The headlines are hard to miss. SpaceX. Anthropic. OpenAI. Three of the most talked-about private companies in history are preparing to go public — and together, they could raise more money in a matter of months than the entire U.S. IPO market raised all of last year. Today on the blog, we explore what to expect from the hottest Wall Street darlings and what these shiny objects mean for markets.

Let’s Set the Table

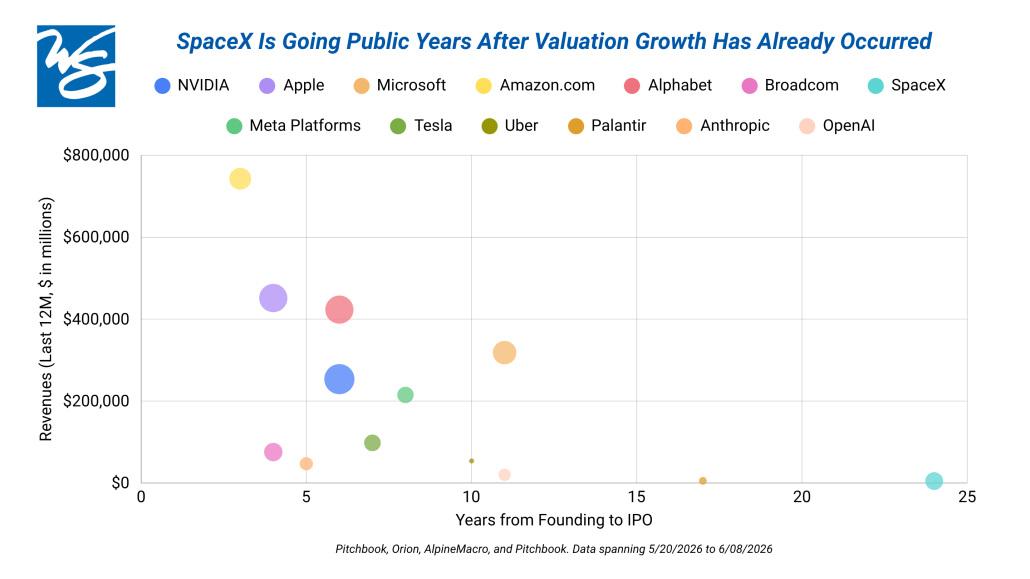

In 2025, the entire U.S. IPO market raised $77 billion. SpaceX alone is targeting a $75 billion raise — add Anthropic ($60–65 billion) and OpenAI ($60 billion), and you’re looking at a combined raise close to $200 billion.

These are no longer the scrappy startups where early public investors get in on the ground floor. Much of the value has already been captured by venture capitalists and private investors. Before going public, SpaceX was reportedly valued at ~$1.25 trillion, Anthropic at ~$900 billion, and OpenAI at ~$825 billion — nearly $3 trillion in private market value accumulated behind the scenes. SpaceX here is the outlier, going public 24 years after inception as indicated by the turquoise bubble in the chart above.

Don’t Forget to Ask — Why Now?

I usually view IPOs with a skeptical eye – not because success stories can’t be made, but because an information asymmetry will permanently exist. Insiders can tell when the public is overpaying for their company and use it as an opportunity to cash out. So why go public now?

These companies need cash. Building cutting-edge AI and sending rockets to space is extraordinarily expensive. Going public gives them a massive influx of capital to fund that growth.

Early investors need an exit. Founders, employees, and early-stage investors have been waiting years to convert paper gains into real dollars. It’s also worth noting: history has eerie examples of companies timing public offerings around industry peaks — Blackstone before the 2008 real estate crisis, Glencore before the 2011 commodity cycle pop. Worth pausing a moment for.

The market is excited. The AI investment environment has been exceptionally strong, recovering from the skepticism that characterized earlier this year.

What Comes After the Honeymoon?

IPOs are often explosive in the short-term — a honeymoon period followed by selling pressures where the relationship starts to go south. Here’s what to expect:

Short-term: Prices get a boost from engineered scarcity (companies deliberately underprice and limit tradable shares), retail enthusiasm and FOMO, and index fund buying — which could account for approximately 17–24% of tradable shares within the first 15 trading days, based on estimates from AlpineMacro.

Medium-term: Here comes the reality-check. Lock-up expirations release insider shares onto the market, applying downward pressure on prices. This year, those lock-ups are unusually concentrated in adjacent AI and tech companies, introducing more fragility than prior cycles. It’s also worth noting that most IPO’s have underperformed their broader industry in the 12 months following launch, with gains often concentrating in only a small number of big winners while the rest disappoint. Past performance and historical trends are not indicative of future results.

Longer-term — the Index Dilemma: Major index providers like S&P and Nasdaq are reportedly bending their own rules to fast-track these mega-IPOs into their benchmarks. Most consequentially, S&P is considering relaxing its profitability requirement. As these stocks join indexes and lock-ups expire, automated buying algorithms will be forced to fund those purchases by selling something else — most likely the largest, most liquid names: Apple, Microsoft, Nvidia.

Investment Implications

If these IPOs execute well, it’s a green light for the AI trade and would lift companies across the ecosystem. If they stumble, it’s a meaningful warning signal for anyone spending heavily without yet turning a profit.

We believe the index risk is the more underrated story. When index rules are bent to accommodate unprofitable companies, the passive investor is quietly exposed to degraded quality screens, less certain cash flow trajectories, and deeper AI concentration. It blurs the line between passive and active investing — and you have to ask yourself: what am I really owning?

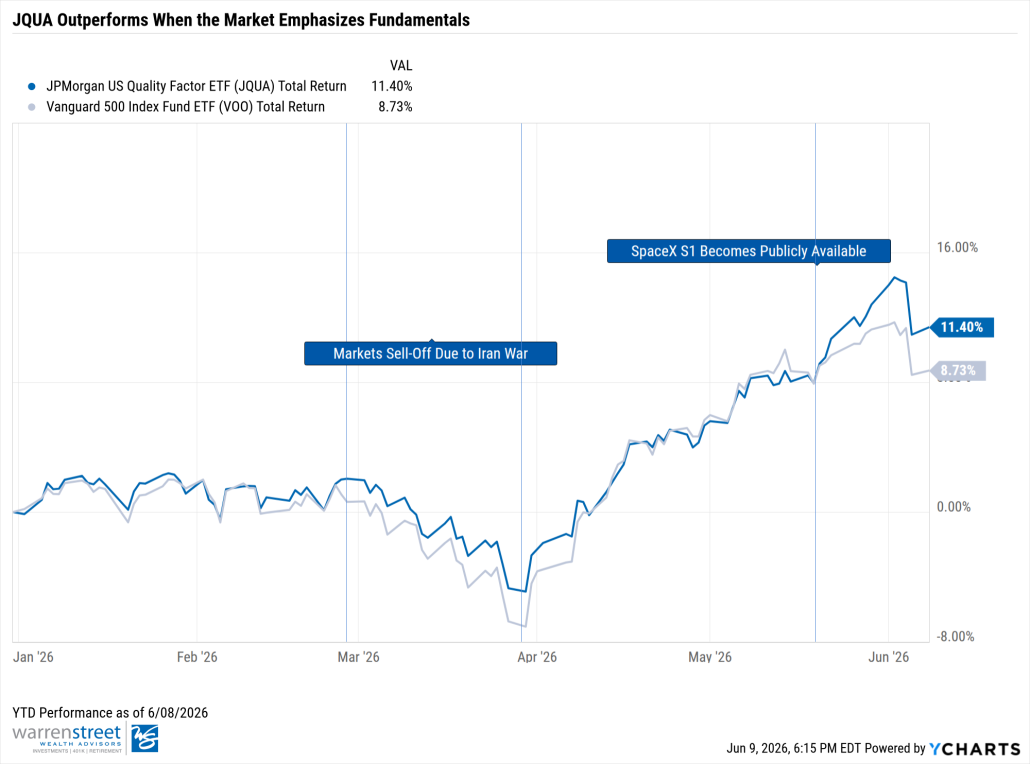

In this environment, we continue to rely on our pairing of market-Cap weighted S&P 500 exposure alongside quality-focused ETFs (for example, JQUA, the JPMorgan U.S. Quality Factor ETF), depending on client objectives and risk tolerance. JQUA generally focuses on companies with strong earnings, healthy balance sheets, high returns on equity, and manageable debt – qualities (no pun intended) meant to ground investments in fundamentals when narratives run ahead of numbers. We believe this approach may allow portfolios to participate broadly in market enthusiasm, depending on client objectives and risk tolerance.

Our Take

We recognize the excitement surrounding this IPO wave, but our role is to navigate these waves with discipline. While these are compelling names and future portfolio candidates across our fund managers, we believe the more prudent approach is to allow valuations to normalize, narratives to mature, and market expectations to recalibrate before committing capital. In other words, we are letting quality discipline and our understanding of IPO markets – not enthusiasm – guide your portfolio’s trajectory.

Name, Company

Phillip Law, CFA

Senior Portfolio Manager

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors and/or its clients may hold positions in the securities mentioned. Holdings may change at any time without notice. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/06/IPO-Mania.png10801080Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2026-06-10 15:01:402026-07-01 14:25:22IPO Mania: What the Rocket Ships, Chatbots, and Rule Changes Mean for Your Portfolio

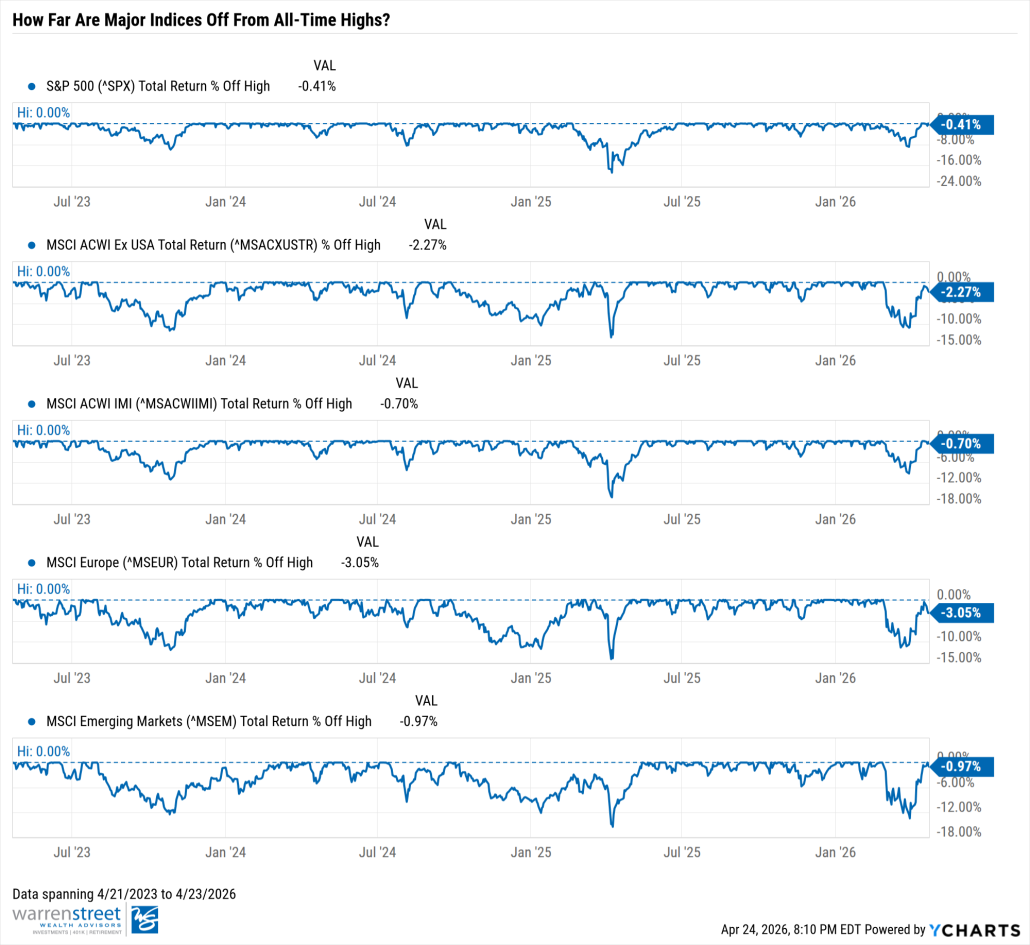

Last month, we emphasized the unpredictability of geopolitical risk and acknowledged its limited ability to depress longer-term returns. Today, we observe roughly 80 oil tankers stranded at sea, a supply shortfall of 9 million barrels per day, and a ceasefire so fragile that ships are still being bombarded. Yet, markets are hovering near all-time highs.

