of interest rates going down. But that seems to be the case at the moment and is a key driver of recent volatility in the U.S. stock market. Let’s be ‘data dependent’ for a minute and draw our own conclusions based on what we can see in the global economic landscape:

The Fed is being cautious about raising or lowering interest rates because economic data doesn’t point strongly either up or down and they don’t want to spook the financial markets

Though corporate earnings forecasts are lower than 2018, the majority of S&P 500 companies reporting slower earnings projections for the 1st quarter of 2019 have experienced positive stock price movement; S&P 500 gains year-to-date have been felt broadly across many sectors

U.S. manufacturing output slipped to its lowest level in 2 years, despite trade tensions between the U.S. and China moderating somewhat rather than getting worse

Challenges persist overseas, particularly in Europe, as trade tariffs hit European and Asian businesses harder than the U.S.; factory output in the Eurozone fell in March at the fastest pace in 6 years

Manufacturing data in China, the second largest economy in the world, was stronger than expected in March; the Chinese economy is expected to slow to a still robust 6% GDP growth in 2019 and beyond

European markets are stabilizing as the U.K. Parliament seems to be making progress identifying a viable ‘Brexit’ strategy; economic disaster in Europe due to stalled trade with Britain seems unlikely

Trade tariffs aside, improved labor conditions, lower headline inflation, and accommodative monetary policy should help support real income growth and household spending in most developed countries

Emerging economies are avoiding much of the global slowdown as many smaller countries benefit from strong capital investment, improving income growth, and economic and political reforms in recent years

What conclusions can we draw from all this data?

The economic data is certainly mixed, but most indicators point to slower growth in 2019, not a recession. From what we can see today, global economies, and consequently financial markets, should stay in modestly positive territory for the near term. We can sleep well at night knowing the ship is headed in the right direction…for now.

ASSET CLASS and SECTOR RETURNS as of MARCH 2019

Source: Morningstar Direct

Source: S&P Dow Jones Indices

Marcia Clark, CFA, MBA Senior Research Analyst Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.

DISCLOSURES

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications.

https://warrenstreetwealth.com/wp-content/uploads/2015/02/Final.jpg5651821Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2018-01-03 11:00:012024-06-03 10:52:15The Many Benefits of a Roth IRA

A “not-to-do” list for the new year & years to follow.

Provided by: Warren Street Wealth Advisors

How are your money habits? Are you getting ahead financially, or does it feel like you are running in place?

It may come down to behavior. Some financial behaviors promote wealth creation, while others lead to frustration. Certainly other factors come into play when determining a household’s financial situation, but behavior and attitudes toward money rank pretty high on the list.

How many households are focusing on the fundamentals? Late in 2014, the Denver-based National Endowment for Financial Education (NEFE) surveyed 2,000 adults from the 10 largest U.S. metro areas and found that 64% wanted to make at least one financial resolution for 2015. The top three financial goals for the new year: building retirement savings, setting a budget, and creating a plan to pay off debt.1

All well and good, but the respondents didn’t feel so good about their financial situations. About one-third of them said the quality of their financial life was “worse than they expected it to be.” In fact, 48% told NEFE they were living paycheck-to-paycheck and 63% reported facing a sudden and major expense last year.1

Fate and lackluster wage growth aside, good money habits might help to reduce those percentages in 2015. There are certain habits that tend to improve household finances, and other habits that tend to harm them. As a cautionary note for 2015, here is a “not-to-do” list – a list of key money blunders that could make you much poorer if repeated over time.

Money Blunder #1: Spend every dollar that comes through your hands. Maybe we should ban the phrase “disposable income.” Too many households are disposing of money that they could save or invest. Or, they are spending money that they don’t actually have (through credit cards).

You have to have creature comforts, and you can’t live on pocket change. Even so, you can vow to put aside a certain number of dollars per month to spend on something really important: YOU. That 24-hour sale where everything is 50% off? It probably isn’t a “once in a lifetime” event; for all you know, it may happen again next weekend. It is nothing special compared to your future.

Money Blunder #2: Pay others before you pay yourself. Our economy is consumer-driven and service-oriented. Every day brings us chances to take on additional consumer debt. That works against wealth. How many bills do you pay a month, and how much money is left when you are done? Less debt equals more money to pay yourself with – money that you can save or invest on behalf of your future and your dreams and priorities.

Money Blunder #3: Don’t save anything. Paying yourself first also means building an emergency fund and a strong cash position. With the middle class making very little economic progress in this generation (at least based on wages versus inflation), this may seem hard to accomplish. It may very well be, but it will be even harder to face an unexpected financial burden with minimal cash on hand.

The U.S. personal savings rate has averaged about 5% recently. Not great, but better than the low of 2.6% measured in 2007. Saving 5% of your disposable income may seem like a challenge, but the challenge is relative: the personal savings rate in China is 50%.2

Money Blunder #4: Invest impulsively. Buying what’s hot, chasing the return, investing in what you don’t fully understand – these are all variations of the same bad habit, which is investing emotionally and trying to time the market. The impulse is to “make money,” with too little attention paid to diversification, risk tolerance and other critical factors along the way. Money may be made, but it may not be retained.

Make 2015 the year of good money habits. You may be doing all the right things right now and if so, you may be making financial strides. If you find yourself doing things that are halting your financial progress, remember the old saying: change is good. A change in financial behavior may be rewarding.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svg00Cary Facerhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgCary Facer2015-01-27 17:39:422015-01-27 17:39:424 Money Blunders That Could Leave You Poorer