![]()

Q3 2018 – Trade Report and Market Commentary

Portfolio Changes – August 23, 2018

There was little change to the global equity allocation this quarter. Small and Mid-Cap stock exposure were modestly reduced in favor of Large Cap stocks to begin positioning for a slightly more conservative risk posture.

As the economic expansion nears the end of its historic run, we’ve reduced the allocation to credit-based strategies to protect the portfolios should an unexpected downturn arise. Multi-asset exposure was increased to provide more diversification in the bond allocation until the path ahead becomes more clear.

The allocation to Energy, Gold, and TIPS was reduced to redeploy assets into Foreign Real Estate, Infrastructure, and Natural Resources. With political uncertainty in the global landscape and stretched affordability in U.S. real estate, broadening exposure across global diversifier sectors should smooth this strategy’s performance going into the November elections and moving toward year-end.

Q3 2018 Commentary

It’s been a bumpy ride!

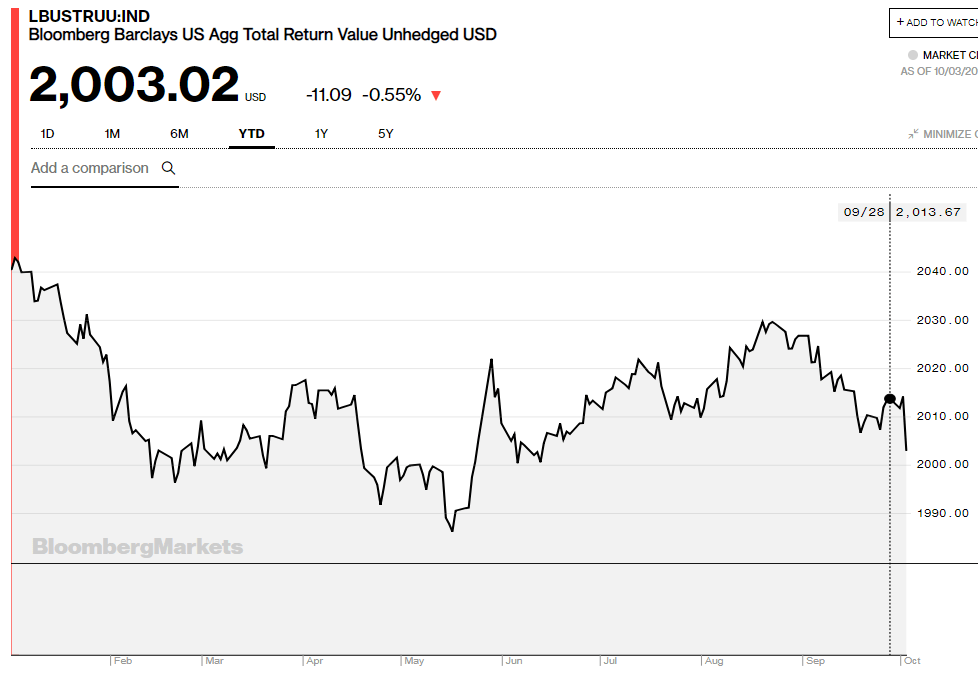

2018 has been quite a year! As you can see in the chart above, the U.S. stock market opened the year with a roar, sputtered in February, geared up in March only to stall again, and closed the first quarter down -0.76% before continuing its historical run to end with a 10.56%¹ return by September. In bumpy stock environments such as this, bonds usually act as shock absorbers to help smooth out the potholes – but not this time. The U.S. bond market as measured by the Bloomberg Barclays U.S. Aggregate bond index closed the 1st quarter with a negative return of -1.46%², even worse than the stock market. And bonds didn’t get any better as the year went on, ending the 3rd quarter down -1.60%.

