Over the next few decades, an enormous amount of wealth is expected to pass from older to younger generations. This has been dubbed the “Great Wealth Transfer,” and one estimate suggests that $124 trillion will change hands by 2048. It’s an eye-popping figure, to be sure, but it also highlights the reality that many families are, or soon will be, navigating how to pass on their wealth. A top-of-mind question: Is the next generation ready to take on the responsibility?

Wealth is not just cash in the bank; it can include investments, real estate, businesses and more that require stewardship and foresight. Successful management means preserving and growing assets and using them wisely. Striking the right balance here is key: For the next generation to succeed, it takes intentional preparation and education.

Plant the Seeds of Financial Literacy

Where to begin? In an ideal world, financial education starts in early childhood and is treated as an open and ongoing conversation as kids age. The goal is to build financial literacy gradually, so wealth management feels natural rather than overwhelming.

When kids are young, this might mean introducing simple topics like the difference between saving and spending. Managing an allowance can help put those ideas into practice. As kids get older you can begin introducing more complex topics, such as investing, compound interest, debt and taxes.

It’s equally important to engage adult children, many of whom may have received no other formal financial education. While 29 states now have K–12 financial education requirements in public schools, this focus has largely come to the forefront only in the last few years. If your kids are adults now, they may have missed out. So it’s worth finding out what they know, what they don’t know and what they’d like to know more about.

Put Structure Around Learning

In addition to ongoing conversations about money, your family might benefit from more intentional ways of building financial literacy. Some families hold regular financial meetings where they share goals, key issues and address questions or concerns. Others put together more formal workshops with wealth advisors or other experts.

There also is a wealth of credible educational content online that is built to both educate and engage audiences around financial literacy topics.

Turn Conversations into Action

Eventually, theory should give way to practice. As younger family members learn the basics, you might consider providing a “practice portfolio,” giving them the chance to make investment decisions with small amounts of money and learn from their successes and mistakes.

When family members have honed their knowledge, consider assigning them real responsibilities that match their skills and interest. This might mean relatively simple tasks like helping guide gifts made through a donor-advised fund. Or these responsibilities could be more involved, such as taking a role in the family business or helping to make investment decisions with the family’s wealth. With your guidance and oversight, these experiences can help develop confidence and capability.

Ground Wealth in Purpose and Values

One of the most important things that helps guide families on how to grow and spend wealth is imparting a strong value system. Values can help you frame wealth as a tool rather than a goal.

Your values will be unique to you, but some worth considering may be:

Stewardship: Recognizing the responsibility that comes with wealth. Stewardship encourages careful management and intentional choices so resources can benefit both current and future generations.

Giving back: Using wealth to help create positive change in your community and the greater world.

Self-worth beyond wealth: Remembering that wealth is a tool to achieve goals—whether gaining an education, pursuing passion or giving back, for instance—not a measure of personal value.

By grounding financial decisions in values, families can help prevent counterproductive or reckless financial decisions, foster responsibility and ensure wealth is not seen as something to be simply consumed.

Keep the Conversation Going

Discussing money isn’t always easy, and for many families, it’s downright taboo. While 66% of Americans say conversations about wealth are important, 62% say they never have them.

But getting over this hurdle is incredibly valuable. The most successful families treat wealth education not as a one-time event, but as an ongoing process that evolves as your family grows and your financial picture changes. We can work with you to create an environment where family members can openly discuss the unique challenges and opportunities that come with wealth.

Veronica Cabral, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/03/image-1.png9001600Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2026-03-02 09:49:032026-03-02 09:49:08How Do You Prepare the Next Generation to Manage Family Wealth?

A few years ago, ads from financial services companies asked, “What’s your number?” The “number” represented the amount of money you needed to retire comfortably. There are, of course, various approaches to estimating your retirement “number,” all of which are influenced by your goals and factors, such as your expected retirement age and the lifestyle you hope to maintain in retirement. So, while this question may have been an effective way to spark conversations about retirement, we believe that it doesn’t paint the complete picture.

Retirement isn’t just about reaching a specific monetary goal. It also involves creating a comprehensive strategy that looks to optimize your various savings vehicles, each playing a different role in your retirement income approach. It also means factoring in healthcare costs, thinking about the legacy you wish to leave, and being flexible enough to adapt to life’s unexpected twists and turns. Ultimately, your strategy needs to consider how your assets will work together to fund the retirement you envision.

An essential part of orchestrating your retirement income strategy is determining which assets to take and in which order.

There is no one-size-fits-all answer, but some general guidelines can help when you are starting to think about a withdrawal strategy.

For example, one approach to consider is withdrawing money from taxable accounts first, then tax-deferred, then tax-exempt. By using taxable money first, you can avoid paying taxes as long as possible with tax-deferred investments. And your tax-exempt accounts remain tax-exempt for a longer period. Ultimately, your decision will be influenced by a wide range of other considerations, including withdrawal fees, surrender charges, and other costs that may be associated with each specific account. But when possible, consider using the power of tax deferral and tax exemption to your advantage.

Regardless of your age or financial position, having a well-thought-out retirement strategy is one of the most critical actions you can take. If you would like to review your current strategy, please contact our office. We’re here for you!

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/02/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2026-02-06 10:58:592026-02-06 10:59:05How Much Do I Need to Retire in 2026?

If you’re a business owner, you’ll eventually step away from the company you’ve built. You might cash out to the highest bidder or work out a deal to sell the business to the next generation of your family or even to employees. The question is will you be able to make this transition on your own terms? The reality is that most business owners don’t have a clear, documented exit plan. And if you find yourself among them, you could find it leaves you in a tight spot when it’s time for you to step down.

Delaying planning your exit risks settling for a below-market sale price, losing control of choosing your successor or rushing into choices that don’t reflect your vision. Delays also leave you with little time to take steps to boost the business’s valuation and ensure business continuity. A clear exit plan helps maximize options and value. If you haven’t mapped out yours yet, there’s no time like the present. Consider these steps:

Put a Price on Your Business

Proper valuation of your business is the first step in exit planning. Some back-of-the-envelope math can provide a decent starting point. But to really understand what your business is worth, meet with a valuation expert. Besides a healthy dose of objectivity, these professionals bring market expertise and a knowledge of valuation standards. They can identify intangible sources of value you may have overlooked and help ensure your valuation passes muster with potential buyers and the IRS.

There are three main approaches to determining value:

The asset approach adds up the value of your company’s tangible and intangible assets, then subtracts liabilities.

