IPO Mania: What the Rocket Ships, Chatbots, and Rule Changes Mean for Your Portfolio

The headlines are hard to miss. SpaceX. Anthropic. OpenAI. Three of the most talked-about private companies in history are preparing to go public — and together, they could raise more money in a matter of months than the entire U.S. IPO market raised all of last year. Today on the blog, we explore what to expect from the hottest Wall Street darlings and what these shiny objects mean for markets.

Let’s Set the Table

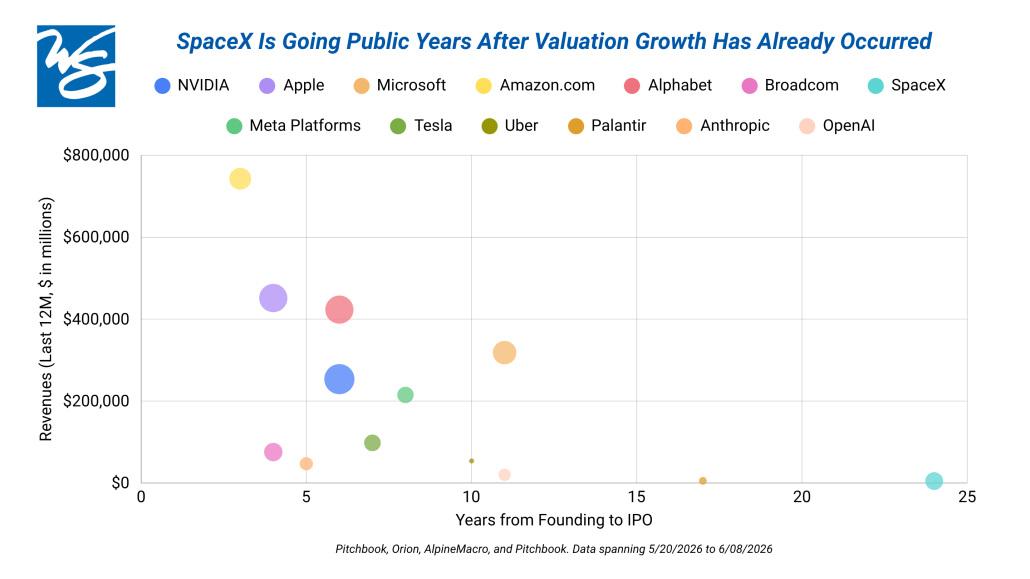

In 2025, the entire U.S. IPO market raised $77 billion. SpaceX alone is targeting a $75 billion raise — add Anthropic ($60–65 billion) and OpenAI ($60 billion), and you’re looking at a combined raise close to $200 billion.

These are no longer the scrappy startups where early public investors get in on the ground floor. Much of the value has already been captured by venture capitalists and private investors. Before going public, SpaceX was reportedly valued at ~$1.25 trillion, Anthropic at ~$900 billion, and OpenAI at ~$825 billion — nearly $3 trillion in private market value accumulated behind the scenes. SpaceX here is the outlier, going public 24 years after inception as indicated by the turquoise bubble in the chart above.

Don’t Forget to Ask — Why Now?

I usually view IPOs with a skeptical eye – not because success stories can’t be made, but because an information asymmetry will permanently exist. Insiders can tell when the public is overpaying for their company and use it as an opportunity to cash out. So why go public now?