It seems as if markets have already asked, “Will this war matter in a year?” and answered “Probably not.” Are they correct to think that the worst is behind us, or are we seeing an irrational optimism? More importantly, how are we thinking and what are we doing about it?

Both Sides Are Boxed In

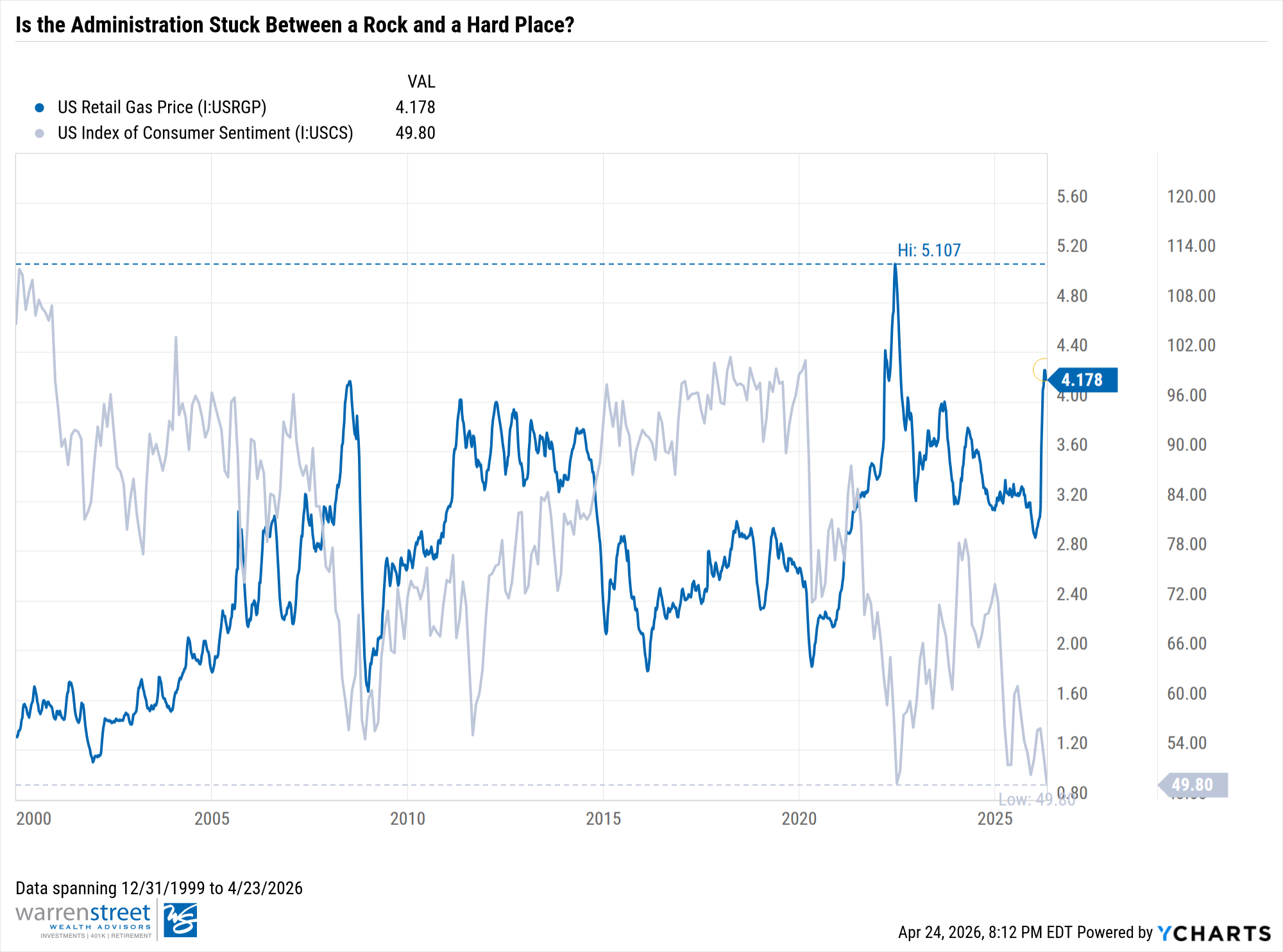

At first glance, it would seem that markets are celebrating the ceasefire. Instead, we believe they’re celebrating the constraints on both sides. Despite the current administration’s bravado on social media, the US is operating within real limits:

Gas prices are climbing into politically damaging territory.

We’ve burned through years of munitions stockpiles and missile interceptors — replenishing them adds to an already strained debt picture.

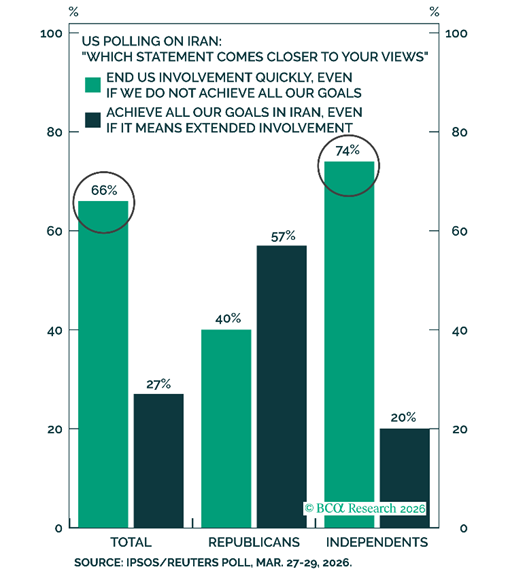

At the start of the war, only 53% of the public supported it, and support has only eroded from there. With the midterms approaching, this war is becoming a liability.

Iran’s position is also complicated:

Its arsenal is materially depleted, forcing more selective targeting.

Headline inflation is near 50%, causing social unrest that has spilled into the streets and warranted radical response.

Yes, the regime is exhibiting an unexpected tolerance for pain despite being under genuine strain. It has come to realize how powerful its leverage over the Strait of Hormuz is, but that leverage has a ceiling. If Iran pushes hard enough to tip the world into recession, the world could coalesce to force the Strait open.

At that point, nobody is negotiating with Tehran and will not care about its capitulation. Iran’s smarter play is subtler — agitate just enough to keep oil prices elevated, respect the ceasefire to the bare minimum, and let the pressure build on Trump’s midterm prospects.

Where Are We in the Playbook?

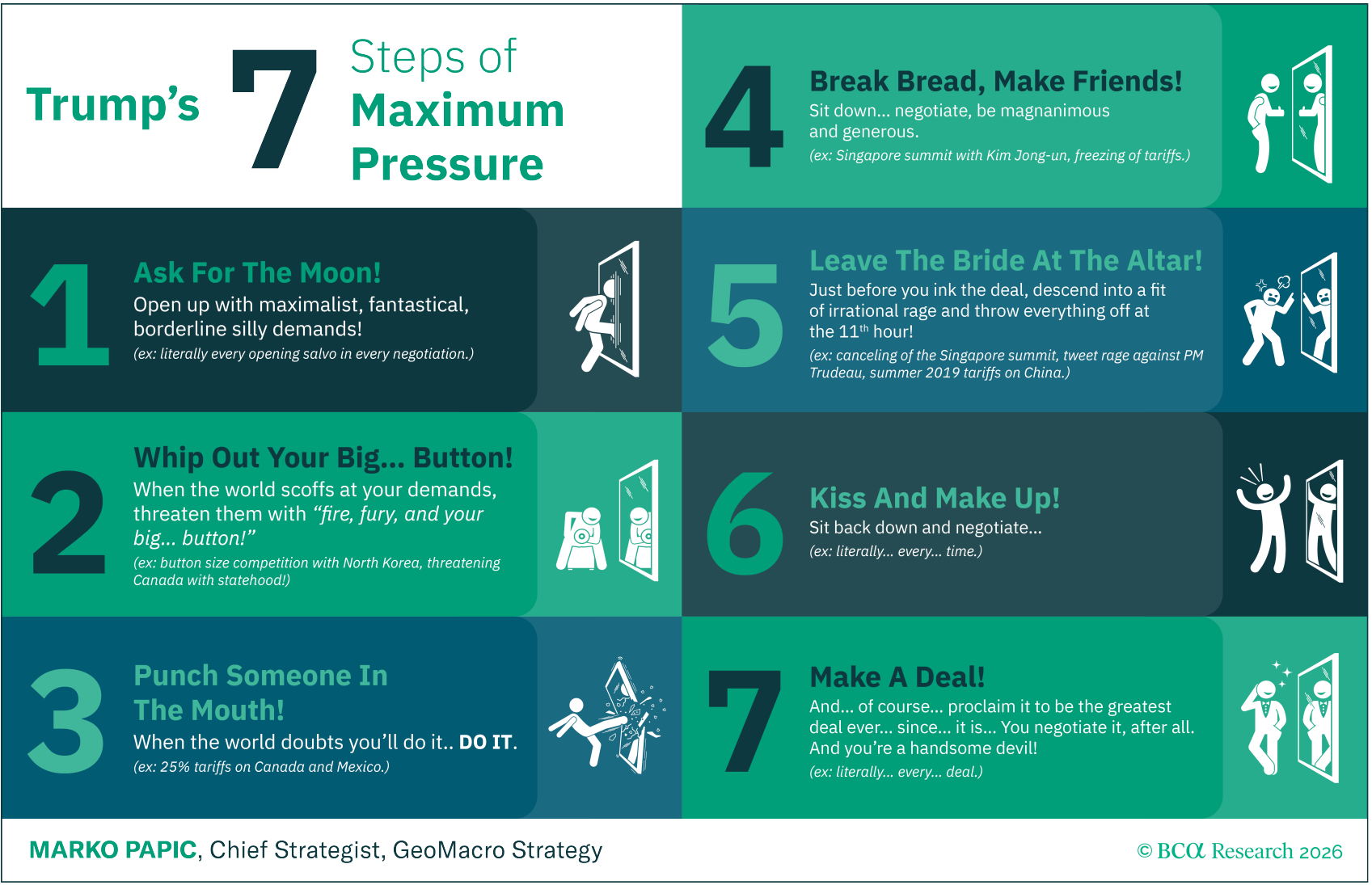

Some people might describe President Trump’s tactic using the TACO — Trump Always Chickens Out — acronym. Instead, BCA Research’s Marko Papic put together a seven-step framework for Trump’s maximum pressure negotiating style that we find more instructive.

Steps 1 through 3 — maximalist demands, threats, and following through — are in the rearview. We appear to be entering Step 4: fragile ceasefire, back-channel signals, and political jockeying from both sides to frame their position as a win. If the framework holds, we could be in for one more dramatic detour before a deal gets done.

A breakdown in negotiations or a miscalculation on either side could push oil prices meaningfully higher with downstream impacts on earnings and global growth. This is more of a tail-risk scenario, but Trump has left the altar before. The question is – will Iran still be there when he returns?

We imagine the likely base case resembles a uranium moratorium — perhaps similar to the Obama-era Joint Comprehensive Plan of Action, but sold very differently. Trump’s version will lean on the military degradation of Iranian capabilities. For Iran, the goal was always a shift in US policy posture. Both sides will aim to find a version of that story to tell their constituents.