The income approach calculates value according to your business’s expected future cash flows.

The market approach compares your business to recent sales of similar companies.

You may find one approach is more apt than another for the type of business you own, but a comprehensive valuation is likely to incorporate all three in one way or another. Bear in mind that valuation isn’t a one-time event. As your business grows and market conditions change, you’ll likely want to update your valuation.

Clarify Your Vision

Before you can build an effective exit plan, it’s necessary to clarify your goals. Be as specific as possible as you define what a successful transition looks like to you.

Some questions to keep in mind: Do you want to maximize the sale price, selling at the highest price possible? Do you intend to keep the business within your family or pass it to a handpicked successor? What are your obligations to employees? Is it important that your business maintains a consistent set of values when you’re gone? What timeline makes sense for you? How involved—if at all—do you want to be with the business after you exit?

The answers to these questions will guide the decisions that follow. They can be deeply personal, and we’re here to be a resource as you consider what’s truly important to you.

Shape Your Exit

With valuation and goals in hand, there are a range of steps you can take to support your transition. What you do will depend largely on the type of exit you’re planning. For some owners, you might make strategic adjustments to boost the value of your business, such as reducing unnecessary expenses or diversifying revenue streams to make your company more attractive to buyers.

If your plan involves transferring the business to a family member or a long-time employee, the sooner you identify them, the better. That way you’ll have plenty of lead time to train them in the leadership skills necessary to provide a smooth handoff. Depending on your situation, you might consider a sale, a gift or a combination of the two. Be aware that gifts to family members above the lifetime gift and estate tax exemption ($15 million for individuals in 2026) might trigger gift taxes. Meanwhile, sales to employees could trigger capital gains taxes. If your business is structured as an S corp or C corp, you might consider an employee stock ownership plan (ESOP), which could defer or even eliminate capital gain taxes if structured properly.

Seeking an external buyer? Preparation is equally as important. In addition to boosting your valuation, you’ll need to organize your financial records, legal documents, contracts, employee agreements and operational procedures. One thing to consider is the type of deal structure that works best for you: Would you like to be paid over time or in one lump sum? And would you like to exit the company immediately or would you be open to staying on in an advisory capacity to help the new owner learn the ropes?

Begin the process of finding and vetting buyers early. These could be industry competitors, investment groups or individual entrepreneurs who may be a good fit. A business broker can help you identify potential buyers and spread the word through their network.

Charting the Future

For many business owners, exit planning rarely tops the to-do list. After all, there are plenty of day-to-day demands competing for attention, let alone the fact that it can be difficult for owners to think about the day they’ll no longer lead the company they built. Yet the most successful exits are those planned in advance, allowing owners to optimize value, identify an ideal buyer or successor, and prepare their employees for a smooth transition.

If you’d like to start a conversation about exit planning, we’d be happy to help you explore your options, develop a strategy that meets your financial goals and protects your legacy. here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/11/image.png9001600Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-11-07 08:52:472025-11-07 08:52:58Business Exit Strategies on Your Terms

Inheritances come in all shapes and sizes, whether an heirloom left to you by a loved one or a life-changing financial windfall. Regardless of the form it takes, figuring out what to do next can be a crucial question. This is especially true with inherited IRAs, which can be very well funded, but also come with very specific and complicated rules you must follow to unlock the assets within them.

This guide will walk you through the basics of what to do. From there, we can review your personal situation together to help ensure you don’t overlook anything important.

What Kind of Beneficiary Are You?

When you inherit an IRA, the very first step is to figure out what type of beneficiary you are. Here’s why: There are three main types, and the rules around key issues like withdrawal requirements will differ depending on which type you are.

You will fall into one of the following categories:

Designated beneficiary. You are the person named as the beneficiary on the retirement account itself.

Eligible designated beneficiary. You are a designated beneficiary who is also any one of the following:

Spouse or minor child of the account owner.

Someone not more than 10 years younger than the account owner. (Someone whose age is equal to or greater than the age of the account owner minus 10.)

Someone who meets the IRS’s definition of chronically ill or disabled.

Nondesignated beneficiary. You are not named as the beneficiary on the retirement account itself, but you may inherit the IRA through a will or estate.

Another important step you might have to take early: If the owner of the account you inherit was taking required minimum distributions (RMDs)—the mandatory withdrawals from tax-deferred retirement account that start when the account owner reaches age 73—you’ll need to make that withdrawal before the end of the current calendar year. If you don’t, you’ll risk triggering a 25% penalty on the amount of that distribution.

Options for Your Inherited IRA

When you inherit an IRA, you have several choices for how to handle that account.

Disclaim it: If for any reason you don’t want to accept the IRA—such as avoiding tax consequences from additional income—you can refuse it by disclaiming it. If you decide to take this route, you must disclaim within nine months of the account owner’s death. The IRA will then be passed to an alternate beneficiary or to the estate.

Take a lump-sum: You can opt to withdraw all the funds of the IRA at once. If it’s a traditional IRA, the IRS will tax the withdrawal as income, which may bump you into a higher tax bracket. If it’s a Roth IRA, the withdrawal is tax-free, but the account must be at least five years old to avoid incurring a 10% penalty.

Withdraw assets over time: If you don’t want to take a lump sum, you can keep the assets in an inherited IRA, where they can continue to grow tax deferred. This is where things get a bit more complicated depending on what type of beneficiary you are.

If you’re a designated beneficiary (but not an eligible designated beneficiary), you must empty the inherited IRA within 10 years to avoid penalties on undistributed amounts. The clock starts ticking a year after the original owner’s death. So if the original owner died in 2024, you’d have until December 31, 2034 to empty the account. Also, if the original account owner had already started taking RMDs, you’ll have to continue taking them based on your own life expectancy each year to avoid penalties. (Don’t worry about calculating your own life expectancy. The IRS does that for you through its life expectancy tables, and we can work with you to make sure you get it right.)

If you’re an eligible designated beneficiary, you generally aren’t subject to the 10-year rule. You’ll have to take RMDs, but you can calculate the amount based on your own life expectancy and hold onto the inherited IRA indefinitely. An exception to this is minor children. For them, the 10-year rule will kick in at age 21.

If you’re a nondesignated beneficiary inheriting the IRA through a will or an estate, your requirements are determined by the account owner’s age. If the account owner hadn’t reached the age where distributions were required, you must empty the account within five years. If the account owner had begun taking RMDs, you will continue to take RMDs based on the same timeline.