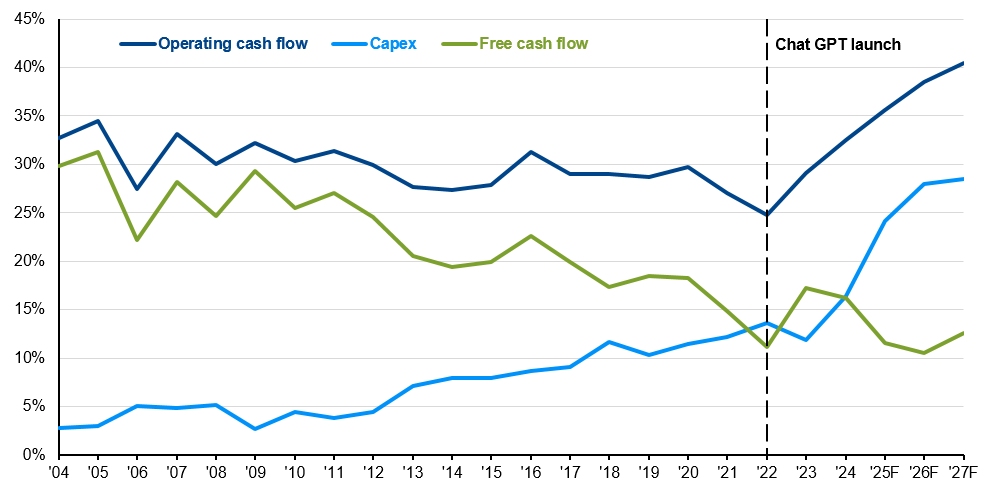

- These companies need cash. Building cutting-edge AI and sending rockets to space is extraordinarily expensive. Going public gives them a massive influx of capital to fund that growth.

- Early investors need an exit. Founders, employees, and early-stage investors have been waiting years to convert paper gains into real dollars. It’s also worth noting: history has eerie examples of companies timing public offerings around industry peaks — Blackstone before the 2008 real estate crisis, Glencore before the 2011 commodity cycle pop. Worth pausing a moment for.

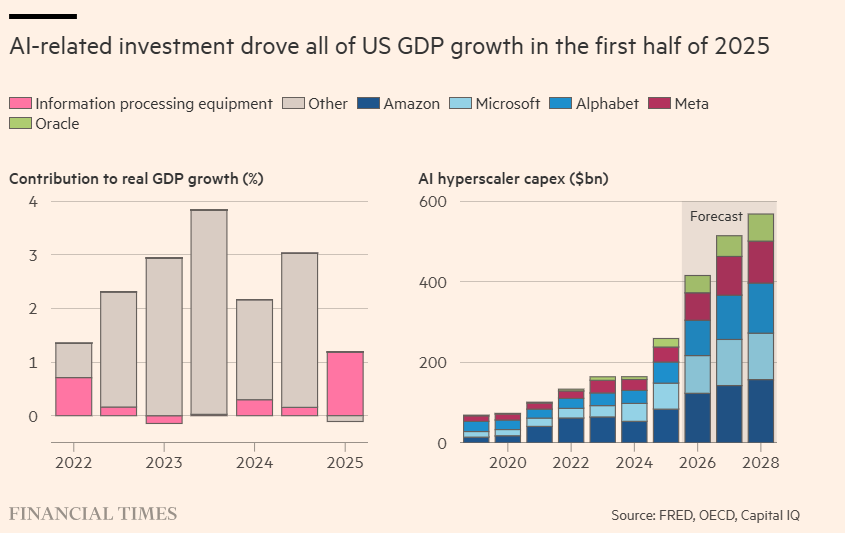

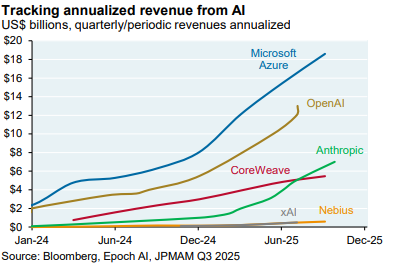

- The market is excited. The AI investment environment has been exceptionally strong, recovering from the skepticism that characterized earlier this year.

What Comes After the Honeymoon?

