Oil, Conflict, and Your Portfolio: What We’re Watching

Before we dive into the facts, we want to take a moment to recognize that before we are advisors or investment analysts, we are human. Our hearts go out to the families and individuals affected. We hold that reality close as we do our job of helping you navigate what it means for your financial future.

Part of that job is cutting through the noise, so let’s talk about what’s happening, what it means, and what we’re doing about it.

What’s Happening

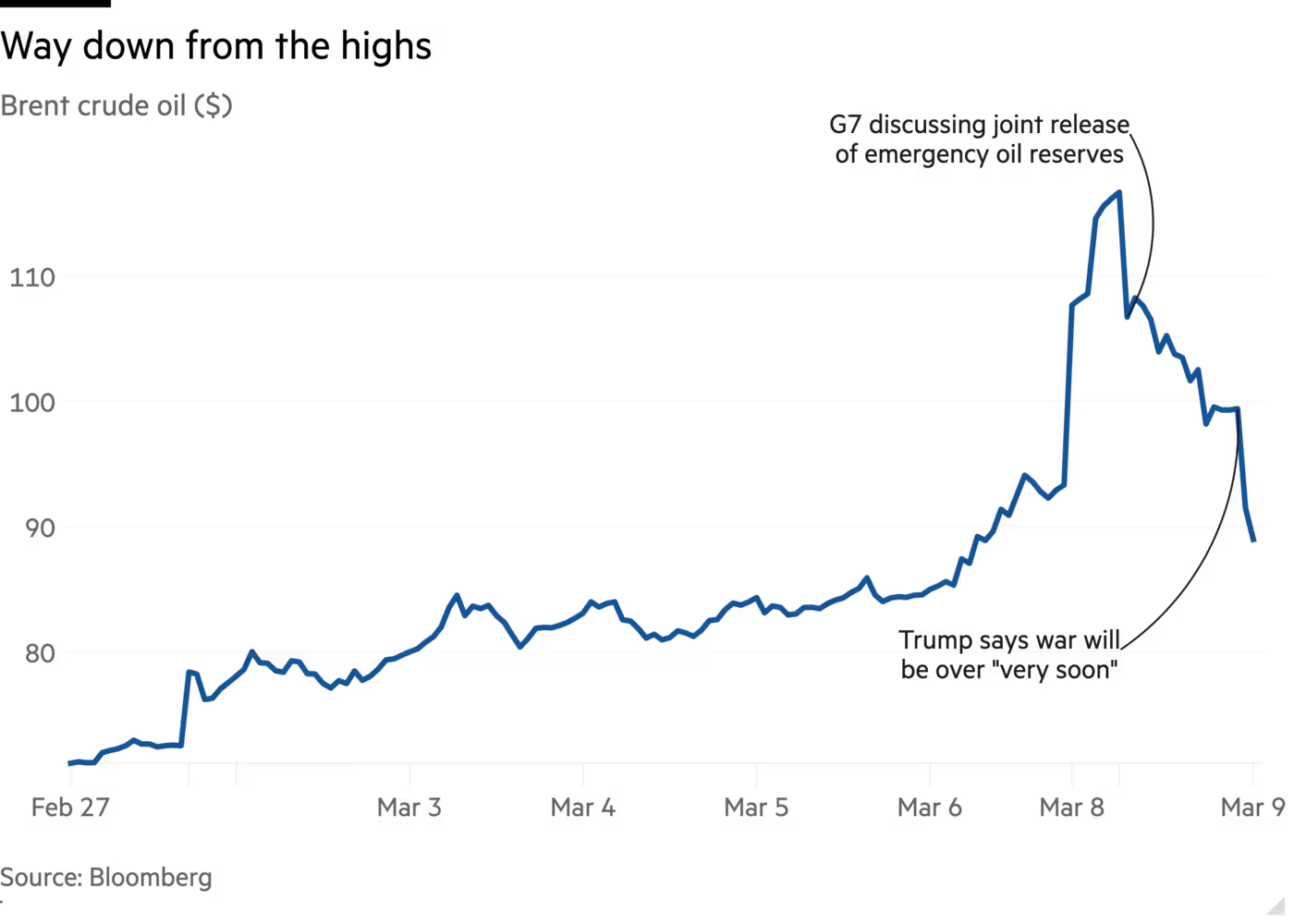

The conflict entered its second week with crude oil briefly crossing $110 per barrel. Energy infrastructure in the region sustained damage, and the world turned its attention to the Strait of Hormuz — the narrow waterway through which roughly 20% of global oil supply flows — and whether it would remain open for business.