Transferring funds to your own IRA: If you are a surviving spouse, you have the option to roll the assets from an inherited IRA into an IRA in your own name. If the original account owner hadn’t taken an RMD for the current year, you’ll have to take that RMD on their behalf before moving the funds.

Let Us Simplify the Process for You

Inheriting an IRA, like receiving any inheritance, can feel both meaningful and overwhelming. It’s a reminder that someone cared for you, but it comes with important financial decisions.

Making the right choices around an inherited IRA can help you avoid big tax bills and penalties. But of all the things there are to know about inherited IRAs, the most important is that you don’t have to figure those choices out alone. We’re here to help you understand your options and move forward with a tax-efficient strategy that supports your financial goals.

Veronica Cabral

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/10/image-1.png9001600Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2025-10-27 08:16:142025-10-27 08:16:18What Should I Do With an Inherited IRA?

Open enrollment is your annual opportunity to review and select your employee benefits for the upcoming year. While it might seem like just another task on your to-do list, the choices you make now can have a significant impact on your health and finances. Don’t simply “roll over” last year’s elections without a review. A proactive approach will ensure your benefits align with your needs and goals.

Analyzing Your Health Insurance Options

Start by assessing your current situation. Think about your health needs from the past year: how many doctor’s visits did you have? What were your prescription costs? Do you anticipate any major life changes, such as getting married or having a baby? These factors will help you choose the right plan.

Understanding Key Terms

Before diving into plan specifics, it’s crucial to understand a few key terms:

Premium: The fixed monthly cost you pay for your insurance plan.

Deductible: The amount you pay out of pocket before your insurance coverage begins.

Copay: A fixed amount you pay for a doctor’s visit or prescription after your deductible is met.

Coinsurance: A percentage of costs you pay for covered services after the deductible is met.

Out-of-Pocket Maximum: The maximum amount you will pay in a year before the plan covers 100% of costs.

Comparing Plan Types: PPO vs. HDHP

The two most common types of health plans are a Preferred Provider Organization (PPO) and a High-Deductible Health Plan (HDHP).

A PPO typically has a lower deductible but higher premiums. It also offers more flexibility for seeing out-of-network doctors. This type of plan is generally best for people who use a lot of medical services, as the costs are more predictable.

An HDHP has a higher deductible but lower premiums. While you’ll pay more upfront for care, this type of plan makes you eligible for a Health Savings Account (HSA). An HDHP is often a great choice for generally healthy individuals or those who can comfortably afford the higher upfront costs if a major health event were to occur.

To help with your decision, compare the total estimated annual cost of each plan. For example, calculate the premiums plus potential out-of-pocket costs for a year with no major health events versus a year with a major surgery. This simple exercise can reveal which plan offers the most financial sense for your situation.

Maximizing Your Tax-Advantaged Accounts

In addition to health insurance, open enrollment is your chance to enroll in or update contributions to valuable tax-advantaged accounts.

Flexible Spending Accounts (FSA)

An FSA allows you to use pre-tax dollars for qualified medical or dependent care expenses, which lowers your taxable income. The key rule to remember is “use it or lose it”—funds typically do not roll over from one year to the next. Carefully estimate your upcoming year’s expenses to avoid forfeiting any money.

Health Savings Accounts (HSA)

An HSA is a powerful financial tool with a triple tax advantage:

Contributions are pre-tax.

Funds grow tax-free.

Withdrawals for qualified medical expenses are tax-free.

Unlike an FSA, an HSA is portable, meaning the account belongs to you even if you change jobs. This makes it an excellent long-term savings tool. After age 65, you can withdraw funds for any reason without penalty, although non-medical withdrawals are subject to income tax. Remember, an HSA is only available if you are enrolled in an HDHP.

Reviewing Other Important Benefits

Don’t stop at health insurance; open enrollment is the perfect time to review your other benefits.

Retirement Contributions

Check your retirement contributions to your 401(k) or 403(b). If your employer offers a matching contribution, be sure you’re contributing at least enough to get the full match—it’s free money! Consider increasing your contribution rate by at least 1% each year. Small, consistent increases can make a huge difference over time.

Life and Disability Insurance

Life Insurance: Review your coverage needs based on your dependents and debts. Your employer may provide basic coverage, but you might need supplemental, voluntary coverage to fully protect your loved ones.

Disability Insurance: This benefit protects your income if you are unable to work due to illness or injury. Review your short-term and long-term disability options to ensure your income is protected.

Final Steps and Action Plan

Making your benefit selections requires a few final steps to ensure you’re fully prepared.

Check Beneficiaries: In case of a major life change like a marriage or divorce, update the beneficiaries on all your accounts (retirement, life insurance) to ensure your assets go to the right people.

Gather Your Information: Have all your plan documents, a list of your regular doctors, and an estimate of last year’s medical expenses ready. This information will help you make a more accurate and informed choice.

Make Your Choices and Submit: Be mindful of the deadline and submit your final selections on time.

By taking the time to review your options and make informed decisions, you can ensure your benefits package is working for you and your financial well-being. Be sure to reach out to your advisor to discuss any of these items in more detail.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-6.png11522048Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-10-02 08:56:462025-10-02 08:56:52Financial Planning for Open Enrollment: A Guide to Making Smart Choices

Retirement is a major life shift, one that impacts more than just your schedule. It can reshape your sense of identity, daily habits and even your health. In fact, research has shown that retirement can raise the risk of heart disease and other medical issues by up to 40%. The reason? Experts point to a loss of purpose and reduced social connection, both of which can take a toll on mental and physical well-being.

Without a plan for how to spend your time meaningfully, the transition can bring unexpected emotional challenges.

The Risks of Unstructured Retirement

Many retirees begin this new chapter with a “honeymoon phase”—a period marked by the novelty of free time, relaxation or long-awaited travel plans. But this initial high can eventually fade.

When the excitement of sleeping in and checking items off the bucket list wears off, retirees can find themselves facing unexpected emotional challenges. Common struggles include boredom, loss of routine, identity shifts and social isolation. In fact, 24% of older adults are considered to be socially isolated. Isolation can also have a ripple effect on health: It’s associated with a 50% increase in risk of developing dementia and increased risk of premature mortality.

Designing a Retirement with Purpose

To avoid some of the potential pitfalls of an unstructured retirement, it’s important to think carefully—and proactively—about purpose. What do you want this next phase of life to look and feel like? Beyond financial planning, consider how you’ll meet the deeper needs your pre-retirement life—including work and raising kids—may have fulfilled: structure, identity, accomplishment, social connection and a sense of meaning.

