The Retirement Handbook: Southern California Edison Edition

The Retirement Handbook: Southern California Edison Edition

Retirement is just around the corner, and you should be excited. But some of us have many questions and concerns about retirement causing us to feel more nervous than anything else.

We understand these feelings.

At Warren Street Wealth Advisors, we’ve helped hundreds of Southern California Edison retirees navigate this crucial time. In the process, we’ve learned about SCE’s retirement and employee benefits programs inside and out. We’ve put together our Southern California Edison Retirement Handbook as a guide for you.

1. Have a Plan

Nothing else on this list matters if you don’t have a personalized financial plan.

A personalized financial plan is the roadmap to your comfortable retirement. You can know your benefits inside-out and be clever about taxes and investments, but if you don’t have a roadmap for navigating your retirement, you’ll never feel confident along the way.

2. Seriously, Have a Plan

Having a plan is essential for any major life transition, and navigating your retirement with wisdom and confidence is certainly part of a major life transition!

OK, let’s move on…

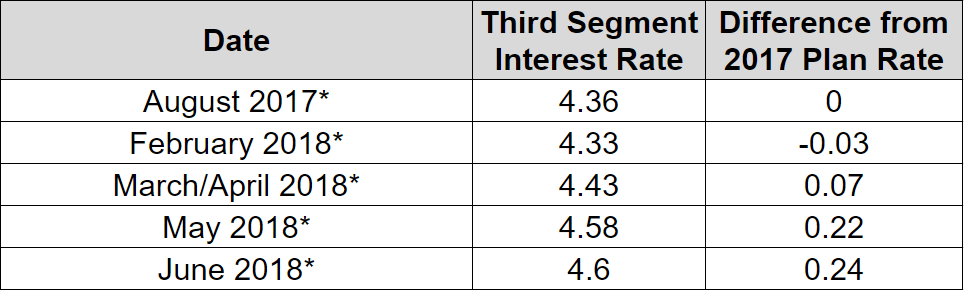

3. Plan to Retire Around October

If you are grandfathered into the old SCE pension formula, then you should plan to retire around October. This will allow you to choose which year’s plan rate provides you with the better benefit (Learn more HERE).

It’s important to know that you have a choice, review your options, then decide whether to retire on December 1st or January 1st – whichever projection pays the higher benefit.

If you are not grandfathered, retiring at the end of the year is still a great idea, especially if you need to take a large distribution pre-59 ½.

You are not forced to take your final distribution at retirement. You can wait until January 1st, request your final distribution, and then take a direct payment to avoid penalties using the “55 rule” if you are 55 years or older. This will also allow you to defer the income tax to the following year’s tax return.

This might seem complicated, but it’s a normal process for our clients who retired early.

4. Retire After 55 But Before 59 1/2 Without Paying Penalties.

Here’s a scenario we see all the time: you’re 57. You want to retire. You don’t want to wait until 59 ½ to do it. But you know that there’s a 10% federal tax penalty and a 2.5% California state tax penalty if you take the money out of your IRA before 59 ½. So are you stuck? Nope.

There are a lot of moving parts to this process, but we can take advantage of IRS rules like 72(t) distributions or the previously mentioned “55 rule” to ensure our clients do everything possible to avoid paying penalties.

5. Take Advantage of Your Medical Subsidy

Did you know that you are eligible for a retiree medical subsidy? The most common subsidies are 50% and 85%. When you retire, Edison will pay either 50% or 85% of your current medical insurance premium as a “continuation benefit” in retirement. Simply put, what you pay today is what you’ll pay in retirement. Of course, this is as long as you reach your required benefit milestone.

Unsure what your benefit is? You can call EIX Benefits to ask what benefit you have and at what age you’ll receive it. Call 866-693-4947.

Medical expenses are a huge cost for retirees, knowing what portion is covered by your employer is critical to planning a successful retirement.

6. Say “Goodbye” to Credit Card Debt

If you have credit card debt, then it’s time for a plan, a budget, and some hard work.

Debt can be intimidating, but you can pay it off! One of our favorite things is a client freeing themselves from the stress of mounting credit card debt. You may just need some help and a plan.

7. If Eligible, Plan for Your Sick Time Payout

Your sick time payout can be a significant amount and can be a boost into retirement, especially if you’re retiring early. You can run a pension projection online that will include a calculation of your accrued sick time payout . This will provide you more clarity about how much money you’ll start with when you retire, and it could help bridge the gap to 59 ½.

8. Build and Keep a Budget

We get it: it’s no fun to build a budget, but it’s the first step to discovering what retirement will look like.

Get rid of the stuff you don’t use and keep what makes you happy! Not sure where to start? No problem, use our Retirement Tool Kit to make it easy.

9. Build Up 6-Months Worth of Emergency Savings

We’re always optimistic about the future, but sometimes life takes surprising and difficult turns. Wise financial planning means being prepared for those situations.

We recommend that you save at least 6-months worth of living expenses in case of an emergency. Need $4,000/month to live? Then have around $24,000 in savings & checking. Now, you’re prepared for the ups and downs that life can throw at us at any age.

10. Weigh All Your Options on Social Security

There is a lot of information out there about what to do with Social Security. Let me boil it all down: you don’t have to take it at 62! When we build a financial plan for a client, we calculate all options for optimizing Social Security.

It’s ultimately your decision, we suggest weighing your options before committing to collecting the 25-30% reduced benefit at age 62.

11. Invest for Retirement

Max out your 401(k). Diversify your investments. Consider hiring a pro.

Make sure your investments are retirement ready. Do you have too much cash? Too much of a single stock? If you have ESOP shares, are you getting the most tax efficiency with them?

If you’re unsure, then having a team on your side can help you get the most out of your plan and make sure your investments match your goals and objectives.

12. Have a Plan

You didn’t think this was going to end without one more reminder, did you? If you’re not sure where to start with your financial plan, that’s OK: we can help.

Schedule a free consultation to talk through your finances and take the first step toward building a confident retirement.

Joe Occhipinti

Joe Occhipinti