How Compound Returns Work: A Guide to Growing Your Money

If you’re like most people, you need your investments to grow to achieve the life you want. Fortunately, there’s a simple yet powerful tool that can help you achieve that growth: compounding. Compounding is the process of earning returns on your past investment returns.

The Wonders of Compounding

Compounding can help your portfolio grow exponentially over time. Here’s a simplified example:

You invest $10,000 and earn a 10% return in the first year. By the end of the year, you have an additional $1,000, totaling $11,000. If you keep it invested and earn another 10% return the next year, your 10% return now produces $1,100 rather than $1,000.

The more your investments grow, the more you can reinvest for further growth.

You can pull a couple key levers to make the most of compounding. Using these strategies wisely can significantly boost your savings:

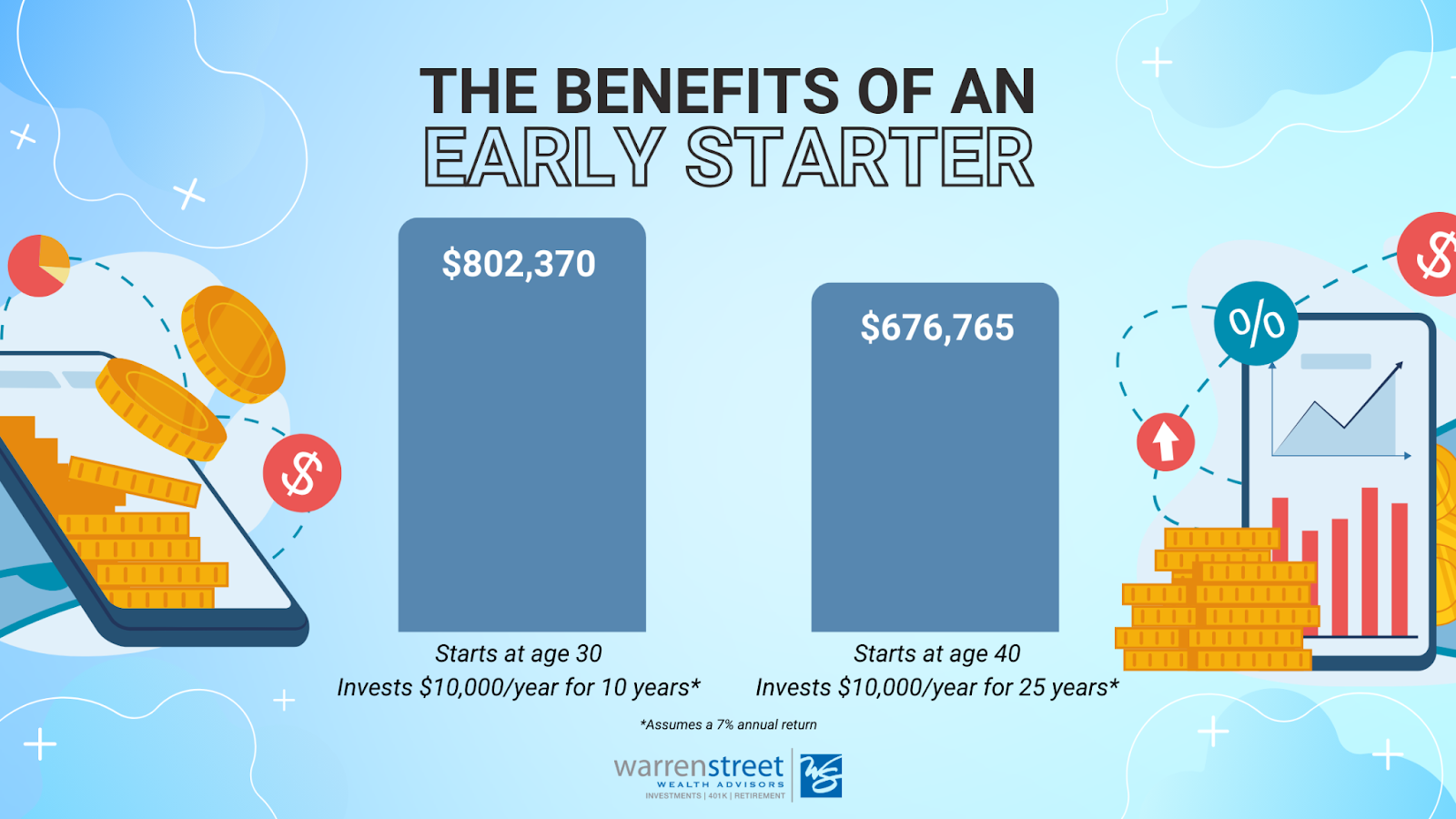

Give It Time

Time allows your investments to snowball. The longer you let your returns compound, the greater the snowball effect. Here’s an example why:

Investor 1: Starts at age 30, invests $10,000 annually for 10 years, earning a 7% annual return. They contribute a total of $100,000 and then stop adding money but let it grow.

- Portfolio value at age 65: $802,370

Investor 2: Starts at age 40, invests $10,000 annually for 25 years, earning a 7% annual return. They contribute a total of $250,000.

- Portfolio value at age 65: $676,765

Despite contributing $150,000 more, Investor 2 ends up with about $125,000 less than Investor 1. Starting early makes a huge difference.

Make the Most of Tax Advantages

Taxes can reduce compounding’s power. In a taxable account, interest, dividends, and capital gains trigger taxes that lower your annual return. Lower returns mean less money to grow the next year.

However, in tax-advantaged accounts like a 401(k), traditional IRA, or Roth IRA, you don’t pay taxes on gains while the money is in the account. This allows all your gains to keep working for you.

- Traditional 401(k) and IRA: You contribute pre-tax money, it grows tax-deferred, and withdrawals after age 59 ½ are taxed at normal income tax rates.

- Roth IRA: You contribute after-tax money, it grows tax-free, and withdrawals after age 59 ½ and a 5-year holding period are tax-free.

Control What You Can

Like most things in life, investing has many uncontrollable elements, so focus on what you can control. Start early, stay invested for the long term, and use tax-advantaged accounts to maximize compounding and work towards your long-term goals.

Bryan Cassick, MBA, CFP®

Wealth Advisor, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.