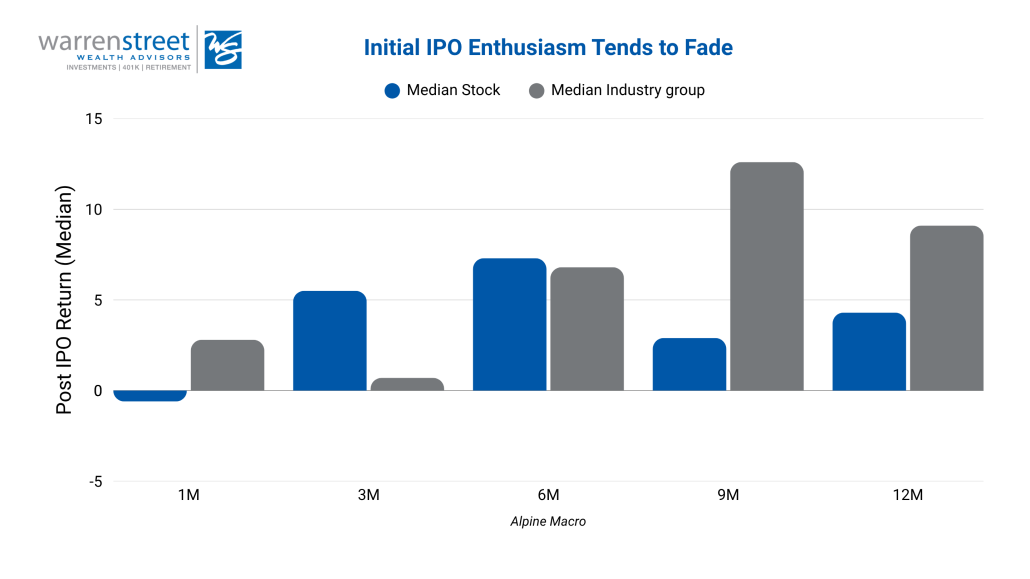

IPOs are often explosive in the short-term — a honeymoon period followed by selling pressures where the relationship starts to go south. Here’s what to expect:

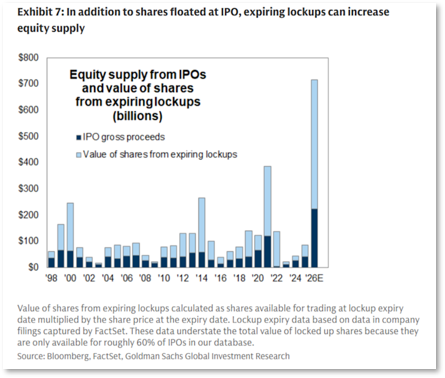

Short-term: Prices get a boost from engineered scarcity (companies deliberately underprice and limit tradable shares), retail enthusiasm and FOMO, and index fund buying — which could account for approximately 17–24% of tradable shares within the first 15 trading days, based on estimates from AlpineMacro.

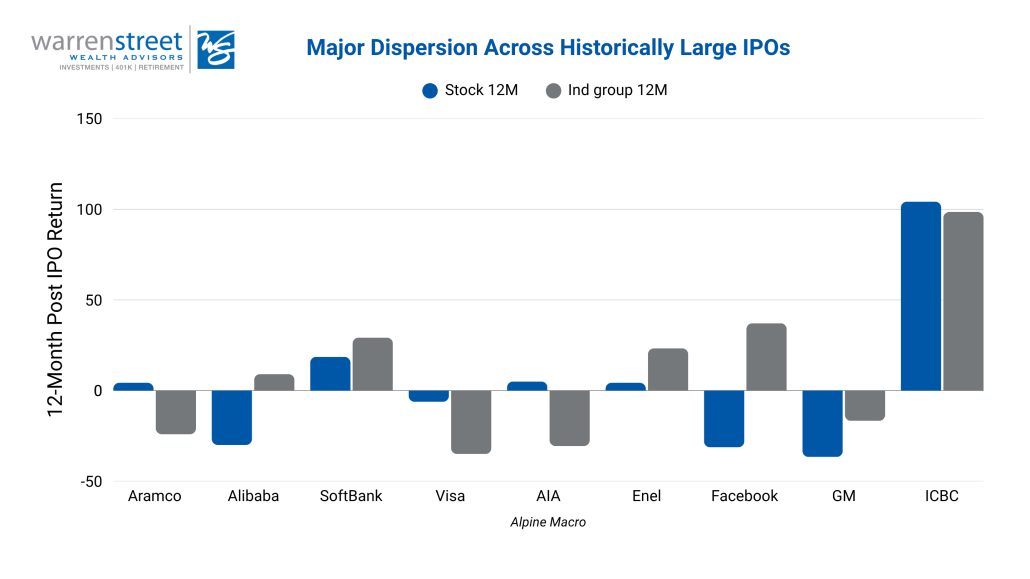

Medium-term: Here comes the reality-check. Lock-up expirations release insider shares onto the market, applying downward pressure on prices. This year, those lock-ups are unusually concentrated in adjacent AI and tech companies, introducing more fragility than prior cycles. It’s also worth noting that most IPO’s have underperformed their broader industry in the 12 months following launch, with gains often concentrating in only a small number of big winners while the rest disappoint. Past performance and historical trends are not indicative of future results.

Longer-term — the Index Dilemma: Major index providers like S&P and Nasdaq are reportedly bending their own rules to fast-track these mega-IPOs into their benchmarks. Most consequentially, S&P is considering relaxing its profitability requirement. As these stocks join indexes and lock-ups expire, automated buying algorithms will be forced to fund those purchases by selling something else — most likely the largest, most liquid names: Apple, Microsoft, Nvidia.