Where We Stand

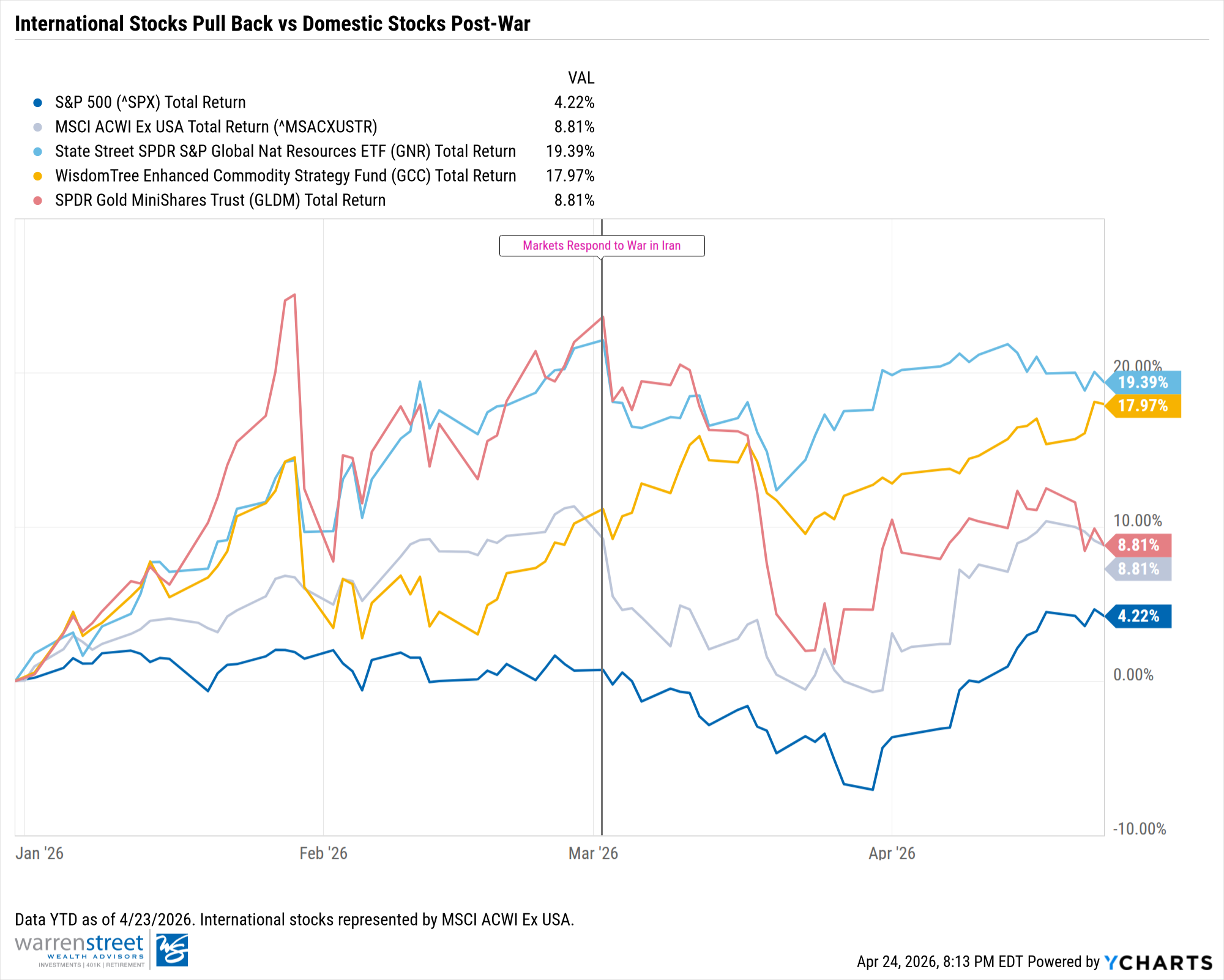

Before the conflict, our strategies had real momentum. Our tilt towards international equities was outperforming the US, and the Diversifiers strategy (i.e., gold, natural resources, commodities) boosted returns. Some of that outperformance has pulled back as international markets are more vulnerable to gulf energy. However, we believe that the bigger picture is unchanged.

Prior to the war, deglobalization was already underway, only to be accelerated by this conflict. Nations that spent decades outsourcing their energy and security needs are now building for self-sufficiency with more urgency. New trade arrangements, energy partnerships, and military alliances are forming in rooms the US is not in. The map is being redrawn, and we want exposure to that.

And What We Did

Our take? Rather than dramatic strategy shifts, we acknowledge the market’s ability to look past geopolitical noise and instead rebalanced firmwide back to target. This trimmed what held up — gold, commodities — and rotated into areas that sold off, including US equities. Should markets sell off further in a tail-risk event, we are actively watching for opportunities to tactically pivot strength into weakness.

To clients, the right posture might seem boring — and boring is probably correct. Sometimes, boring means hedging against the risks you can see, and diversifying against the ones you cannot.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Sources:

BCA Research

https://warrenstreetwealth.com/wp-content/uploads/2026/04/On-the-War-in-Iran-Do-Markets-Not-Care-and-Whats-Next.png10801080Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2026-04-24 16:48:312026-04-27 14:44:45On the War in Iran: Do Markets Not Care, and What’s Next?

Before we dive into the facts, we want to take a moment to recognize that before we are advisors or investment analysts, we are human. Our hearts go out to the families and individuals affected. We hold that reality close as we do our job of helping you navigate what it means for your financial future.

Part of that job is cutting through the noise, so let’s talk about what’s happening, what it means, and what we’re doing about it.

What’s Happening

The conflict entered its second week with crude oil briefly crossing $110 per barrel. Energy infrastructure in the region sustained damage, and the world turned its attention to the Strait of Hormuz — the narrow waterway through which roughly 20% of global oil supply flows — and whether it would remain open for business.

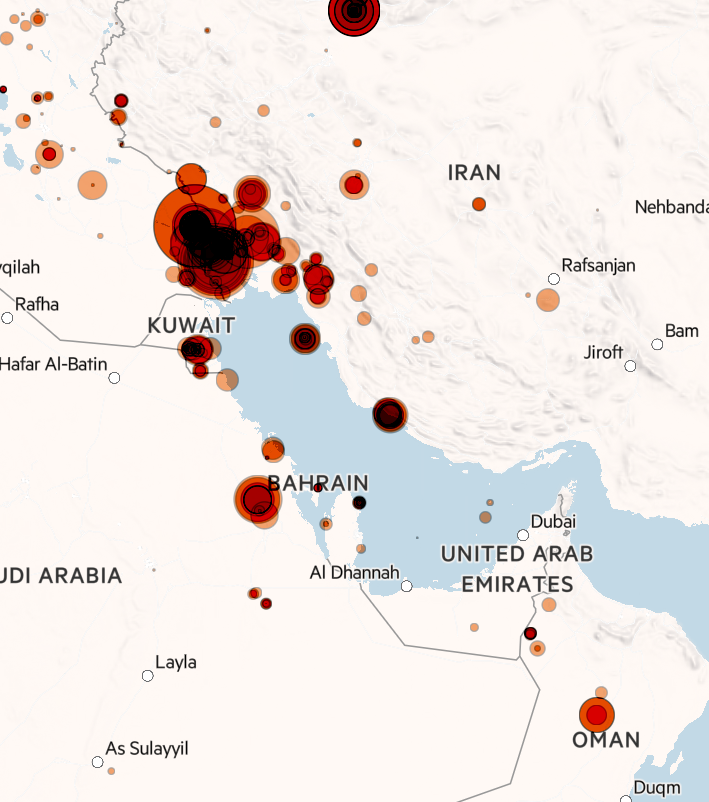

The View from fire-detecting satellites: Fire anomalies detected by infrared sensors on 7-8 March. Circles are sized by fire radiative power, darker circles mean several fires in close proximity

Sources: FT Analysis, Nasa Firms. Fires reported are either in locations with no history of regular burns or are unusually bright.

We don’t have a crystal ball for what will happen next, but there are three questions we’re watching closely:

Will there be more lasting damage to energy infrastructure?

What does the endgame look like in terms of leadership and capabilities on both sides?

Can a compromise be reached that keeps oil flowing through the gulf?

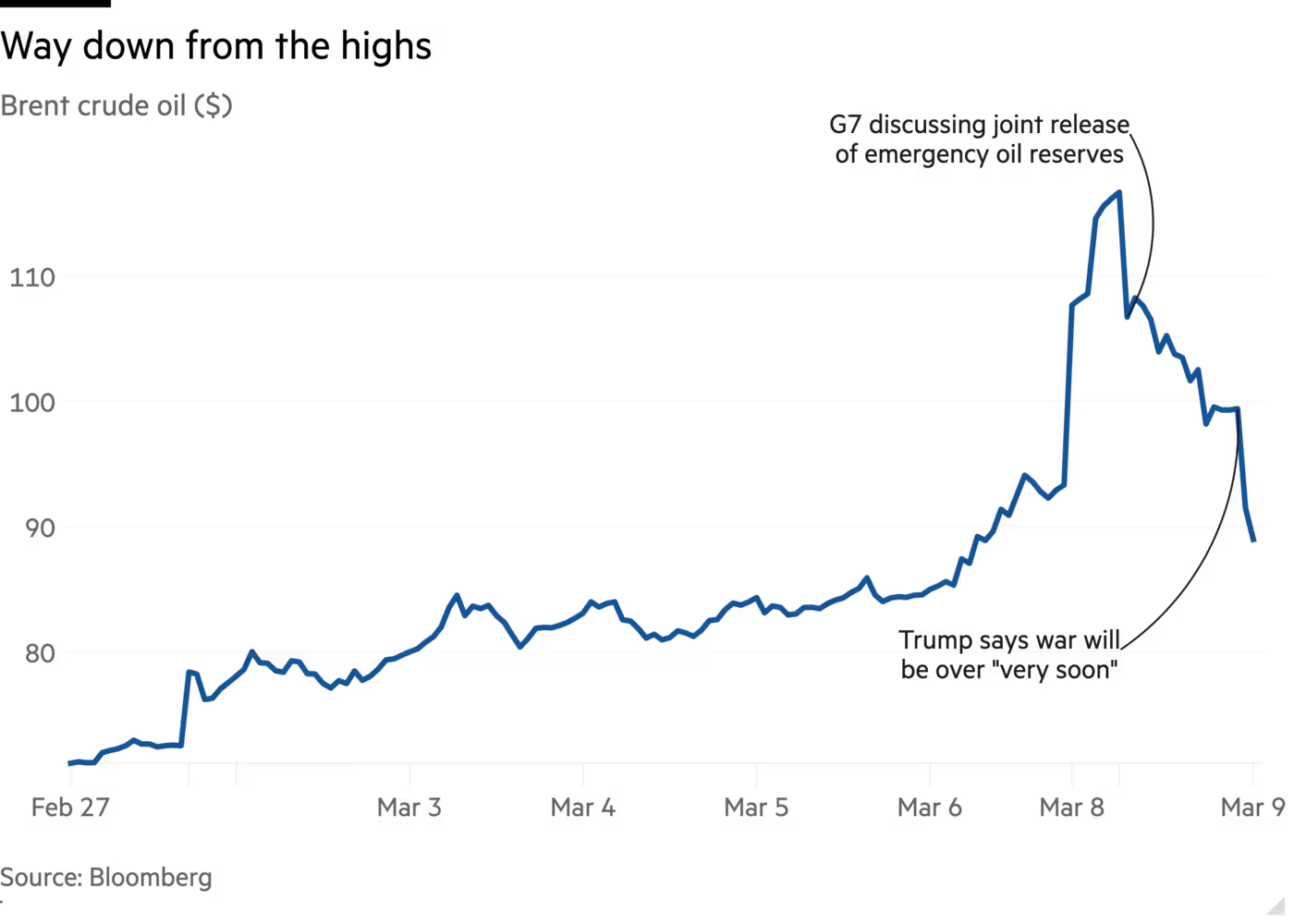

And Then Oil Dropped $20

Here’s the thing about geopolitical risk: it tends to be loud and unpredictable.

As I’m writing this, oil has pulled back from $110+ per barrel to below $90 — after President Donald Trump suggested the potential for a swift conclusion to the conflict. Meanwhile, the Strait of Hormuz is seeing vessel traffic increase, recovering from post-attack lows with inbound and outbound ship movements gradually rising.

While it’s too soon to declare a resolution, the swift oil price drop following comments from President Trump shows the market was pricing in a major supply shock that hasn’t materialized. This underscores why we avoid trading headlines, which often lead to emotional decisions mistaken for analysis. Our consistent advice for geopolitical headlines remains: stay diversified, stay disciplined, and trust your portfolio strategy.