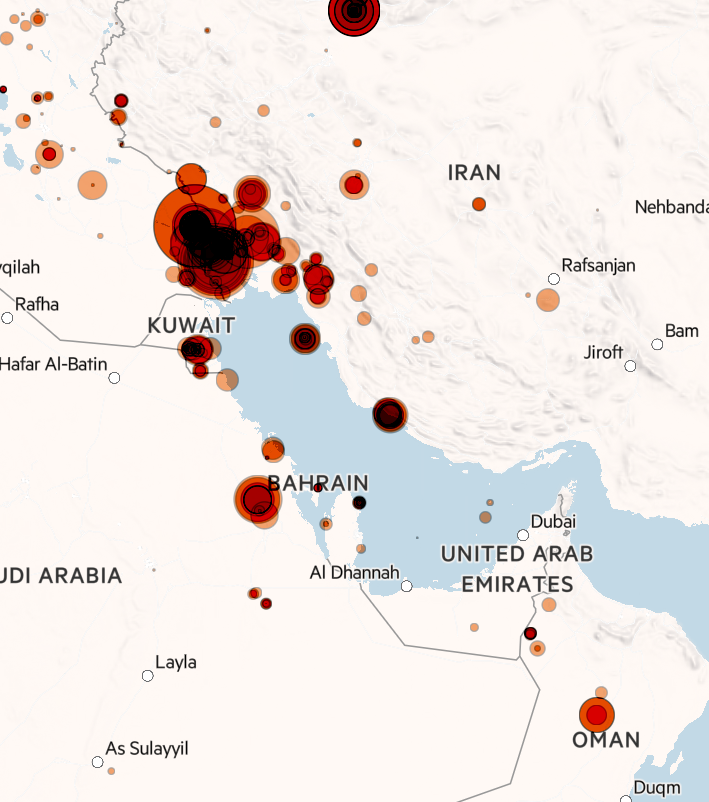

Fire anomalies detected by infrared sensors on 7-8 March. Circles are sized by fire radiative power, darker circles mean several fires in close proximity

Sources: FT Analysis, Nasa Firms. Fires reported are either in locations with no history of regular burns or are unusually bright.

We don’t have a crystal ball for what will happen next, but there are three questions we’re watching closely:

- Will there be more lasting damage to energy infrastructure?

- What does the endgame look like in terms of leadership and capabilities on both sides?

- Can a compromise be reached that keeps oil flowing through the gulf?

And Then Oil Dropped $20

Here’s the thing about geopolitical risk: it tends to be loud and unpredictable.

As I’m writing this, oil has pulled back from $110+ per barrel to below $90 — after President Donald Trump suggested the potential for a swift conclusion to the conflict. Meanwhile, the Strait of Hormuz is seeing vessel traffic increase, recovering from post-attack lows with inbound and outbound ship movements gradually rising.

While it’s too soon to declare a resolution, the swift oil price drop following comments from President Trump shows the market was pricing in a major supply shock that hasn’t materialized. This underscores why we avoid trading headlines, which often lead to emotional decisions mistaken for analysis. Our consistent advice for geopolitical headlines remains: stay diversified, stay disciplined, and trust your portfolio strategy.