What brings you pleasure and meaning? What have you always wanted to try or learn? Pursuing these activities can provide purpose and help ensure retirement’s not just a long vacation, but a rewarding chapter of your life.

Feeling stuck here? Try asking close friends or family what they see light you up. Often, others can reflect back passions or strengths that are hard to see on your own.

Staying Connected and Active

Relationships and physical routines matter more than ever when you retire. Staying active, both physically and socially, offers measurable health benefits. Regular physical activity lowers risks, including the likelihood of dementia, heart disease, stroke and eight types of cancer.

People-centered activity is important, too. Look for ways to stay engaged, whether through volunteering, mentoring, part-time work, creative pursuits or community involvement. Older volunteers, aged 55 and up, who gave 100 hours or more each year were two-thirds less likely to report poor health than non-volunteers.

Spending more time with family is a high priority for many retirees and can be a great way to fulfill social needs. But make sure that vision is shared. Open conversations with loved ones about time together, expectations and boundaries can help align plans and avoid disappointment down the road.

The Retirement Identity Shift

In many ways, it’s hard to define what retirement is. After all, it’s not a single moment but a series of transitions. For instance, rather than an abrupt shift to not working at all, you may consider bridge employment—usually part-time work in a temporary position or as a consultant in your field or in a different industry. This can offer a gradual shift into retirement, providing continued income and engagement as you adjust.

As your vision for retirement evolves, keep us in the loop. We’d love to hear what you’re planning—and we’re here to help ensure your financial strategy stays aligned with your goals.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/image-5.png11522048Emily Balmages, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgEmily Balmages, CFP®2025-09-26 07:38:002025-10-07 16:02:46The Power of Purpose in Retirement

As summer winds down, your thoughts may drift toward a final escape. Whether your idea of a perfect getaway is one last trip to a pristine beach, fishing in a mountain lake, or playing the back nine between pickleball matches, many of our clients have come to us over the years with the same question—should I buy a vacation home or just continue to rent?

As financial professionals, our answer is, “It depends.”

Renting a house for a week or two can be less expensive and time-consuming than buying a vacation property. Renting is a short-term commitment, while buying a second home often requires an ongoing investment of time and money. Renting allows you to choose different vacation destinations every year without maintenance and upkeep concerns. However, buyers can decide to rent out the property when they’re not there.

We caution our clients to consider the pros and cons before making decisions. While we aren’t real estate experts, we’ve compiled some information that you may find helpful.

Buying A Vacation Home

Non-Financial Considerations Many financial considerations must be pondered with a vacation property. Will you buy it outright or take out a mortgage? Are you interested in renting it when you’re not there? Will it impact your cash flow? There are also many nonfinancial issues you may want to consider, the most important being how a second home will affect your lifestyle.

Here are a few more aspects to consider before signing on the dotted line:

How Much Time Will You Spend There?1 If you only intend to spend a few weeks a year there, is renting a better choice? The expense and hassle of owning a second home may not be worth it unless you stay a few months each year to enjoy the place. Over time, you can develop friendships and become part of the community, making your second house more of a home.

How Does a Second Home Fit Into Your Travel Patterns?1 By owning a vacation home, you may spend less time traveling to other locations. Consider whether focusing vacation time on one location fits your desired travel patterns. For example, if you believe you’ll be happy spending all your free time in Florida, then buying may be right for you. However, you may feel tied down to one place if you like to travel the world.

Will a Second Home Increase Your Stress?1 Before buying, be aware of the potential stress of owning a second home. Like your primary residence, you’ll need to deal with utilities, maintenance, repairs, and other considerations. While you may find these issues worth the benefits of owning a vacation home, you should enter ownership with your eyes wide open.

Will Purchasing a Vacation Home Enhance Your Experiences and Relationships?1 If your vacation home becomes a hub for family and friends to visit and for you to engage in social activities and adventures with them, owning a second home can increase your happiness. Clients who enjoy their vacation homes the most tend to create memories through experiences with family and friends at their second homes. On the other hand, buying a vacation home primarily as a relaxing retreat may not add much to your overall happiness—despite the weather and scenery.

What Are the Potential Advantages of Buying a Vacation Property2 There are many good reasons to buy a vacation home. After considering the aforementioned nonfinancial factors, it may be the right course of action for you and your family. Here are some potential benefits:

Possible Real Estate Appreciation: One potential advantage to buying a vacation property is that the value of the real estate may increase over time. Of course, there are no guarantees, and your property could lose value.

Renting Costs for Your Vacation: Owning a property in a vacation spot means you won’t need to pay for weekly accommodations.

Perhaps Generate Rental Income: Another benefit to buying a vacation property is the opportunity to generate rental income. If you choose a vacation home in a bustling short-term rental market, you may have the chance to rent out your place when you’re not in town.

Convenience: Owning a vacation home can be more convenient than arranging short-term rentals. It’s also more familiar, comfortable, and allows you to host friends and family.

Retirement: A vacation home can be part of your retirement strategy. Some clients have used their second homes in later life and moved in permanently.

Potential Disadvantages of Buying a Vacation Property

Of course, where there are pros, there are cons. While we don’t want to rain on anyone’s parade, as financial professionals, we strive to provide a fair and balanced view. So, here are some of the potential downsides of buying a vacation property:

Money Management: Buying a property can be costly, especially a second home in an expensive vacation area. In addition to initial costs, there are also ongoing maintenance and other costs. If money is an issue, buying another house may not be your best choice.2

Financing: If you cannot self-finance your purchase, financing a vacation home can be challenging because of different mortgage requirements. A higher credit score and a larger down payment are often required to qualify for a mortgage. So, if you are not paying in cash, expect a more complicated financing experience than purchasing a primary residence.2

Property Management: If you plan to generate rental income when you’re not using your vacation home, you may want to hire a property manager to find renters, collect rent, and clean the place. This could add up to 15% of the rental income.2

Inconsistent Rental Income: Rental income often depends on the season or certain times of the year. There are usually seasonal periods when no one might rent. Vacation property rental income is impacted directly by the destination and its popular times, which can affect income.2

Lack of Disaster Aid: FEMA disaster assistance is limited to your primary home, i.e., where you live for more than six months out of the year. Second homes or vacation homes used as vacation rentals don’t qualify for FEMA assistance. Thus, if hurricanes, wildfires, or floods destroy or damage your second home, you must rely on other options.3

Markets for Luxury Second Homes

While demand for luxury second homes rose during the pandemic, you may think that today’s relatively high interest rates, tight inventory, and uncertain economic environment would’ve damaged the market. They haven’t.4

Despite the numerous challenges hitting residential real estate, the luxury housing market has remained strong. According to The Agency’s 2025 Red Paper, the number of U.S. homes selling for $1 million-plus increased by 5.2% in the first half of 2024, while the median price for high-end properties rose by 14.2%. Compared with the broader market, in which overall home sales fell by 12.9%, the median price increased by just 5% over the same period.4

With more cash on hand and fewer financial constraints, wealthy homebuyers are often less reliant on loans. According to The Agency’s report, homebuyers paid cash for nearly half of all luxury homes sold in the first quarter of 2024.4 So, if you’re in the market for a high-end second home, you’re in good company.