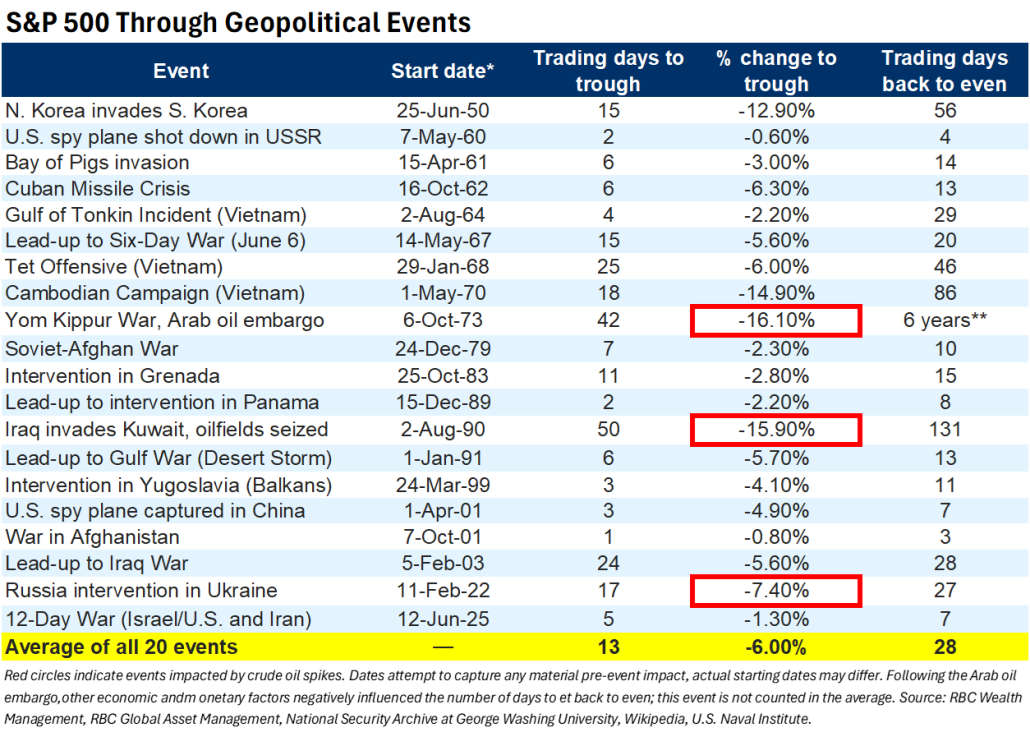

History Has Seen This Before

Here’s something worth sitting with. Looking at the past 20 major military conflicts and their impact on the S&P 500 over the last 75 years, the average decline from the initial shock to the market bottom was around 6%, and in 19 out of 20 cases, markets returned to pre-event levels in an average of just 28 days.

The two biggest exceptions — the 1973 Yom Kippur War and Iraq’s 1990 invasion of Kuwait — both involved sustained oil supply disruptions that pushed stocks down 15–16%. The 1973 episode scarred a generation of investors who sold out of equities and missed the enormous bull run of the 1980s.

The lesson isn’t that conflicts don’t matter. It’s that panicking out of a well-structured portfolio tends to hurt more than the conflict itself does.

This Isn’t 1973

Clients who lived through the Yom Kippur War might flinch from the prospect of re-living around-the-block gas lines, federally imposed speed reductions, or darkened cities to conserve energy. We understand the instinct, but there are major differences today.

In 1973, the U.S. was heavily dependent on imported oil. Every extra dollar at the pump was more money in the pockets of Middle Eastern countries. Today, the U.S. is a net energy exporter. Higher oil prices are painful for consumers, yes — but every extra dollar is more cash in the pockets of domestic energy producers. It’s a redistribution within the economy, not a pure drain out of it.

As for inflation, Energy makes up only about 6% of today’s U.S. inflation basket. There also headwinds blowing against the case for a 1970’s stagflation landscape, including:

Shelter Lags: Shelter costs (33% of the basket) are declining as lagging rent data catches up to reality, which will apply downward pressure on inflation prints.

Technological Progress: AI and technology-driven productivity is quietly acting as a deflationary force as consumers and businesses increase adoption.

Calming Tariff Tantrums: After the recent IEEPA tariff ruling, the effective tariff rate has also come down meaningfully to 9.1%.

Fundamental economic strength: We acknowledge the recent jobs report’s weakness, but also recognize other areas in the economy remain healthy. Corporate profits are expected to grow at high single to double digits in 2026. Tax refunds from last year’s One Big Beautiful Bill (OBBB) haven’t fully hit consumer accounts yet.

The Fed will likely pause at upcoming meetings, but that’s very different from the kind of policy circumstances that defined the stagflation era.

Weeks, Not Months?

Both sides have strong incentives to reach a compromise quickly. Iran can’t export oil under prolonged conditions and is subject to existential economic pressure. In the U.S., $4+ gas heading into a midterm summer is its own political tax. December oil futures were already trading in the low $70s before today’s pullback, suggesting the market never fully bought the doomsday scenario. Inflation breakeven rates have stayed surprisingly calm throughout.

Even after hostilities quiet down, there’s likely a period of elevated shipping costs and more cautious tanker behavior through the region. Think of it as a persistent risk premium rather than a single clean resolution — but a manageable one, not an economy-altering one.

What We’re Doing

We’re not making dramatic moves based on headlines and that’s by design. We are however, sticking to our operating procedure of:

Rebalancing – different parts of our clients’ portfolios have generally weathered the volatility well, but some may have drifted off target. Rebalancing is a disciplined move back toward those levels, not a market call, but a long-term wealth strategy of selling strength and buying weakness.

We built the “Diversifiers” strategy in client’s retirement portfolios for moments like this. It’s doing its job and reminding us that traditional stock-bond portfolios don’t always move in opposite directions when inflation is in the picture.

If markets sell off further in an extreme scenario, we have the flexibility to tilt asset classes within our portfolios.

We’ll continue monitoring the conflict while staying with our standard operating procedure, but what we won’t do is trade headlines. The oil price chart of the last two weeks makes that case better than we ever could.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2026/03/image-3.png802709Warren Street Teamhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgWarren Street Team2026-03-10 04:03:002026-03-10 10:00:34Oil, Conflict, and Your Portfolio: What We’re Watching

“Is AI a bubble?” my uncle asked as I put my fork down mid-bite on New Year’s Eve. I’d wager that this question dominated dinner tables and family gatherings across the country this holiday season. Even my sister, whose focus lies entirely within the arts and creative pursuits, managed to put the two words “AI” and “Bubble” together.

This tells me two things: 1) Concern around AI and “bubble-ness” is virtually inescapable and 2) this question is dominating the audience’s perception of markets, perhaps even more so than the meteoric rise of silver and gold as we enter 2026.

Why Does AI Deserve So Much Attention?

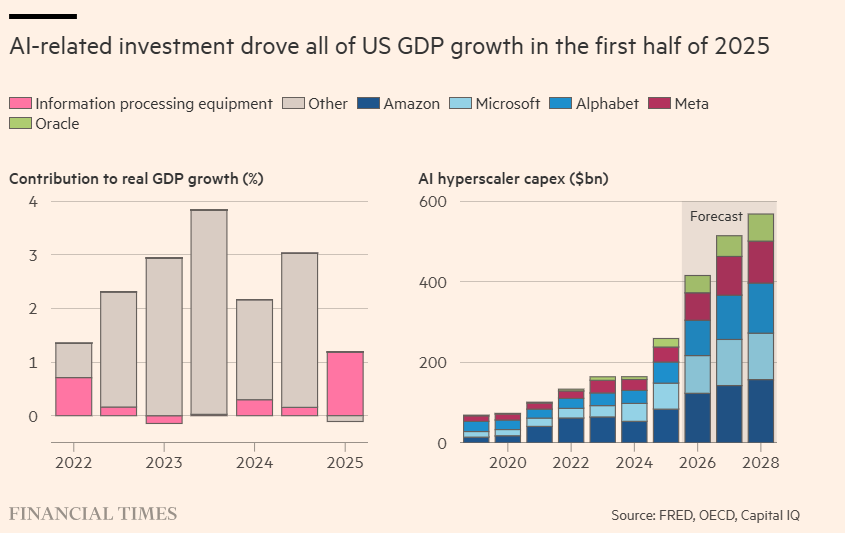

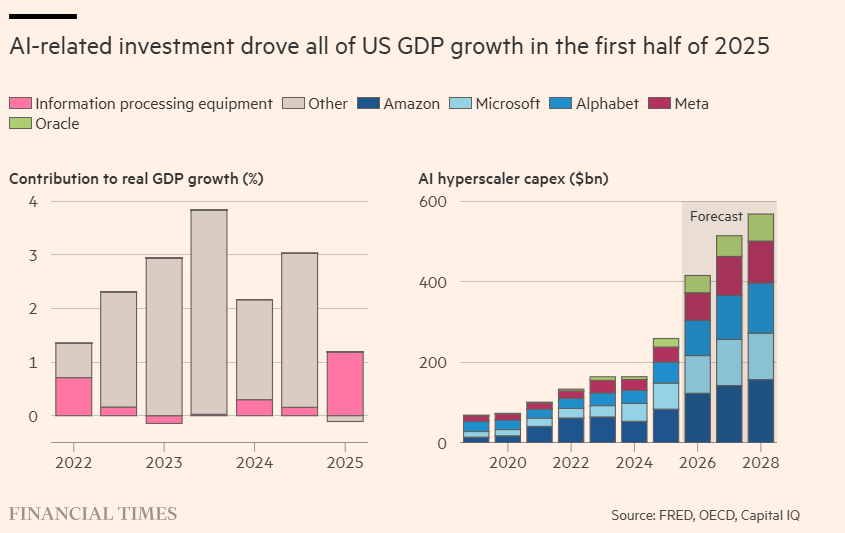

In 2025, AI-related names drove ~60% of the increase in the S&P 500’s value. Furthermore, AI spending from the “Hyperscalers” (Google, Microsoft, etc.) accounted for the lion’s share of our economy’s growth. Without the spending on data center infrastructure—servers, GPUs, and the centers themselves—some estimates suggest US GDP would have grown at a measly 0.1% in the first half of 2025. It’s safe to say that AI alone kept the economy afloat for most of last year.

The robust figures above underscore why AI rightfully commands significant attention. However, fixating on the bubble label can be a trap, much like timing the market. Instead, we should look at bubble psychology and how those excesses may be extending into the AI ecosystem.

Settling the AI Bubble Talk

It’s been over 20 years since we’ve seen such a transformative, general-purpose technology with the potential to deliver productivity gains eclipsing the internet era. This fervor has already minted a class of early winners, leaving everyone else watching with a potent mix of envy and regret. It’s the classic setup for FOMO, where the “AI train” starts looking less like a sound, technological investment and more like a high-speed shortcut to a cushy nest egg.

The danger is that the faster this train moves, the easier it is to speed right past the following flags:

Starting Valuations: We pay prices regardless of whether reasonable returns can be generated.

Risk/Reward Profiles: We stop asking if we’re actually being compensated for the layers of risk we’re adding to our broader portfolio.

Lofty Narratives: AI’s newness unrestrains the imagination to justify price tags that reality can’t yet support.

Behind the Excitement: What’s Different This Time?

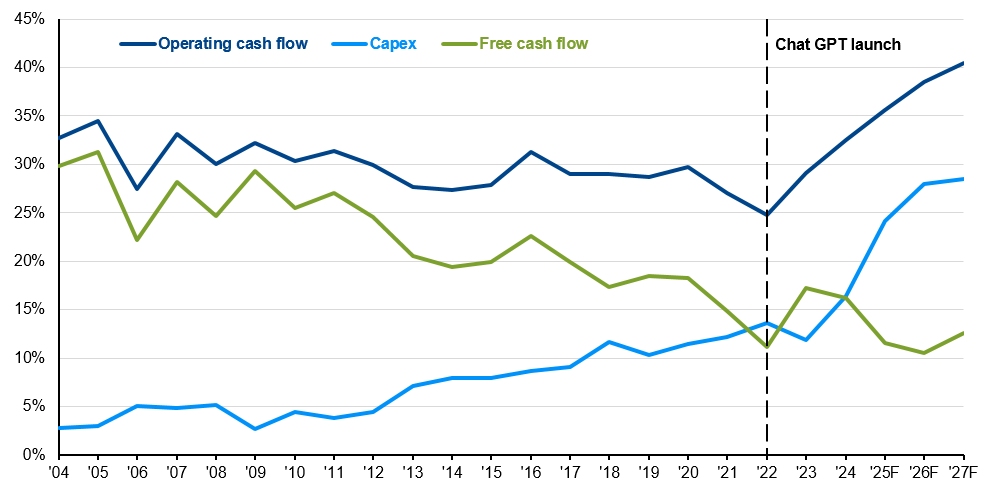

A Stronger Starting Line-Up Unlike the fragile startups of the dotcom era, today’s main AI spenders are profitable, cash-printing businesses. They are self-funding a massive AI arms race with capital expenditures set to leap by 60%, from $250bn in 2025 to over $400bn in 2026. Operating cash flows continue to outspace AI spend as a percentage of sales, allowing this historic investment to feel like a strategic augmentation of their core businesses rather than a reckless gamble.