Source: https://www.bloomberg.com/quote/LBUSTRUU:IND

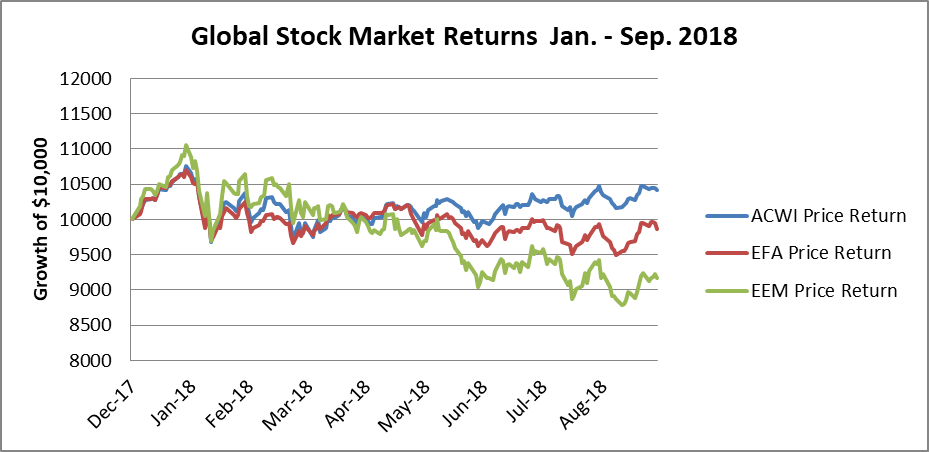

As the U.S. markets were struggling to gain momentum in the early part of the year, what about our neighbors overseas? Sorry, there’s no octane there either. The MSCI All Country World Index ETF (ticker ACWI) posted a loss of -0.54%³ for the 1st quarter despite half of the fund’s exposure coming from U.S. securities. ACWI gained ground by September with a +4.16% return year-to-date, but remained a distant second to the S&P 500. If we look at global markets excluding the U.S., the MSCI Europe, Africa, and Far East ETF (ticker EFA) lost -0.90%⁴ the 1st quarter and continued to fall behind, ending September down -4.12%. But the most exciting ride came from Emerging Markets Equity with the MSCI Emerging Markets ETF (EEM) starting strong at +2.46%⁵ for the first quarter but ending the 3rd quarter far behind the pack with a year-to-date return of -8.31%.

Source: https://finance.yahoo.com Author’s calculations

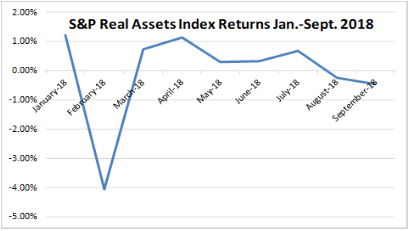

You might be wondering whether commodities and other less-correlated asset classes added fuel to the markets? Nope! The S&P 500 Real Assets index posted the worst loss of the bunch for the 1st quarter at -2.19%⁶, due in part to falling oil prices in January after a strong run in December. Oil prices have picked up speed since April, however, though with occasional pit stops along the way. The Real Assets index closed the 3rd quarter basically flat with a return of -0.49%.

Source: ttp://us.spindices.com/indices/multi-asset/sp-real-assets-total-return-index Author’s calculations

All this drag in the first quarter left us with one question – how bad is 2018 going to be?!

The speed of the U.S. stock markets relative to other developed economies isn’t surprising given our strong economic activity, corporate tax cuts, and the business-friendly policies of the Trump administration. But domestic protectionism can backfire into global markets, particularly when combined with political uncertainties in major economies such as Germany and Italy.⁷

Source: https://www.ft.com/content/41da5d38-6973-11e8-b6eb-4acfcfb08c11

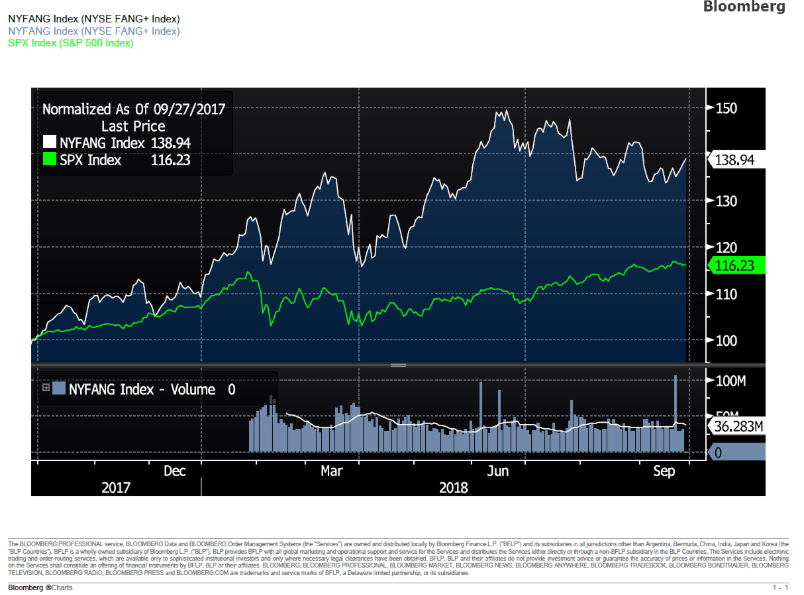

While the U.S. stock market seemed to be leaving competitors in the dust, when we looked under the hood we saw that much of the growth in the S&P 500 index was fueled by the ‘FAANGs’– Facebook, Amazon, Apple, Netflix, and Google, with the remainder of the market fading before reaching the finish line as illustrated in the graph below. Smaller companies may still have some fuel in the tank despite the overall market being expensive by some estimates.