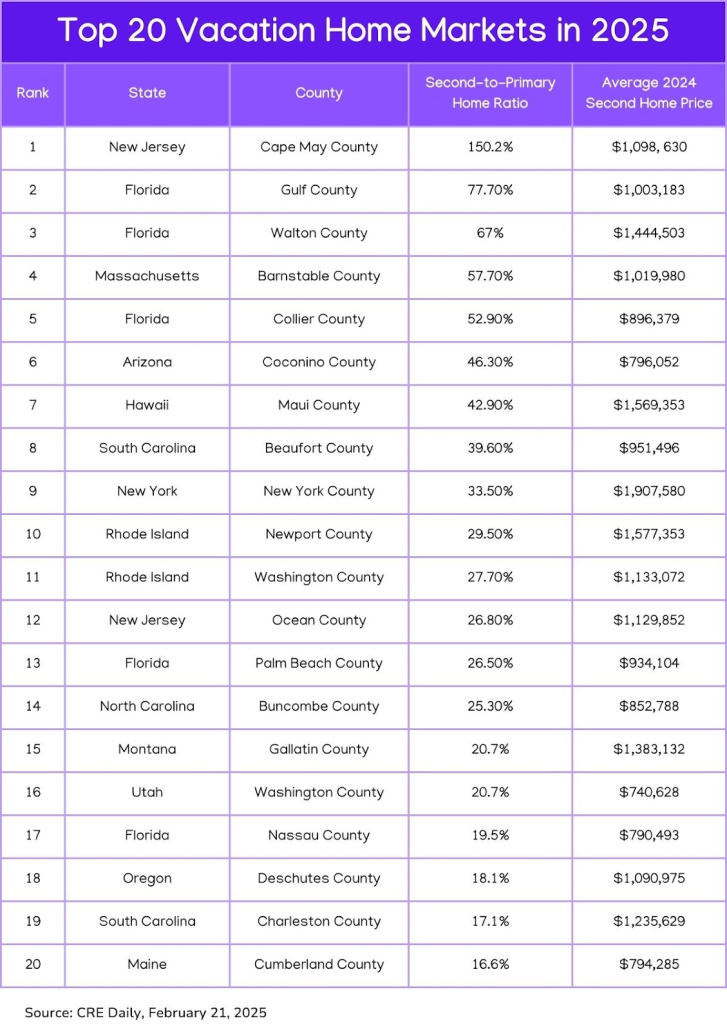

Real estate company Pacaso analyzed the markets with the most significant year-over-year growth in luxury second-home transactions from 2023 to 2024 and average prices for second homes. They believe these second-home destinations could see more growth this year.4

As you’ll see in the chart below, Cape May County, New Jersey, with its Victorian charm and sandy beaches, ranked as the top spot for second home purchases in 2025, with Gulf County, Florida, coming in as a distant runner-up.4

Suppose you’re looking for a second home selling at under $1 million. Washington County, Utah, near Zion National Park; Coconino County, Arizona, near Flagstaff; and Cumberland County in south-central Maine along the coast are popular locations.4

Insurance Considerations for Second Homes

Unless you have the resources to “self-insure,” you might want to consider homeowners insurance to protect your real estate purchase. Second home insurance is a specialized policy designed to cover properties that are not your primary residence. Policies differ because a second home may have additional risks not associated with your primary residence.

Standard homeowners’ insurance for a full-time residence costs an average of $1,754 per year, but you might pay more for a second home insurance policy. For example, American Family estimates that vacation home policies are typically two to three times more expensive than home insurance for a full-time residence.5

The additional risks that cause second home insurance to be higher include:6

Vacancy Periods: Unoccupied homes are more vulnerable to theft or damage.

Location-Based Risks: Coastal or mountainous properties may face specific hazards like hurricanes, floods, or wildfires.

Higher-End Property: If your second home is a luxury property, consider high-value property insurance.

Rental Use: If you rent to others, you may face additional liability concerns, such as tenant-caused damages and liability for injuries sustained by renters or their guests.

Banks will require that your second home be insured if you take out a mortgage. If you are paying cash, the insurance coverage you want, if any, is up to you. If you seek coverage, you should evaluate risks, compare providers, and determine if the policy aligns with your needs and property usage.

Including a Vacation Home in Your Estate

If you buy a vacation home, consider what happens to the property after you’re gone. If a family vacation home is part of your estate, you should put the time and effort into outlining your intentions for the next generation. Your heirs should know what they’re getting and the time, effort, and resources they’ll need to put into the property to keep it functioning well. You know your family’s dynamics and that not all of your heirs will have that same level of interest or involvement in the family vacation home. Thus, be mindful of this and flexible when creating your strategy.7

Consider working with your financial professional and estate team to determine the best way to transfer your vacation home based on your situation. Here are a few choices you may want to evaluate:7

Sell the house outright or gift it to one or more of your children.

Establish a trust in which one or more trustees are responsible for owning and maintaining the property. Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional familiar with the relevant rules and regulations.

Form an LLC or other legal entity where your heirs will be owners and follow specific governance rules and operating agreements in how the property is used.

As financial professionals, we can offer insights into how your vacation house may contribute to your overall estate strategy.

Tax Implications of Owning a Second Home

As we mentioned before, we’re not tax experts, but we work with people who are. We’re outlining some general information, but it’s not a replacement for real-life advice. Consult your tax, legal, and accounting professionals for more specifics regarding your second home.