History Has Seen This Before

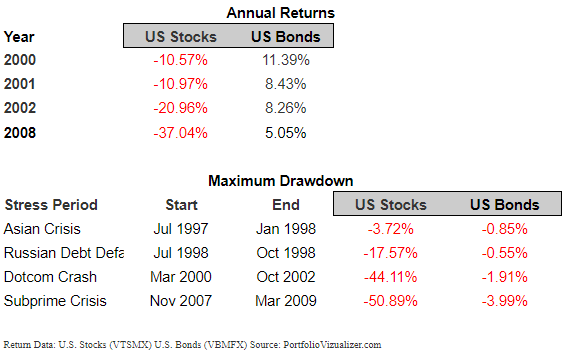

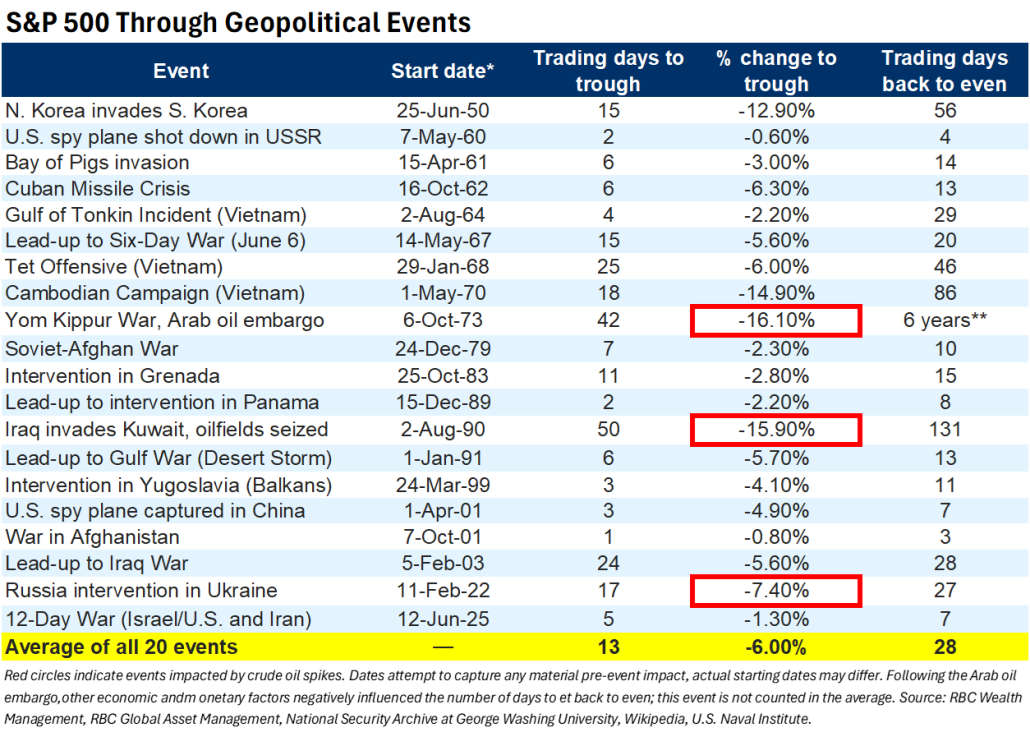

Here’s something worth sitting with. Looking at the past 20 major military conflicts and their impact on the S&P 500 over the last 75 years, the average decline from the initial shock to the market bottom was around 6%, and in 19 out of 20 cases, markets returned to pre-event levels in an average of just 28 days.

The two biggest exceptions — the 1973 Yom Kippur War and Iraq’s 1990 invasion of Kuwait — both involved sustained oil supply disruptions that pushed stocks down 15–16%. The 1973 episode scarred a generation of investors who sold out of equities and missed the enormous bull run of the 1980s.

The lesson isn’t that conflicts don’t matter. It’s that panicking out of a well-structured portfolio tends to hurt more than the conflict itself does.

This Isn’t 1973

Clients who lived through the Yom Kippur War might flinch from the prospect of re-living around-the-block gas lines, federally imposed speed reductions, or darkened cities to conserve energy. We understand the instinct, but there are major differences today.

In 1973, the U.S. was heavily dependent on imported oil. Every extra dollar at the pump was more money in the pockets of Middle Eastern countries. Today, the U.S. is a net energy exporter. Higher oil prices are painful for consumers, yes — but every extra dollar is more cash in the pockets of domestic energy producers. It’s a redistribution within the economy, not a pure drain out of it.

As for inflation, Energy makes up only about 6% of today’s U.S. inflation basket. There also headwinds blowing against the case for a 1970’s stagflation landscape, including:

- Shelter Lags: Shelter costs (33% of the basket) are declining as lagging rent data catches up to reality, which will apply downward pressure on inflation prints.

- Technological Progress: AI and technology-driven productivity is quietly acting as a deflationary force as consumers and businesses increase adoption.

- Calming Tariff Tantrums: After the recent IEEPA tariff ruling, the effective tariff rate has also come down meaningfully to 9.1%.

- Fundamental economic strength: We acknowledge the recent jobs report’s weakness, but also recognize other areas in the economy remain healthy. Corporate profits are expected to grow at high single to double digits in 2026. Tax refunds from last year’s One Big Beautiful Bill (OBBB) haven’t fully hit consumer accounts yet.

The Fed will likely pause at upcoming meetings, but that’s very different from the kind of policy circumstances that defined the stagflation era.

Weeks, Not Months?

Both sides have strong incentives to reach a compromise quickly. Iran can’t export oil under prolonged conditions and is subject to existential economic pressure. In the U.S., $4+ gas heading into a midterm summer is its own political tax. December oil futures were already trading in the low $70s before today’s pullback, suggesting the market never fully bought the doomsday scenario. Inflation breakeven rates have stayed surprisingly calm throughout.

Even after hostilities quiet down, there’s likely a period of elevated shipping costs and more cautious tanker behavior through the region. Think of it as a persistent risk premium rather than a single clean resolution — but a manageable one, not an economy-altering one.

What We’re Doing

We’re not making dramatic moves based on headlines and that’s by design. We are however, sticking to our operating procedure of:

- Rebalancing – different parts of our clients’ portfolios have generally weathered the volatility well, but some may have drifted off target. Rebalancing is a disciplined move back toward those levels, not a market call, but a long-term wealth strategy of selling strength and buying weakness.

- We built the “Diversifiers” strategy in client’s retirement portfolios for moments like this. It’s doing its job and reminding us that traditional stock-bond portfolios don’t always move in opposite directions when inflation is in the picture.

- If markets sell off further in an extreme scenario, we have the flexibility to tilt asset classes within our portfolios.

We’ll continue monitoring the conflict while staying with our standard operating procedure, but what we won’t do is trade headlines. The oil price chart of the last two weeks makes that case better than we ever could.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Sources:

- https://www.ft.com/content/56dd339c-51ea-41b0-983a-fe13c0d5ab54#post-2777139a-5545-4ece-8753-34d1868ddd08

- https://www.reuters.com/graphics/IRAN-CRISIS/MAPS/znpnmelervl/#tanker-traffic-in-the-strait-of-hormuz-comes-to-a-standstill

- https://privatebank.jpmorgan.com/nam/en/insights/audio-and-webcasts/webcasts/the-evolving-conflict-with-iran-and-investment-implications