Equity Compensation: Benefits and Risks You Need to Know

A small slice of equity compensation can boost your income, while a larger slice might bring a significant financial windfall. However, luck and careful management play crucial roles. Balancing the risks and rewards of your equity compensation is essential. Understanding how it fits into your overall financial plan can help you maximize benefits and avoid concentration risk—the danger of having too much wealth in one stock.

Equity Compensation Basics

Equity compensation comes in various forms, such as stock options, restricted stock units, or employee stock purchase plans. The equity package you receive might come with a vesting schedule, which determines how quickly you’re able to take ownership of your shares. For companies, these vesting schedules accomplish an important goal: They help keep you around longer.

Understanding every part of your equity compensation package is essential. This includes vesting rules, types of shares, expiration dates for exercising stock options, and tax implications. Missing an expiration date can mean losing the chance to buy company stock at a discount, and knowing the tax details can help you manage your tax burden and retain more of your hard-earned equity. While you don’t need to master every detail, it’s crucial to understand your equity compensation offer.

At Warren Street, we guide clients through the wealth-building potential of their executive compensation packages. We help you maximize opportunities, integrate the package with your broader financial goals, and collaborate with other resources. For example, your company’s HR department or benefits administrator can provide details, your accountant can advise on taxes, and a lawyer can help with legal aspects and estate planning related to your equity compensation.

Understanding the Risks of Equity Compensation

One downside of equity compensation is that it can tie up a large portion of your wealth in a single stock. This is known as concentration risk.

Not all risk is bad. In fact, a foundational part of investing is taking on risk in exchange for potentially higher returns. This is systemic risk—the risk inherent in the financial markets at large. However, concentration risk means your wealth is closely tied to one company’s performance, posing significant danger if the company faces issues like scandals or competitive disruptions.

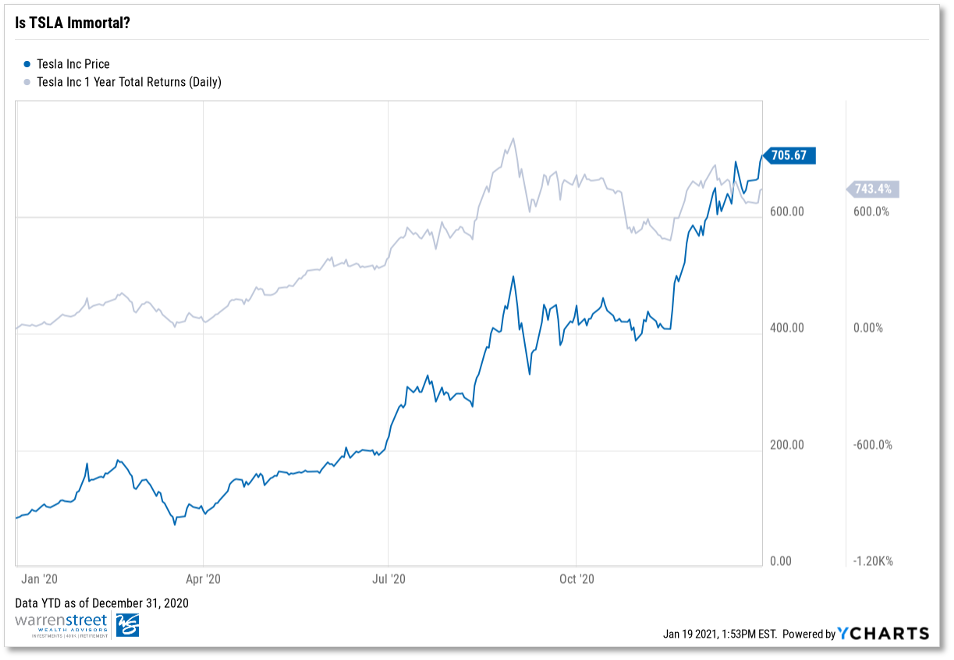

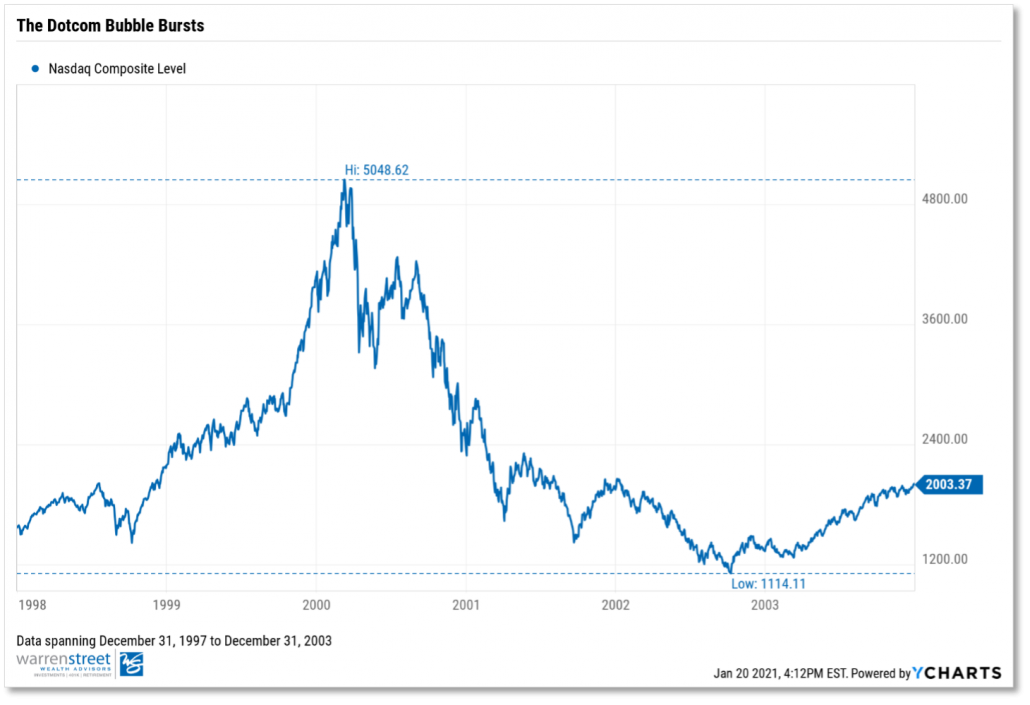

Relying on your employer for income and savings can be risky. If the company performs poorly, you could lose both your job and a significant part of your wealth. For example, during the 2020 pandemic, ridesharing company stock prices tended to lose value as ridership plummeted. These companies laid off thousands of workers, and employees lost both jobs and equity value.

“But” you may counter, “I know my own company, and I’m confident its future is bright.” This is a common reaction—and may be a sign you’re falling into a common behavioral tendency known as familiarity bias. It can lead you to the false assumption that your own company is safer, and your familiarity may actually be keeping you from making a level-headed investment decision. Instead, lean on objective data and research rather than feelings to inform your investment decisions.

Solving Concentration Risk

Minimize concentration risk by diversifying, carefully divesting company shares, and investing in broad market funds. This approach smooths out volatility, maximizes long-term returns, and manages systemic risks.

If you work for a privately held company, selling your shares can be more tricky—and perhaps not possible. In that case, we can help you explore options to reduce risk. For example, that may mean building a larger emergency fund to give you more protection from the unexpected or exploring financial strategies to hedge your equity position.

No matter your equity compensation package, you don’t have to navigate its complexities alone. Contact us to discuss your options and maximize your financial potential.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.