If your second home is a residential home, you may be able to deduct mortgage interest up to $750,000 as long as the second home is the one that secures the loan. If your mortgage on your second home originated before Dec. 16, 2017, you can deduct up to $1 million in mortgage interest. You also can deduct state and local property taxes––up to $10,000 combined for all real estate taxes between your homes.8

If you rent your property for 14 days or less during the year, you may not need to report this as income to the IRS.8

If you rent your second home for more than 14 days a year, the IRS considers it an investment property. If your second home is an investment property, you might be able to deduct mortgage interest or real estate taxes on your personal income tax return. Still, you may be able to deduct those costs against your rental business income.8

When you sell your second home, you must be aware that you may not receive the same capital gains tax deduction when selling your primary residence – $250,000 for single filers and $500,000 for married.8

Renting a Vacation Home

If you have gone through all the pros and cons of buying a vacation home and are leaning toward renting, this approach also has two sides. Let’s start with the positives.

Potential advantages of renting a vacation home2

Little Responsibility: If you choose to rent a vacation home, your only responsibility is to leave the house the same way you found it. None of the property maintenance or utilities fall onto a short-term renter to take care of, which means you can enjoy your holiday and then dump your garbage on the way out, turn out the lights, and lock the door behind you.

Variety of Options: Renting vacation homes means renting a different home anywhere you go. You won’t be limited to revisiting the same place over and over. Instead, you can change locations each time you go on vacation and experiment with the type of property to see what you enjoy best – in town or out, kid-friendly or over 55, nightlife or peace and quiet, etc.

Cost Considerations: Renting a vacation home can be a more affordable way to go on various vacations in many areas. After all, you will not pay a mortgage, maintenance fees, or other charges.

Disadvantages of Renting a Vacation Home

Anyone who has rented a vacation home knows that there are some downsides. Here are a few of them:

Cost: In 2024, the expected average daily rate for U.S. vacation rentals is $326.9 This number will fluctuate based on the type of home you rent. A luxury rental could be significantly higher.

Not Your Space: When renting a vacation property, you live in someone else’s home. For many people, it’s never as comfortable as staying in a place you own. You may find problems with the house, it may not have all the features you are accustomed to, and you may need a learning curve to figure out how to use everything from the TV to the thermostat.2

Availability: You may need to book your vacation homes well in advance during peak seasons. Chances are you want to go away at the same time of year, but others have the same idea. Availability can be problematic if you book too late or the area is extremely popular.2

Inconvenient: Renting a vacation home can be a hassle. You have to choose the home, make sure it’s available when you want, and then go through the booking process with the owner, the property manager, or a third-party website. If anything accidentally breaks during your stay, you’ll also be liable to cover it. There can also be unexpected fees that drive up the price.2

Make Your Decision Carefully

I’m sure you’ve gone on vacation to a terrific location and fallen in love with it. The experience might have been so wonderful that you thought about buying a home to spend more time there. That’s how the time-share industry became so popular in the 1970s and 80s—catering to impulse buyers.

However, it’s important to remember that while you might be swayed by the most enjoyable aspects of your vacation, you should consider the negative factors that owning a second home can bring. Between costs, extra work of taking care of another property, and the impact on your other travel habits, owning a vacation home can have drawbacks. You also may want to factor in how being away could impact your relationships back home.

Before you commit to buying a vacation property, you might want to consider living there for a month or two first. Spending an extended amount of time in a rental property at your intended vacation home location may provide you with a more realistic view of the area.

There is no right or wrong answer on whether to buy or rent a vacation home. Please take the time to weigh the pros and cons thoroughly before deciding. Please do not hesitate to contact us if we can help or just be an impartial sounding board.

Veronica Cabral

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/09/Buy-vs-Rent.png10801080Veronica Cabral, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgVeronica Cabral, CFP®2025-09-04 10:39:142025-09-04 10:39:19Is It Smarter to Buy or Rent a Second Home?

The “One Big Beautiful Bill Act” (OBBBA), signed July 4, 2025, is poised to significantly impact nearly every aspect of your financial life. From your tax bill to your healthcare and your children’s future savings, understanding the nuances of this bill is crucial for effective financial planning.

Here’s a breakdown of what the OBBB means for you:

Tax Planning: More in Your Pocket, But Mind the Details

The OBBB makes permanent many of the individual income tax rates and brackets from the 2017 Tax Cuts and Jobs Act (TCJA), providing long-term clarity. But there’s more:

Expanded Standard Deduction: The standard deduction sees a permanent expansion, making tax filing simpler for many and potentially reducing the need to itemize.

Temporary Deductions (2025-2028): Get ready for some new, but temporary, tax breaks.

No Tax on Tips/Overtime: If you earn qualified tip income (up to $25,000) or overtime premium pay (up to $12,500 for individuals, $25,000 for joint filers), you may be able to deduct it. Keep an eye on income phase-outs.

Senior Tax Deduction: Individuals 65 and older meeting income thresholds ($75,000 single, $150,000 joint) can claim an additional $6,000 deduction, aiming to offset federal taxes on Social Security.

Auto Loan Interest Deduction: A temporary deduction of up to $10,000 for interest on loans for U.S.-assembled vehicles is available, subject to income phase-outs.

Increased SALT Deduction Cap: For five years, the State and Local Tax (SALT) deduction cap temporarily increases to $40,000 (from $10,000), with income-based phase-outs. This is a win for residents of high-tax states.

Enhanced Child Tax Credit: The Child Tax Credit permanently increases to $2,200 per child and will be indexed for inflation.

Business Tax Incentives: Businesses will see the reinstatement of 100% bonus depreciation and permanent Section 199A (Qualified Business Income) deduction, encouraging investment.

Estate and Gift Tax Relief: The unified credit and Generation-Skipping Transfer Tax (GSTT) exemption thresholds are permanently increased to $15 million per individual, offering substantial relief for high-net-worth individuals.

Your Action Plan: Review your current tax strategies with a financial advisor to maximize these new permanent and temporary provisions. Consider whether itemizing still makes sense for you.

Healthcare & Social Programs: A Shifting Landscape

The OBBB includes significant cuts to federal funding for vital social programs:

Medicaid Changes: Expect cuts to Medicaid funding and new work requirements for many adult beneficiaries. If you or your loved ones rely on Medicaid, be aware of potential reduced coverage or new eligibility hurdles.

SNAP (Food Assistance) Adjustments: The Supplemental Nutrition Assistance Program (SNAP) also faces federal funding cuts and expanded work requirements.

Affordable Care Act (ACA) Implications: New eligibility verification requirements are imposed for ACA marketplace coverage, and enhanced tax credits for ACA coverage are set to expire. This could lead to higher out-of-pocket premium payments for many, particularly older adults. The CBO estimates these changes could lead to a significant increase in the uninsured population.