Justified Valuations While Forward P/E ratios look expensive, today’s multiples are anchored by real-world profit. Take Nvidia: its stock price increased 14x over the last five years, but earnings grew 20x. Today’s titans aren’t as frothy as the dotcom class of 2000 because they are delivering healthy bottom-line results. However, this optimism hinges on perfection. While bulls argue we are buying “cheaper” growth today than at any point in the decade, that narrative leaves a near zero margin for error if adoption slows.

Infrastructure Demand In contrast to the fiber-optic mania of the 90s, the demand for AI build-outs can’t seem to catch a break. Data center vacancy rates are at a record low of 1.6%, and ~75% of pre-construction builds are already pre-leased. Additionally, past infrastructure bubbles saw spending peak between 2% and 5% of GDP, whereas today’s AI investment sits at roughly 1%. This suggests the build-out still has room to run.

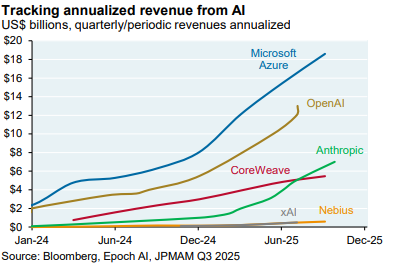

Show Me the Money Revenues are skyrocketing. Alphabet’s Q3 2025 results proved that AI-driven features are accelerating search and ads, with generative AI product revenue surging into the triple-digit percentage range year-over-year. Beyond the titans, some industry participants have grown revenues nearly ninefold since ChatGPT launched. For now, the receipts are keeping the optimism alive.

AI Is Running Fast… But Will it Trip a Wire?

We are in a high-stakes arms race on both a micro level (hyperscalers) and a macro level (US vs. China). Businesses are pouring trillions into this effort to secure US leadership in a technology that will change the fabric of society. But in this race to the top, it’s easy to overlook the blind spots.

Revenues & Profits: Can We Reach the Promised Land? Despite the growth, there is a staggering gap between spending and earning. Analyst Azeem Azhar points out that AI companies are projected to generate $60bn in revenue against $400bn in spending for 2025. That’s a 6-7x gap—far wider than the dotcom bubble (4x) or the railroad boom (2x). Even if revenue catches up, will it translate to profit, or will we see a “race to the bottom” where large language models (LLMs) become commoditized?

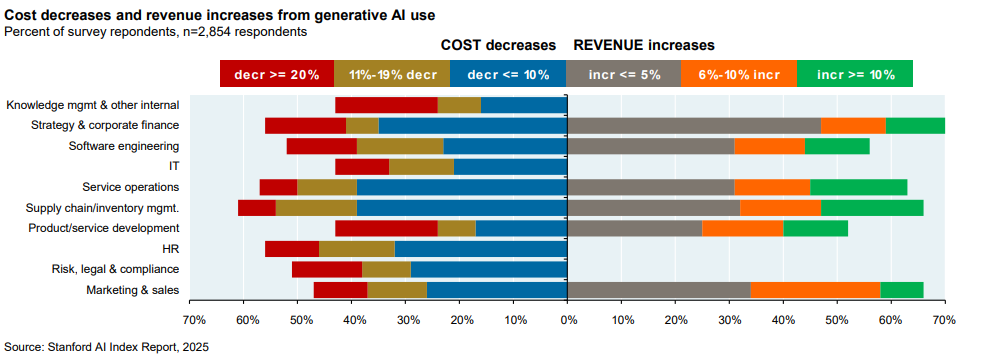

Is Demand Real? Adoption is still in its awkward early stages. Only roughly 10% of firms are using AI to produce goods, though 45% pay for LLM subscriptions. According to the Stanford AI Index and McKinsey, the majority of firms are seeing only modest cost savings (≤10%) and negligible revenue gains (≤5%). Will AI adoption ever truly scale into broad, durable profit expansion?

How Long is Your (Useful) Life? Hyperscalers like Microsoft and Google have boosted profits by extending the “useful life” of their AI assets in their books. If innovation renders chips obsolete in 24 months, these companies will face massive write-downs. More importantly, they are funding this short-lived hardware with 30-year debt, leaving investors holding the bag for “obsolete” infrastructure that won’t be paid off for decades.

The AI Ouroboros There is an increasingly circular dance where Microsoft invests in OpenAI and then books cloud revenue from them. Nvidia buys stakes in the startups they sell chips to. This means a chunk of today’s “booming” revenue is an internal recycling of capital where true economic profit from external customers remains hypothetical.

Cloudy with a Chance of IOUs: While the biggest players usually use cash, we’re seeing a pivot toward the bond market. Oracle and Meta have emerged as outliers, using long-term bonds and project finance to bankroll their data centers. As free cash flow wilts under the weight of AI spend, their stock prices are feeling the gravity. Furthermore, the industry is using Special Purpose Vehicles (SPVs) to hide this leverage off-balance sheet, adding a layer of obscurity to the trillions being spent.

Conclusion: A Massive Collection of What-Ifs

Ultimately, the AI story comes down to “what-ifs.” What if AGI finally shows up and productivity explodes? Or, what if demand never materializes and the hyperscalers finally blink? With cracks showing—like OpenAI’s recent “Code Red”—it’s impossible to say if we’re headed for a minor correction or a systemic burst.

Our 2026 Recommendations:

Keep a seat at the table: Exposure to market-cap weighted indices allows you to benefit if the “promised land” materializes.

Diversify your sources of risk: Anchor beyond US tech. Gold, international markets, and bonds offer a necessary buffer if signs of excess turn into a choppy ride.

Rebalance systematically: Rebalancing is a controllable hedge. When sector weights become excessive, returning to target allocations helps lock in gains and reduce concentration risk.

Phillip Law, CFA

Senior Portfolio Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

With 2025 in the rear view mirror, we look towards the new year. What lessons did we learn and what trends deserve attention? How do we allocate portfolios based on that knowledge? In this piece, we’d like to share three areas of focus heading into 2026:

Artificial Intelligence and Bubbleness

The State of the US Economy

The Biggest Risks to Asset Markets (Namely Inflation)

2025 Recap: Laughing in the Face of Di-worsification:

After years of US led-dominance, we saw narratives across asset classes flip on their heads. For the first time in years:

US Stocks underperformed developed international and emerging market geographies.

Gold, held for its diversification benefits, shined more brightly than most major asset categories.

Source: YCharts

The year reminded us that “di-worsification” – a term long used to parody the idea that diversifying into less correlated, non-US assets only made portfolios worse – isn’t a universal truth. In 2025, holding different asset segments helped weather volatile trade policy, weakening dollar, and US deficit concerns.

Ultimately, we left 2025 with a more fragmented globe where nations now emphasize national security and independence over globalized efficiencies. In this new regime where the global economy is de-synchronized, we believe diversification is more essential than ever.

Looking to 2026: What of AI and Its Bubbleness?

The topic of artificial intelligence being a bubble is almost inescapable. AI Hyperscalers, bolstered by massive spending commitments on AI investments, drove over 60% of the S&P 500’s growth and was a key lifeline for the economy in 2025. With AI hyperscalers and key players constituting a significant portion of the S&P 500, the ecosystem will likely continue to define US markets in 2026. So is it a bubble?

We have a separate piece that deep dives into the AI Bubble question which I’ve summarized below:

The Bull Case:

Proponents argue that this time is different compared to other speculative manias. The players here are profitable, cash-printing businesses whose valuations are not only reasonable, but also are pricing in achievable growth. Furthermore, there is ample demand for infrastructure, particularly data centers, unlike the railroad and dotcom bubbles. This all will enable revenue to follow, which has already exhibited enormous growth rates.

The Bear Case:

Despite tremendous growth, AI companies are spending way more than they’re making, (higher than past bubbles). Demand from businesses remains uncertain, with early studies showing only modest cost savings/revenue gains. Also, most revenue booked today is a result of circular investing amongst AI players. Meanwhile, AI companies are using aggressive accounting methods for their chips, which puts future earnings estimates at risk. Lastly, debt is now being used to finance spending, officially adding a shot clock for return on investment to materialize.

What to Do?

Within the deep-dive, we reach two conclusions:

1. Focusing on the “bubble” label is often unproductive. Even if excesses exist, timing the eventual “burst” is a fool’s errand—will it be in one year or five? Selling too early means potentially missing out on healthy gains.

As Peter Lynch noted, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

2. The AI dilemma is ultimately a huge collection of what-ifs, but we believe keeping a seat at the table while diversifying sources of risk and return in other parts of the portfolio such as international stocks, bonds, or gold is prudent.

How’s the US Economy?

Objectively speaking, the economy is in a healthy state heading into 2026. Let’s look at a few primary indicators:

A Productive Economy – GDP grew at an astonishing annualized rate of 4.3% in Q3 2025 and is projected to grow ~2% (long-term average) in 2026. We expect AI spending to continue as hyperscalers add to productivity and other businesses increase adoption.

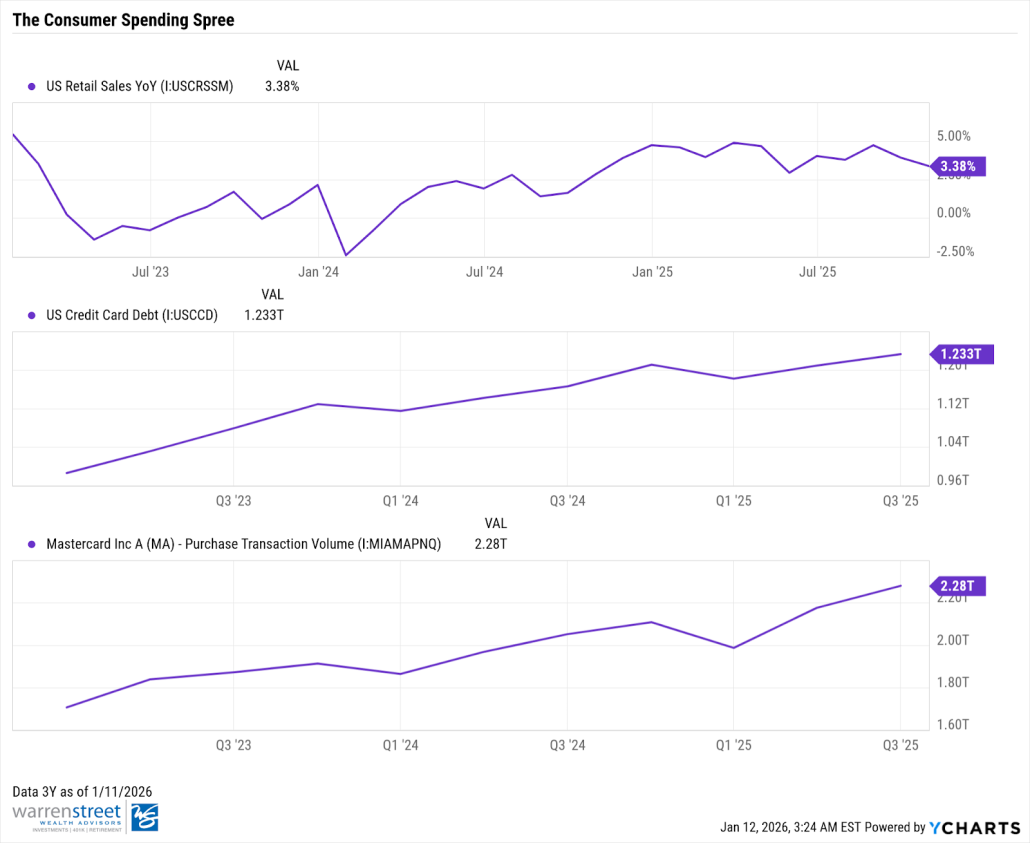

The Spending Surprise – Despite rising concerns around job security and waning sentiment, Americans are still spending. In late 2025, retail sales surged 3.5% year-over-year and we observed a healthy uptick in credit card balances.