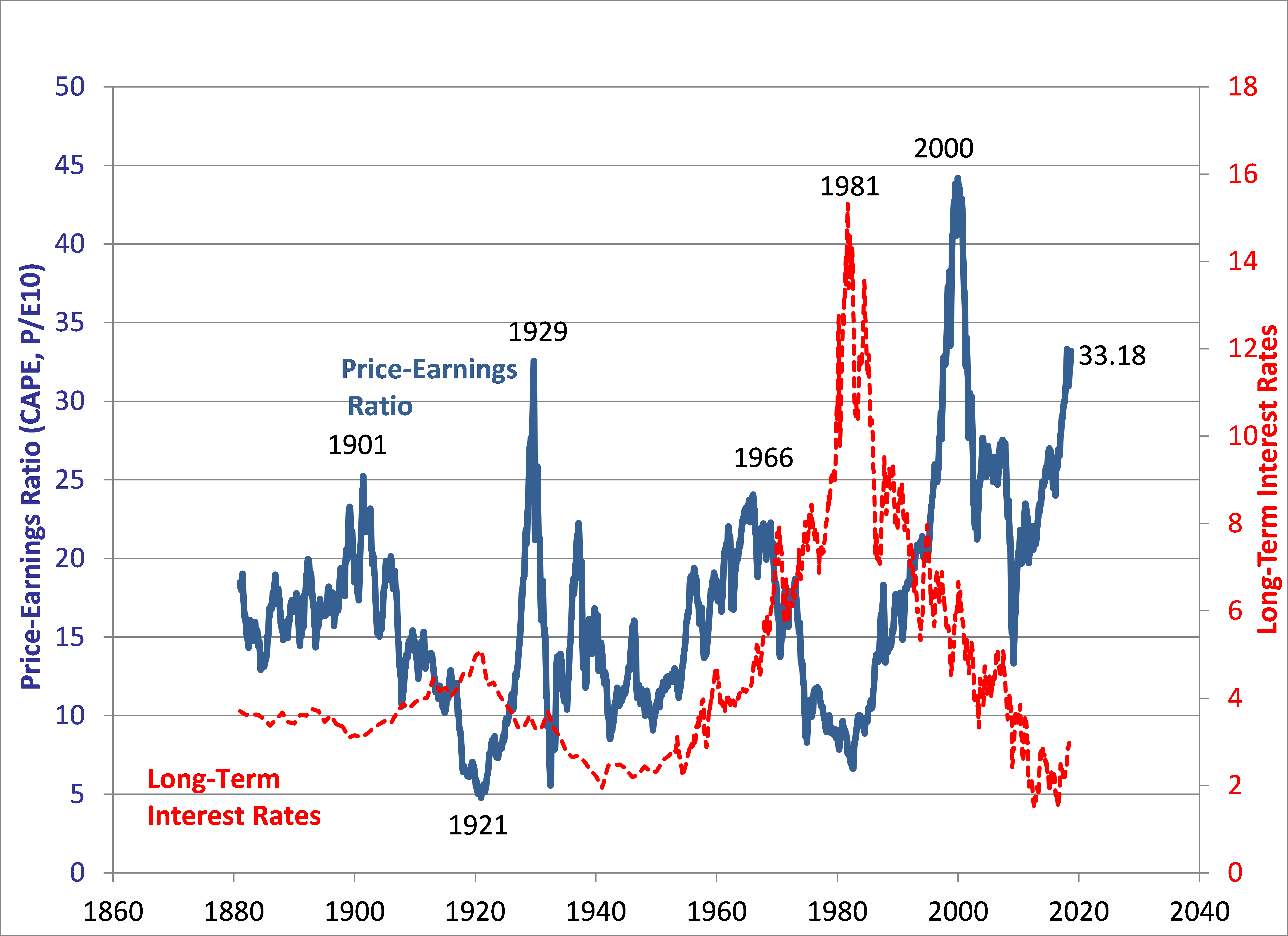

The Case-Shiller Cyclically Adjusted Price/Earnings ratio (CAPE) is often used to assess likely future returns of the U.S. stock market over long periods, such as 10 or 20 years. The blue line on the graph below indicates the current CAPE ratio is higher-than-average, implying the possibility of lower-than-average stock market returns going forward.