Your Action Plan: Reassess your healthcare and benefits planning. Explore alternative options if you’re impacted by changes to Medicaid or ACA, and adjust your budget accordingly.

Retirement & Savings: New Avenues and Program Shifts

The bill introduces both opportunities and challenges for your long-term financial goals:

“Trump Accounts” for Children: A brand-new savings option for newborns. These “Trump Accounts” receive an initial federal contribution of $1,000, with parents able to contribute up to $5,000 annually. Classified as IRAs, gains are tax-deferred until age 18. This is a new consideration for long-term savings for your children.

Student Loan Program Overhaul: Federal student loan programs are undergoing significant alterations, potentially ending subsidized and income-driven repayment options. Limits are also placed on Pell Grant eligibility. Current and future students will need to adjust their education financial planning.

HSA and 529 Expansion: Good news for healthcare and education savings. Eligible uses for Health Savings Accounts (HSAs) and 529 education savings plans are expanded, offering more flexibility.

Social Security Outlook: While the bill provides some temporary tax relief for seniors, its overall impact on the national debt could accelerate the insolvency of Social Security. This is a long-term consideration for retirement planning.

Your Action Plan: Evaluate “Trump Accounts” alongside existing savings vehicles like 529 plans. If you have student loans or are planning for higher education, understand the new repayment and eligibility rules. Review how you leverage your HSA and 529 plans for maximum benefit.

Investment & Business Considerations: Adapting to Policy Shifts

The OBBB also brings changes that could influence your investment portfolio:

Clean Energy Tax Credits: Many clean energy tax credits from the Inflation Reduction Act are being phased out, which may impact investments in renewable energy and electric vehicles.

Fossil Fuel Promotion: The bill promotes increased domestic oil and gas production, which could influence investment strategies in the energy sector.

Your Action Plan: Consider how these policy shifts might affect your investment portfolio. Diversification and a long-term perspective remain key.

Overall Financial Planning Implications: A Holistic Approach

The “Big Beautiful Bill” is a game-changer. It necessitates a comprehensive review of your financial strategy.

Review Tax Strategies: Don’t miss out on new deductions!

Reassess Healthcare and Benefits Planning: Understand potential impacts on coverage and eligibility.

Evaluate Savings Options: Explore new opportunities like “Trump Accounts” and expanded HSA/529 uses.

Update Estate Plans: High-net-worth individuals should revisit their estate plans due to increased exemptions.

Adjust Investment Portfolios: Align your investments with the new economic realities. If you’re a client of ours, we’ve already done this for you.

The “One Big Beautiful Bill” is far-reaching. Given its complexity, consulting with a qualified financial advisor and tax professional is highly recommended to understand how these provisions specifically impact your unique financial situation and to adjust your plans accordingly. Schedule time with a Warren Street advisor today. .

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/07/Big-Beautiful-Bill.png10801080Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-07-10 12:14:072025-07-10 12:15:13The “Big Beautiful Bill”: What It Means for Your Finances

Statistics show that nearly 33% of Americans have faced some identity theft attempts in their lives, and experts estimate there is a new case of identity theft every 22 seconds. As financial professionals, one of our primary goals is to help our clients create a financial strategy and protect their wealth. In today’s digital age, identity theft threatens your finances, so it’s crucial to understand the risks and take proactive measures.1

This blog aims to equip you with practical strategies for protecting your personal and financial information with the goal of maintaining your financial well-being.

The most common types of identity theft are1:

Credit card fraud

Government documents or benefits fraud

Loan or lease fraud

How Identity Theft Impacts Your Finances

The financial hardships caused by identity theft can last for months or even years after your personal information is exposed. Depending on the type of data identity thieves obtain, the recovery process can involve several hurdles. Victims often need to dispute fraudulent activities in their credit files and work to restore their good credit. This may include cleaning up and making changes to compromised bank accounts.2

If an identity thief uses your Social Security number to obtain employment, you may need to work with the Social Security Administration. Similarly, if you become a victim of tax refund identity theft or an identity thief’s income makes it appear you are under-reporting your income, you may need to work with the IRS.2

Identity theft involving sensitive, personally identifiable information like your Social Security number can have long-lasting effects. Thieves may wait months or even years to use your information, or they might sell it on the dark web, requiring you to stay vigilant indefinitely. Legal fees and other costs could add to the financial impact if your identity theft issue is complex. Some victims even need to seek government assistance during recovery, highlighting the potential magnitude of identity theft hardships.2

Steps You Can Take to Help Protect Yourself

It can be difficult for victims to deal with identity security issues because bad actors are becoming more sophisticated all the time. You can use technology-enabled safeguards to help protect your identity and personal data, such as antivirus protection software, password managers, identity theft protection, virtual personal networks, and two-factor authentication on devices and accounts. There are also other actions you can take to help manage the risk of becoming a victim, including:

1. Check your mail often.

A low-tech way criminals can steal your identity is to simply take bank or credit card statements, utility bills, health care or tax forms, or pre-approved credit card offers out of your mailbox. So, don’t let your mail sit uncollected too long. Also, if you are going away, have a trusted neighbor bring in your mail or put your mail on hold with the post office.3

2. Review credit card and bank statements regularly.

By reviewing your credit card and bank statements, you may be able to spot any suspicious activity. Thieves with your credit card number or bank account information could make small purchases to see if they can get away with it. These transactions can go unnoticed. Thieves may try to make large purchases if they get away with minor ones.3

3. Freeze your credit.

In some cases, you may want to consider freezing your credit file so no one can look at or request your credit report. That means no one can open an account, apply for a loan, or get a new credit card while your credit is frozen. Remember, a credit freeze applies to you as well. To get started, contact each of the three major credit reporting agencies. In some instances, credit freezes are free and won’t impact your credit score.3

4. Don’t use the same password twice.

According to the Federal Trade Commission (FTC), secure passwords are longer, more complex, and unique. Many people use the same password for multiple accounts, which could be problematic. You should consider creating different passwords for various accounts and avoid using information related to your identity, such as the last four digits of your Social Security number, your birthday, your initials, or parts of your name.3

The FBI and the National Institute of Standards and Technology have issued guidelines stating that passwords should consist of at least 15 characters because these are more difficult for a computer program or hacker to crack. Regarding security questions, the FTC’s guidelines suggest questions that only you can answer; avoid information that could be available online, such as your ZIP code, city of birth, or mother’s maiden name.3

5. Consider shredding documents with personal information.

As stated earlier, not all identity theft is high-tech. Old-fashioned dumpster diving might sound like a thing of the past, but it still happens. Consider buying a household shredder and destroying sensitive paperwork, such as credit card and bank statements, utility bills, and other documents containing personally identifiable information.3

6. Opt out of prescreened credit card offers.

Credit card companies often send prescreened offers to open new accounts, and criminals can intercept these mailed or emailed offers and open accounts in your name. One way to help avoid a potential identity theft issue is to opt out of receiving these offers.2

Day-to-Day Security Best Practices

Small steps can make a big difference when it comes to keeping your information safe. Here are a few suggestions, starting with cleaning out your wallet.