Fiscal & Monetary Stimulus:

Heading into 2026, we’ve unlocked tax credits from the One Big Beautiful Bill (OBBB). We take estimates with a grain of salt, but if $100bn in total tax refunds and a $3,750 average tax cut per filer could further stimulate consumer spending.

The market currently anticipates two rate cuts, which will lower the cost of borrowing for both businesses and consumers (maybe more, pending Federal Reserve politics).

With a solid launching pad to start the year followed by additional liquidity in consumers pockets, we believe the US economy is well-equipped heading into 2026.

What About the Risks?

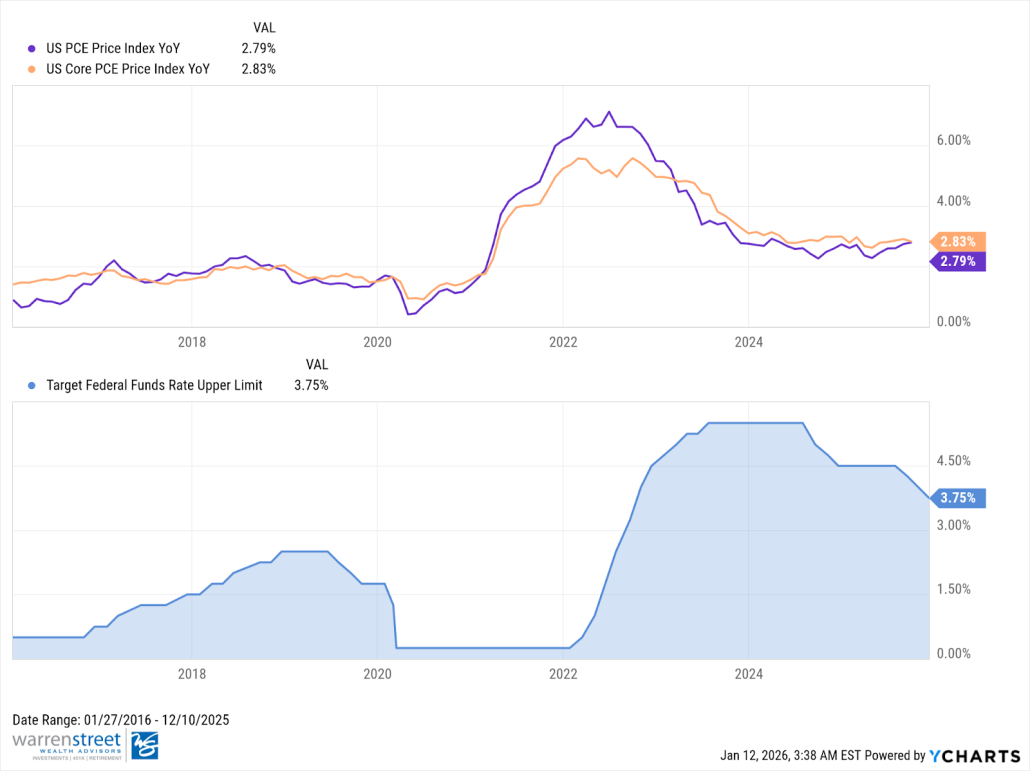

We believe the primary, non-wildcard risk to asset markets is inflation. Although inflation has stabilized from recent years, it remains sticky compared to pre-pandemic levels (around 2%), with the Fed’s preferred measure recently estimated at 2.8%.

The current economic backdrop does allow more sensitivities to a spike in inflation.

Trade fragmentation and tariffs – while most businesses seemingly absorbed the price increases of tariffs in 2025, we’ve begun to see some price hikes passed to consumers in recent inflation prints.

Is Stimulus a Double-Edged Sword? – While increased liquidity for consumers can be helpful, it may also fuel inflation. The prior stimulus checks led to double-digit drops in equities and bonds (2022) as we raised rates to fight policy-driven inflation.

Financial Repression – With US Debt-to-GDP approaching 120%, there is a risk that policymakers resort to “financial repression” – intentionally allowing higher inflation to “inflate away” the real value of government debt.

With US equities trading expensively and bonds vulnerable to inflation, I’d park this risk in the low probability, but high impact camp. To mitigate this risk, owning a portion of your portfolio to hedges (gold, commodities, natural resources) can cushion against a potential 2022 repeat.

Conclusion:

Ultimately, the backdrop seems favorable for US equity markets heading into 2026. Even if markets are frothy, the solution to managing potential excesses and drawdowns is not in timing them, but instead: a) building adequately diversified portfolios b) aligning allocations with your risk tolerance and financial objective and c) rebalancing into weakness to harness the long-term growth of capital markets at more advantageous price levels.

That’s our 2026 outlook. Our advice remains: use these investing principles as your foundation. This will allow 2026 to be less about watching tickers and more about the life you’re building. Hit that PR, read those books, or learn to cook—aim to achieve your best self. While we can recommend investments and share outlooks, there’s no substitute for investing in your own growth and happiness.

Phillip Law, CFA

Senior Portfolio Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

We’re thrilled to announce a major milestone for our firm and our clients: the launch of the Warren Street Global Equity ETF (NASDAQ: WSGE)!

This new Exchange-Traded Fund (ETF) is now available, bringing our disciplined investment philosophy to the public in a convenient, accessible format. This is an exciting step forward as we continue to provide sophisticated investment solutions while delivering on our fiduciary commitment.

The Warren Street Wealth Advisors team celebrates the launch with a visit to the NASDAQ MarketSite in Times Square, New York.

What is WSGE and Why Did We Create It?

The Warren Street Global Equity ETF (WSGE) is designed to be a smarter way to invest in the global stock market. The traditional choice has always been either a simple, broad index fund or a complicated, expensive actively managed fund. We created WSGE to give you the best of both worlds: global diversification with a smart strategy built to enhance returns.

Focus on You: The Key Client Benefits

While the investment strategy is robust, the most important reason we created WSGE is to provide direct, tangible benefits to you, our clients, and to uphold our fiduciary standard:

Embedded Tax Efficiencies: As an ETF, WSGE is structured to minimize capital gains distributions compared to traditional mutual funds. This powerful tax efficiency helps you keep more of your investment returns, making your portfolio work harder over the long term.

Economies of Scale: By bundling diverse global exposures and our proprietary strategy into a single vehicle, we achieve significant economies of scale. This approach reduces complexity and overall costs, effectively providing you with institutional-quality management at a lower expense.

Uniformity Across Clients: WSGE ensures every client benefits from the exact same research-driven exposure and proprietary factor tilts. This uniformity across clients leads to greater consistency, streamlined execution, and clearer reporting, regardless of account size.

Time Savings & Simplicity: The single-fund structure drastically simplifies trade execution, rebalancing, and overall portfolio maintenance. This provides time savings for both our advisory team and you, the client, allowing us to focus more on your comprehensive financial plan, retirement goals, and tax strategies.

Learn More

When you invest in WSGE, you’re accessing the same level of rigorous due diligence that defines Warren Street Wealth Advisors. We meticulously select the fund’s underlying investments, focusing on quality management, low cost, and alignment with our goals.

We are proud to bring this innovative solution to market and look forward to partnering with you on your journey toward long-term capital appreciation.

To learn more about the fund, view the prospectus, and review important disclosures, please visit warrenstreetetf.com.

Phillip Law, CFA

Senior Portfolio Manager, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Important Information

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. This and other important information is contained in the prospectus, which may be obtained by following the links Prospectus and Summary Prospectus or by calling +1.714.876.6200. Please read the prospectus carefully before investing.

The Fund is actively-managed and is subject to the risk that the strategy may not produce the intended results. The Fund is new and has a limited operating history to evaluate.

Median 30 Day Spread: is a calculation of Fund’s median bid-ask spread, expressed as a percentage rounded to the nearest hundredth, computed by: identifying the Fund’s national best bid and national best offer as of the end of each 10 second interval during each trading day of the last 30 calendar days; dividing the difference between each such bid and offer by the midpoint of the national best bid and national best offer; and identifying the median of those values.

Basis Points (bps): A unit of measure used in quoting yields, changes in yields or differences between yields. One basis point is equal to 0.01%, or one one-hundredth of a percent of yield and 100 basis points equals 1%.

Equity Investing Risk. An investment in the Fund involves risks similar to those of investing in any fund holding equity securities, such as market fluctuations, changes in interest rates and perceived trends in stock prices. The values of equity securities could decline generally or could underperform other investments. In addition, securities may decline in value due to factors affecting a specific issuer, market or securities markets generally.

Fixed-Income Risk. The market value of fixed-income securities will change in response to interest rate changes and other factors, such as changes in the effective maturities and credit ratings of fixed-income investments. During periods of falling interest rates, the values of outstanding fixed-income securities and related financial instruments generally rise. Conversely, during periods of rising interest rates, the values of such securities and related financial instruments generally decline. Fixed-income investments are also subject to credit risk.

Large-Capitalization Companies Risk. Large-capitalization companies may trail the returns of the overall stock market. Large-capitalization stocks tend to go through cycles of doing better – or worse – than the stock market in general. These periods have, in the past, lasted for as long as several years.

Mid-Capitalization Companies Risk. Investing in securities of mid-capitalization companies involves greater risk than customarily is associated with investing in larger, more established companies. These companies’ securities may be more volatile and less liquid than those of more established companies. Often mid-capitalization companies and the industries in which they focus are still evolving and, as a result, they may be more sensitive to changing market conditions.

Depositary Receipt Risk. ADRs and GDRs are generally subject to the risks of investing directly in foreign securities and, in some cases, there may be less information available about the underlying issuers than would be the case with a direct investment in the foreign issuer. ADRs are U.S. dollar-denominated receipts representing shares of foreign-based corporations. GDRs are similar to ADRs but are shares of foreign-based corporations generally issued by international banks in one or more markets around the world.

Risk of Investing in Other ETFs. Because the Fund may invest in Underlying ETFs, the Fund’s investment performance is impacted by the investment performance of the selected Underlying ETFs. An investment in the Fund is subject to the risks associated with the Underlying ETFs that then-currently comprise the Fund’s portfolio. At times, certain of the segments of the market represented by the Fund’s Underlying ETFs may be out of favor and underperform other segments.

Focus Investing Risk. The Fund seeks to hold the stocks of approximately 40 companies. As a result, the Fund invests a high percentage of its assets in a small number of companies, which may add to Fund volatility.

Foreign Investment Risk. Returns on investments in foreign securities could be more volatile than, or trail the returns on U.S. securities. Investments in or exposures to foreign securities are subject to special risks, including differences in information available about issuers of securities and investor protection standards. In addition, foreign securities denominated in other currencies could decline due to changes in local currency.

Factor-Based Investing Risk. There can be no assurance that the factor-based investment selection process employed by the Sub-Adviser will enhance the Fund’s performance. Exposure to the different investment cycles identified by the Sub-Adviser may detract from the Fund’s performance in some market environments.

ETFs may trade at a premium or discount to their net asset value. ETF shares may only be redeemed at NAV by authorized participants in large creation units. There can be no guarantee that an active trading market for shares will exist. The trading of shares may incur brokerage.

This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. We make no representation or warranty as to the accuracy or completeness of the information contained herein including third-party data sources. The views expressed are as of the publication date and subject to change at any time. No part of this material may be reproduced in any form, or referred to in any other publication without express written permission. References to other funds should not to be interpreted as an offer or recommendation of these securities.

An investment in the Fund involves risk, including possible loss of principal. Exchange-traded funds (ETFs) trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value (NAV), and are not individually redeemable directly with the ETF. Brokerage commissions and ETF expenses will reduce returns. ETFs are subject to specific risks, depending on the nature of the underlying strategy of the Fund, which should be considered carefully when making investment decisions. For a complete description of the Fund’s principal investment risks, please refer to the prospectus.