Investment Implications

If these IPOs execute well, it’s a green light for the AI trade and would lift companies across the ecosystem. If they stumble, it’s a meaningful warning signal for anyone spending heavily without yet turning a profit.

We believe the index risk is the more underrated story. When index rules are bent to accommodate unprofitable companies, the passive investor is quietly exposed to degraded quality screens, less certain cash flow trajectories, and deeper AI concentration. It blurs the line between passive and active investing — and you have to ask yourself: what am I really owning?

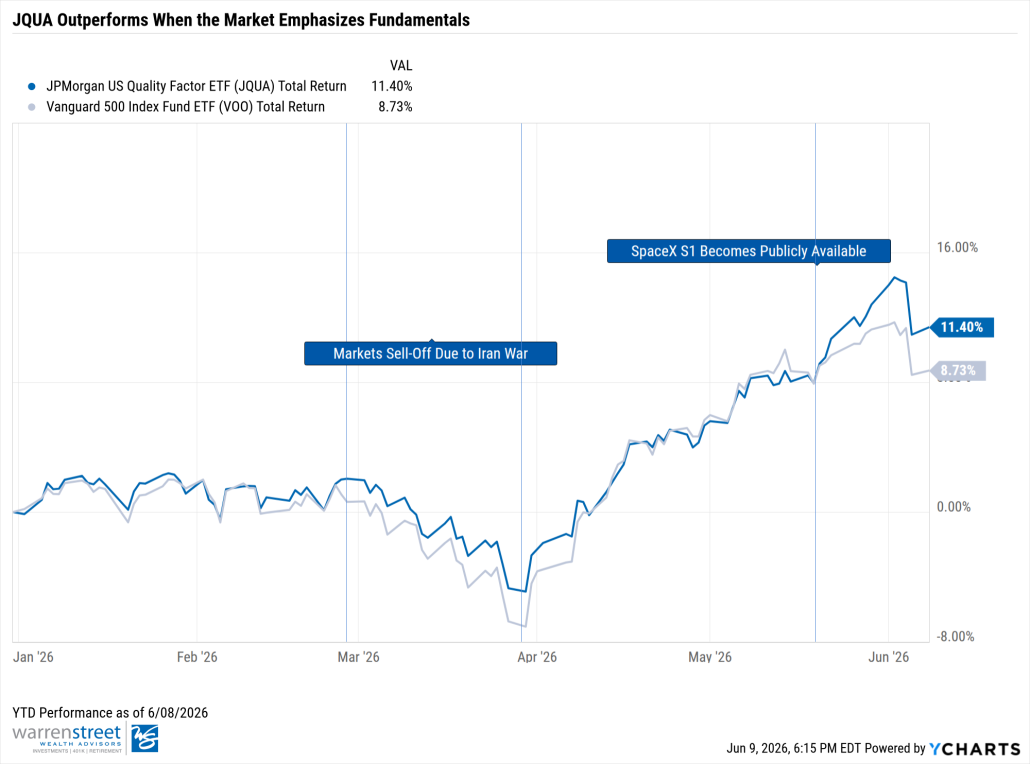

In this environment, we continue to rely on our pairing of market-Cap weighted S&P 500 exposure alongside quality-focused ETFs (for example, JQUA, the JPMorgan U.S. Quality Factor ETF), depending on client objectives and risk tolerance. JQUA generally focuses on companies with strong earnings, healthy balance sheets, high returns on equity, and manageable debt – qualities (no pun intended) meant to ground investments in fundamentals when narratives run ahead of numbers. We believe this approach may allow portfolios to participate broadly in market enthusiasm, depending on client objectives and risk tolerance.

Our Take

We recognize the excitement surrounding this IPO wave, but our role is to navigate these waves with discipline. While these are compelling names and future portfolio candidates across our fund managers, we believe the more prudent approach is to allow valuations to normalize, narratives to mature, and market expectations to recalibrate before committing capital. In other words, we are letting quality discipline and our understanding of IPO markets – not enthusiasm – guide your portfolio’s trajectory.

Phillip Law, CFA

Senior Portfolio Manager

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors and/or its clients may hold positions in the securities mentioned. Holdings may change at any time without notice. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.