1. Keep your Social Security card at home in a safe location—not in your wallet.

Those nine digits can help an identity thief to obtain loans or credit card accounts in your name. A bad actor could also use your Social Security number with the IRS.

2. Leave checks and deposit slips at home.

Consider leaving checks and deposit slips at home. These items may contain more information than you think, including your name, address, bank name, routing number, and account number.

3. Shred and trash any password cheat sheets.

Scraps of paper with sensitive information, such as PINs and passwords, can be risky, so dispose of any you have in your wallet after noting them in a password manager at home

4. Limit the number of credit cards in your wallet.

It may be best to limit the number of credit cards in your wallet. The same goes for excess cash and gift cards.

5. Bypass the PIN at the gas pump.5

One of the most common schemes is when criminals install a skimming device directly over the credit card slot at a gas pump. These skimmers capture and store your card data when you insert or swipe your card. If something looks off, don’t use that pump. Also, if you use a debit card to pay for your gas, bypass the PIN if possible and use your zip code instead. That may prevent someone from stealing your PIN using a pinhole camera.

Dispose of Old Devices Safely

Improper disposal of old digital devices is a key but often overlooked aspect of identity theft. Simply deleting files may not be enough on some digital devices, as thieves may be able to recover the data. Therefore, safe disposal is critical. Many communities have secure electronics recycling events where devices can be disposed of. However, it’s important to note that different devices and storage media types may require different disposal methods.

Identity Theft Protection Services

Identity theft protection services offer a range of features designed to detect identity theft, alert you to identity theft, and help you recover from identity theft. These services typically monitor credit reports, dark web activity, and public records for signs of fraudulent use of personal information. When suspicious activity is detected, they alert the user and provide next steps. While these services can be helpful, their effectiveness can vary. However, these services can be a valuable first step for those who lack the time or expertise to monitor their credit and personal information.

What to Do if Your Identity Has Been Stolen

You may not know that you have been a victim of identity theft immediately when it happens, but there are warning signs you can look out for, such as:6

Bills for items you did not buy

Debt collection calls for accounts you did not open

Information on your credit report for accounts you did not open

Denials of loan applications

Mail stops coming to or is missing from your mailbox

If you are a victim of identity theft, you may want to place fraud alerts or security freezes on your credit reports. A fraud alert requires creditors to verify your identity before opening a new account, issuing an additional card, or increasing the credit limit on an existing account based on a consumer’s request.

Pro tip: When you place a fraud alert on your credit report at one of the nationwide credit reporting companies, it must notify the others.7

Protecting your identity is an integral part of maintaining your overall financial health. As financial professionals, we believe safeguarding your personal information can be as crucial as making sound investment decisions. By implementing these preventive measures and staying vigilant, you can help manage the risk of becoming a victim of identity theft. Remember, your financial security encompasses every aspect of your financial life.

If you have any concerns about identity theft or would like to discuss how it fits into your broader financial strategy, don’t hesitate to contact us. We’re here to help provide you with information that can help improve your personal finances.

Emily Balmages, CFP®

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

This blog is for informational purposes only and is not a replacement for real-life advice. We encourage you to consult your tax, legal, and accounting professionals if you believe identity theft involves using your tax records.2

What should you do if you’ve just received a big bonus at work, inherited some money, sold a business, or come into a financial windfall? Should you invest it all at once, even if the market feels high or low, or take a gradual approach by investing in smaller increments over time?

This is a common question we hear from clients and investors alike. It’s no surprise—deciding how to invest a significant sum of money can feel overwhelming. What if you invest it now and the market drops? Or, what if you wait and the market takes off? It’s natural to worry about making the wrong choice or missing out on potential gains.

Both investing a lump sum immediately and spreading it out over time come with their pros and cons. Let’s explore some key factors to help guide your decision.

Start with Your Goals

Before making any investment decisions, consider your financial goals.

If you need the money for short-term purposes, like upcoming college tuition, the market’s volatility could be a concern. In this case, conservative options like short-term bonds, bond funds, or CDs might be better suited to protect your funds.

For long-term goals, such as retirement, investing in the stock market may be a better choice. Despite short-term fluctuations, the market has historically trended upward over time.

Compare Lump-Sum Investing vs. Dollar-Cost Averaging

Investing a lump sum means your money is fully exposed to the market immediately, allowing you to benefit from any immediate gains if the market is rising. However, since markets are unpredictable, a downturn could occur soon after you invest.

If the risk of short-term losses makes you uneasy, dollar-cost averaging (DCA)—where you invest a fixed amount at regular intervals—might be a more comfortable approach. For instance, you could invest $12,000 by putting in $1,000 monthly over a year. This way, you buy more shares when prices are low and fewer when they’re high, helping you manage the average cost over time.

Keep in mind, though, that research shows lump-sum investing outperforms DCA 68% of the time. If maximizing returns is your main goal, lump-sum investing could be the better option. However, if you’re worried about losses and potential emotional reactions, DCA may be worth the slight reduction in expected returns.

Don’t Wait to Invest

Historically, stocks and bonds outperform cash over the long term, so it’s important to start investing as soon as possible. Holding off is essentially an attempt to time the market, which is notoriously difficult. In 2023, equity fund investor returns trailed the S&P 500 by 5.5%, largely due to market timing efforts.

Both lump-sum investing and DCA help you avoid this pitfall, letting you benefit from the market’s long-term growth. The key is choosing the strategy that aligns with your risk tolerance and long-term plan.

If you’re unsure which strategy is best for you, reach out—we’d be happy to help you decide.

Justin D. Rucci, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/04/Lump-Sum.png12602240Justin D. Rucci, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgJustin D. Rucci, CFP®2025-04-17 07:16:422025-04-17 07:19:16I’ve Got a Lump Sum in Cash, Should I Invest It Right Away?