Shares of the Funds Are Not FDIC Insured, May Lose Value, and Have No Bank Guarantee.

The Fund is distributed by PINE Distributors LLC. The Fund’s investment adviser is Empowered Funds, LLC, which is doing business as ETF Architect. Warren Street Wealth Advisors, LLC serve as the Sub-advisers to the Fund. PINE Distributors LLC is not affiliated with ETF Architect or Warren Street Wealth Advisors, LLC. Learn more about PINE Distributors LLC at FINRA’s BrokerCheck.

ETFAC-4941235-10/25

https://warrenstreetwealth.com/wp-content/uploads/2025/11/image.jpeg13652048Phillip Law, CFAhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgPhillip Law, CFA2025-12-12 08:00:002025-12-12 08:44:36Introducing Warren Street Global Equity ETF (WSGE) – An Informed Approach to Diversification

Choosing a health care plan at work can be a bit of a headache—charts comparing premiums, copays and deductibles isn’t exactly light reading. One option you might have encountered in this process is the high-deductible health plan (HDHP). The name might sound intimidating. After all, who really wants to pay high deductibles? But when paired with a health savings account (HSA), an HDHP can be a powerful tool to help you save for your health care now and your future.

What is an HDHP?

An HDHP is a type of health insurance plan that comes with lower monthly premiums but higher out-of-pocket costs. In other words, you’ll pay less each month, but you’ll be on the hook for more when you actually visit a doctor. These plans shift more financial risk to you in exchange for upfront savings—and they often come with access to an HSA.

An HSA allows you to set aside pre-tax money to pay for qualified medical expenses like doctor visits, prescriptions, dental care and vision services. Unlike a flexible spending account (FSA), which is “use it or lose it,” the money in an HSA is yours to keep. It rolls over from year to year, stays with you if you change jobs and often has investment options.

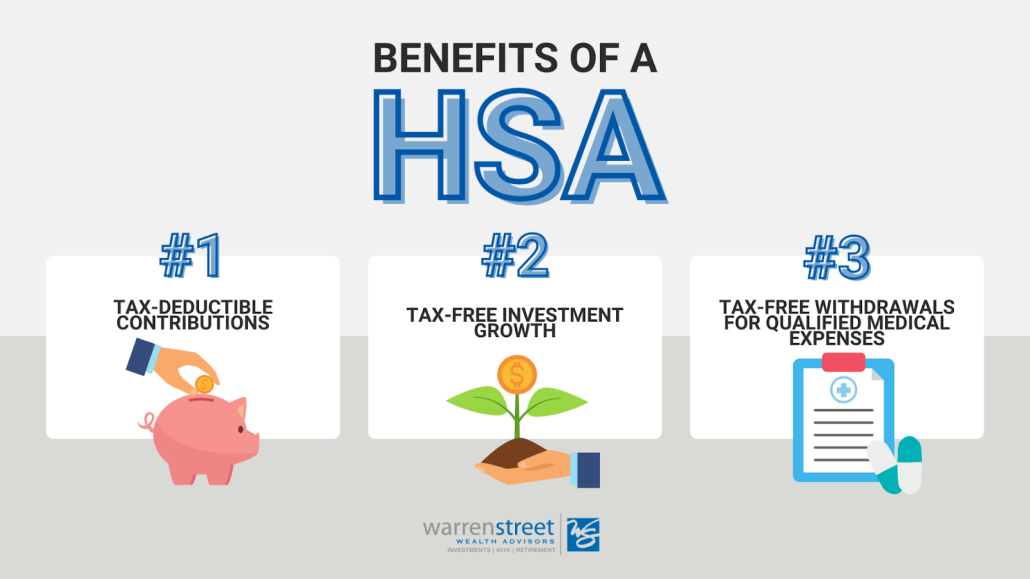

What makes HSAs especially appealing are their triple tax benefits:

Tax-deductible contributions.

Tax-free growth on investments inside the HSA.

Tax-free withdrawals at any time if the money is used for qualified medical expenses.

These features make HSAs one of the most tax-efficient savings vehicles available. But there’s another way to get more from your HSA: It can serve as a powerful retirement savings vehicle.

Should You Use a High-Deductible Health Plan?

Before we get to the benefits of an HSA as an investment vehicle, how do you decide whether to use an HDHP in the first place? Choosing between a traditional plan and an HDHP depends on a few key factors.

First, compare the total potential cost under each plan. That means looking at monthly premiums, deductibles, coinsurance and out-of-pocket maximums. HDHPs typically offer significantly lower monthly premiums but come with higher deductibles. If you’re generally healthy and don’t expect to need much medical care, this tradeoff could work in your favor.

But be honest with yourself about your cash flow. If you had a sudden medical emergency, would you be able to cover the high out-of-pocket costs until your insurance kicks in? For people with chronic health conditions or frequent doctor visits, a traditional plan might offer more predictable costs.

Using an HSA as a Retirement Account

Once you’ve maxed out your traditional retirement accounts, an HSA becomes an excellent next stop. HSA contribution limits are $4,300 for self-only coverage and $8,550 for family coverage in 2025. You can leave that money in cash or invest it. You can, of course, use it to pay for qualified out-of-pocket medical expenses at any time. But you can also leave it in the account untouched, letting it grow and enjoy the power of tax-advantaged compounding—just as you would with an IRA or 401(k).

Health care is one of the biggest expenses in retirement. So building a tax-free fund dedicated to future medical needs makes a lot of sense. According to recent estimates, a 65-year-old retiring in 2024 can expect to spend around $165,000 on health care in retirement—and that number is only expected to rise.

Here’s the kicker: When you turn 65, you aren’t limited to using your HSA for medical expenses. You can make withdrawals for non-medical expenses, and these will simply be taxed as income, just like withdrawals from a traditional IRA or 401(k). In short, your HSA can function like a traditional retirement account with the added perk of tax-free withdrawals for medical expenses at any age.

Your HSA as Part of Your Investment Strategy

Your HSA is a financial asset, whether it’s sitting in cash or invested in the market. As such, it can play an important role in your strategies for long-term asset allocation, diversification and rebalancing. Managed well, it can contribute meaningfully to your future financial security.

You can manage your HSA investments on your own. Or, depending on your HSA provider, we may be able to manage the assets within the account on your behalf. Even if direct management isn’t possible, we’re here to help you evaluate your options, choose appropriate investments and determine how best to incorporate your HSA into your long-term plan.

If you’re not sure whether an HDHP and HSA are right for you, let’s talk. Together, we can evaluate your health needs, cash flow and retirement goals to determine the best path forward.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2025/10/HSA-Benefits.png10801080Bryan Cassick, MBA, CFP®https://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgBryan Cassick, MBA, CFP®2025-10-10 10:30:532025-10-10 10:31:01Should I Be Using a Health Savings Account?

As we approach the end of 2024, it’s an opportune time to reflect on the year’s financial developments and consider what 2025 may bring. We believe in understanding both the past and potential future of our economic landscape, which may help inform financial decisions.

This year has brought its share of financial developments, from market fluctuations to policy changes that have shaped the economic environment. Shifts in various sectors, interest rate movements, and global events have influenced financial strategies across the board.

Looking ahead to 2025, we anticipate new opportunities and challenges in the financial world. Our team watches current trends and indicators to provide some insights for the coming year.

In this review, we’ll examine the key financial events of 2024 and their impact and potential implications. We’ll then turn our attention to 2025, offering our perspective on trends that may emerge in the coming months.

Whether you’re a long-standing client or simply interested in staying informed, we believe this overview may provide some insights for your financial strategies as we move into the new year.

Key Economic Factors in 2024

Interest Rates

During the September meeting, the Federal Reserve voted to lower interest rates by 0.5 percent, the first reduction in rates since 2020. While the pivot was long-anticipated, the size of the cut surprised many pundits following the Fed’s all-out fight against inflation launched two years ago. The move, unusual in an election year, brought the benchmark federal funds rate to a range between 4.75% and 5%. Some anticipate the Fed may adjust interest rates again in 2024.1

Inflation

The decision to trim interest rates moved the central bank into a new phase, and preventing further weakening of the U.S. labor market is now an important priority. For most of the past 2½ years, the Fed focused on fighting inflation. With the Consumer Price Index receding from 6.4% in January 2023 to 2.9% this July, the Fed pivoted attention to the softening job market. By comparison, the seasonally-adjusted unemployment rate rose to 4.2% in August, up from 3.7% in January.1

GDP Growth

Real GDP growth rose by 3.0% quarterly annualized in Q2 2024, up from 1.6% in Q1 2024. This increase was led by stronger domestic demand and a surge in inventories. The Conference Board Economic Forecast estimates a 0.8% annualized GDP growth for Q3 and 1% annualized for Q4. With the third and final Q3 GDP estimate due to be released on December 19, attention will shift to Q4 and 2025. Looking into 2025, some economists watch the Atlanta Fed’s GDPNow tool, which gives a running estimate of real GDP growth based on available economic data for the current measured quarter.2

Market Performance

Equity markets have seen strong, if uneven, performance in 2024. As of the end of October, the S&P 500 index was up 19.62% while the Dow Jones Industrial Average rose 10.81%. The tech-heavy NASDAQ increased 20.54%.3

Bonds have also shown volatility in 2024. As of October 31, the total return of the 10-Year Treasury Note was 4.28%.4

Past performance does not guarantee future results. Individuals cannot invest directly in an index. The return and principal value of financial markets will fluctuate as conditions change.

Key Takeaways

Up Markets Can Still Experience Volatility

While equity markets had strong overall performance in 2024, stocks did not go up in a straight line. There were some scary moments for investors, like April 12, when inflation and geopolitical worries saw the Dow Jones Industrial Average slide by 1.24%, the S&P 500 tumble by 1.46%, and the Nasdaq pull back by 1.62%. That bad day for the markets was dwarfed by August 5, when worries about slowing U.S. economic growth caused the Dow to fall more than 1,000 points, or 2.6%, while the broader S&P 500 lost 3% and the Nasdaq fell 3.4%.5,6

As disconcerting as these pullbacks felt at the time, stocks returned to record highs by September. An important lesson from this year is that stocks can, and often do, go down. It’s also critical to know that, on average, stocks have corrected approximately every two years, and that correction typically lasts a few months. Corrections, which are declines of between 10% and 20% from a recent high, can occur for a variety of reasons, including when unexpected news shakes investors’ confidence. Selling investments during a downturn may lock in your losses and lower your potential long-term returns.7

Don’t Fight the Fed

The past year has reinforced the influence the Federal Reserve has over the markets and investor psychology. The Fed held rates steady for much of 2024. It wasn’t until the September meeting that they made an adjustment. Markets reacted to every Fed meeting and Chairman Jerome Powell press conference. With inflation down from its highs (but not yet at the Fed’s 2% target) and employment softening, but not cratering, the Fed may have orchestrated the oft-talked-about “soft landing” for the economy. The lesson learned for next year is to pay attention to what the Fed is doing and remember the old Wall Street saying, “Don’t fight the Fed.”

Markets Shift Focus in an Instant

We all know that stocks can be volatile, but we only seem to care when they are volatile on the downside. Those 24 hours of angst between August 5 and 6, when the Dow dropped more than 1,000 points due in part to angst over the Bank of Japan boosting interest rates at a time when investors were borrowing the yen on the cheap to buy higher-risk stocks and derivatives. I doubt many of us had “Bank of Japan” on our radar, but market psychology can shift abruptly from “it’s all good” to “the sky is falling” without much justification. Focus can flip from concerns over an overheating economy to fears of a job-crushing recession on a dime. One lesson we hope you take away from 2024 is not to let emotions control your investment decisions. A solid financial strategy should be designed to withstand short-term market moves and keep you on track toward your long-term financial goals.9

Artificial Intelligence (AI) is Here to Stay

AI has been a major market story in 2023 and 2024 and shows no signs of slowing. While AI has been advancing for decades, innovations in machine learning have found exciting and extraordinary new use cases in areas from healthcare to manufacturing. One popular chatbot jump-started the current AI interest, reaching 100 million monthly active users just two months after its launch, making it the fastest-growing consumer application in history.8

AI is being seen as the most innovative technology of the 21st century and has the potential to both enhance and disrupt major industries. Innovations in electricity and personal computers unleashed investment booms of as much as 2% of U.S. GDP as the technologies were adopted into the broader economy. Now, investment in artificial intelligence is ramping up quickly and could eventually have an even bigger impact on GDP, according to Goldman Sachs Economics Research.10

The AI lesson to take away from 2024 is that AI is not just focused on a handful of companies. Company interest in AI has already increased rapidly, with more than 16% of enterprises in the Russell 3000 mentioning the technology on earnings calls, up from less than 1% in 2016.10

Asset Allocation is Essential

Asset allocation is an approach to help manage, but not eliminate, investment risk in the event that security prices decline. The strategy involves spreading your investments across a wide range of assets to spread the risk associated with concentrating too heavily on any single investment. Simply put, diversification is the “don’t keep all your eggs in one basket” approach to portfolio construction.