Source: http://www.econ.yale.edu/~shiller/data.htm as of 9/28/2018

Now that we understand the terrain a bit better, how should we navigate the rest of the year?

While Warren Street Wealth Advisors is not predicting the U.S. stock market will stall, diversification across asset classes and sectors provides investors some guardrails to protect against a possible skid. Our investment team is staying the course by maintaining an allocation to global equity markets while broadening exposure to real assets and bond market sectors.

A significant component of our global equity exposure is focused on banks, including BNP Paribas and Lloyd’s Banking Group, and automakers such as Daimler and BMW. Because of reforms put into place after the financial crisis of 2008-2009, global banks are well capitalized and regularly stress-tested to avoid insolvency should economic turbulence persist. And while the current battle of tariffs and trade has negatively impacted German automakers in particular, companies like Daimler and BMW have survived much worse challenges. Though we are comfortable with our current international position, the investment team at Warren Street Wealth Advisors is taking a deeper look at developed and emerging markets exposures across investment strategies. We believe that the current headwinds in Europe will subside, and selective exposure in emerging markets could add welcome diversification with the possibility of superior returns in the future.

As we’ve seen so far in 2018, when U.S. stock markets charge ahead, bond markets tend to lag. The U.S. bond market has been fighting the gridlock of tightening monetary policy combined with strong GDP growth, both of which point toward the possibility of rising inflation. If the bond market stays on its current course, 2018 could become one of only two times in the past 10 years when the Bloomberg Barclays U.S. Aggregate Bond Index posts a negative annual return.

Source: http://performance.morningstar.com/Performance/index-c/performance-return.action?t=XIUSA000MC

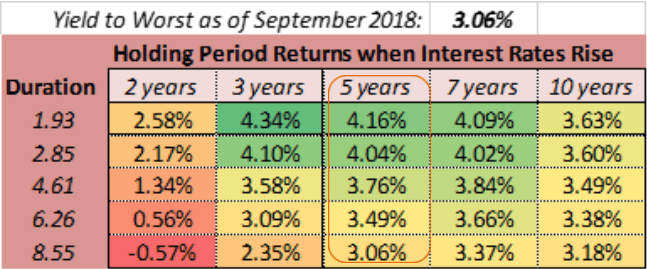

Though the transition can be painful, ultimately higher interest rates will repay investors who stay in the race long enough to benefit. The table below illustrates how rising interest rates impact bond returns over time.⁸ If an investor stays the course for at least 5 years, all but the most interest-sensitive investment strategies should be better off than before the rate hikes.

But given that we can’t predict with certainty what’s around the next turn, we will continue to broaden exposure in less-correlated assets classes such as real estate and natural resources to provide a smoother ride for our clients.

So, what should you do to ride out the rest the year? Buckle your seatbelt and keep your hands inside the car at all times as the investment team at Warren Street Wealth Advisors has both hands on the wheel and our heads on a swivel as we race toward an exciting finish for 2018!

——————————————————————————————

Quiz Question: How many references to cars and racing can you find in the commentary?

A. 0-10

B. 11-20

C. 21-30

D. More than 30

Marcia Clark, MBA, CFA

Marcia Clark, MBA, CFA

Senior Research Analyst

Warren Street Wealth Advisors

Warren Street Wealth Advisors, a Registered Investment Advisor. The information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional advisor should be consulted before implementing any of the strategies or options presented. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss.

-

- http://performance.morningstar.com/funds/etf/total-returns.action?t=SPY®ion=USA&culture=en_

- http://performance.morningstar.com/Performance/index-c/performance-return.action?t=XIUSA000MC

- http://performance.morningstar.com/funds/etf/total-returns.action?t=ACWI price return

- http://performance.morningstar.com/funds/etf/total-returns.action?t=EFA price return

- http://performance.morningstar.com/funds/etf/total-returns.action?t=EEM price return

- http://us.spindices.com/indices/multi-asset/sp-real-assets-total-return-index

- https://www.ft.com/content/41da5d38-6973-11e8-b6eb-4acfcfb08c11

- The table depicts the annualized total return for the holding period indicated at the top of each column. Total return calculation is: [Prior value x (1+((beginning yield/12)-(duration x change in yield)) / Prior value]^(1/holding period)

Estimated returns in the table begin with the yield-to-worst of the Bloomberg Barclays U.S. Aggregate Bond Index as of September 28, 2018. We then increase interest rates by 0.25% in December 2018 and again in March, June, September, and December of 2019. These higher rates depress bond prices initially but reinvesting coupon payments at the higher yield eventually overcomes the earlier loss.