Actions to Take in a Market Downturn

Market downturns are an expected part of investing, but they can be painful and nerve-racking nonetheless. Investors often want to take action or make changes during these times. Predicting which way the market will move in the short term is nearly impossible; short-term changes usually work against us. Below you will find some actions that you can take during a market pullback that will often yield positive results.

Here are some potential actions to take during a market downturn:

- Continue to invest. Market downturns may provide an opportunity to buy into the market at a lower entry point. Consider increasing your savings and investing rate during this time.

- Tax loss harvesting. Loss harvesting is a way to turn lemons into lemonade. Loss harvesting allows investors to take advantage of their portfolio losses by realizing the losses and using them to reduce taxable income.

- Hold off on large withdrawals. Wait until the market recovers to make larger-than-usual portfolio withdrawals.

- Overall financial planning check-up. Now is a good time to take care of any financial planning items that have been lingering on your to-do list. Check your beneficiaries, review your estate documents, and review your insurance coverage. The market is not in your control, so take a minute to review and manage anything that is in your control.

- Check your 401(k) allocation and contributions. Make sure you are on track to receive any company matching contributions.

- Roth conversions. Roth conversions are case-by-case specific, but generally speaking periods of market volatility may create opportunities for Roth conversions. The idea is to convert funds from a Regular to a Roth IRA while your account value is low, decreasing the amount of tax generated from the conversion. Assuming the market eventually recovers, your newly converted Roth dollars will appreciate tax free (assuming you meet all the other criteria necessary for Roth tax treatment). This scenario works best when you are in a low tax bracket and have the cash to pay tax on the conversion.

- Rebalance your portfolio. Rebalancing your portfolio often forces you to sell high and buy low, even during periods of market downturn. By rebalancing during volatility, you are selling the funds that have held up better (typically bonds and other diversifiers), and reinvesting into the areas that have pulled back. This forces you to “buy the dip.” If/when the weaker parts of your portfolio recover, you participate more fully.

- Reevaluate your risk level. Market corrections provide an opportunity to increase your risk level (i.e., your stock exposure) and to take advantage of lower stock prices. Typically these periods are not a good time to lower risk by selling stocks unless your goals and/or investment time horizon has changed.

Usually the best action is no action. If you’re not in a position to save more, sticking to your long-term allocation and plan is likely the best way to weather market turbulence. Market corrections will continue to happen over the course of your investing life. While overall the long term trend tends to be upward, corrections will typically happen every few years. During turbulent times, emotional decision-making often works against us.

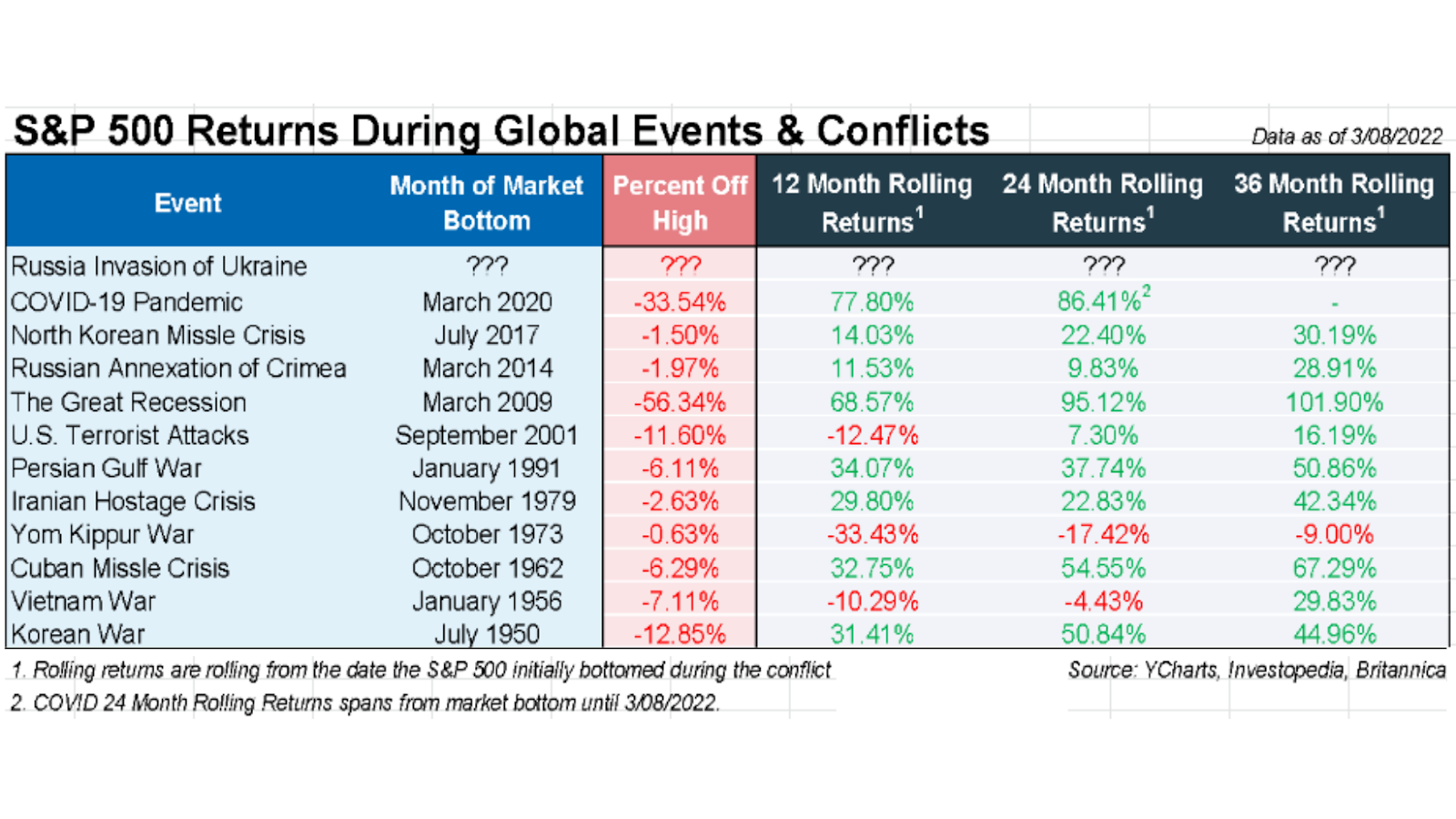

The chart below illustrates how the S&P 500 has performed after a variety of global events and conflicts since 1950. You can see that in most cases, the market has had strong performance in the years following a crisis.

Please feel free to reach out to us if you have any questions. If you would like to speak with one of our advisors for complimentary portfolio review, you can schedule a consultation here.

Emily Balmages, CFP®, CRTP

Director of Financial Planning, Warren Street Wealth Advisors

Investment Advisor Representative, Warren Street Wealth Advisors, LLC., a Registered Investment Advisor

The information presented here represents opinions and is not meant as personal or actionable advice to any individual, corporation, or other entity. Any investments discussed carry unique risks and should be carefully considered and reviewed by you and your financial professional. Nothing in this document is a solicitation to buy or sell any securities, or an attempt to furnish personal investment advice. Warren Street Wealth Advisors may own securities referenced in this document. Due to the static nature of content, securities held may change over time and current trades may be contrary to outdated publications. Form ADV available upon request 714-876-6200.