Asset allocation is more than choosing a single investment, like one that is based on the S&P 500 stock index. One of the more significant and concerning trends in recent years has been the rise of market-cap-weighted indexes, which has led to increased concentration in just a few dominant stocks, mostly in the technology sector. Due to their outsized market capitalizations, these stocks, dubbed “The Magnificent 7,” may make up a disproportionate part of some investor portfolios. Another lesson from 2024 is that the downside can be significant when heavily concentrated stocks pull back simultaneously.11

Emergency Preparedness is Always Critical

The year 2024 has shown us that unexpected economic downturns or crises can impact investors without warning. You should consider having an emergency fund to cover living expenses so you aren’t forced to make short-term decisions that could impact your long-term goals. You should also work with a financial professional to discuss risk management strategies that can keep you moving toward your goals.

Prepare for What You Can, Don’t Overreact to What You Can’t

With the presidential election now behind us, potential tax and regulation policy transitions remain. Politically speaking, implementing policy goals and regulations is more challenging than making pledges. Be ready to shift strategies for you, your loved ones, and your heirs if necessary. In other areas, there may be little you can do other than to try not to overreact to what comes down from Washington. Working with financial, tax, and estate professionals can help you navigate what may happen in 2025 and beyond.

Applying Lessons and Looking Forward to 2025

As we reflect on the financial landscape of 2024, it’s clear that the market continues to evolve in response to global events, technological advancements, and economic policies. The lessons from this past year underscore the importance of maintaining a balanced, long-term perspective with your personal finances.

To summarize the key takeaways from 2024:

Market volatility remains a constant, emphasizing the need for diversified portfolios.

The Federal Reserve’s decisions continue to impact market dynamics.

Emerging technologies, particularly AI, are reshaping industries and potentially creating new investment opportunities.

Global events can rapidly shift market focus, reinforcing the value of a well-structured financial strategy.

Looking ahead to 2025, we anticipate continued evolution in the financial sector and are committed to staying on top of these changes and providing you with timely insights and guidance. Our team is dedicated to helping you navigate the complexities of the financial world and working towards your long-term goals.

We will continue to monitor key economic indicators, policy changes, and market trends, sharing our analysis through our regular blog posts and communications. Our aim is to provide you with the information and support you need to make informed financial decisions in the coming year and beyond.

Remember, personal finance is a collaborative effort. While we provide the insights, your personal goals and circumstances are at the heart of every strategy we develop. We encourage you to reach out to us with any questions or concerns as we move into 2025.

Thank you for your continued trust in our team. We look forward to guiding you through another year of financial opportunities and challenges.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

3. Yahoo.com, October 31, 2024. The S&P 500 Composite Index is an unmanaged group of securities considered to be representative of the stock market in general. Past performance does not guarantee future results. Individuals cannot invest directly in an index. The return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost.

4. Yahoo.com, October 31, 2024. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

With election day over, many are reflecting on what this new leadership might mean for their financial future and the country. While elections can stir strong emotions, it’s important to remember that, historically, markets have been influenced more by economic fundamentals than by which party is in power.

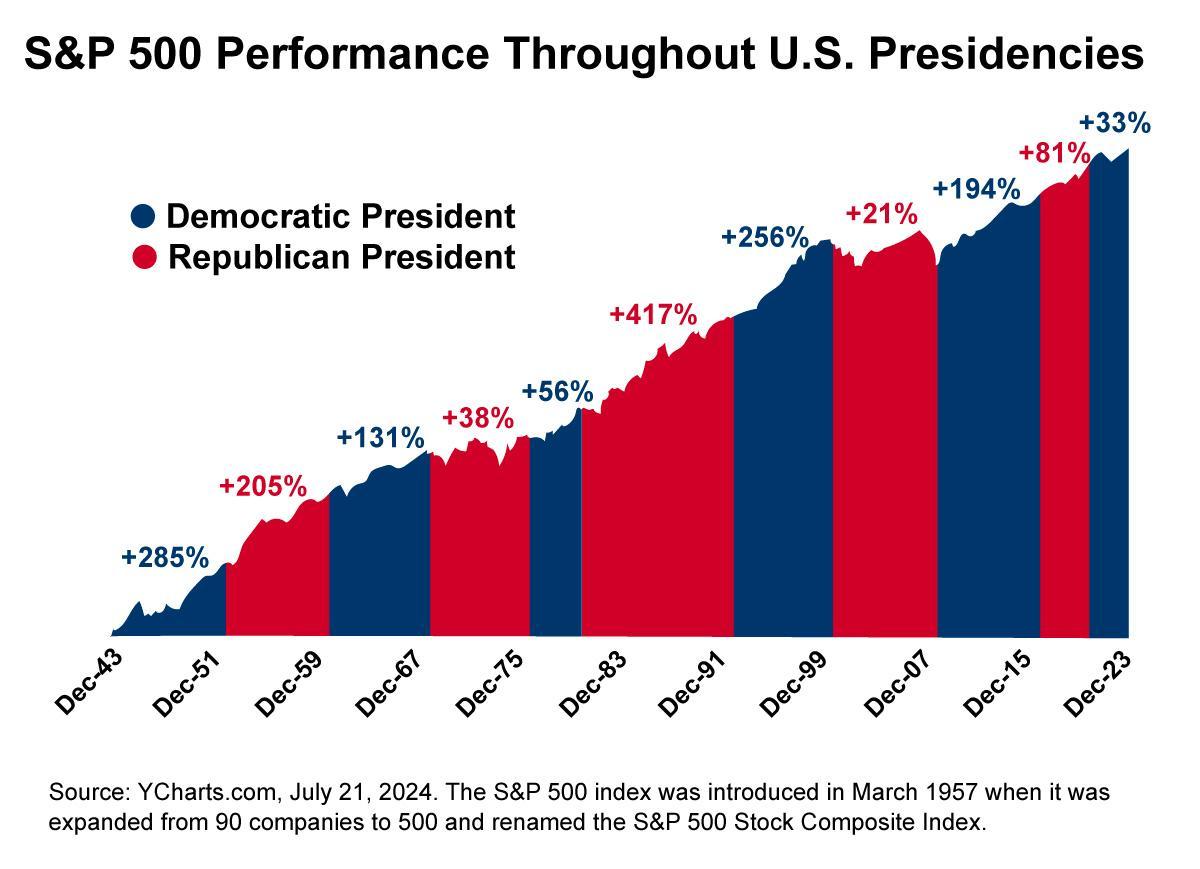

As this chart shows, while the stock market has fluctuated under presidents of both parties, the S&P 500 has trended higher over the long term, no matter who’s sitting in the Oval Office.1

Long-Term Trends: The stock market, as represented by the S&P 500, has generally trended higher over the long term, regardless of which party holds the presidency.

Company Growth: The dynamic U.S. economy has consistently produced successful companies, contributing to economic strength under various administrations.

Market Priorities: Factors like earnings growth, economic conditions, and technological advancements can have more influence on market performance than political changes.

Investor Focus: Your investment strategy should align with your goals, time horizon, and risk tolerance—not the outcome of a single election.

While elections do have consequences, it’s important to keep perspective. In the meantime, we’ll be closely monitoring how the new administration’s agenda might impact areas like tax policy, regulations, and corporate competitiveness. Market reactions to political shifts can create short-term volatility, but these fluctuations can be temporary.

As always, the key is to stay focused on your financial goals. Sudden moves in response to short-term events might be more detrimental than beneficial. We’re here to help you navigate any uncertainty while pursuing your overall financial strategy.

If you have questions about how current events could impact your investments or want to discuss your financial strategy, feel free to reach out.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

Stocks are measured by the Standard & Poor’s 500 Composite Index, an unmanaged index considered representative of the overall U.S. stock market. Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index. Stock price returns and principal values will fluctuate as market conditions change. Shares, when sold, may be worth more or less than their original cost.

We’re heading toward another contentious presidential election in the United States. If you’re on edge in this political climate, you’re not alone.

We don’t want your valid political qualms to lead you to make financial missteps. That’s why we’ve compiled four essential tips to help you maintain a level head and effectively manage your financial future in the face of political uncertainty.

1. Look at the History

Despite the month-long parade of anxiety-inducing headlines that typically precede a national election, recent history shows that elections rarely cause significant upset to financial markets.

In evaluating data from the past five presidential elections, short-term volatility does occur in the days and weeks immediately before and after the election. But those fluctuations fade quickly, and the market reverts to whatever trajectory it was already on.*

2. Enhance Your Media Literacy

In the coming months, headlines will likely try to tie every newsworthy event — big and small — into the 2024 election. While that will include financial news, it’s important to remember that small events typically don’t drive markets.

Instead, macro events move the needle. The subprime mortgage crisis sparked the Great Recession. A once-in-a-century pandemic set off economic upheaval in 2020. Be wary of headlines that try to convince you the economic world is falling off its axis because of an event that is ultimately micro in scale.

To navigate stories around the upcoming election it helps to increase your media literacy. Some sources cultivate panic or anger to drive more views, clicks, and revenue.

Use these tactics to evaluate the trustworthiness of a story:

Scrutinize the source. Does the individual or organization have the credentials to speak on the topic?

Question the melodrama. Is any emotion in the piece necessary, or is it a tactic to elicit a specific response or manipulate the reader?

Examine the tone. Look for words that are designed to provoke emotional reactions.

Consider the motive. Is the information neutral and purely informative, or is there a self-serving angle to the piece?

Check the facts. Is the piece based on facts or opinions? If information is being presented as factual, can you independently verify it with a reputable third party?

3. Keep Calm and Invest On

Advisors preach this all the time, but it bears repeating during a stressful news cycle: Staying invested is one of the most beneficial things you can do for your financial future.

The stock market has averaged a 10% rate of return over the past 50 years — a period that includes stagflation, the ’79 energy crisis, the dot-com bubble, the Great Recession, and Covid-19.** Those who have remained invested regardless of the economic ups and downs have seen their money grow thanks to compounding.

Instead of letting external economic forces influence your decision, look inward. Remaining focused on your personal long-term financial goals can help you stick to the plan you and your advisor have created.

4. Turn To Your Advisor for Support

If you’re struggling to maintain your serenity, reach out to your advisor. The economic chatter can be stressful and advisors are committed to helping you tune out the noise and remain focused.

Advisors can help you by:

Contextualizing economic headlines. Advisors spend a lot of time tracking trends and watching markets. They can fill in critical blanks when you encounter a news story that sounds scary.

Running stress tests. Advisors use technology to help us create hypothetical projections so they can better understand potential upside and downside risk in various macroeconomic scenarios. If you have a particular concern about a macro force, they can run that stress test on your portfolio and walk you through the results.

Revisiting your financial plan. Advisors are here to help you keep a level head and stay focused on what matters. They can walk through your plan together and review projections to inspire you to stay the course.

Feel free todownload this guideand share it with your friends, so they too can benefit from these strategies for navigating market uncertainty during election season.

If you’re feeling uncertain or have questions about how the current events may impact your investments, don’t hesitate to reach out. We’re here to provide guidance, offer perspective, and help you stay focused on your long-term financial goals.

Warren Street Wealth Advisors

Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.

https://warrenstreetwealth.com/wp-content/uploads/2024/10/4-Tips-for-Navigating-the-Markets-During-Election-Season-3.png10801080Warren Street Teamhttps://warrenstreetwealth.com/wp-content/uploads/2014/11/Warren_Street_logo-01.svgWarren Street Team2024-10-22 08:03:002024-11-07 15:27:584 Tips for Navigating the Markets During Election Season